- Metalworking & Fabrication

- Computer Numerical Control (CNC) Machines Market

Computer Numerical Control (CNC) Machines Market Size, Share, and Growth Forecast 2026 - 2033

Computer Numerical Control (CNC) Machines Market by Machine Type (Lathes and Turning Machines, Milling Machines, Router Machines, Laser Cutting Machines, Waterjet Cutting Machines, Drilling Machines, Grinding Machines, Electric Discharge Machines), by Axis Type (2-Axis, 3-Axis, 4-Axis, 5-Axis, 6-Axis), by End Use Industry (Automotive, Aerospace & Defense, Construction Equipment, Power & Energy, Industrial), by Regional Analysis, 2026 - 2033

Computer Numerical Control (CNC) Machines Market Size and Trend Analysis

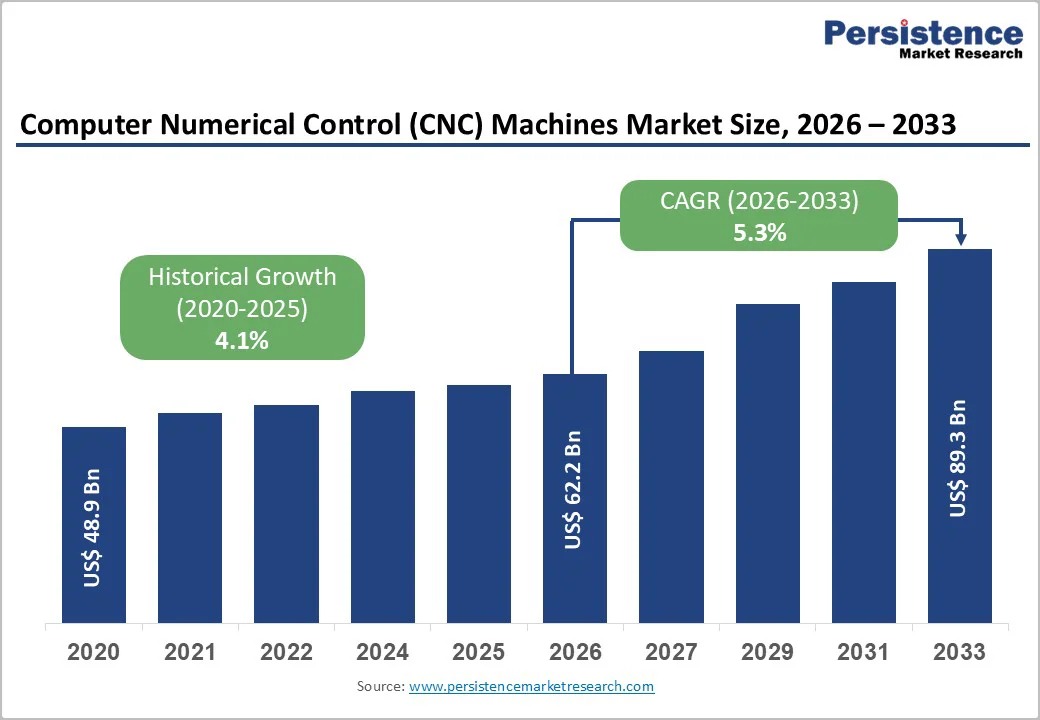

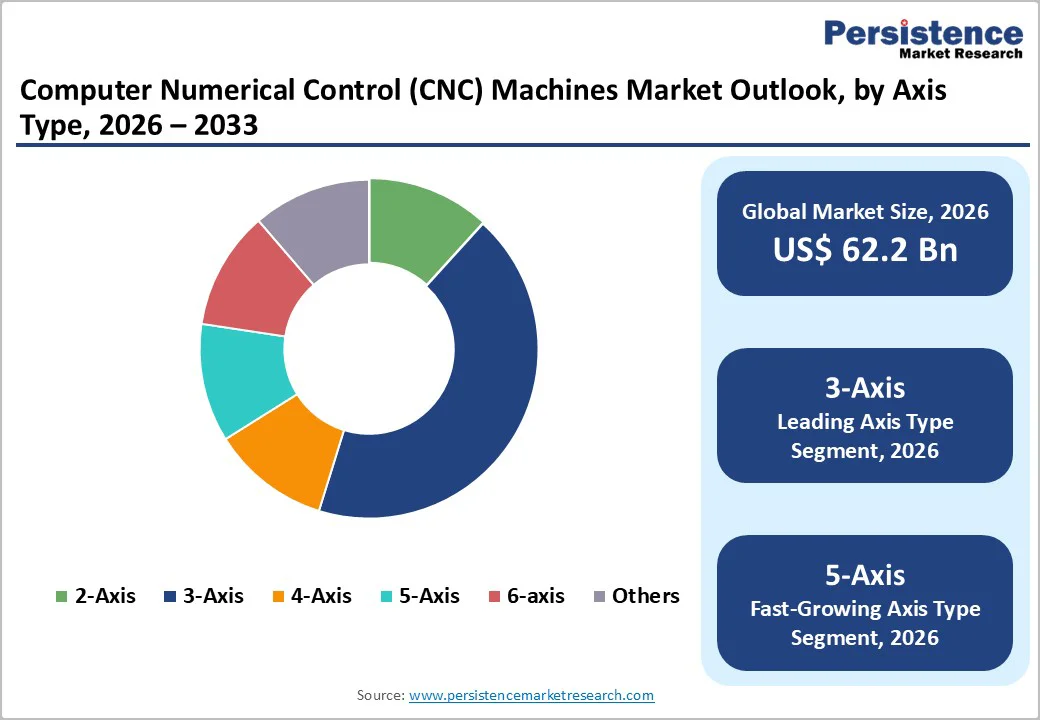

The global computer numerical control (CNC) machines market size is likely to be valued at US$ 62.2 billion in 2026 and projected to reach US$ 89.3 billion by 2033, growing at a CAGR of 5.3% between 2026 and 2033. The market expansion is fundamentally driven by accelerating industrial automation initiatives, rising demand for precision-engineered components across aerospace and automotive sectors, and the widespread adoption of Industry 4.0 technologies.

The integration of Artificial Intelligence (AI), the Internet of Things (IoT), and cloud-based manufacturing solutions into CNC systems is revolutionizing operational efficiency, predictive maintenance, and real-time process monitoring. Governments worldwide are prioritizing advanced manufacturing infrastructure through initiatives such as “Make in India,” Industry 4.0 in Germany, and strategic manufacturing investments in emerging economies, thereby creating sustained demand for sophisticated CNC machinery.

Key Industry Highlights:

