- Automotive Components & Materials

- Automotive Rear Combination Lamp Market

Automotive Rear Combination Lamp Market Size, Share, and Growth Forecast, 2025 - 2032

Automotive Rear Combination Lamp Market By Product Type (Traditional Rear Lamps, Laser Rear Lamps, Plasma Rear Lamp), Technology (Reflector Technology, Projector Technology, Matrix Technology), and Regional Analysis for 2025 – 2032

Automotive Rear Combination Lamp Market Size and Trends Analysis

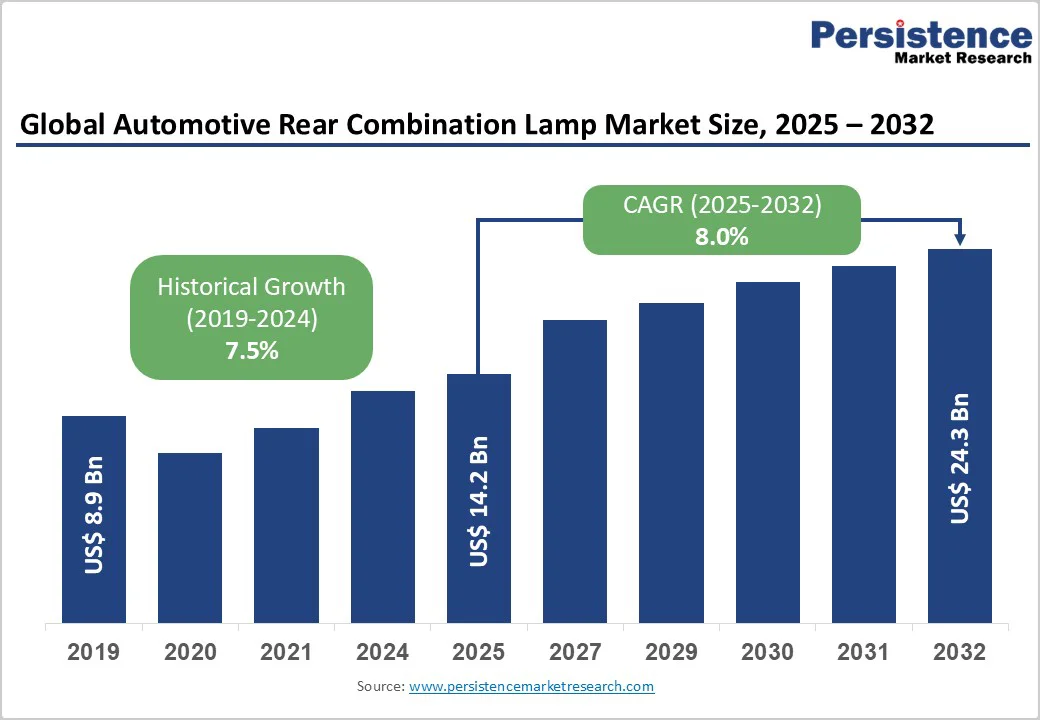

The global automotive rear combination lamp market size is likely to be valued US$14.2 Billion in 2025, projected to US$24.3 Billion by 2032, growing at a CAGR of 8.0% during the forecast period from 2025 to 2032. The automotive rear combination lamp market is experiencing robust growth driven by the increasing prevalence of safety regulations, rising vehicle production, and advancements in lighting technologies. The need for enhanced visibility and aesthetic appeal, particularly in passenger cars, has significantly boosted the adoption of automotive rear combination lamps across various demographics. The market is further propelled by innovations in LED and laser-based designs, catering to preferences for energy-efficient and stylish options. The growing acceptance of automotive rear combination lamps as essential safety features, particularly in EVs, is a key growth factor.

Key Industry Highlights:

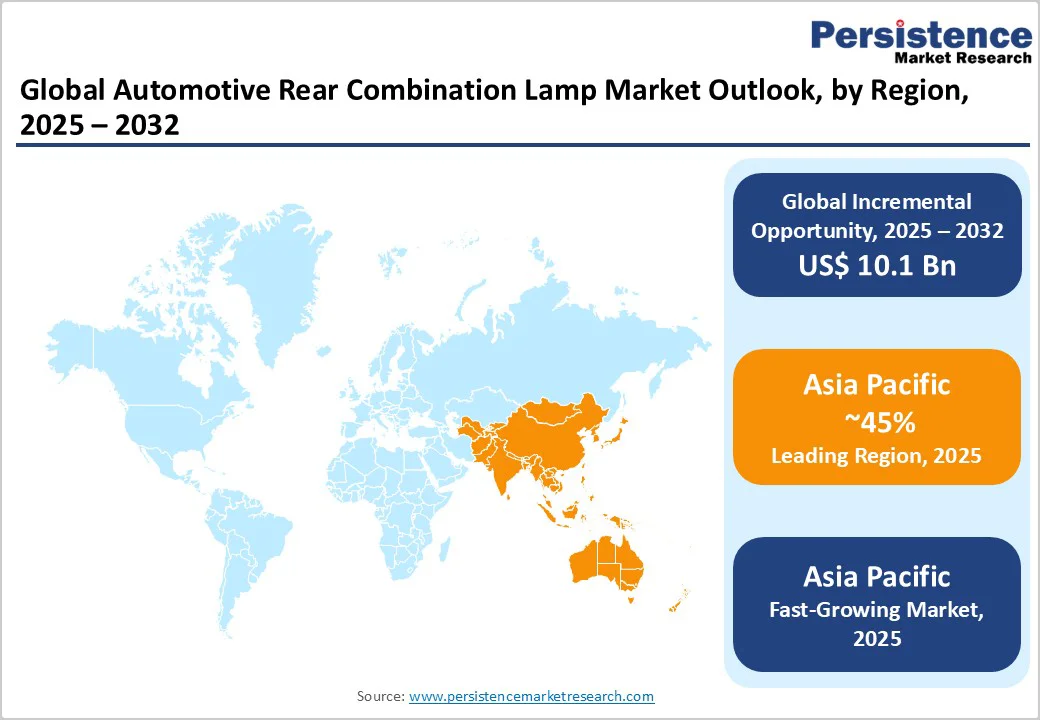

- Leading Region: Asia Pacific, commanding a 45% market share in 2025, driven by massive vehicle manufacturing, high prevalence of LED integrations, and strong R&D activities in China.

- Fastest-growing Region: Asia Pacific is the fastest-growing market due to booming automotive production and expanding consumer demand in countries such as China, India, and Japan.

- Dominant Product Type: Traditional rear lamps, holding approximately 60% of the market share, due to cost-effectiveness and widespread use.

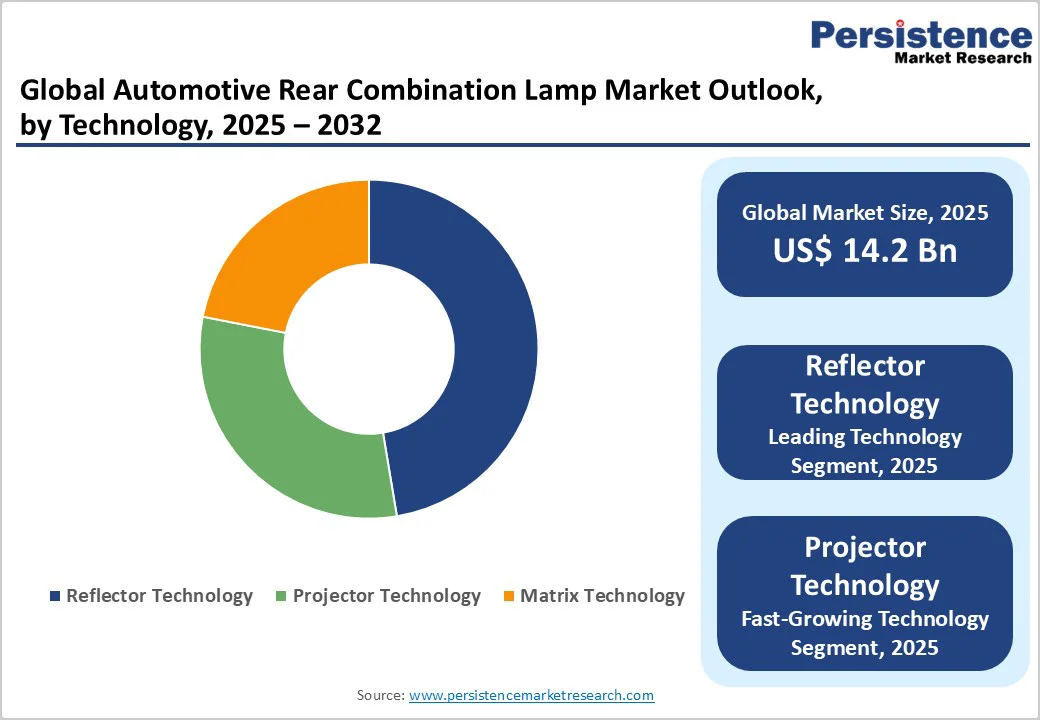

- Leading Technology: Reflector technology, accounting for over 50% of market revenue, driven by reliability in mass production.

