- Plastics, Polymers & Resins

- Conductive Plastics Market

Conductive Plastics Market Size, Share, and Growth Forecast 2026 - 2033

Conductive Plastics Market by Conductive Filler Type (Carbon-based, Metal-based, and Intrinsically conductive polymers), Material Type (Polyphenylene Sulfide (PPS), Polyamide, Polycarbonate, Polyethylene, Polypropylene, Polysulfones, PBT, and Others), Application (EMI/RFI shielding, ESD protection, Sensors & electronic components, and Battery & energy systems), by End-Use, and by Regional Analysis, 2026 - 2033

Conductive Plastics Market Size and Trend Analysis

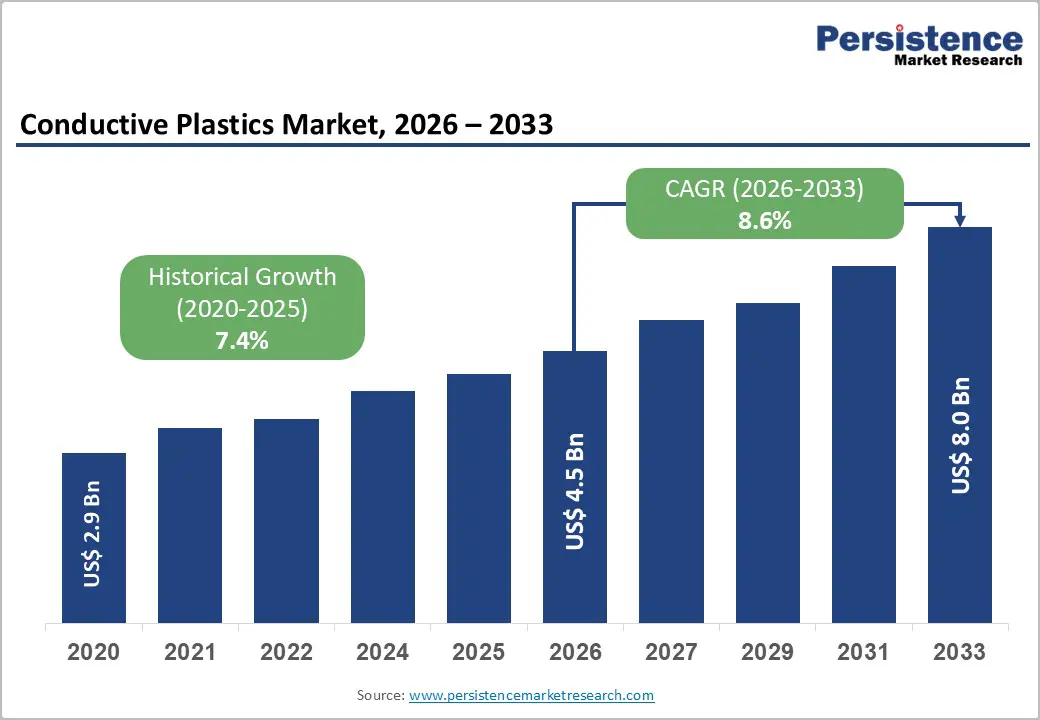

The global conductive plastics market size is likely to be valued at US$ 4.5 Billion in 2026 and is expected to reach US$ 8.0 Billion by 2033, growing at a CAGR of 8.6% during the forecast period from 2026 to 2033. This robust expansion is driven by escalating demand for lightweight, durable, and electrically conductive materials across industries, particularly as miniaturization and sustainability trends intensify in electronics, automotive, and healthcare sectors.