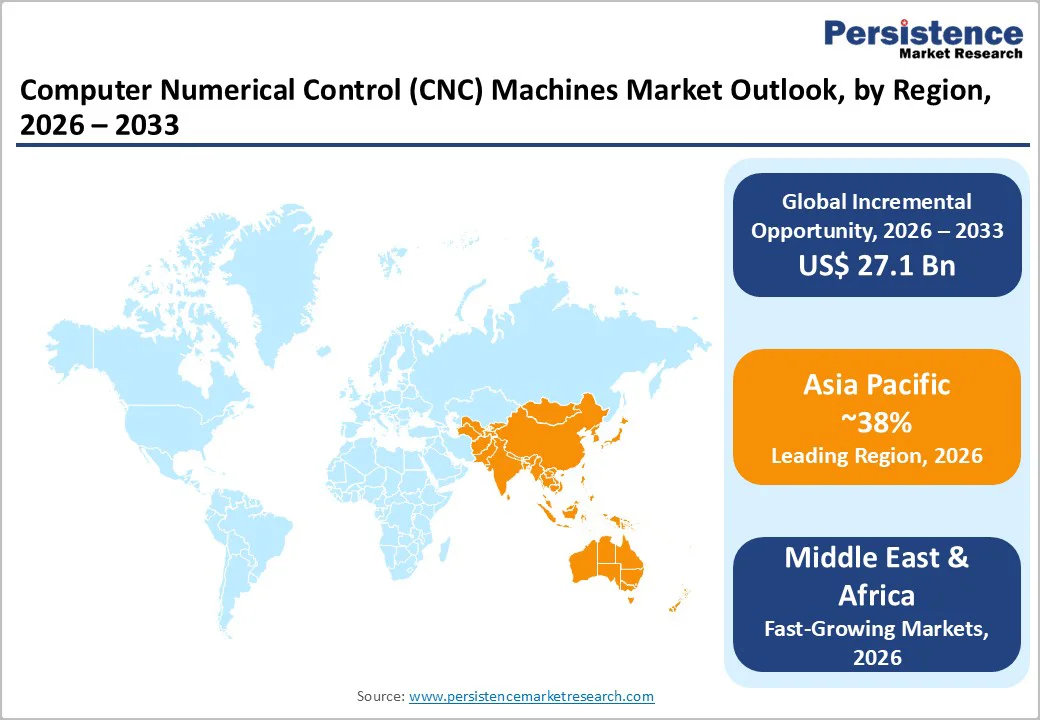

- Leading Region: Asia Pacific leads the global CNC machinery market in 2025 with around 38% share, supported by China’s large manufacturing base, Japan’s precision engineering, and India’s expanding automotive and aerospace sectors.

- Fastest Growing Region: The Middle East & Africa is the fastest-growing CNC machinery market, projected to grow at 8.5% CAGR through 2033, driven by industrial diversification and manufacturing expansion in Saudi Arabia, UAE, and Egypt.

- Dominant Segment by Machine Type: Milling machines dominate the CNC machinery market, with about 45% share in 2025, driven by their versatility across industries and the strong adoption of cost-effective vertical CNC milling systems.

- Fastest Growing Segment by Axis Type: 5-Axis CNC machining centers are the fastest-growing axis category, forecast to expand at 10.7% CAGR through 2032, owing to rising aerospace and medical demand for complex, high-precision, single-setup manufacturing.

- Key Market Opportunity: Advanced manufacturing initiatives across major economies, combined with growing aerospace output and customized medical device needs, are creating major opportunities for CNC makers offering AI-enabled, digital-twin, and sustainability-focused systems.

| Key Insights | Details |

|---|---|

|

CNC Machines Market Size (2026E) |

US$ 62.2 Bn |

|

Market Value Forecast (2033F) |

US$ 89.3 Bn |

|

Projected Growth CAGR (2026-2033) |

5.3% |

|

Historical Market Growth (2020-2025) |

4.1% |

Market Dynamics

Drivers - Industrial Automation and Manufacturing Precision Driving Market Expansion

Industrial automation represents the primary catalyst for CNC machine market expansion globally. According to the European Confederation of the Machine Tool Industries (CECIMO), global machine tool production reached approximately €79.5 billion in 2022, representing a 12% increase compared to 2021 and 7.9% growth versus pre-pandemic 2019 levels. The International Federation of Robotics reports that CNC machines account for a substantial share of industrial automation projects across regions, with manufacturers increasingly recognizing their critical role in achieving Industry 4.0 objectives.

In India, the machine tools market is experiencing accelerated growth at 8% CAGR through 2031, driven by the government’s “Make in India” initiative and Production-Linked Incentive (PLI) schemes, which have catalyzed investments in domestic manufacturing capabilities. The automotive industry, representing more than 40% market share in Asia-Pacific machine tools consumption, continues generating substantial CNC equipment demand as manufacturers upgrade to multi-axis systems capable of producing complex components with tighter tolerances. Research from the National Institute of Standards and Technology (NIST) demonstrates that manufacturers implementing advanced CNC systems achieve 20-30% productivity improvements and 15-25% reductions in material waste, creating compelling economic justification for capital investments in precision machinery.

Aerospace and Defense Sector Demand Catalyzing Advanced CNC Technology Adoption

The aerospace and defense industries represent critical demand drivers for advanced CNC machinery, particularly 5-axis and multi-tasking systems capable of manufacturing complex, high-precision components. The International Air Transport Association (IATA) reports that global commercial aircraft production is projected to exceed 40,000 aircraft deliveries over the next 20 years, creating sustained demand for precision-machined airframe components, engine parts, and landing gear assemblies. Manufacturers like Boeing produce approximately 38 aircraft per month, including 5 Dreamliners, using CNC machining technology to manufacture fuselage sections, wings, and landing gear structures.

