- Medical Devices

- EEG Devices Market

EEG Devices Market Size, Share, and Growth Forecast 2026 - 2033

EEG Devices Market by Product Type (21 Channel, 25 Channel, 32 Channel, 40 Channel, 8 Channel, Multi-channel), by Modality (Portable Devices, Standalone/Fixed Devices), End-user (Diagnostic Centers, Hospitals, Ambulatory Surgical Centers, Others), and Regional Analysis, 2026 - 2033

EEG Devices Market Size and Trend Analysis

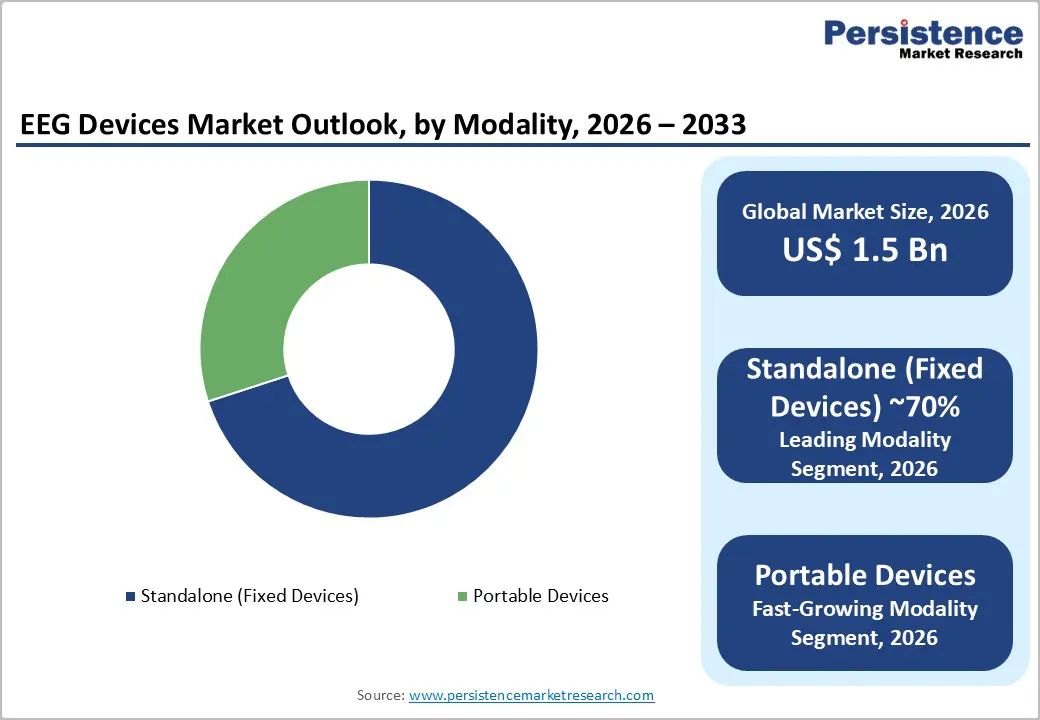

The global EEG devices market size is expected to be valued at US$ 1.5 billion in 2026 and projected to reach US$ 2.5 billion by 2033, growing at a CAGR of 7.2% between 2026 and 2033.

EEG devices emphasize technologies used for recording and monitoring the brain’s electrical activity for diagnosing neurological disorders such as epilepsy, sleep disorders, brain tumors, stroke, and neurodegenerative diseases.

Electroencephalography (EEG) devices are widely used in hospitals, diagnostic centers, research institutes, and ambulatory care settings due to their non-invasive nature and high diagnostic value. Rising prevalence of neurological conditions, increasing geriatric population, and growing awareness of early brain disorder diagnosis are driving market growth. Technological advancements such as portable, wireless, and AI-integrated EEG systems are improving accessibility and efficiency. Expanding neuroscience research, government funding initiatives, and the adoption of home-based monitoring solutions further support the global demand for EEG devices.

