- Food Ingredients & Additives

- Citrus Pectin Market

Citrus Pectin Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Citrus Pectin Market by Product Type (High Methoxyl Pectin, Low Methoxyl Pectin), by Source (Oranges, Tangerines/Mandarins, Grapefruit, Lemon and Lime), by Application (Food & Beverages, Pharmaceuticals & Nutraceuticals, Personal Care & Cosmetics, Industrial Applications), by Regional Analysis, 2026-2033

Citrus Pectin Market Share and Trends Analysis

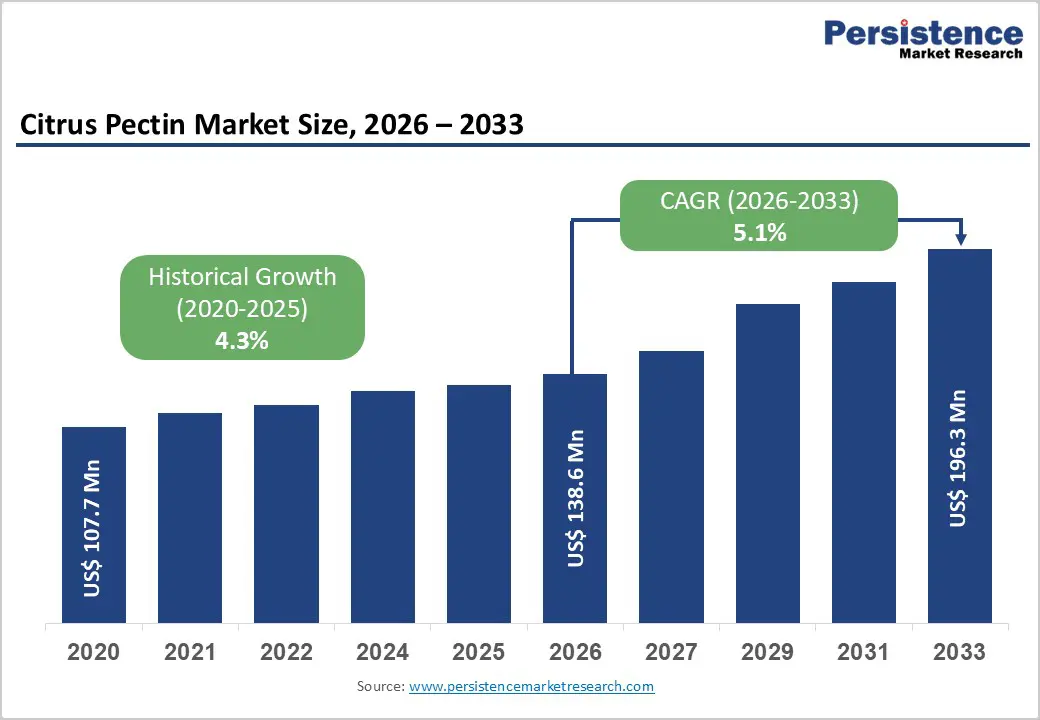

The global Citrus Pectin market is expected to be valued at US$ 138.6 million in 2026 and projected to reach US$ 196.3 million by 2033, growing at a CAGR of 5.1% between 2026 and 2033.

The market is primarily propelled by the clean-label revolution and a systemic shift toward plant-based stabilizers in the global food processing industry. Manufacturers are increasingly replacing synthetic gelling agents with citrus-derived polysaccharides to meet stringent FDA and EFSA transparency requirements. Furthermore, the rising integration of modified citrus pectin (MCP) in oncology and cardiovascular research is opening high-value revenue pockets within the pharmaceutical sector.