Airbus, Europe’s leading aerospace manufacturer, extensively employs 5-axis CNC systems to produce lighter, more durable, modular aircraft designs with reduced maintenance requirements. The U.S. Defense Department and allied nations continue to prioritize advanced manufacturing capabilities for military applications, with defense contractors requiring sophisticated CNC systems to produce complex turbine components, missile housings, and precision-machined defense electronics enclosures. The Fraunhofer Institute's research indicates that aerospace-grade 5-axis machining centers enable single-setup machining of complex components such as aircraft impellers and turbine blisks, reducing production cycles by 40-50% compared to traditional multi-setup machining approaches, thereby justifying premium pricing for advanced systems.

Restraints - Capital Investment Requirements and Skilled Labor Shortages Creating Market Barriers

Substantial initial capital expenditures pose significant barriers to CNC machinery adoption, particularly for small and medium-sized enterprises (SMEs) in developing economies. Comprehensive CNC machining centers with 5-axis capabilities typically require investment ranges of US$ 200,000 to US$ 500,000 or higher, depending on specifications and automation features, creating prohibitive costs for many manufacturing facilities in resource-constrained regions. The German Machine Tool Builders’ Association (VDW) reported that German machine tool orders declined by 19% in 2024, with export orders dropping 24%, reflecting the challenging global economic environment that constrains capital investments in manufacturing equipment.

Moreover, global shortages of skilled CNC machine operators and programmers create significant operational constraints. Research from the National Association of Manufacturers indicates that approximately 2 million manufacturing jobs remain unfilled globally due to skill shortages, with CNC machine operation requiring specialized technical expertise that educational institutions struggle to provide in sufficient numbers. The Bureau of Labor Statistics projects that skilled trade shortages will persist through 2030, with experienced CNC programmers and operators commanding premium wages, increasing total manufacturing costs and complicating workforce development initiatives.

Opportunity- Rising Demand for Customization and Flexibility in Manufacturing Processes

Evolving consumer preferences for customized products are creating substantial opportunities for flexible CNC machining systems capable of rapid product changeovers and batch-size optimization. The Massachusetts Institute of Technology (MIT) research demonstrates that companies implementing advanced CNC systems with quick-change tooling, including high-precision diamond tools, and adaptive control systems achieve 50% reductions in setup times and can economically produce batch sizes down to single units, enabling mass-customization business models previously impossible. Medical device manufacturers increasingly rely on CNC machining for producing patient-specific implants and surgical instruments tailored to individual anatomical requirements.

Precision medical device manufacturers utilizing 5-axis CNC systems report that customization capabilities enable 30% faster product development cycles and superior patient outcomes through optimized implant designs. The construction equipment sector is also experiencing accelerating demand for customized components, with manufacturers such as Caterpillar and Komatsu increasingly deploying advanced CNC systems equipped with diamond-tool machining to produce specialized equipment configurations that meet region-specific regulatory requirements and customer specifications.

Government Support for Advanced Manufacturing and Smart Factory Initiatives

International and national government initiatives promoting advanced manufacturing infrastructure are catalyzing substantial investments in CNC machinery. The European Commission established the Horizon Europe research program with €95.5 billion allocation through 2027, prioritizing advanced manufacturing technologies, including AI-integrated CNC systems, digital twin simulations, and sustainable production methods. Germany’s Federal Government has committed substantial resources to Industry 4.0 initiatives, with the German Federation of Mechanical Engineering (VDMA) reporting that approximately 70% of German machine tool manufacturers now embed IoT connectivity and AI-based analytics into CNC systems.

The U.S. Infrastructure Investment and Jobs Act provides federal funding for advanced manufacturing initiatives, supporting state and local programs encouraging CNC machinery modernization and adoption. India’s Make in India program explicitly targets increasing manufacturing’s contribution to GDP from 16% to 25% by 2025, with government allocations for smart manufacturing initiatives and CNC machine modernization grants reaching US$ 200 million since 2019. Japan’s Society 5.0 program mandates the adoption of IoT-enabled machine tools across manufacturing sectors, with government incentives supporting the integration of advanced CNC systems into production facilities. The World Economic Forum estimates that global government investments in advanced manufacturing infrastructure will exceed US$ 50 billion annually through 2030, creating substantial market opportunities for CNC equipment manufacturers and systems integrators.

