- Medical Devices

- Eye Health Products Market

Eye Health Products Market Size, Share, and Growth Forecast 2026 - 2033

Eye Health Products Market by Products (Eye Drops/Solutions, Eye Gel/Ointment, Tablet, Capsule, Softgels, Others), Ingredient (Lutein & Zeaxanthin, Fatty Acids, Flavonoids, Vitamins, Others), Indication (Dry Eye Syndrome, Age-Related Macular Degeneration (AMD), Cataracts, Glaucoma, Diabetic Retinopathy, Others), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), by Regional Analysis, 2026 - 2033

Eye Health Products Market Size and Trend Analysis

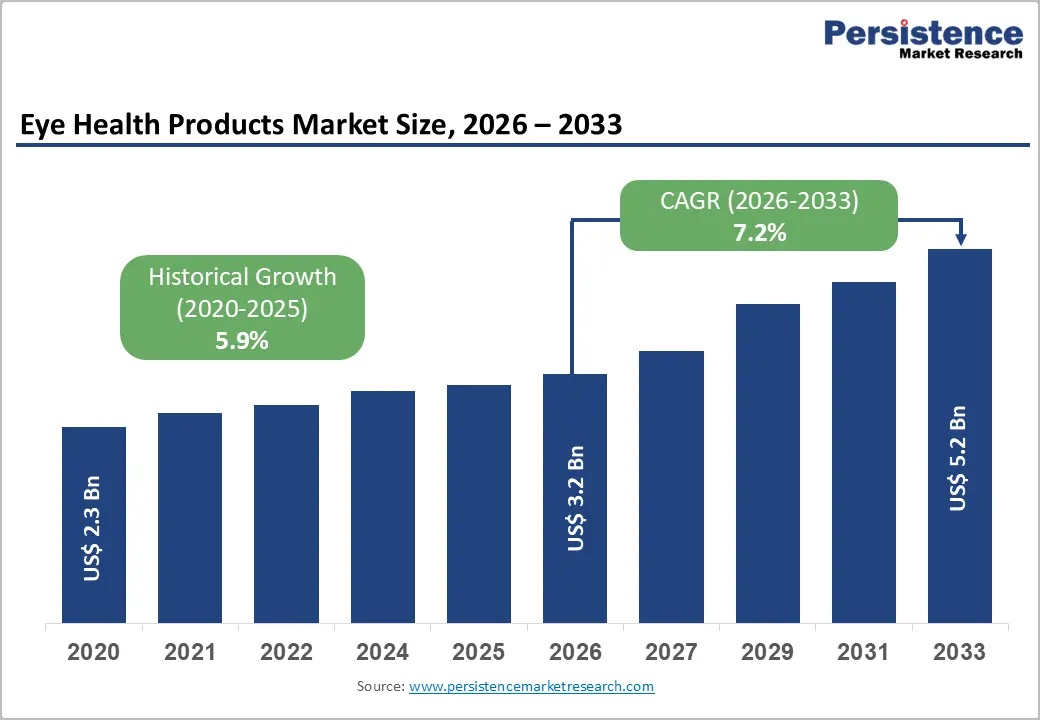

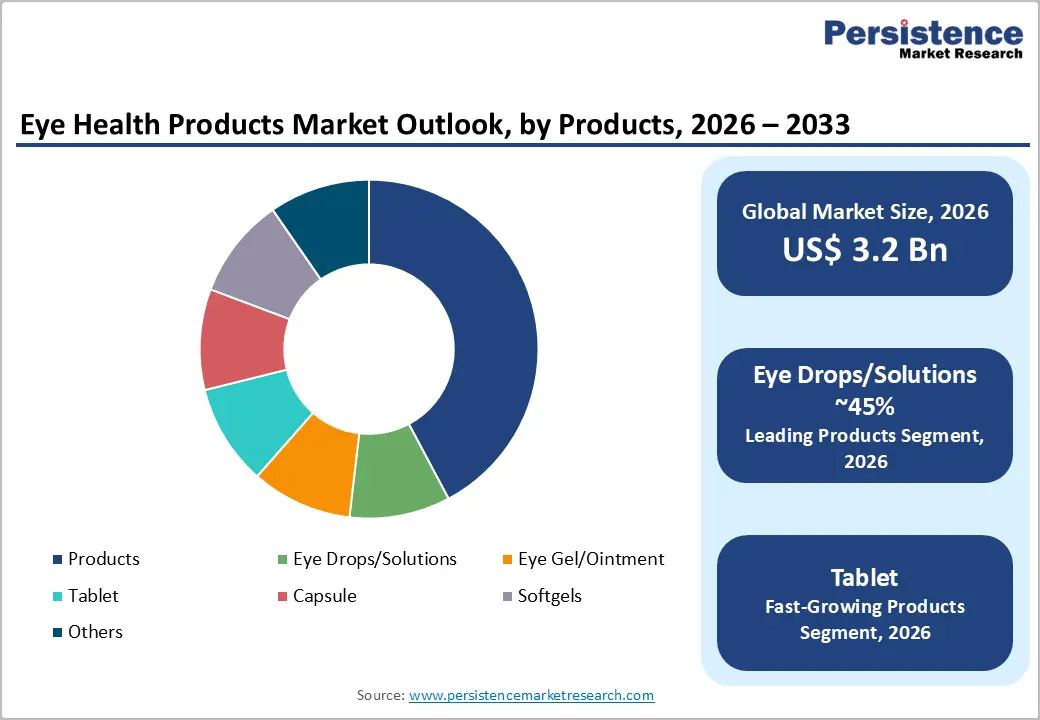

The global eye health products market size is expected to be valued at US$ 3.2 billion in 2026 and projected to reach US$ 5.2 billion by 2033, growing at a CAGR of 7.2% between 2026 and 2033. Market growth is primarily driven by the escalating global burden of ocular diseases, an aging world population, and surging consumer awareness of preventive eye nutrition.

