- Pharmaceuticals

- Fixed-Dose Combination Drugs Market

Fixed-Dose Combination Drugs Market Size, Share, and Growth Forecast, 2026 - 2033

Fixed-Dose Combination Drugs Market by Therapeutic Area (Cardiovascular Diseases, Others), Formulation Type (Tablets, Capsules, Others), Route of Administration (Oral, Others), Distribution Channel (Retail Pharmacies, Others), and Regional Analysis for 2026 - 2033

Fixed-Dose Combination Drugs Market Size and Trends Analysis

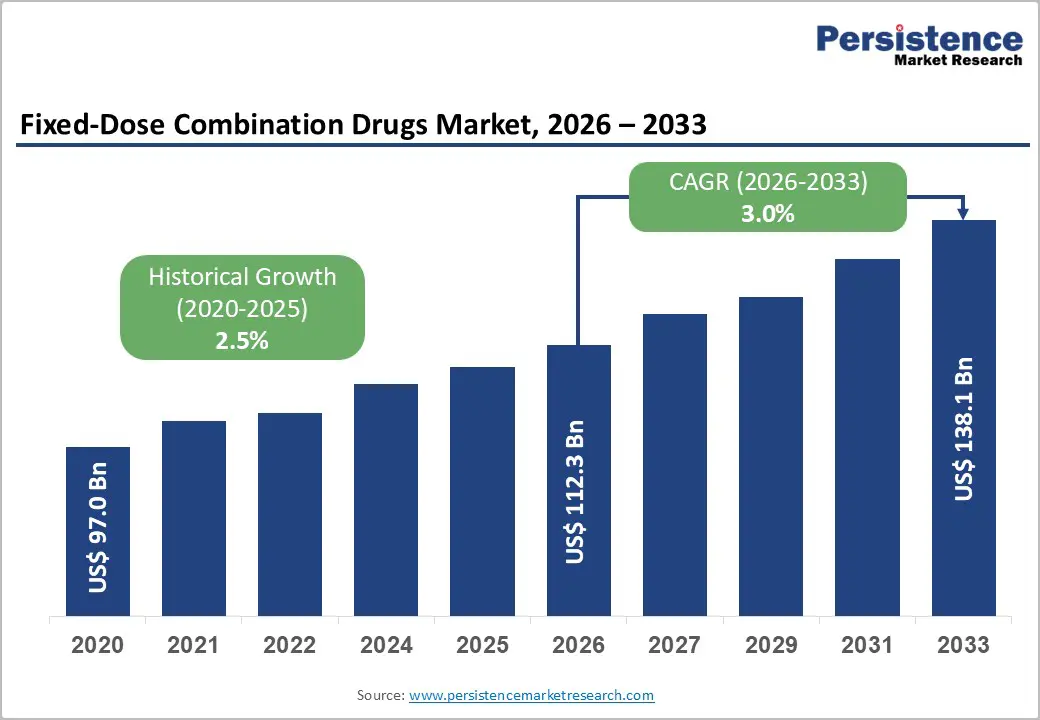

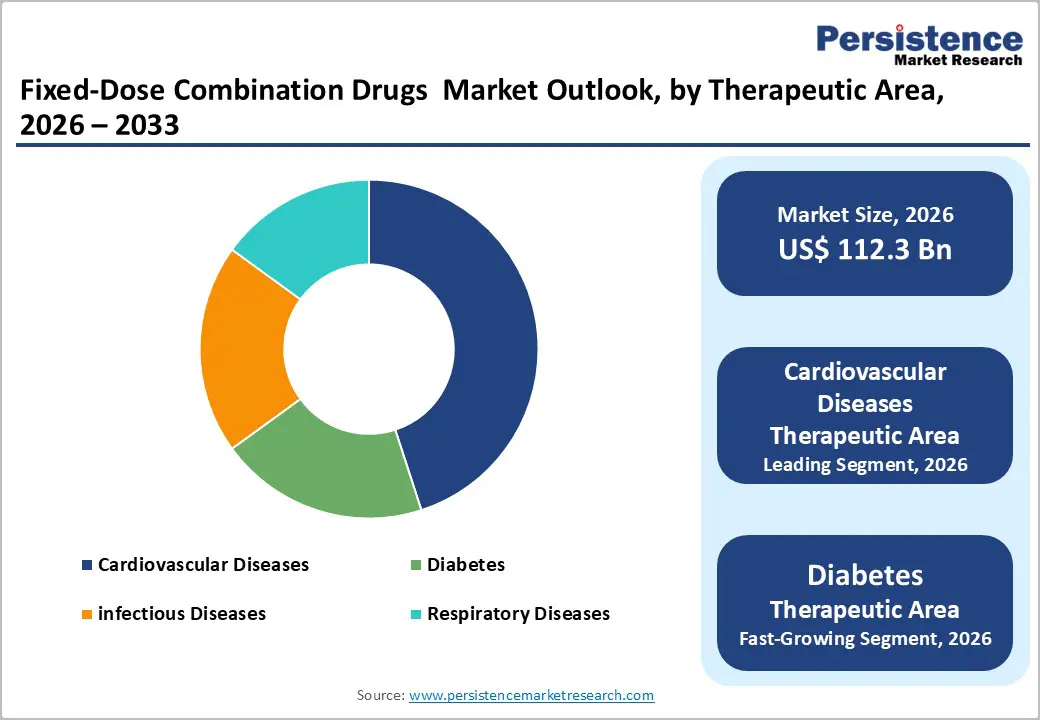

The global fixed-dose combination drugs market size is likely to be valued at US$112.3 billion in 2026, and is expected to reach US$138.1 billion by 2033, growing at a CAGR of 3.0% during the forecast period from 2026 to 2033, driven by the increasing prevalence of chronic diseases, rising demand for improved patient adherence through simplified regimens, and advancements in multi-drug formulations.

Growing demand for effective, convenient fixed-dose combination drugs, especially in cardiovascular diseases and diabetes, is accelerating adoption across therapeutic areas. Advances in oral tablets and capsules are further boosting uptake by offering more bioavailable, user-friendly options. Increasing recognition of fixed-dose combination drugs as critical for cost-effective treatment in emerging healthcare systems remains a major driver of market growth.

Key Industry Highlights:

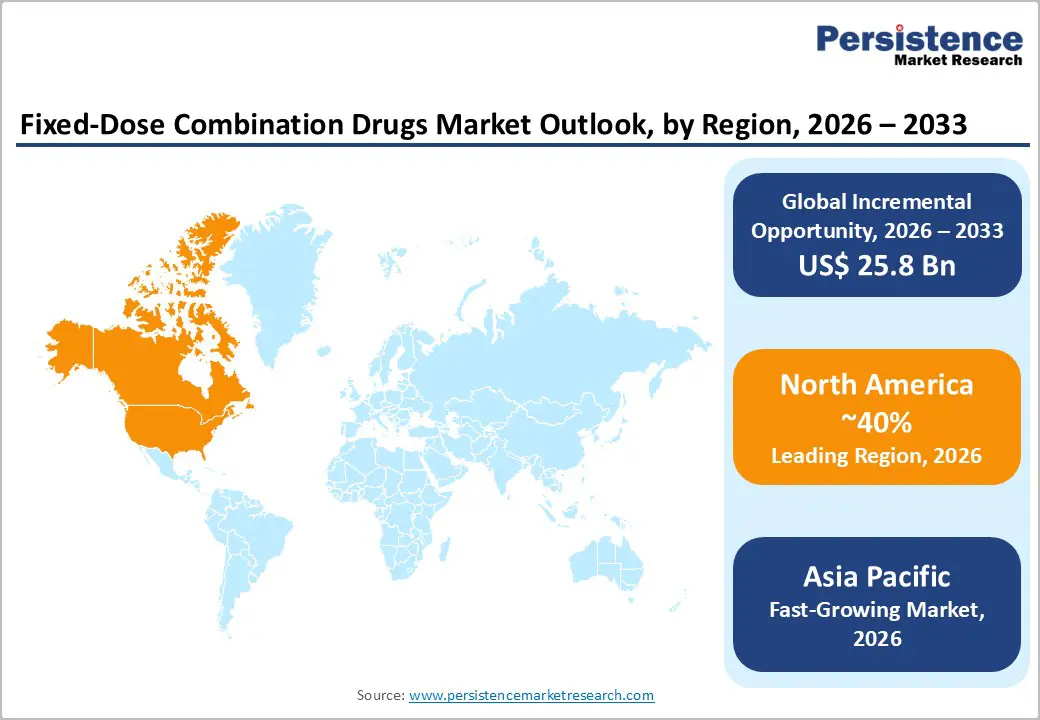

- Leading Region: North America, anticipated to account for a 40% market share in 2026, driven by high chronic disease burden, strong pharmaceutical innovation, and favorable reimbursement in the U.S.

- Fastest-growing Region: Asia Pacific, fueled by aging populations, rising diabetes prevalence, and growing investments in affordable generics in India and China.

- Dominant Therapeutic Area: Cardiovascular diseases, to hold approximately 45% of the market share, as it addresses hypertension and dyslipidemia with dual therapies.

- Leading Formulation Type: Tablets, to account for over 60% of the market revenue, due to ease of administration and patient preference.

- Leading Route of Administration: Oral, to contribute nearly 70% of the market revenue, due to non-invasive delivery and high compliance.

- Leading Distribution Channel: Retail pharmacies, to contribute nearly 50% of the market revenue, due to widespread accessibility and prescription fulfillment.

| Key Insights | Details |

|---|---|

|

Fixed-Dose Combination Drugs Market Size (2026E) |

US$112.3 Bn |

|

Market Value Forecast (2033F) |

US$138.1 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

3.0% |

|

Historical Market Growth (CAGR 2020 to 2025) |

2.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Prevalence of Chronic Diseases

The increasing global burden of chronic diseases is a major driver of the fixed-dose combination (FDC) drugs market. Conditions such as diabetes, cardiovascular disorders, hypertension, asthma, chronic obstructive pulmonary disease, and HIV require long-term or lifelong treatment, often involving multiple medications taken simultaneously. As life expectancy rises and lifestyles become more sedentary, the number of patients living with two or more chronic conditions continues to grow, significantly increasing the complexity of treatment regimens.

Managing these diseases with separate drugs can lead to a high pill burden, frequent dosing schedules, and an increased risk of missed doses, which can negatively impact treatment effectiveness. Fixed-dose combination drugs address this challenge by integrating multiple active ingredients into a single formulation, enabling patients to manage their conditions more easily and consistently. This approach is particularly valuable for chronic diseases where sustained medication adherence is critical to prevent disease progression, complications, and hospitalizations. Healthcare providers also favor FDCs in chronic disease management as they support standardized treatment protocols and improve long-term patient outcomes.

Complex Regulatory Approval Processes

Complex regulatory approval processes pose a major challenge for the fixed-dose combination (FDC) drugs market. Unlike single-ingredient medicines, FDCs must demonstrate the safety and efficacy of each component, and also the clinical benefits of their combined use in a fixed ratio. Regulators often require additional studies to ensure the combination provides consistent therapeutic effects without adverse drug interactions or altered pharmacokinetics.

The approval pathway for FDCs can be lengthy and expensive, as developers may need to conduct comparative trials against individual monotherapies to validate the combination’s medical value. Authorities frequently demand evidence that the FDC offers clear advantages, such as improved adherence or better clinical outcomes, rather than just convenience. These requirements extend development timelines and increase R&D costs, especially for innovative or first-in-class combinations.