Key Industry Highlights:

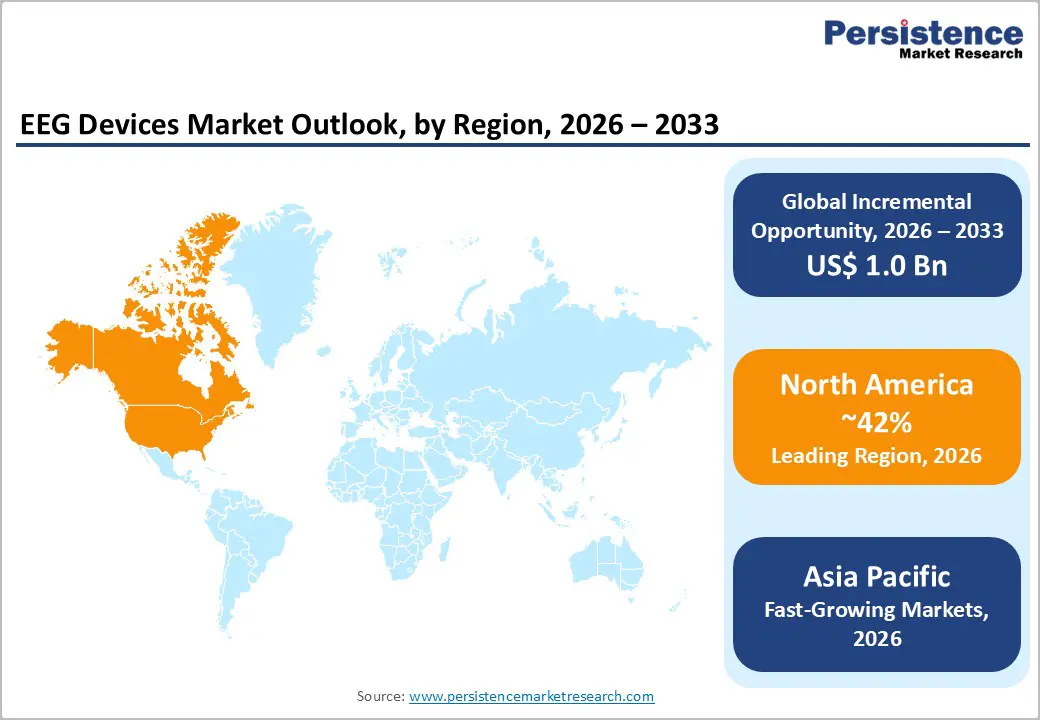

- Leading Region - North America holds ~42% of the global market share in 2026, driven by robust NIH BRAIN Initiative research funding, comprehensive CMS reimbursement for diagnostic EEG, and the U.S.'s position as the global hub for portable and AI-integrated EEG innovation.

- Fastest Growing Region - Asia Pacific is the fastest-growing region, fueled by China's Healthy China 2030 neurological care investments, India's 12 million epilepsy patients, rapid hospital neurology infrastructure expansion, and NMPA and CDSCO device approval acceleration across key markets.

- Dominant Segment -Standalone devices lead the Modality category with ~70% market share in 2026, entrenched by hospital EMU adoption, long-term video-EEG monitoring applications, and NICE- and CMS-aligned reimbursement frameworks for inpatient neurological assessment.

- Fastest Growing Segment - Portable EEG Devices are the fastest-growing modality, driven by FDA-cleared dry-electrode systems, ambulatory epilepsy monitoring adoption endorsed by the American Epilepsy Society, and telehealth-integrated neurological consultation workflows expanding beyond hospital boundaries.

- Key Market Opportunity - The NIH BRAIN Initiative (USD 500M+) and EU Horizon Europe neuroscience funding, combined with BCI commercialization, are creating high-value R&D-driven procurement demand for advanced EEG platforms beyond traditional clinical diagnostics.

Market Dynamics

Drivers - Rising Global Prevalence of Epilepsy and Neurological Disorders Fuelling EEG Demand

The escalating global burden of epilepsy, sleep disorders, and neurodegenerative conditions is the primary structural driver of EEG device demand. The WHO reports that ~50 million people globally have epilepsy, with nearly 80% living in low- and middle-income countries where EEG access remains significantly underserved representing a substantial untapped market opportunity. The International League Against Epilepsy (ILAE) underscores EEG as the gold-standard diagnostic tool for epilepsy classification and seizure monitoring, ensuring its indispensable role in neurology practice.