The World Health Organization (WHO) estimates that at least 2.2 billion people worldwide have a vision impairment or blindness, and at least one billion of these cases could have been prevented or have yet to be addressed.

Rapid growth in screen time across all age groups, amplified by remote working and digital learning trends, is accelerating the incidence of dry eye syndrome and digital eye strain, directly expanding demand for eye drops, lubricating solutions, and nutritional supplement products. Concurrently, favorable reimbursement frameworks and expanding retail and online pharmacy distribution are improving product accessibility globally.

Key Industry Highlights:

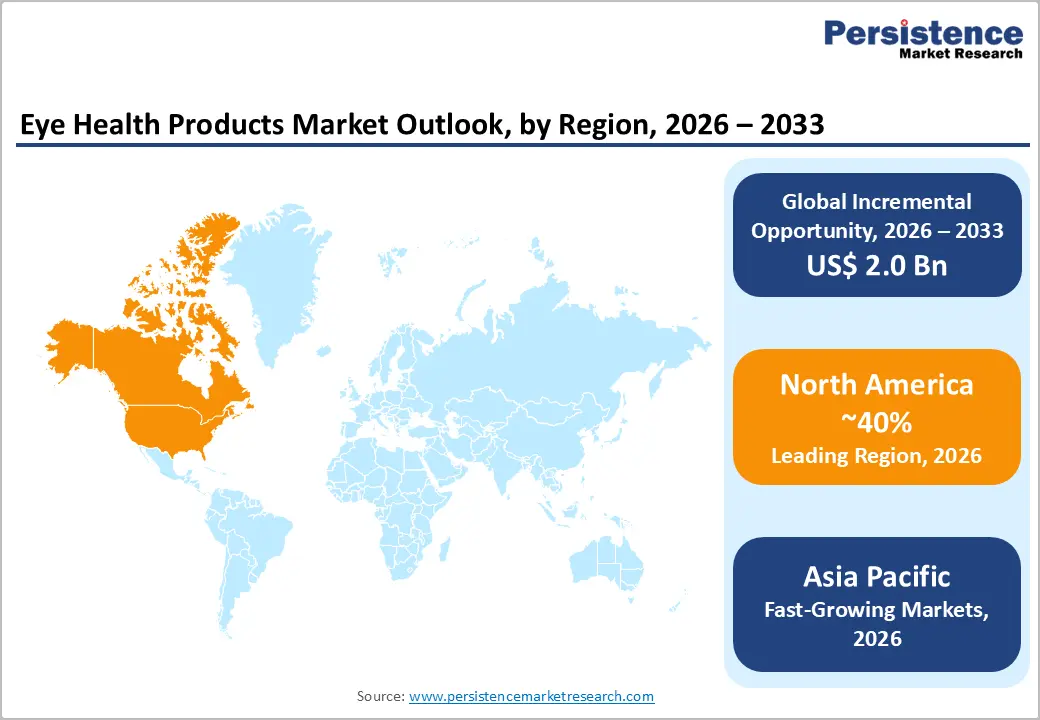

- Leading Region: North America holds 40% of the global eye health products market share in 2026, driven by high AMD prevalence, strong AAO supplement recommendation rates, aging baby boomers, and an expansive OTC retail pharmacy and e-commerce distribution infrastructure.

