- Electrical Equipment & Services

- Mortar Fire Control Computer Market

Mortar Fire Control Computer Market Size, Share, and Growth Forecast 2025 – 2032

Mortar Fire Control Computer Market by Platform Type (Man-Portable System, Vehicle-Mounted System, Fixed Installations), Range (Short-range, Medium-range, Long-range), End-user (Army, Special Forces, Paramilitary Units, Others), and Regional Analysis for 2025-2032

Mortar Fire Control Computer Market Size and Trend Analysis

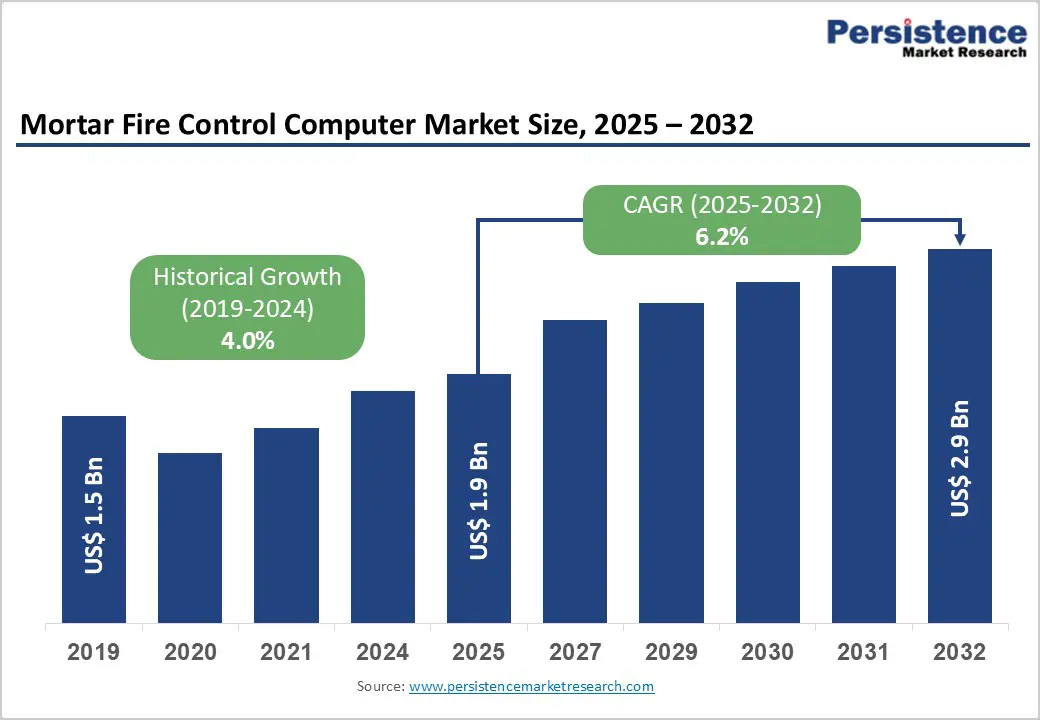

The global mortar fire control computer market size is likely to be valued at US$1.9 billion in 2025 and is expected to reach US$2.9 billion by 2032, growing at a CAGR of 6.2% during the forecast period from 2025 to 2032, driven by widespread defense modernization programs, as armed forces replace legacy, manual fire-control methods with digitized, automated, and network-enabled systems to improve accuracy and response time. The integration of advanced computing, AI-assisted ballistic calculations, inertial navigation, and real-time data sharing is significantly enhancing mortar effectiveness in complex combat environments. Rising geopolitical tensions and asymmetric warfare scenarios are accelerating demand for precision indirect-fire capabilities, particularly for rapid-deployment infantry and mechanized units.