Beyond epilepsy, the American Sleep Association estimates that 50-70 million U.S. adults suffer from sleep disorders requiring polysomnography incorporating EEG, while Alzheimer's disease affecting over 55 million people globally per the Alzheimer's Disease International is driving research-grade EEG adoption for cognitive decline monitoring.

Technological Advancements in Portable and Wireless EEG Systems

Continuous innovation in portable, wireless, and dry-electrode EEG systems is significantly expanding the clinical and research addressable market. Next-generation portable EEG devices eliminate the traditional requirement for conductive gel and stationary recording setups, enabling ambulatory monitoring, point-of-care testing, and home-based neurological assessments. The U.S. Food and Drug Administration (FDA) has cleared multiple portable EEG platforms under its 510(k) pathway in recent years, validating their clinical-grade performance.

Integration of artificial intelligence (AI) and machine learning algorithms for automated seizure detection and brainwave pattern classification is substantially enhancing diagnostic accuracy and clinical workflow efficiency. Academic institutions, including programs funded by the National Institutes of Health (NIH), are actively deploying wearable EEG in longitudinal neuroscience studies, further validating the technology and accelerating commercial adoption across clinical and research end-users.

Restraints - High Cost of Advanced EEG Systems and Skilled Operator Dependency

Advanced multi-channel EEG systems particularly high-density 64-channel to 256-channel research-grade platforms can cost between USD 15,000 to over USD 150,000 per unit, creating significant procurement barriers for diagnostic centers and hospitals in lower-middle-income markets. Beyond capital expenditure, EEG interpretation requires highly trained neurologists and neurophysiology technicians a specialized workforce that is acutely scarce in many developing regions.

The World Federation of Neurology (WFN) highlights a critical shortage of neurologists in low-income countries, with some nations recording fewer than 1 neurologist per million population, directly constraining the clinical deployment and utilization of EEG equipment in these markets.

Opportunities - Portable EEG Devices: Capturing the Fastest-Growing Segment Through Ambulatory and Home Monitoring

Portable EEG devices represent the fastest-growing product modality, driven by expanding clinical applications in ambulatory epilepsy monitoring, telehealth integrated neurological assessments, and home-based sleep disorder diagnostics. The American Epilepsy Society (AES) increasingly endorses ambulatory EEG as a cost-effective alternative to inpatient video-EEG monitoring for certain seizure classification workflows, opening a significant volume opportunity.

The post-pandemic acceleration of telehealth adoption with the U.S. Department of Health and Human Services (HHS) documenting sustained telehealth utilization growth is enabling remote neurological consultation workflows where portable EEG data is transmitted to specialists for review. Companies developing FDA-cleared, dry-electrode portable EEG systems with cloud-connected AI analysis platforms are positioned to disrupt traditional EEG paradigms and access a far larger patient population outside hospital settings.

Neuroscience Research Funding and Brain-Computer Interface Applications Driving Innovation

Unprecedented government and private investment in neuroscience research is creating significant downstream demand for advanced EEG platforms. The U.S. BRAIN Initiative funded with over USD 500 million by the NIH since its 2013 launch has catalyzed development of high-density EEG systems for mapping neural circuitry with unprecedented resolution. The European Union's Horizon Europe program continues to fund brain research under its EUR 95.5 billion framework, with neuroscience as a priority domain.

Simultaneously, the emerging brain-computer interface (BCI) sector attracting commercial investment from companies including Neuralink and Synchron is elevating EEG's strategic importance as a non-invasive neural measurement tool. These converging investment streams are accelerating product innovation, expanding research procurement budgets, and elevating EEG platforms into high-growth scientific instrumentation applications beyond traditional clinical diagnostics.

Category-wise Insights

Product Type Insights

The 32-Channel EEG system leads the product type category, accounting for ~27% of total market share in 2026. The 32-channel configuration occupies the optimal clinical sweet spot between diagnostic comprehensiveness and operational practicality, providing sufficient spatial resolution for reliable seizure focus localization, epilepsy classification, and sleep stage analysis without the prohibitive cost and technical complexity of ultra-high-density systems. Leading neurology departments, epilepsy monitoring units, and clinical research centers globally have standardized on 32-channel platforms as their primary EEG workhorses.