Key Industry Highlights

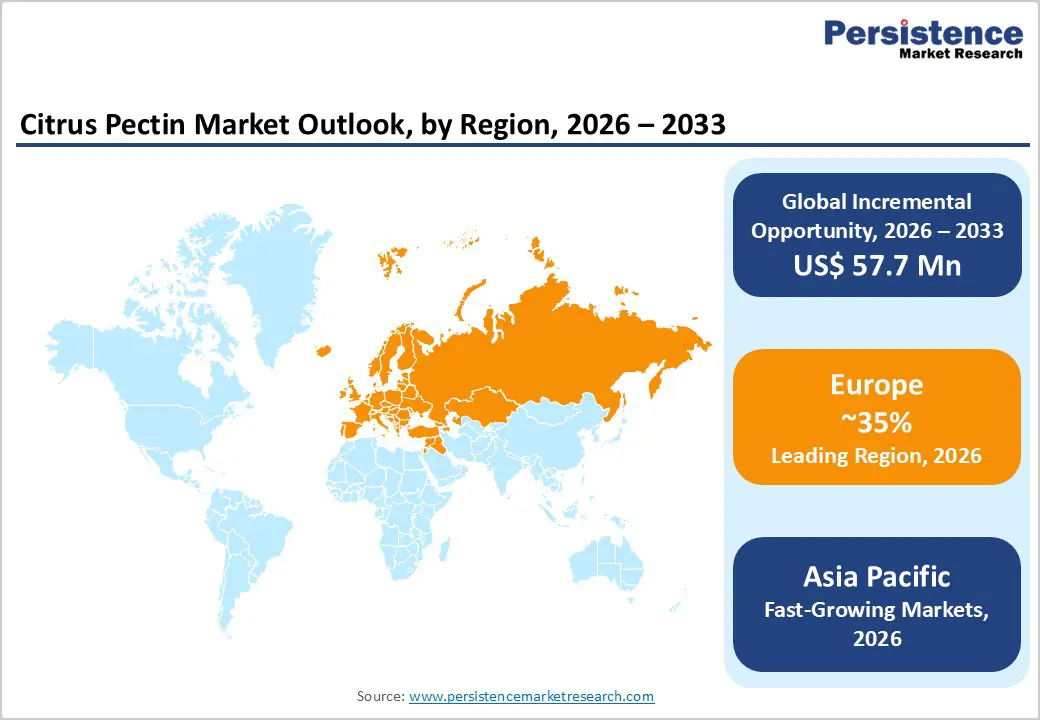

- Leading Region: Europe dominates the landscape with a 35% share, driven by stringent food safety standards and a mature market for premium fruit-based confectionery and bakery items.

- Fastest Growing Region: Asia Pacific is the primary growth engine, fueled by the rising middle-class population and rapid industrialization in the food processing sectors of China and India.

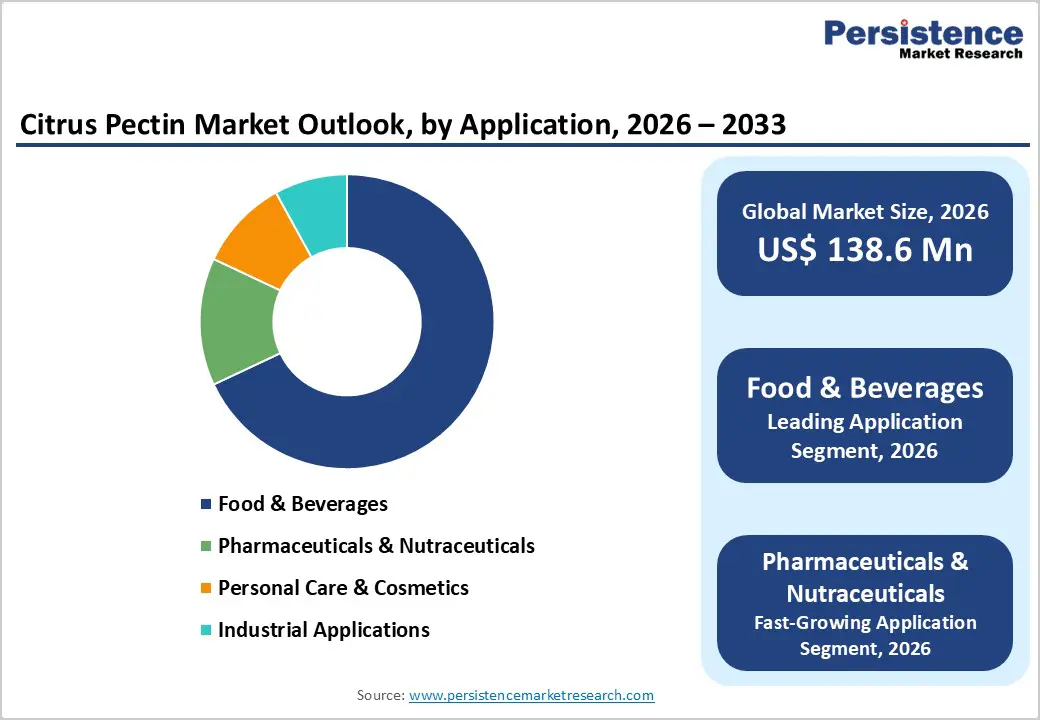

- Dominant Segment: The Food & Beverages application segment remains the largest revenue contributor, essential for the stability and texture of billions of processed food units globally.

- Fastest Growing Segment: Pharmaceuticals & Nutraceuticals is the most dynamic category, as clinical research validates the use of modified citrus pectin in high-value medical treatments.