Key Industry Highlights

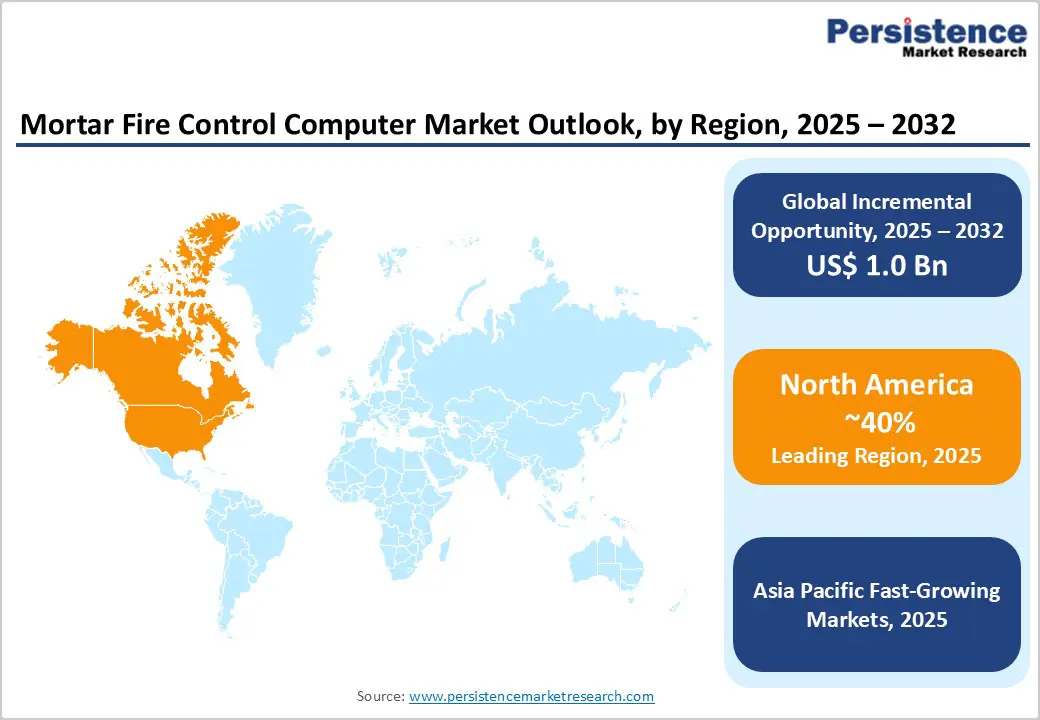

- Leading Region: North America leads the market with around 40% share, driven by robust defense modernization programs, advanced technology ecosystems, and widespread adoption of digitally integrated vehicle-mounted fire control systems across the U.S., Canada, and Mexico.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, driven by rising defense spending in China, India, and other nations, supported by strong local manufacturing, government incentives for indigenous technologies, and increasing demand for versatile man-portable and vehicle-mounted systems across diverse terrains.

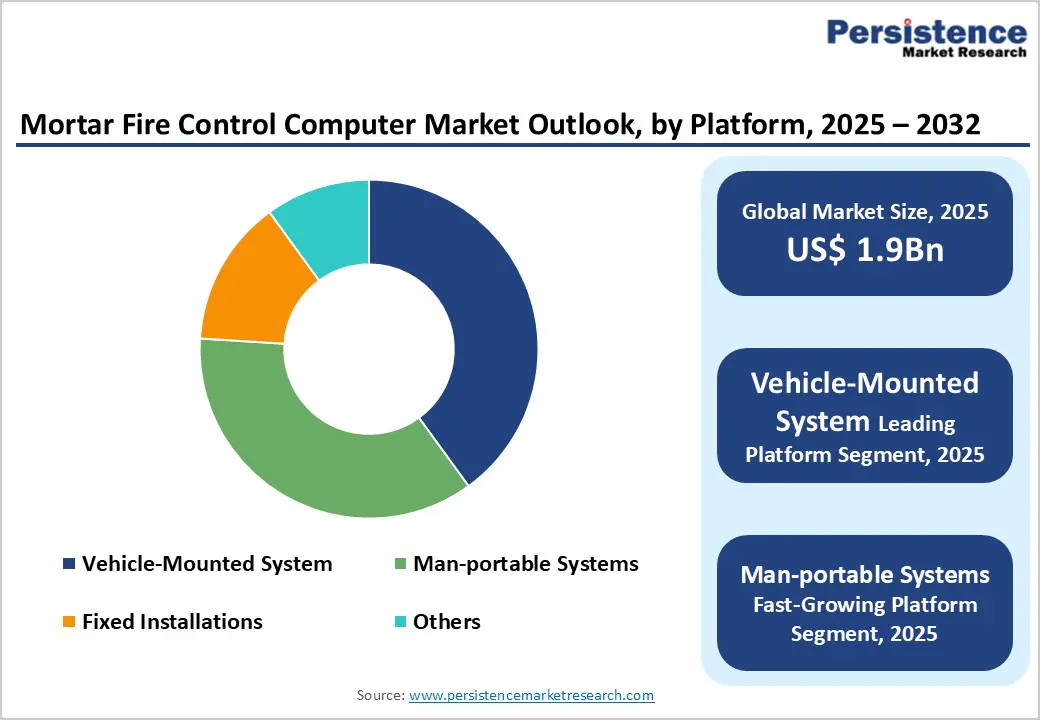

- Leading Platform Type: Vehicle-mounted systems lead the platform market with 47.2% revenue share, driven by their integration with mechanized and armored units for rapid, flexible deployment.