Key Market Highlights

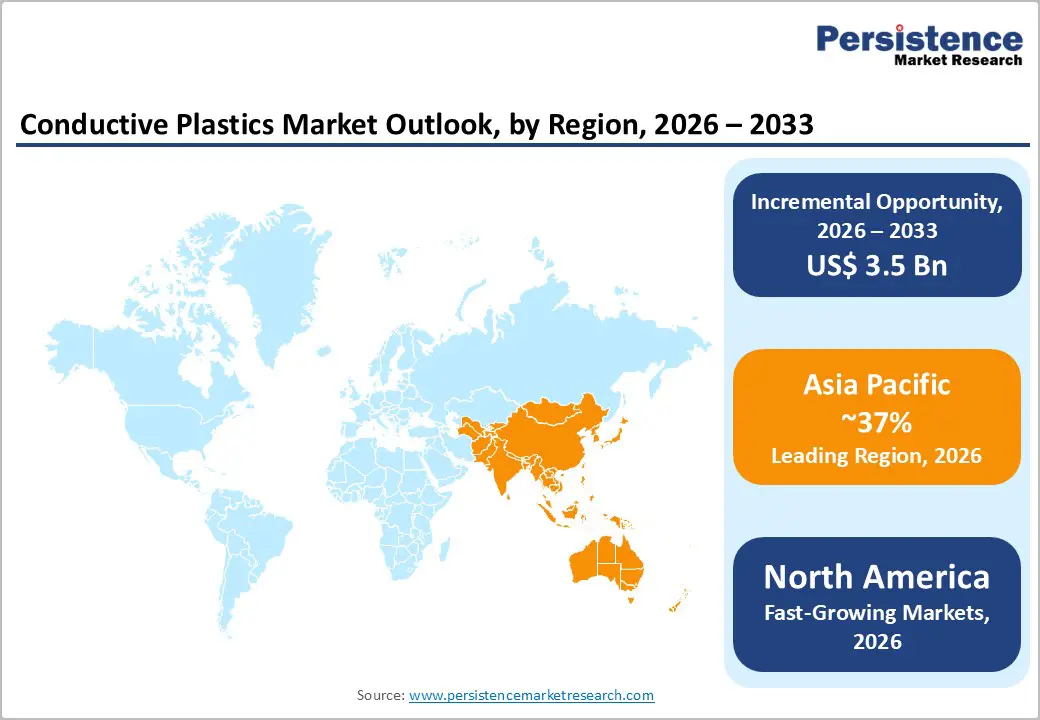

- Leading Region: Asia Pacific is the leading market, likely to account for a 37% share, due to high demand for conductive plastics, driven by strong electronics and automotive sectors.

- Fastest Growing Region: North America is the fastest growing region with a rising CAGR of 11.2%, with rapid adoption in electric vehicles and consumer electronics.