- Fastest Growing Region: Asia Pacific is forecast to register the highest regional CAGR through 2033, fueled by China's 600 million myopic population, India's diabetic retinopathy burden, rising middle-class health spending, and rapidly expanding online health retail channels.

- Dominant Product Segment: Eye Drops/Solutions hold 45% product type share in 2026, driven by broad AAO recommendation as first-line dry eye therapy and continuous innovation in preservative-free, lipid-based, and hyaluronic acid lubricant formulations.

- Fast-Growing Segment: Oral tablet and softgel supplements are forecast to register the highest product format CAGR, driven by NEI AREDS2 clinical validation, growing ophthalmologist recommendations, and expanding consumer self-purchase through online and retail pharmacy channels.

- Key Opportunity: Online pharmacy is the fastest-growing distribution channel, presenting brands with DTC subscription, personalized recommendation, and repeat-purchase revenue opportunities that are reshaping the competitive landscape for eye health supplement manufacturers globally.

Market Dynamics

Drivers - Rising Demand for Novel Eye Health Supplement Ingredients

Lutein, Zeaxanthin, Vitamin A, and Vitamin C collectively account for approximately 60% of all eye health products in 2024. To enhance differentiation, companies are actively developing novel ingredient formulations that provide additional benefits for eye health.

Emerging ingredients such as astaxanthin, blueberries, omega-3 long-chain PUFAs, DHA, and genistein are being integrated into new product offerings. However, clinical validation remains limited, as companies seldom conduct comprehensive studies to verify efficacy. Cyanotech Corporation has undertaken multiple clinical trials to assess the impact of astaxanthin on eye health, reinforcing its commitment to scientific validation. Additionally, in 2024, blueberry anthocyanins gained regulatory approval as a new raw food material due to their antioxidant properties, which may help reduce eye fatigue and improve vision.

Expanding Distribution Channels for Greater Market Accessibility

To drive sales and expand market reach, companies are leveraging multiple distribution channels. Traditional retail outlets, including supermarkets, hypermarkets, pharmacies, and specialty stores, continue to dominate vitamin and mineral-based product sales. However, with rising internet penetration and the growing convenience of online shopping, e-commerce has witnessed substantial growth, a trend expected to persist.

To enhance product accessibility, manufacturers are increasingly partnering with hypermarkets and digital retail platforms to strengthen their distribution networks. For instance, Valeant Pharmaceuticals collaborated with major retail chains such as Costco, Kroger, Walmart, Walgreens, Rite Aid, and Amazon to extend the availability of its eye health products across multiple sales channels.

Restraints - Regulatory Complexity and Stringent Approval Requirements for Eye Drops

During the projected period, the eye health products market expansion is predicted to be hampered by stringent regulations surrounding manufacturing, product safety, and efficacy claims. Regional differences in regulations exist. Some regions do not permit any efficacy or health benefit claims, whereas others do.

Therefore, in order to avoid regulatory actions, manufacturers need to be careful about the claims they choose to make on labels and while promoting their products. n May 2022, the FDA conducted a regulatory check on certain products of Golden Lab LLC. After the review, the FDA sent a warning letter to the company, stating that its claims about various formulations and eye health supplements were considered drug claims.

During an inspection of the company's manufacturing facility, products were found to be contaminated due to improper storage conditions that did not comply with current good manufacturing practice (cGMP) for nutritional supplements. The violations included the inability to ensure the products' purity, strength, and composition, as well as inadequate documentation regarding manufacturing and batch control.

Product recalls and directives from regulatory authorities across different regions, including summons, can render products unmarketable. Consequently, such recalls are expected to hinder market growth.

In December 2024, Alcon Laboratories voluntarily recalled a lot of its Systane Lubricant Eye Drops Ultra PF due to potential fungal contamination. This action was taken after a consumer reported foreign material in a sealed vial, identified as fungal in nature. Although no adverse events were reported, the recall underscores the critical importance of stringent manufacturing practices to ensure product safety.