The International Federation of Clinical Neurophysiology (IFCN) guidelines reference multi-electrode configurations as the standard for comprehensive EEG diagnostics. Major manufacturers, including Nihon Kohden Corporation, Natus Medical Incorporated, and Compumedics Limited, offer well-validated 32-channel platforms with established installed bases across global hospital and diagnostic center networks.

Modality Insights

Standalone (Fixed) EEG Devices hold the leading position in the modality category with ~70% of market share in 2026. Fixed EEG systems remain the dominant clinical standard in hospital neurology departments, epilepsy monitoring units (EMUs), and established diagnostic centers, where they are deployed for comprehensive long-term video-EEG monitoring, intraoperative neurophysiology, and intensive care brain function assessment. These systems offer superior electrode coverage, signal amplification, and advanced co-registration with video monitoring capabilities that are essential for pre-surgical epilepsy evaluation protocols endorsed by the National Institute for Health and Care Excellence (NICE) in the UK and comparable bodies globally. Their integration with hospital information systems and established reimbursement frameworks for inpatient EEG procedures reinforces their institutional dominance, despite the rapid growth trajectory of portable alternatives.

End-user Insights

Hospitals represent the leading end-user segment with an estimated 52% of the global EEG devices market share in 2026. Hospitals, particularly those with dedicated neurology departments, epilepsy monitoring units, and intensive care facilities, are the primary institutional buyers and operators of EEG devices.

The WHO recommends that national healthcare systems ensure the availability of EEG services at district and referral hospital levels for epilepsy management, reinforcing institutional procurement mandates globally. Hospitals benefit from the full clinical spectrum of EEG applications, including seizure diagnosis, brain death determination, intraoperative monitoring, and neonatal neurological assessment. CMS reimbursement for both routine and prolonged hospital-based EEG monitoring supports consistent utilization in U.S. hospital settings, while equivalent frameworks in Germany, France, and Japan sustain high institutional demand in European and Asia-Pacific markets.

Regional Insights

North America EEG Devices Market Trends and Insights

North America leads the global EEG Devices market with ~42% of market share in 2026, driven by a mature neurology infrastructure, strong CMS reimbursement for diagnostic EEG procedures, and active NIH BRAIN Initiative research funding. The U.S. is the innovation hub for next-generation portable and AI-integrated EEG platforms, with growing adoption across outpatient epilepsy clinics and sleep diagnostic centers.

U.S. EEG Devices Market Size

The U.S. dominates North America, accounting for ~88% of regional revenue in 2026, equivalent to around US$ 554 million. Over 3 million EEG tests are performed annually in the U.S. per ASET - The Neurodiagnostic Society estimates, with robust reimbursement, high neurologist density, and expanding ambulatory monitoring driving consistent demand.

Europe EEG Devices Market Trends and Insights

Europe is the second-largest EEG devices market, supported by established national neurology programs, EU MDR-regulated quality standards, and comprehensive public health insurance coverage for diagnostic EEG in Germany, France, UK, and Spain. Growing investment in epilepsy centers and clinical neuroscience research under Horizon Europe is sustaining demand for both clinical and research-grade EEG platforms.

Germany EEG Devices Market Size

Germany is Europe's largest EEG devices market, valued at ~US$ 92 million in 2026, representing around 26% of European revenue. Germany's dense network of university hospitals and dedicated epilepsy centers, combined with GKV statutory insurance coverage for EEG diagnostics and strong neuroscience research institutions, underpins consistent high-volume device procurement.

UK EEG Devices Market Size

The UK accounts for ~18% of regional revenue in 2026, valued at around US$ 64 million. NHS commissioning of EEG services for epilepsy and sleep disorders, NICE clinical guidelines mandating EEG in seizure evaluation, and active academic EEG research at institutions such as UCL and King's College London support steady market demand.

France EEG Devices Market Size

France holds ~15% of the European EEG Devices market in 2026, estimated at around US$ 53 million. The Haute Autorité de Santé (HAS) recommends EEG as a mandatory diagnostic tool for epilepsy assessment under national neurological care guidelines, and France's network of SEEG-specialized epilepsy centers drives demand for high-density EEG systems.