- Key Market Driver: Stringent safety and visibility regulations worldwide are accelerating the demand for advanced, durable, and high-performance automotive lighting solutions.

- Market Opportunity: Advancements in OLED and adaptive lighting technologies create scope for premium, customizable rear combination lamps across global markets.

| Key Insights | Details |

|---|---|

| Automotive Rear Combination Lamp Market Size (2025E) | US$14.2 Bn |

| Market Value Forecast (2032F) | US$24.3 Bn |

| Projected Growth (CAGR 2025 to 2032) | 8.0% |

| Historical Market Growth (CAGR 2019 to 2024) | 7.5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Prevalence of Safety Regulations and Demand for Enhanced Vehicle Lighting

The increasing prevalence of safety regulations globally is a primary driver of the automotive rear combination lamp market. Governments and regulatory authorities across regions including the U.S. NHTSA, European Union (EU), and Asia-Pacific transport bodies are enforcing stricter standards for vehicle visibility, signaling, and energy efficiency to reduce road accidents and improve night-time driving safety. These regulations encourage automakers to adopt advanced lighting technologies such as LED, OLED, and laser-based systems, which offer superior brightness, faster response times, and greater reliability than traditional halogen lamps.

The increasing production of electric and autonomous vehicles is driving the integration of smart rear lighting systems capable of adaptive illumination and communication functions. Consumers are also becoming more aware of vehicle safety features, fueling demand for enhanced lighting aesthetics that combine functionality with design appeal.

High Development and Integration Costs

The high costs associated with development and integration of automotive rear combination lamps pose a significant restraint on market growth. Developing these lamps requires advanced LED arrays, rigorous durability testing, and seamless integration with vehicle systems. These processes involve substantial financial investment, often exceeding millions of dollars, which can be a barrier for smaller manufacturers. Regulatory bodies impose stringent requirements for photometric performance and EMC compliance.

Compliance with these standards, along with the need for specialized testing facilities, increases overall costs and extends development timelines. For instance, certifying matrix technology lamps for EVs can take years, with costs escalating due to multiple phases of light distribution trials. Smaller firms struggle against players such as OSRAM GmbH. Complexity of multi-color LEDs adds to production challenges, deterring innovation in cost-sensitive regions.

Advancements in LED and Laser-Based Lighting Technologies

Advancements in LED and laser-based lighting technologies present significant growth opportunities for the automotive rear combination lamp market. LED lamps offer superior energy efficiency, longer lifespan, and compact design flexibility, making them ideal for modern, sustainable vehicles. Their integration with smart lighting systems supports adaptive brightness and connectivity features, enhancing both safety and style. Meanwhile, laser-based lighting provides high-intensity, focused beams that deliver exceptional visibility and precision in compact assemblies.

For example, companies Peterson Manufacturing Company and LED Autolamps Europe LLP are investing in R&D for laser-integrated lamps combining brightness with durability. These reduce timelines via modular optics. Furthermore, adaptive features enhance safety. As demand for innovative lighting grows, these drive expansion in regions such as Asia Pacific and Europe.

Category-wise Analysis

Product Type Insights

Traditional rear lamps dominates the market, accounting for 60% of the share in 2025. Its dominance is driven by cost-effectiveness, reliability, and mass production suitability, making it preferred for passenger cars. Traditional rear lamps, such as those from Gordon Equipments Limited (Durite), provide basic functionality, ensuring compliance. Its simplicity and integration make it preferred for manufacturers.

Laser rear lamps is the fastest-growing segment, driven by compact design and increasing adoption in premium vehicles. Laser rear lamps offer high intensity, appealing for aesthetics. Focus on premium innovation accelerates adoption in Europe and North America.

Technology Insights

Reflector technology leads the market, holding 50% of the share in 2025, due to its cost efficiency, simplicity, and ease of mass production. Widely used in standard and mid-range vehicles, reflector systems offer reliable illumination for basic lighting needs, with rising demand driven by affordability and consistent performance in large-scale manufacturing.

Projector technology is the fastest-growing segment, driven by its ability to deliver focused light beams and sharp cutoffs for improved visibility and safety. Its growing adoption in luxury and premium vehicles is fueled by enhanced aesthetic appeal, energy efficiency, and advanced optical performance, making it a preferred choice for modern automotive lighting systems.