Category-wise Analysis

Machine Type Insights

Milling machines hold the leading position in the global CNC market with around 45% share in 2025, driven by their versatility, precision, and suitability for a wide range of industrial applications. Vertical CNC milling machines dominate this segment, offering efficient production of complex 3D features, slots, holes, and intricate contours across metals and composites. Their strong adoption stems from cost-effectiveness compared to specialized systems and their essential role in automotive and industrial component manufacturing. Continued demand for high-volume machining, combined with easier access through refurbished units and leasing options, ensures sustained growth and broad penetration across SMEs and large manufacturers.

Axis Type Insights

5-axis CNC machining centers represent the fastest-growing axis category, expected to expand at a robust 10.7% CAGR through 2032, driven by rising demand for highly complex geometries and single-setup machining. While 3-axis systems still hold the largest share of about 40%, 5-axis platforms are rapidly gaining traction due to their ability to manufacture turbine blisks, orthopedic implants, impellers, and aerospace structural components with exceptional accuracy. Their capability to reduce cycle times by up to half makes them strategically important for industries requiring advanced precision. As manufacturers pursue greater productivity, flexibility, and tighter tolerances, 5-axis CNC systems increasingly become the preferred investment for high-value applications.

Industry Insights

The automotive industry remains the dominant end-use segment in the CNC machinery market, accounting for about 52% share in 2025, underscoring its heavy reliance on precision machining for engines, transmissions, braking systems, and structural components. High-volume manufacturing in China, Europe, and India drives continuous investment in CNC technology to meet stringent productivity and quality demands. The widespread use of High Speed Steel Cutting Tools in machining operations supports the industry’s need for durability, cost-effectiveness, and high-speed material removal. The rise of electric vehicles, requiring precise machining of battery housings, motor components, and lightweight structural parts, further boosts segment growth. As OEMs and Tier-1 suppliers modernize production lines for automation and consistency, the automotive sector remains the largest consumer of CNC machinery worldwide.

Regional Insights

North America CNC Machines Market Trends

North America accounts for about 25% of global CNC machinery demand, supported by mature manufacturing capabilities, strong technological adoption, and continuous investment in precision engineering. The United States leads the region, operating over 290,000 machine tools and generating nearly US$ 5.6 billion in machine tool production, with companies like Haas Automation supplying more than 40,000 CNC machines annually. Demand is reinforced by ongoing upgrades to AI-enabled, IoT-integrated, and Industry 4.0-compatible systems across automotive, aerospace, and general engineering sectors.

Canada remains a significant contributor, particularly through its aerospace clusters in Toronto and Montreal, which rely heavily on 5-axis CNC systems for aircraft component manufacturing. Regional regulations promoting energy efficiency, safety, and reduced environmental impact are accelerating adoption of CNC machines with predictive maintenance, smart diagnostics, and optimized energy systems. Strong R&D investments, proximity to leading technology hubs, and a continuous shift toward automation ensure sustained demand for advanced CNC machinery across North America.

Europe CNC Machines Market Trends

Europe holds roughly 32% of global CNC machinery consumption, supported by long-established precision engineering capabilities and strong automotive and aerospace industries in Germany, Italy, France, and Spain. Germany leads regional demand and production, benefiting from globally recognized machine tool manufacturers such as DMG MORI and Siemens as well as a strong network of specialized Mittelstand firms. However, the European CNC industry is experiencing contraction, with CECIMO reporting a 9.2% production decline to €25.1 billion in 2024 and projecting a further 8.6% drop in 2025.

Consumption is also weakening, falling 16% in 2024 and expected to decline an additional 3.6% in 2025 due to economic uncertainty and delayed capital investments. Despite short-term pressures, Europe’s sustainability targets under the European Green Deal are driving long-term demand for energy-efficient CNC machines equipped with IoT monitoring and low-emission operating capabilities. Italy remains a key export-oriented market, while ongoing automation and Industry 4.0 integration help sustain demand for advanced CNC systems.