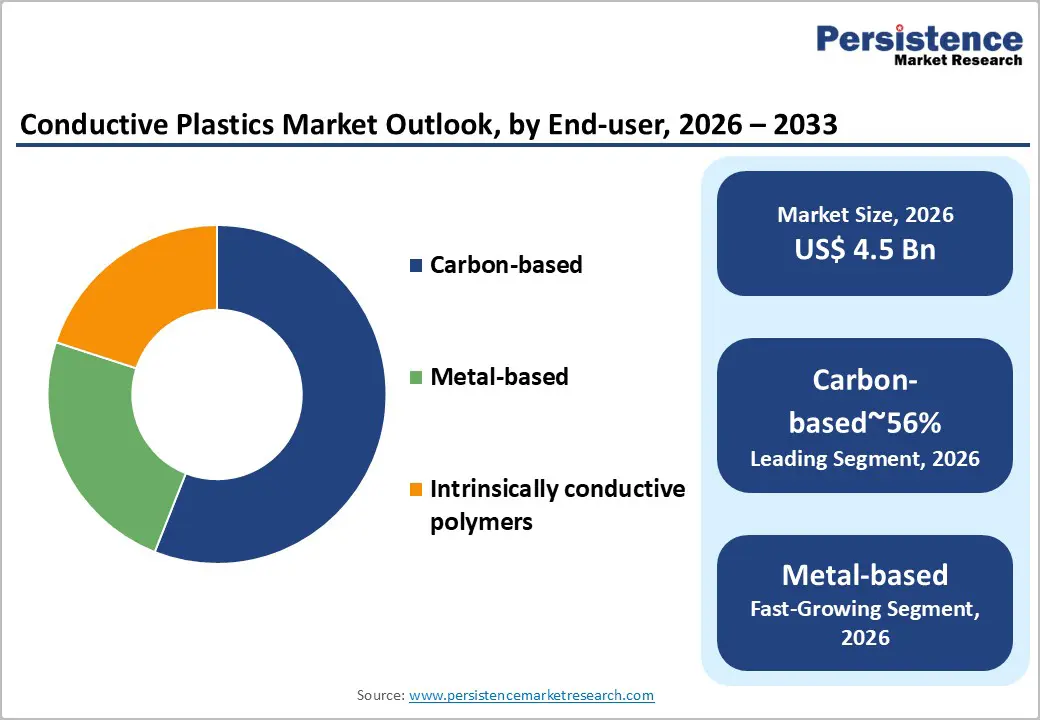

- Leading Segment: The dominant segment is carbon-based conductive filler, having 56% market share, widely used for its cost-effectiveness and performance.

- Fastest Growing Segment: Intrinsically Conductive Polymers is the fastest growing region with a rising CAGR of 9.2%, favored for emerging applications in wearable electronics.

- Key market opportunity lies in the development of sustainable and recyclable conductive plastics for automotive and electronics applications.

| Key Insights | Details |

|---|---|

|

Market Name Size (2026E) |

US$ 4.5 Billion |

|

Market Value Forecast (2033F) |

US$ 8.0 Billion |

|

Projected Growth CAGR(2026-2033) |

8.6% |

|

Historical Market Growth (2020-2025) |

7.4% |

Market Dynamics

Drivers - Miniaturization, IoT Expansion, and Advanced Polymers Accelerate Demand for High-Performance Conductive Plastics in Electronics

Rapid technological progress in electronics and electrical industries is significantly accelerating demand for conductive plastics. Key trends such as device miniaturization, flexible electronics, and the rapid expansion of the Internet of Things (IoT) are reshaping material requirements across applications. Conductive plastics offer critical advantages including lightweight properties, corrosion resistance, design flexibility, and ease of integration, making them ideal for printed circuit boards, automotive electronics, and consumer devices.

The incorporation of advanced nanomaterials such as carbon nanotubes and graphene further enhances electrical conductivity, enabling high-performance applications in medical devices, sensors, and next-generation electronics. In 2025, Merck KGaA reported strong growth in its Electronics segment, driven by rising demand for materials that support heterogeneous integration and high-density semiconductor designs. These advanced polymers play a vital role in AI processors and data-center chips, where compact size, thermal stability, and reliability are essential. This trend strongly supports the growing adoption of conductive plastics in miniaturized and high-performance electronic systems.

Automotive and Industrial Shift from Metals to Conductive Plastics Drives Lightweighting, Cost Reduction, and Design Efficiency

Industries including automotive, aerospace, and healthcare are increasingly shifting from traditional metals such as aluminum and copper to conductive plastics to improve efficiency and reduce costs. Conductive plastics offer a compelling balance of electrical performance, mechanical strength, and reduced weight, enabling manufacturers to lower overall production costs while maintaining functionality. This transition is particularly evident in the electric vehicle (EV) and autonomous vehicle segments, where lightweight materials are essential for improving driving range, energy efficiency, and system integration.

Conductive plastics are widely used in battery enclosures, wiring systems, connectors, and charging components. At CHINAPLAS 2025, SABIC showcased its BLUEHERO solutions for EV batteries, highlighting advanced thermoplastic compounds designed to enhance safety, reduce weight, and enable large-format battery components. The company also presented specialty plastics for compact electronics and autonomous-driving systems, demonstrating how OEMs are replacing metal parts with engineered plastics to optimize vehicle performance, design flexibility, and overall system efficiency.

Restraints - Stringent Environmental Regulations and Plastic Sustainability Requirements Increase Compliance Costs and Slow Market Innovation

The conductive plastics market faces increasing regulatory challenges related to environmental sustainability and plastic waste management. Governments worldwide are enforcing stricter regulations on plastic usage, disposal, and the incorporation of conductive additives due to concerns over pollution, non-biodegradability, and carbon emissions. Compliance with regulations such as the European Union’s REACH framework, along with similar policies in Asia and North America, requires manufacturers to invest heavily in environmentally compliant materials, production processes, and documentation. These regulatory demands increase operational costs and often slow down product development and commercialization.