Opportunities - Oral Tablet and Softgel Supplements Poised for Accelerated Growth Amid Preventive Health Trends

Oral eye health supplements tablets, capsules, and softgels are forecast to be the fastest-growing product format in the eye health products market, driven by the preventive health and wellness mega-trend and the strong clinical evidence base established by the National Eye Institute's (NEI) AREDS2 study, which demonstrated that specific antioxidant and mineral supplements reduce the risk of advanced AMD progression by 25%.

The global dietary supplement market sustained expansion, growing ophthalmologist recommendation rates for AREDS2-formulated products, and increasing consumer self-management of eye health through e-commerce and retail pharmacy channels are collectively driving this segment. Companies such as Bausch + Lomb (PreserVision), The Nature's Bounty Co., and Vitabiotics Ltd. (Visionace) are well-positioned to capture this growth with clinically validated formulations.

Online Pharmacy Channel Expansion: Unlocking New Consumer Access and Revenue Streams

Online pharmacies represent the fastest-growing distribution channel for eye health products, driven by post-pandemic acceleration of e-commerce health purchasing, consumer convenience preferences, and the ability of digital platforms to provide product education, subscription models, and personalized supplement recommendations. The National Association of Boards of Pharmacy (NABP) reported a substantial surge in verified online pharmacy usage in the U.S. following 2020.

Platforms including Amazon Health, Walmart Health, and specialized health e-tailers are expanding eye health product assortments significantly. Brand owners investing in digital-first distribution strategies, direct-to-consumer subscription services, and SEO-optimized product content are capturing disproportionate share of this high-growth channel particularly for repeat-purchase nutritional supplement products where consumer loyalty and auto-replenishment models generate predictable recurring revenue.

Category-wise Analysis

Products Insights

Eye Drops/Solutions dominate the product type category with an estimated 45% share in 2026. Eye drops are the primary therapeutic and symptomatic relief product for a wide range of ocular conditions, including dry eye syndrome, allergic conjunctivitis, and glaucoma, making them the most frequently purchased and clinically recommended eye health product category.

The American Academy of Ophthalmology (AAO) guidelines recommend artificial tear eye drops as first-line therapy for mild-to-moderate dry eye disease. Rapid innovation in preservative-free single-dose unit formats, lipid-containing emulsion drops, and next-generation hyaluronic acid-based lubricants is expanding the product tier and price-point range. Market leaders, including Alcon Inc. (Systane) and Bausch + Lomb (Biotrue, Soothe) command strong brand equity within this dominant segment.

Distribution Channel Insights

Retail Pharmacies constitute the dominant distribution channel, accounting for ~48% of eye health product revenue in 2025. The established OTC infrastructure of retail pharmacy chains, including CVS Health, Walgreens, and Boots in the UK, provides unmatched consumer accessibility, pharmacist recommendation touchpoints, and brand visibility for eye drops, supplements, and protective eyewear products.

Retail pharmacies also benefit from loyalty programs, in-store consultation services, and adjacency to optician practices that drive eye health supplement impulse and recommendation purchases. Their role as the primary first-contact channel for self-managed dry eye, allergy, and nutritional supplement products sustains retail pharmacy's commanding channel leadership.

Regional Insights

North America Eye Health Products Market Trends and Insights

North America leads the global eye health products market with ~40% share in 2026, supported by high healthcare spending, strong consumer awareness of preventive eye nutrition, well-established OTC supplement retail infrastructure, and broad ophthalmologist recommendation of AREDS2-formulated products. The region's aging baby boomer population and high digital device penetration sustain consistently robust demand growth.

U.S. Eye Health Products Market Size

The U.S. accounts for ~87% of the North American market in 2025. High AMD prevalence with over 11 million affected Americans per the AAO, combined with high per-capita supplement spending, dominant retail pharmacy chains, and expanding online health platforms, are key demand drivers sustaining U.S. market leadership.

Europe Eye Health Products Market Trends and Insights

Europe is the second-largest regional market, characterized by aging demographics, government-supported eye health screening programs, and strong herbal and nutritional supplement traditions in Germany and France. The European Public Health Alliance (EPHA) has called for greater emphasis on preventive eye care, and rising awareness of blue-light-induced retinal stress is expanding demand for lutein-enriched supplements across the region.

Germany Eye Health Products Market Size

Germany holds ~23% of the European eye health products market in 2026. Germany's strong nutraceutical and OTC pharmaceutical culture, aging population, and high optician and ophthalmologist density drive consistent demand for both lutein supplement formulations and preservative-free eye drop products through hospital pharmacies, optical retailers, and DM/Rossmann drugstore chains.