Asia Pacific CNC Machines Market Trends

Asia Pacific dominates the global CNC machinery landscape with nearly 38% market share in 2025 and continues to be the fastest-growing region due to rapid industrialization and strong government support for smart manufacturing. China leads regional consumption with roughly 40.5% share, driven by large-scale automotive, electronics, and aerospace production and reinforced by policies under Made in China 2025 that promote adoption of advanced CNC machines and robotics.

Efforts to localize high-end machine tool technology, including state-backed investments such as First Automation’s RMB 100 million funding round, further strengthen domestic capabilities. Japan maintains a premium position through manufacturers like Yamazaki Mazak, OKUMA, and Makino, known for high-precision, multi-tasking, and automation-rich CNC systems. India is emerging rapidly, with its machine tool market projected to grow from US$ 1.92 billion in 2025 to US$ 2.86 billion by 2031, driven by Make in India initiatives and a shift toward automated production. Southeast Asian nations, including Vietnam and Thailand, are also accelerating CNC adoption to support expanding automotive and electronics supply chains.

Competitive Landscape

The global CNC machinery market is moderately consolidated, with a balanced mix of large multinational manufacturers and agile regional players shaping competitive dynamics. Leading firms collectively capture around 45–50% of global share, supported by broad product portfolios, strong control-system capabilities, and extensive service networks. Market competition increasingly centers on technology differentiation, with manufacturers prioritizing AI-enabled adaptive machining, predictive maintenance, digital twin integration, and cloud-connected production platforms.

Companies are shifting toward ecosystem-based strategies, offering software upgrades, automation packages, and lifecycle services to enhance customer stickiness. Business models are evolving as well, with Equipment-as-a-Service (EaaS), long-term service agreements, and subscription-based software optimization emerging as strong alternatives to traditional machine sales. Regional manufacturers compete through cost-effective solutions, customization, and faster delivery cycles. Across the market, R&D efforts emphasize automation, IoT integration, cybersecurity, and sustainable manufacturing, positioning CNC machinery as a core enabler of next-generation smart factory operations.

Key Market Developments

- November 2024: Siemens expanded SINUMERIK ONE’s digital-twin machining capabilities, enabling virtual simulation, collision detection, and optimized tool paths. While the technology boosts efficiency, it is an enhancement—not a new 2024 product launch.

- September 2024: FANUC introduced AI-based thermal displacement compensation for CNC systems, using machine-learning prediction to correct thermal expansion. The technology ensures sustained micron-level accuracy for aerospace, medical, and high-precision manufacturing operations.

Companies Covered in Computer Numerical Control (CNC) Machines Market

- Hurco Companies Inc.

- Protomatic Inc.

- Metal Craft

- OKUMA Corporation

- JTEKT Corporation

- Haas Automation

- Fanuc Corporation

- Siemens AG

- DMG Mori Seiki Co., Ltd.

- AMADA MACHINERY CO., LTD.

- Amera Seiki

- DMG MORI CO., LTD.

- General Technology Group Dalian Machine Tool Corporation

- DATRON AG

- Mitsubishi Electric Corporation

- Yamazaki Mazak Corporation

- Makino Milling Machine Company

- Sodick Co., Ltd.

- Doosan Corporation

- Gleason Corporation

- Hyundai WIA

- Hardinge Inc.

- Mazak (Yamazaki Mazak)

- Kitamura Machinery Inc.

- Mori Seiki

Frequently Asked Questions

The global CNC Machines Market is expected to reach US$ 89.3 billion by 2033, up from US$ 62.2 billion in 2026 at a 5.3% CAGR.

Global demand is driven by industrial automation, rising precision needs in automotive and aerospace, Industry 4.0 adoption, and government-backed advanced manufacturing initiatives.

Milling machines dominate in 2025 with around 45% share, supported by their versatility and strong adoption of vertical milling systems.

Asia Pacific leads with about 38% market share in 2025, driven by China, Japan, India, and Southeast Asia’s expanding manufacturing sectors.

Major opportunities lie in AI-enabled CNC systems, digital-twin technologies, aerospace production growth, medical device customization, and strong industrial expansion in the Middle East & Africa.