The need to redesign formulations to meet sustainability criteria can limit material choices and delay innovation cycles. While these regulations encourage long-term environmental responsibility, they pose short-term challenges for manufacturers, particularly smaller players with limited resources. As a result, regulatory pressure remains a significant restraint affecting cost structures, development timelines, and market expansion across the global conductive plastics industry.

Performance Gaps in Thermal Stability and Conductivity Limit Conductive Plastics Adoption in High-Demand Industrial Applications

Despite their advantages, conductive plastics often face limitations when compared to traditional metals in terms of electrical conductivity, thermal resistance, and long-term durability. In high-performance or safety-critical applications, metals still outperform plastics, restricting broader adoption in demanding environments such as aerospace, heavy industrial equipment, and high-temperature systems. Achieving consistent conductivity while maintaining mechanical strength across different polymer matrices remains a technical challenge.

Variations in filler dispersion, processing conditions, and operating environments can affect performance reliability. Additionally, conductive plastics may struggle with heat dissipation in applications requiring sustained thermal stability. Overcoming these limitations requires significant investments in research and development, advanced compounding technologies, and rigorous testing. These efforts increase development costs and extend time-to-market, slowing penetration in certain end-use industries. As a result, performance trade-offs and compatibility constraints continue to act as a restraint on the widespread adoption of conductive plastics in critical applications.

Opportunity - Rapid Electric Vehicle Innovation Creates Strong Growth Opportunities for Lightweight, Conductive, and Thermally Efficient Plastics

The global transition toward electric and hybrid vehicles presents substantial growth opportunities for the conductive plastics market. EVs require lightweight, electrically functional materials for components such as battery enclosures, wiring harnesses, EMI shielding, and thermal management systems. Conductive plastics meet these requirements by offering reduced weight, reliable conductivity, and design flexibility, supporting improved vehicle efficiency and safety. Strong government incentives and regulatory support for EV adoption, particularly in Europe and China, further accelerate demand.

In December 2025, BASF introduced a next-generation solid-state battery pack in collaboration with Welion at the Guangzhou International Automobile Exhibition. The design incorporates advanced engineered plastics, including Ultramid PA cooling manifolds and Elastoflex polyurethane battery covers, achieving approximately 50% weight reduction compared to metal alternatives. These components provide electrical insulation, fire resistance, and thermal runaway protection, demonstrating how conductive and thermally conductive plastics directly enhance EV performance, safety, and driving range.

Rising Demand for Flexible, Miniaturized Consumer Electronics Boosts Adoption of Conductive Plastics and Advanced Materials

The rapid expansion of consumer electronics, including smartphones, wearables, flexible displays, and IoT devices, is creating strong demand for conductive plastics. These materials play a critical role in electromagnetic interference shielding, static dissipation, and thermal management, all of which are essential for modern electronic devices. Trends toward thinner, lighter, and more ergonomic products further support the adoption of conductive plastics over conventional materials. Flexible and foldable devices, in particular, require materials that combine conductivity with mechanical flexibility.

In 2025, Merck KGaA continues to lead innovation in this space, highlighting strong growth in its Electronics business during Capital Markets Day 2025. The company emphasized rising demand for advanced materials supporting heterogeneous integration and high-performance semiconductors. Merck’s low-temperature Plasma Enhanced Atomic Layer Deposition (ALD) barrier and encapsulation solutions enable OLED displays that are significantly thinner and more efficient. These innovations are essential for next-generation consumer electronics requiring lightweight, flexible, and reliable conductive materials.

Category-wise Analysis

Conductive Filler Type Insights

Carbon-based fillers dominate the conductive plastics market, accounting for approximately 56% of total market share. Materials such as carbon black, carbon fibers, and carbon nanotubes are widely used due to their excellent electrical conductivity, cost-effectiveness, and compatibility with a wide range of polymer matrices. These fillers are commonly incorporated into plastics used for antistatic packaging, EMI shielding, automotive components, and electronic housings. Carbon-based fillers also offer processing flexibility, allowing manufacturers to tailor conductivity levels according to application requirements.