UK Eye Health Products Market Size

The UK represents ~18% of the European market in 2026. High awareness of AMD risk among aging NHS patient populations, broad availability of Vitabiotics Visionace and Bausch + Lomb PreserVision through Boots and online channels, and increasing optician recommendations of eye supplements are key drivers of UK market growth.

France Eye Health Products Market Size

France accounts for ~15% of the European eye health products market in 2026. The French pharmacy-centric healthcare model with over 22,000 community pharmacies providing health product counseling and strong consumer openness to dietary supplements for eye health, is sustaining demand for lutein, zeaxanthin, and omega-3 formulations across both urban and rural consumer segments.

Asia Pacific Eye Health Products Market Trends and Insights

Asia Pacific is the fastest-growing regional market for eye health products, driven by the world's largest and most rapidly expanding diabetic and aging populations, exceptionally high myopia prevalence, with China reporting over 600 million myopic individuals per the Chinese Ophthalmological Society and increasing middle-class health spending on preventive ocular nutrition across the region.

India Eye Health Products Market Size

India holds ~17% of the Asia Pacific eye health products market in 2026. India's 72 million diabetic patients (per the IDF) and growing diabetic retinopathy burden, rising optician and ophthalmologist penetration in tier-2 cities, and expanding e-commerce supplement distribution via Flipkart Health+ and Netmeds are driving accelerating market growth.

Japan Eye Health Products Market Size

Japan represents ~21% of the Asia Pacific market in 2026. Japan’s highly aged population established functional food and supplement culture under the Foods with Function Claims (FFC) framework, and high consumer demand for premium lutein-based supplements targeting macular health is a key factor. Japanese ophthalmologists actively recommend AREDS2-equivalent formulations, supporting consistent clinical channel demand.

Competitive Landscape

The global eye health products market exhibits a moderately fragmented competitive landscape, with multinational consumer health and pharmaceutical companies, including Alcon Inc., Bausch + Lomb, and The Nature's Bounty Co., holding significant shares alongside specialist nutraceutical companies such as ZeaVision LLC, Vitabiotics Ltd., and Nordic Naturals. Key competitive strategies include clinical study investment to support health claims, premium preservative-free product innovation, sustainability-focused packaging, and digital-first DTC e-commerce expansion.

Differentiation is achieved through ingredient sourcing provenance (e.g., FloraGLO-branded lutein), clinical evidence depth, and ophthalmologist endorsement. Private-label supplement proliferation in online channels is intensifying price competition in the standard supplement segment.

Key Developments

- In May 2025, Alcon announced that the U.S. FDA approved TRYPTYR® 0.003% for treating signs and symptoms of Dry Eye Disease. Formerly known as AR-15512, TRYPTYR is a first-in-class TRPM8 receptor agonist that stimulates corneal sensory nerves to rapidly enhance natural tear production.

- In October 2024, SCOPE Health Inc. acquired EYETAMINS, a provider of eye health supplements. This strategic acquisition allows SCOPE Health to broaden its range of eyecare products, integrating EYETAMINS' innovative supplements into its portfolio to enhance patients' vision and overall eye health.

- In April 2023, Sun Pharmaceutical Industries introduced CEQUA in India, targeting patients with Dry Eye Disease (DED) accompanied by inflammation. CEQUA utilizes nano micellar (NCELL) technology, marking it as the first treatment of its kind in the Indian market.

Companies Covered in Eye Health Products Market

- The Nature's Bounty Co.

- Amway International

- Bausch + Lomb

- Nutrivein

- ZeaVision LLC

- Kemin Industries, Inc.

- EyeScience

- NutraChamps

- Vitabiotics Ltd.

- Herbalife International of America, Inc.

- Nature Made (Pharmavite LLC)

- Nordic Naturals

- Puritan’s Pride

- Alcon Inc.

- Others

Frequently Asked Questions

The global eye health products market is expected to be valued at US$ 3.2 billion in 2026.

The global eye health products market is driven by rising eye disorders, increasing awareness regarding eye care, and demand for vision supplements drive market growth.

North America is projected to hold the largest share of the industry in 2025.

Key opportunities include growing demand for oral eye supplements and expanding online pharmacy channels supporting personalized recommendations and repeat purchases.

Bausch & Lomb Incorporated, Amway International, The Nature's Bounty Co, Vitabiotics Ltd, ZeaVision LLC Company among others are a few key players.