- Leading Range: The medium-range systems (5–10 km) segment leads the market with over 52% revenue share, driven by their optimal balance of range and accuracy for conventional indirect-fire missions.

- Leading End-user Type: Army units represent the leading segment with about 55% revenue share, driven by their extensive deployment of indirect-fire systems and ongoing global modernization programs.

| Key Insights | Details |

|---|---|

| Mortar Fire Control Computer Market Size (2025E) | US$1.9 Bn |

| Market Value Forecast (2032F) | US$2.9 Bn |

| Projected Growth CAGR (2025-2032) | 6.2% |

| Historical Market Growth (2019-2024) | 4.0% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Defense Modernization and Increasing Geopolitical Tensions

Armed forces are steadily moving away from traditional, manual fire-control practices toward advanced digital solutions that deliver faster target acquisition, automated ballistic computations, and greater firing precision. Modern mortar fire control computers (MFCCs) combine inertial navigation, GPS-enabled positioning, ruggedized hardware, and real-time data sharing to significantly shorten response times during indirect-fire operations. These capabilities are especially important for infantry and mechanized units, where timely and accurate mortar support can be decisive.

As militaries emphasize interoperability and network-centric operations, MFCCs are increasingly designed to integrate seamlessly with command-and-control and battlefield management systems, strengthening their position within broader artillery modernization efforts. Rising geopolitical tensions in regions such as Eastern Europe, the Middle East, and the Asia Pacific are further driving adoption. Ongoing border disputes, asymmetric conflicts, and regional instability have heightened demand for precise, mobile, and rapidly deployable indirect-fire systems. In these environments, mortars remain a vital asset, and MFCCs significantly enhance their effectiveness by enabling accurate engagement while reducing the risk of collateral damage.

Regulatory and Supply Chain Challenges

Mortar fire control computers are classified as sensitive military technologies, subject to strict approval processes, national security regulations, and compliance with international arms control frameworks. These requirements frequently result in lengthy procurement timelines and delayed contract execution, particularly for international sales. Differences in defense certification and compliance standards across regions further complicate interoperability, increasing development complexity, time, and costs for manufacturers. Smaller suppliers are especially challenged by complex tendering procedures and stringent regulatory demands, which can restrict market entry and limit competition.

Market growth is also constrained by supply chain disruptions, as MFCC production relies on specialized electronic components such as ruggedized processors, sensors, and secure communication systems. Global semiconductor shortages, geopolitical trade barriers, and reliance on a narrow pool of defense-qualified suppliers have highlighted vulnerabilities in the supply chain. Component delays can slow production and disrupt delivery schedules for military programs, while rising material costs and logistical challenges place additional pressure on defense contractors, potentially affecting pricing strategies and long-term supply commitments.

Technological Convergence with Autonomous Weapon Systems

Armed forces around the world are increasingly testing and deploying unmanned ground vehicles (UGVs), remotely operated weapon stations, and semi-autonomous combat systems to reduce risks to personnel and enhance operational effectiveness. As mortars are more frequently integrated onto robotic or remotely controlled platforms, mortar fire control computers become a key enabling technology, delivering automated ballistic calculations, target data processing, and remote execution of fire missions. Consequently, lightweight and modular MFCC designs tailored for autonomous platforms are attracting growing interest as militaries evaluate next-generation indirect-fire solutions.

Progress in artificial intelligence, sensor fusion, and secure communications further amplifies this opportunity. AI-driven MFCCs can analyze inputs from UAVs, battlefield sensors, and command networks to support autonomous or semi-autonomous firing decisions with improved accuracy and reduced response times. Their integration with autonomous systems enables seamless sensor-to-shooter connectivity, enhancing coordination in network-centric combat environments. As defense organizations continue to invest in unmanned and autonomous warfare technologies, demand for advanced MFCCs compatible with these platforms is expected to increase, creating new pathways for innovation and sustained market growth.