Innovations in Multi-Drug and Patient-Centric Delivery Platforms

Innovations in multi-drug and patient-centric fixed-dose combination (FDC) delivery platforms are reshaping the global treatment landscape by addressing two key challenges, polypharmacy and medication adherence. Multi-drug platforms are designed for synergistic effects, reducing the need for multiple pills and enabling comprehensive therapy in a single dose. Advances such as bilayer tablets, osmotic pumps, nanoparticle encapsulation, and taste-masked granules improve efficacy, minimize side effects, and help lower healthcare costs.

Patient-centric platforms, including once-daily oral formulations, child-friendly capsules, topical patches, and injectable depots, enhance adherence by reducing dosing frequency, eliminating pill burden, and increasing convenience. These formats are particularly suited for large-scale chronic disease programs. Emerging technologies, such as 3D-printed combinations, bio-adhesive films, and virus-like particle (VLP)-based monitoring, further enable personalized treatment and improved therapeutic response.

Category-wise Analysis

Therapeutic Area Insights

Cardiovascular diseases are expected to lead the market, representing around 45% of the market share in 2026. This dominance is driven by the high prevalence of hypertension, widespread polypill programs, and strong global demand for combination therapies. Cardiovascular treatments offer enhanced efficacy, improve patient adherence, and support better clinical outcomes, making them well-suited for large-scale treatment initiatives. For example, Cadila Pharmaceuticals’ Polycap polypill combines multiple medications to reduce the risk of cardiovascular events and has demonstrated significant benefits in large clinical trials presented at major scientific conferences.

Diabetes is the fastest-growing segment, driven by rising prevalence and increased use of multi-drug regimens. Its favorable glycemic profile allows for targeted blood sugar control, overcoming the limitations of monotherapy. Ongoing innovations in combination therapies are boosting their adoption, particularly in North America and Europe, where demand for convenient diabetes management solutions is increasing. For instance, Glenmark introduced Zita DM in India, a triple-drug fixed-dose combination (FDC) containing Teneligliptin (DPP-4 inhibitor), Dapagliflozin (SGLT2 inhibitor), and Metformin. This therapy addresses multiple pathophysiological pathways of type 2 diabetes, enabling patients to achieve better blood sugar control with a single daily dose instead of separate medications. It is indicated for adult patients whose diabetes is not adequately managed with monotherapy or dual therapy, aiming to lower HbA1c and improve overall glycemic outcomes.

Formulation Type Insights

Tablets are expected to dominate the market in 2026, holding around 60% of the share, driven by their ease of swallowing, large-scale production, and strong global demand for oral delivery. Their continued popularity reflects patient preference for non-invasive treatments. The rising adoption of capsules and expanding injectable programs highlights growing interest in alternative dosage forms. Industry data shows that tablets accounted for the majority of the oral solid dosage market in 2025 (~68%), supported by cost-effective manufacturing, ease of use, and suitability for combination therapies across multiple therapeutic areas, including chronic diseases.

Capsules represent the fastest-growing segment, fueled by advancements in taste-masking and increasing use in pediatric and geriatric formulations. The shift toward swallow-friendly designs and improved protection is accelerating adoption. Innovations such as gelatin improvements and the introduction of vegan capsules are key drivers. For example, ACG Capsules (ACG Group) launched fully vegan printed capsules, reflecting growing demand for plant-based, ethical, and transparent options, particularly among health-conscious and diet-sensitive patients.

Route of Administration Insights

The oral route is expected to dominate the market, accounting for nearly 70% of revenue in 2026. This is due to its continued role as the preferred method for convenience, large patient programs, and the management of chronic conditions that require daily dosing. Strong patient acceptance, well-trained prescribers, and the ability to handle high-volume or combination formulations drive higher consumption. Oral medications are leading the rollout of new tablets and emerging capsule trials. Pfizer Inc. is a leading producer of oral solid dosage forms, including fixed-dose combination tablets and capsules for chronic conditions such as cardiovascular diseases, diabetes, and infectious diseases. The company reportedly holds a significant share of the global oral solid dosage pharmaceutical market (approximately 19%), highlighting the extensive production and demand for oral therapies worldwide.