Their established supply chains and proven performance make them the preferred choice across multiple industries. In addition, ongoing advancements in nanocarbon technologies continue to enhance conductivity and material efficiency, further reinforcing the dominance of this segment. As demand grows for lightweight, electrically functional materials in electronics, automotive, and industrial applications, carbon-based conductive fillers are expected to maintain their strong position in the global conductive plastics market.

Material Type Insights

Polyphenylene Sulfide (PPS) leads the conductive plastics market by material type, holding approximately 40% of the total market share. PPS is highly valued for its exceptional thermal stability, electrical insulation properties, chemical resistance, and mechanical strength. These characteristics make it particularly suitable for demanding applications in automotive, electrical, and industrial environments. PPS-based conductive plastics are widely used in connectors, sensors, motor components, and battery systems, where consistent performance under high temperatures and harsh conditions is critical.

The material also offers excellent dimensional stability and resistance to automotive fluids and chemicals, further enhancing its appeal. As electric vehicles and advanced electronics continue to grow, demand for high-performance materials such as PPS is increasing. Manufacturers prefer PPS due to its long service life, reliability, and ability to meet stringent regulatory and performance standards, positioning it as the dominant material choice in the conductive plastics market.

Application Insights

EMI and RFI shielding represents the largest application segment in the conductive plastics market, accounting for nearly 35% of total demand. The increasing proliferation of electronic devices, wireless communication systems, and connected technologies has significantly raised the need for effective electromagnetic interference protection. Conductive plastics are widely used to shield sensitive electronic components from signal disruption, ensuring reliable device performance.

This demand is particularly strong in consumer electronics, automotive electronics, aerospace systems, and industrial equipment. Compared to traditional metal shielding, conductive plastics offer advantages such as reduced weight, design flexibility, and easier integration into complex component geometries. Additionally, they support miniaturization trends by enabling thinner and more compact shielding solutions. As technologies such as 5G, autonomous driving, and IoT continue to expand, the need for reliable EMI/RFI shielding will remain critical, reinforcing the dominant position of this application segment within the global conductive plastics market.

End-user Insights

The automotive and electric vehicles segment is the largest end-use for conductive plastics, accounting for approximately 30% of global market consumption. Automakers increasingly rely on conductive plastics to meet requirements for lightweighting, electrification, and advanced electronics integration. These materials are extensively used in battery systems, electronic control units, sensors, wiring components, and structural parts. The shift toward electric and autonomous vehicles has significantly increased the use of conductive materials for EMI shielding, thermal management, and electrical connectivity.

Conductive plastics help reduce vehicle weight, improve energy efficiency, and enhance overall system reliability. Additionally, their corrosion resistance and design flexibility support longer service life and improved safety. As global automotive production continues to evolve toward electric mobility and smart vehicle technologies, the automotive and EV sector is expected to remain the primary growth driver for the conductive plastics market.

Regional Insights

North America Conductive Plastics Trends

North America holds a significant share of the global conductive plastics market, driven primarily by strong demand from the U.S. automotive and electronics industries. The region benefits from advanced manufacturing capabilities, high R&D investment, and rapid adoption of innovative materials, particularly for EMI shielding and electric vehicle components. Supportive regulatory frameworks and strong intellectual property protection further encourage innovation.

In January 2025, Celanese Corporation launched a new range of thermally conductive polyamides designed for EVs and consumer electronics, offering improved heat management and electrical insulation for battery systems and power modules. Additionally, in April 2025, UBE Corporation completed its acquisition of Lanxess’s polyurethane systems business, expanding its footprint across North America and Asia. The company is also constructing a new North American manufacturing facility scheduled to begin operations in fiscal 2026, reinforcing its long-term commitment to serving growing regional demand for advanced conductive plastics.

Europe Conductive Plastics Market Trends

Europe’s conductive plastics market is strongly influenced by stringent environmental regulations and sustainability initiatives, particularly under frameworks such as REACH and the EU circular economy strategy. Countries including Germany, the UK, and France lead regional demand, supported by growth in the electrical, electronics, and automotive sectors. Manufacturers are increasingly focused on recyclable, low-carbon, and mass-balance certified materials. At K 2025 in Düsseldorf, BASF showcased its #rPlasticsJourney initiative, highlighting advanced recycling technologies such as chemical depolymerization and solvent-based recycling for end-of-life vehicles.