Category-wise Analysis

Platform Type Insights

The vehicle-mounted segment dominates, accounting for approximately 47.2% of total revenue in 2025. This leadership is largely driven by widespread integration with armored vehicles, mechanized infantry platforms, and self-propelled mortar systems. Compared with dismounted setups, vehicle-mounted solutions provide greater firing stability, faster processing of fire missions, and enhanced crew protection. Their ability to integrate seamlessly with digital command networks, GPS-based navigation, and advanced communications makes them essential for rapid-response and high-intensity combat operations. For instance, the U.S. Army’s M125 and M1064 self-propelled mortar carriers employ vehicle-mounted digital fire-control systems to support rapid sensor-to-shooter engagement.

Man-portable MFCCs represent the fastest-growing platform segment, driven by increasing demand from Special Forces, expeditionary units, and light infantry for lightweight, rugged, and rapidly deployable solutions. These portable systems allow troops to conduct accurate fire missions in challenging environments such as mountainous terrain, dense urban settings, and remote areas where vehicles cannot operate effectively. Advances in battery endurance, compact ruggedized hardware, and AI-enabled fire-control software have significantly enhanced their performance, making them well-suited for fast-paced tactical operations. For instance, infantry units engaged in urban counterinsurgency missions rely on man-portable MFCCs to deliver precise indirect fire with minimal preparation time.

Range Type Insights

The medium-range segment is both the dominant and fastest-growing segment in the mortar fire control computer market, generating more than 52% of total revenue. It offers an effective balance of operational range, accuracy, and tactical versatility for conventional indirect-fire missions, making it widely adopted by infantry and mechanized formations. These systems support the most commonly deployed mortar calibers and deliver reliable fire support across diverse scenarios, including border security, counterinsurgency, and conventional combat, while maintaining high precision and relatively modest logistical demands.

Continuous improvements in fire-control software, sensor integration, and user interface design, such as advances in ballistic modeling, enhanced GPS/INS accuracy, and user-friendly touchscreen interfaces, are further increasing system reliability and ease of use in dynamic combat environments. For instance, NATO ground forces extensively employ medium-range digital fire-control systems integrated with 81 mm and 120 mm mortars, and Asian defense forces are increasingly procuring these systems to enhance firing accuracy and reduce response times.

End-user Type Insights

Army units dominate the market, accounting for roughly 55% of the total revenue, driven by their widespread use of indirect-fire systems and ongoing large-scale modernization programs. Armies around the world maintain extensive inventories of mortars across light infantry, mechanized, and artillery formations, generating sustained demand for advanced fire control computers that improve accuracy, response speed, and interoperability. For instance, the U.S. Army has modernized its mortar forces with digital fire-control computers to strengthen sensor-to-shooter connectivity.

Special Forces constitute the fastest-growing end-user segment, as rising operational demands are pushing the adoption of lightweight, compact, and highly autonomous fire-control solutions. These elite units frequently operate in austere, contested environments where conventional fire-support infrastructure is unavailable, making portable and AI-enabled MFCCs critical. As Special Forces expand their roles and conduct more precision-driven missions, demand for next-generation MFCCs continues to grow. For example, special operations units operating in mountainous and jungle terrain depend on man-portable MFCCs to enable rapid mortar deployment and accurate fire support.

Regional Insights

North America Mortar Fire Control Computer Market Trends

North America is emerging as the dominant region in the mortar fire control computer market, supported by its advanced defense infrastructure, substantial military budgets, and ongoing modernization of indirect-fire capabilities. The U.S., which generates the majority of regional demand, is actively upgrading mortar and artillery units with digital fire-direction systems, automated targeting technologies, and network-enabled command platforms. These initiatives are aimed at shortening sensor-to-shooter timelines and improving interoperability across joint and coalition forces. The strong presence of leading defense contractors and continuous testing of next-generation fire-control solutions further reinforce North America’s leadership in MFCC adoption.

Technology integration remains a key growth driver, as North American forces increasingly deploy GPS-based targeting, AI-enabled fire-control software, ruggedized hardware, and modular, upgradeable system architectures. Canada is also progressing with mortar modernization efforts, focusing on NATO-compliant solutions and enhanced battlefield mobility. The region is at the forefront of drone-assisted fire direction, with UAVs supplying real-time target data directly to MFCCs. This capability significantly improves accuracy and responsiveness, accelerating demand for advanced, automated MFCCs that support real-time data fusion and secure communications.

Europe Mortar Fire Control Computer Market Trends

Europe remains an important market for mortar fire control computers, underpinned by ongoing defense modernization programs, NATO obligations, and elevated regional security challenges. Nations including the U.K., Germany, France, and Italy are actively enhancing their mortar and artillery capabilities with advanced digital fire-control systems to improve accuracy, reaction speed, and interoperability. NATO-driven networked operations and regular multinational exercises continue to fuel demand for MFCCs that integrate smoothly with standardized command-and-control frameworks. Increased investments in rapid-response forces and mechanized infantry units are accelerating the adoption of vehicle-mounted MFCCs across European militaries.