Regional Insights

Asia Pacific Automotive Rear Combination Lamp Market Trends

Asia Pacific is commands 45% share in 2025, driven by surging vehicle production, rapid urbanization, and the expanding presence of electric and hybrid vehicles across countries such as China, Japan, India, and South Korea. The region leads global automotive manufacturing, creating substantial demand for advanced lighting solutions that enhance both safety and aesthetics. Manufacturers are increasingly adopting LED and OLED technologies, which offer higher energy efficiency, longer lifespan, and improved design flexibility compared to traditional halogen systems.

Local companies are investing in cost-effective, mass-production capabilities, while global players collaborate with regional partners to localize manufacturing and reduce production costs. The rise of connected and autonomous vehicles further fuels innovation in smart lighting systems with adaptive brightness and communication features. Government regulations promoting road safety and energy-efficient lighting are propelling the adoption of modern rear lamp systems.

North America Automotive Rear Combination Lamp Market Trends

North America is account for nearly 25% share in 2025, driven by increasing demand for vehicle safety, energy-efficient lighting, and advanced design integration. The United States leads the region’s market, supported by strong automotive manufacturing and continuous investment in smart and adaptive lighting technologies. The growing adoption of LED and OLED-based rear lamps is reshaping design aesthetics while improving visibility, durability, and energy savings.

Manufacturers such as OSRAM, HELLA, and Magna International are focusing on developing intelligent lighting systems that enhance vehicle-to-vehicle communication and support autonomous driving features. The rise of electric vehicles (EVs) and stringent National Highway Traffic Safety Administration (NHTSA) regulations for improved road safety are accelerating the use of advanced rear lighting solutions. Consumers are also demanding enhanced styling and customization, prompting automakers to integrate innovative, high-performance lighting designs.

Europe Automotive Rear Combination Lamp Market Trends

Europe accounts 20% share in 2025, supported by strong regulatory standards, advanced automotive engineering, and the region’s commitment to sustainable mobility. Countries such as Germany, France, and Italy lead innovation with premium vehicle manufacturers emphasizing aesthetic design, safety compliance, and energy efficiency. The growing adoption of LED, OLED, and laser lighting technologies is transforming rear combination lamp designs, allowing for lightweight structures, superior brightness, and lower power consumption.

Strict EU safety and environmental regulations, including directives on visibility and vehicle emissions, are driving automakers to integrate intelligent lighting systems with adaptive and communication capabilities. The shift toward electric and hybrid vehicles across Western Europe further amplifies demand for advanced rear lighting solutions that enhance efficiency and styling appeal. Collaborations between automotive OEMs and lighting specialists such as HELLA, OSRAM, and Valeo are fostering product innovation and sustainability.

Competitive Landscape

The global automotive rear combination lamp market is highly competitive, comprising a blend of established lighting giants and specialized regional manufacturers. In North America and Europe, leading players such as HELLA KGaA Hueck & Co. and OSRAM GmbH dominate the market through strong R&D capabilities, advanced design expertise, and well-established distribution networks. These companies focus on developing energy-efficient LED and OLED lighting solutions that meet evolving automotive safety and aesthetic standards.

In the Asia Pacific region, manufacturers such as Automotive Lighting Italia S.p.A. are gaining traction by offering cost-effective, localized solutions tailored to diverse automotive segments, including electric and compact vehicles. The market is witnessing a rapid shift toward smart and adaptive lighting systems, integrating sensors and connectivity features for enhanced vehicle communication and safety. Furthermore, strategic partnerships, mergers, and acquisitions are reshaping the competitive landscape, allowing companies to expand global footprints and technological portfolios.

Key Industry Developments

- In September 2024, Global automotive supplier FORVIA HELLA has brought an RGB LED rear combination lamp with full-color light animations into series production in China for the first time. It boasts a variety of new light-based functionalities and thus addresses the increasing demand for new opportunities for brand differentiation and personalization. The RGB LED rear combination lamp is used in the new luxury C-class sedan Z10 of LYNK & CO, a brand of the car manufacturer Geely Auto Group (collectively referred to as “Geely”).

- In February 2025, ams OSRAM has reached another important milestone in automotive lighting now that the new OSRAM XLS LR6 LED is ready for series production. This innovative solution enables car manufacturers to create impressive lighting designs with improved safety features, as evidenced by a specially developed prototype for tail lighting, the OSRAM XLS demonstrator.

Companies Covered in Automotive Rear Combination Lamp Market

- HELLA KGaA Hueck & Co.

- Peterson Manufacturing Company

- LED Autolamps Europe LLP

- OSRAM GmbH

- Gordon Equipments Limited (Durite)

- Lucidity Enterprise Co.

- PROPLAST Fahrzeugbeleuchtung GmbH

- Automotive Lighting Italia S.p.A