In September 2025, BASF’s Performance Materials division achieved REDcert² certification across all ten European production sites, enabling certified sustainable feedstock usage. These initiatives demonstrate Europe’s strong alignment with regulatory compliance and sustainability goals, positioning conductive plastics as essential enablers for eco-friendly electronic and automotive applications across the region.

Asia Pacific Conductive Plastics Market Trends

Asia Pacific dominates the global conductive plastics market with approximately 37% share, driven by rapid industrialization and strong growth in electronics and automotive manufacturing. China, Japan, and India are key contributors, supported by government incentives for electric vehicles, electronics production, and sustainable materials. China’s extensive electronics manufacturing ecosystem and India’s expanding EV market are major demand drivers.

In early 2025, BASF began commercial production of loopamid, a recycled polyamide solution, at its Caojing facility in Shanghai, targeting lightweight electronics, wearables, and flexible displays. UBE Corporation also strengthened its regional presence following its acquisition of Lanxess’s polyurethane systems business, expanding operations across Shanghai and Jiangsu. Meanwhile, Mitsubishi Chemical has developed advanced conductive polymer compounds for 5G, EMI shielding, and flexible electronics. These developments highlight Asia Pacific’s leadership in innovation, scale, and adoption of conductive plastics.

Competitive Landscape

Companies are also focusing on customized solutions tailored to automotive, electronics, and EV applications to strengthen customer relationships. Emerging technologies such as 3D printing, additive manufacturing, and nanocomposite engineering are reshaping product development and enabling new business models. Smaller innovators play a key role by introducing niche solutions and application-specific materials. Overall, competitive intensity remains strong as companies balance performance, sustainability, and cost efficiency to capture long-term growth opportunities in the global conductive plastics market.

Key Market Developments:

- In December 2024: Merck KGaA introduced a new line of conductive polymers designed to support flexible electronics, particularly targeting wearable device manufacturers seeking lightweight, bendable, and reliable conductive materials that enhance performance in wearable sensors and flexible circuitry applications.

- In September 2025: SABIC entered into a strategic collaboration with an automotive OEM to co-develop lightweight conductive plastic components tailored for next-generation electric vehicles, enabling improved weight reduction, enhanced electrical functionality, and material performance for EV structural and electronic parts.

- In March 2025: BASF announced a significant R&D investment focused on improving the sustainability and recyclability of its conductive plastic products, reinforcing its commitment to circular economy initiatives and advancing technologies that reduce environmental impact throughout the material lifecycle.

Companies Covered in Conductive Plastics Market

- UBE Corporation

- Merck KGaA

- Connect Chemical GmbH

- Nanjing Chegyi Chemical Co. Ltd.

- HefeiTNJ Chemical Industry Co. Ltd.

- Mudanjiang Fengda Chemical Corporation

- Zhonglan Industry Co. Ltd.

- Ningbo Jiasi Chemical Co. Ltd.

- Changzhou Yetai Fine Chemicals Research Institute Co. Ltd.

- Otto Chemie Pvt. Ltd.

- Richman Chemical Inc.

- Oakwood Products Inc.

- Spectrum Chemical

- Thermo Fisher Scientific Inc.

- SABIC

- BASF

- Celanese Corporation

- RTP Company

- Solvay SA

- 3M Company

- Mitsubishi Chemical

Frequently Asked Questions

The global conductive plastics market is valued at US$ 4.5 Billion in 2026 and is projected to reach US$ 8.0 Billion by 2033, growing at a CAGR of 8.6%.

Key drivers include the rise of electric vehicles, growing need for EMI/RFI shielding, and advancements in nanomaterial integration for electronics.

Polyphenylene Sulfide (PPS) is the leading material type, holding about 40% market share due to its thermal and electrical performance.

Asia Pacific leads the market, capturing 37% share, driven by electronics and automotive growth in China, Japan, and India.

The fastest growing opportunity is the development of sustainable and recyclable conductive plastics for automotive and electronics applications.