Technological advancement is a key factor shaping regional market dynamics, as armed forces increasingly deploy AI-supported targeting, GPS-based navigation, and rugged, modular computing platforms. There is also rising demand for both man-portable and vehicle-mounted MFCCs to enable rapid deployment in varied operational environments, including urban areas and mountainous terrain. European militaries are expanding their use of unmanned ground vehicles and drone-enabled targeting, driving the need for automated MFCCs capable of real-time ballistic processing and advanced sensor fusion.

Asia Pacific Mortar Fire Control Computer Market Trends

Asia Pacific is the fastest-growing region in the mortar fire control computer market, driven by rising defense budgets, regional security tensions, and ongoing military modernization programs. Countries such as India, Japan, South Korea, and Australia are investing heavily in upgrading their artillery and mortar systems with advanced fire control solutions to enhance precision, mobility, and operational readiness. Territorial disputes, border security concerns, and the need for rapid-response capabilities are the key factors boosting the adoption of MFCCs in the region.

Technological advancements are shaping the market, with militaries integrating GPS-guided targeting, AI-powered fire-control algorithms, and ruggedized, modular computing systems. Vehicle-mounted MFCCs are widely adopted for mechanized units, while man-portable systems are increasingly deployed by Special Forces and infantry units in challenging terrains. The region is adopting drone-assisted targeting and UGVs, increasing the demand for automated MFCCs with real-time data processing.

Competitive Landscape

The global mortar fire control computer market exhibits a moderately fragmented structure, driven by a mix of large defense electronics giants and specialized fire-control technology providers competing for contracts with national militaries and integrators. Firms are investing heavily in digital battlefield integration, advanced GPS and inertial navigation systems, and AI-assisted fire-control software to gain an edge. With key leaders including Lockheed Martin Corporation and Raytheon Technologies Corporation, the competitive environment emphasizes technological depth.

These players compete through strategic R&D investments, product portfolio expansion, and partnerships with defense ministries and platform integrators. Differentiation is achieved by offering enhanced user interfaces, modular hardware, ruggedization for battlefield conditions, and seamless interoperability with networked command systems. Collaborations with governments and participation in joint modernization programs further strengthen their market positions.

Key Industry Developments:

- In January 2025, Leonardo DRS was awarded a contract exceeding US$99 million to modernize the U.S. Army’s mortar fire control system, strengthening the Army’s transition toward digitally integrated indirect-fire capabilities. Under the contract, Leonardo DRS will produce and deliver next-generation Mortar Fire Control Systems (MFCS) along with fielding support for mortar weapon and fire-control programs.

- In July 2025, Smartshooter received a new order from the U.S. Marine Corps for its SMASH 2000L fire control system, reinforcing the growing adoption of AI-enabled fire-control technologies within U.S. defense forces. The system is being procured as an interim solution to address the USMC’s urgent requirement for dismounted counter–small unmanned aerial system (C-sUAS) capabilities, following successful operational testing by Marine units. SMASH 2000L is Smartshooter’s lightest handheld fire control system and integrates artificial intelligence, computer vision, and advanced target-tracking algorithms to enable precise engagement of aerial and ground threats.

Companies Covered in Mortar Fire Control Computer Market

- MAS Zengrange

- ARDEC

- Picatinny

- SDT SUSTAV

- General Dynamics

- Denel Land Systems

- Safran

Frequently Asked Questions

The global mortar fire control computer market is valued at US$1.9 billion in 2025 and expected to reach US$2.9 billion by 2032, reflecting robust growth.

The key demand drivers for the mortar fire control computer market include ongoing defense modernization programs, the integration of artificial intelligence into fire-control systems, and increasing geopolitical tensions that require accurate, rapid, and reliable indirect-fire capabilities.

Vehicle-mounted systems lead with 47.2% share, driven by their integration with mechanized and armored units for rapid, flexible deployment.

North America dominates, capturing over 40% market share, driven by high defense spending and a mature technology ecosystem.

A major opportunity in the mortar fire control computer market lies in the Asia Pacific region, where rising defense budgets and a focus on domestic production are driving growth, coupled with expanding prospects from the integration of MFCCs with autonomous weapons technologies.