Asia Pacific EEG Devices Market Trends and Insights

Asia Pacific is the fastest-growing EEG Devices market, propelled by expanding neurology infrastructure, rising neurological disease awareness, and growing government healthcare investment in China, India, Japan, and Southeast Asia.

China is rapidly scaling neurological diagnostics capability under its Healthy China 2030 initiative, with the National Medical Products Administration (NMPA) accelerating approvals for EEG platforms to address epilepsy a major unmet clinical need affecting an estimated 9 million people in China per published epidemiological data.

India EEG Devices Market Size

India represents a high-growth EEG market within Asia Pacific, estimated at ~US$ 28 million in 2026, accounting for around 11% of regional revenue. With ~12 million people with epilepsy, per Epilepsy India estimates one of the world's largest epilepsy populations and significant underdiagnosis rates, India presents a compelling volume expansion opportunity for affordable EEG device manufacturers.

Japan EEG Devices Market Size

Japan is Asia Pacific's largest EEG Devices market, valued at ~US$ 58 million in 2026, representing around 23% of regional revenue. Japan's advanced hospital neurology infrastructure, leadership in EEG-integrated neuroimaging research, and the Japan Epilepsy Society's clinical guidelines supporting comprehensive EEG evaluation sustain high-quality device procurement across academic medical centers and specialty hospitals.

Competitive Landscape

The global EEG devices market is moderately consolidated, with a handful of established medical device manufacturers including Nihon Kohden Corporation, Natus Medical Incorporated, and Compumedics Limited holding significant combined revenue share through strong installed base advantages and clinician familiarity. Key competitive differentiators include channel count range, electrode system design, software intelligence for automated seizure detection, and cloud connectivity.

Emerging players such as Brain Scientific Inc. are disrupting the market with low-cost portable platforms targeting underserved markets. R&D investment in AI-powered neural analytics, dry-electrode technology, and BCI-adjacent applications is a dominant strategic priority among both incumbents and new entrants.

Key Developments

- In April 2025: Nihon Kohden Corporation launched its next-generation EEG-3500 system with integrated AI-assisted seizure pattern analysis, receiving FDA 510(k) clearance and targeting expanded deployment across U.S. epilepsy monitoring units and diagnostic centers.

- In October 2024, U.S. based Natus Medical pursued FDA approval for its innovative EEG device. It uses NeuroWorks software and AI-powered seizure detection algorithms to detect non-convulsive and status epilepticus in acute care settings.

- In September 2024, Boston-based Neurable introduced MW75 Neuro smart headphones with brain-computer interface technology. It incorporates AI-powered EEG sensors for detailed brainwave data and productivity tips.

- In September 2024, U.S.-based Firefly Neuroscience partnered with Zeto to distribute FDA-cleared EEG headsets, integrating Brain Network Analytics technology for diagnosing brain conditions like epilepsy, sleep disorders, and tumors.

- In August 2024, Natus Medical Incorporated introduced autoSCORE, an AI model for automatic clinical EEG interpretation. It aims to improve clinical outcomes and care value for millions with epilepsy.

Companies Covered in EEG Devices Market

- Cardwell Laboratories Inc.

- Nihon Kohden Corporation

- Compumedics Limited

- Natus Medical Incorporated

- Neurosoft Ltd.

- Electrical Geodesics Inc.

- NeuroWave Systems Inc.

- EB Neuro S.p.A

- Brain Scientific Inc.

- Others

Frequently Asked Questions

The global market is estimated at US$ 1.5 billion in 2026.

Rising epilepsy, sleep disorders, neurodegenerative diseases, portable EEG innovation, research funding, and FDA-cleared AI platforms are driving strong global market demand.

North America leads with ~42% of global market share in 2026.

Portable EEG devices for home-based monitoring, AI-powered seizure detection platforms, and expanding brain-computer interface applications offer major high-value growth opportunities.

A few of the key players in the market are Cardwell Laboratories Inc., Nihon Kohden Corporation, and Compumedics Limited.