Injectables, meanwhile, are likely to be the fastest-growing segment, fueled by their high potency and expanding role in biologic combinations. They provide rapid, convenient, and targeted delivery, appealing to clinicians who prioritize long-acting treatment options. Greater outreach programs, hospital-focused initiatives, and wider availability of both routine and premium injectables are further driving adoption across acute and chronic care settings. Biocon Biologics has expanded its injectable portfolio to include biosimilars and biologics, such as insulin products and monoclonal antibody therapies. Biocon’s emphasis on injectable biologics reflects a broader industry trend toward high-potency drugs that deliver targeted, long-acting treatment for chronic conditions such as diabetes, autoimmune disorders, and cancer.

Distribution Channel Insights

Retail pharmacies are expected to dominate the market, capturing around 50% share in 2026, driven by high prescription volumes and a strong global focus on community access. Consistent demand is supported by regular refill schedules, patient needs, and the widespread availability of retail outlets. Growing attention to hospital pharmacies and online channels further reinforces retail’s market leadership. Market data shows that CVS holds over 25% of U.S. prescription drug revenue, making it the largest retail pharmacy by prescription volume. Retail operators such as CVS Health also distribute fixed-dose combinations (FDCs) for routine cardiovascular care, including tablets and capsules, ensuring broad coverage while supporting preventive health initiatives.

Online pharmacies are the fastest-growing segment, fueled by the rising demand for home delivery, convenience, and wider adoption of e-prescriptions. Enhanced access, personalized options, and robust digital platforms for older adults are accelerating uptake. The expansion of telehealth, remote monitoring, and other digital health solutions further drives growth. For example, Tata 1mg allows consumers to order prescription medicines, schedule consultations, and receive medications at home, integrating e-prescriptions, telehealth, and home delivery into a seamless digital patient experience.

Regional Insights

North America Fixed-Dose Combination Drugs Market Trends

North America is projected to lead the global fixed-dose combination (FDC) drugs market, accounting for nearly 40% of revenue in 2026. This growth is supported by the region’s advanced healthcare infrastructure, robust research and development capabilities, and high public awareness of the benefits of medication adherence. Prescription systems in the U.S. and Canada provide strong support for combination therapy programs, ensuring widespread access to FDC drugs for cardiovascular, diabetes, and respiratory patients. Rising demand for oral, convenient, and easy-to-administer formulations is further driving adoption, as these options enhance compliance and reduce the challenges associated with multi-pill regimens.

Technological innovations in FDC drugs, such as stable multi-API formulations, improved capsule delivery, and targeted therapeutic enhancements, are attracting substantial investments from both public and private sectors. Government initiatives and reimbursement policies continue to encourage FDC use, addressing risks from polypharmacy, treatment gaps, and emerging chronic conditions, thereby sustaining market demand. Increasing focus on injectable formulations and specialty applications, particularly in oncology, is expanding the potential use cases for FDC drugs.

Europe Fixed-Dose Combination Drugs Market Trends

Europe’s fixed-dose combination (FDC) drugs market is supported by rising awareness of adherence benefits, strong healthcare systems, and government-led cost-containment initiatives. Countries such as Germany, France, and the U.K. have well-established reimbursement frameworks that encourage routine use of combination therapies and the adoption of innovative FDC delivery methods. These patient-compliant formulations are particularly beneficial for cardiovascular patients, older adults, and individuals with diabetes, improving treatment outcomes and coverage rates.

Technological advancements, such as enhanced stability, targeted delivery, and improved generic formulations, are further boosting market potential. European authorities are increasingly backing research and clinical trials for FDCs addressing both routine and specialized needs, strengthening market confidence. Growing demand for convenient, cost-effective options aligns with the region’s focus on preventive care and reducing hospital workloads. Public awareness campaigns and promotion efforts are expanding reach across urban and rural areas, while suppliers continue to invest in manufacturing and novel variants to enhance efficacy and accessibility.

Asia Pacific Fixed-Dose Combination Drugs Market Trends

Asia Pacific is expected to be the fastest-growing market for fixed-dose combination (FDC) drugs, driven by the rising burden of chronic diseases, expanding government initiatives, and broader application programs across the region. Countries such as India, China, Japan, and Southeast Asian nations are actively promoting FDC campaigns to improve affordability and address adherence challenges. FDC drugs are especially appealing in these markets due to their cost-effective administration, scalability, and suitability for large-scale treatment programs in both urban and rural populations.

Technological advancements are facilitating the development of stable, effective, and easy-to-administer FDC formulations that can withstand challenging access conditions and reduce pill burden. These innovations are crucial for reaching remote healthcare facilities and improving overall therapeutic coverage. Increasing demand in cardiovascular, diabetes, and infectious disease treatments is driving market growth, while public-private partnerships, rising healthcare expenditure, and greater investment in generic manufacturing and research further accelerate expansion. The convenience, improved adherence, and reduced non-compliance risk make FDC drugs a preferred choice in the region.

Competitive Landscape

The global fixed-dose combination drugs market is shaped by competition between established pharmaceutical leaders and emerging generic manufacturers. In North America and Europe, companies such as Pfizer Inc. and Novartis AG dominate through robust R&D capabilities, extensive distribution networks, and strong portfolios, supported by innovative combination therapies and adherence programs. In the Asia Pacific region, generic players are driving growth by offering localized, cost-effective solutions that improve accessibility. Multi-API FDCs enhance therapeutic outcomes, reduce regimen-related risks, and enable large-scale integration across markets. Strategic partnerships, collaborations, and acquisitions are helping companies combine expertise, expand pipelines, and accelerate commercialization. Generic formulations address affordability challenges, supporting market penetration in price-sensitive regions.

Key Industry Developments

- In July 2025, Biocon Biologics Ltd (BBL), a fully integrated global biosimilars company and subsidiary of Biocon Ltd., announced that approval had been granted by the U.S. Food and Drug Administration (FDA) for Kirsty™ (Insulin Aspart-xjhz), 100 units/mL, as the first and only interchangeable biosimilar to NovoLog® (Insulin Aspart). Kirsty™ was indicated to improve glycemic control in adult and pediatric patients with diabetes mellitus. The product was made available as a single-patient-use prefilled pen for subcutaneous administration and as a multiple-dose vial for both subcutaneous and intravenous use.

- In November 2023, Lupin launched the world's first fixed-dose triple combination drug for Chronic Obstructive Pulmonary Disease (COPD) management in India, under the brand name Vilfuro-G®. It combines Vilanterol, Fluticasone Furoate, and Glycopyrronium Bromide.

Companies Covered in Fixed-Dose Combination Drugs Market

- Pfizer Inc

- Novartis AG

- GlaxoSmithKline plc

- Bristol-Myers Squibb Company

- Sanofi S.A.

- AstraZeneca PLC

- Merck & Co., Inc.

- Johnson & Johnson

- AbbVie Inc

Frequently Asked Questions

The global fixed-dose combination drugs market is projected to reach US$112.3 billion in 2026.

The rising prevalence of chronic diseases and demand for improved patient adherence are key drivers.

The fixed-dose combination drugs market is poised to witness a CAGR of 3.0% from 2026 to 2033.

Advancements in multi-drug and patient-centric delivery platforms are key opportunities.

Pfizer Inc., Novartis AG, GlaxoSmithKline plc, Bristol-Myers Squibb Company, and Sanofi S.A. are the key players.