- Key Market Opportunity: The integration of citrus pectin into plant-based meat analogs offers a significant revenue pocket as manufacturers seek natural, moisture-retentive stabilizers to mimic animal fats.

| Key Insights | Details |

|---|---|

| Global Citrus Pectin Market Size (2026E) | US$ 138.6 Mn |

| Market Value Forecast (2033F) | US$ 196.3 Mn |

| Projected Growth (CAGR 2026 to 2033) | 5.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.3% |

Market Dynamics

Driver – Expansion in Nutraceutical and Pharmaceutical Formulations

Beyond food, the pharmaceutical industry is increasingly leveraging the bio-functional properties of citrus pectin for drug delivery systems and specialized health supplements. Research published in various medical journals highlights the efficacy of Modified Citrus Pectin (MCP) in inhibiting galectin-3, a protein associated with cancer metastasis and heart fibrosis.

This clinical potential has transformed pectin from a simple food additive into a high-value active pharmaceutical ingredient (API). Statistics from the National Institutes of Health (NIH) suggest that the uptick in clinical trials involving pectin-based encapsulated delivery systems is a significant contributor to market momentum. The ability of pectin to act as a soluble fiber that supports digestive health further cements its position in the rapidly growing US$ 450 billion global nutraceutical market.

Restraints – Complexity in Extraction and High Production Costs

Producing high-purity pharmaceutical or food-grade pectin requires sophisticated acid extraction and alcohol precipitation processes that are energy-intensive. The high capital expenditure (CAPEX) required to establish manufacturing facilities that meet Good Manufacturing Practices (GMP) standards limits the entry of new players.

Furthermore, the strict environmental regulations regarding wastewater treatment from pectin extraction plantsparticularly in European Union countries add a significant operational cost layer. These overheads often make citrus pectin more expensive than other hydrocolloids, hindering its adoption in low-cost beverage segments where profit margins are traditionally thin.

Opportunity – Emergence of Personalized Nutrition and Functional Gummies

The pill fatigue among consumers has led to a massive shift toward functional gummies and chewable supplements. According to industry data from Persistence Market Research, the gummy delivery format is outperforming traditional tablets in the vitamins, minerals, and supplements (VMS) space.

Pectin is the preferred gelling agent for these products because it offers a superior flavor release and a higher melting point compared to gelatin, making it ideal for tropical climates. This presents a massive opportunity for pectin suppliers to partner with nutraceutical brands to develop organic, vegan-certified citrus pectin gummies that cater to the Gen Z and Millennial demographics who prioritize ethical and plant-based consumption.

Category-wise Analysis

Product Type Analysis

The High Methoxyl Pectin (HMP) segment currently leads the market, accounting for a dominant 62% market share in 2025. The justification for this leadership lies in its indispensable role in high-acid environments, such as traditional jams, jellies, and carbonated fruit drinks. HMP requires a high sugar concentration and a low pH to form a gel, which aligns perfectly with the largest existing application bases in the fruit preserves industry.

However, the Low Methoxyl Pectin (LMP) segment is gaining rapid traction as manufacturers move toward low-sugar and sugar-free formulations. Since LMP gels in the presence of calcium rather than sugar, it is the primary choice for the growing diet and light food categories globally.

Application Analysis

The Food & Beverages segment remains the leading application category, holding a substantial 69% market share as of 2025. Pectin's multifaceted functionality as a gelling agent, thickener, and stabilizer in dairy, bakery, and beverage products makes it a staple in food science. Conversely, the Pharmaceuticals & Nutraceuticals segment is identified as the fastest-growing application area.

With a projected high growth rate through 2032, this segment is fueled by the clinical adoption of modified citrus pectin for heavy metal detoxification and its use in advanced wound care dressings and gastrointestinal treatments.

Region-wise Insights

Europe Citrus Pectin Market Trends and Insights

Europe is the leading regional market, holding a 35% share in 2025. The region's dominance is underpinned by a highly sophisticated food processing industry and early adoption of clean-label regulations. Germany and France are the key consumers, driven by the strong presence of global ingredient leaders and a cultural preference for high-quality fruit preserves and artisanal bakery products.

The regulatory environment in Europe is harmonized under the European Commission (EC), which provides a stable framework for the use of food additives (E440). This harmonization allows manufacturers to distribute pectin-based products seamlessly across the European Economic Area (EEA). Furthermore, the European market is seeing a surge in organic-certified pectin demand, as consumers increasingly shift toward chemical-free and sustainably sourced food ingredients.

Asia Pacific Citrus Pectin Market Trends and Insights

The Asia Pacific region is the fastest-growing market for citrus pectin. This growth is catalyzed by the rapid urbanization in China and India and the corresponding increase in the consumption of processed and convenience foods. The westernization of diets in the ASEAN region has led to a boom in the bakery and confectionery sectors, where pectin is a critical ingredient for fruit fillings and glazes.

Manufacturing advantages in China, which is a global leader in mandarin and tangerine production, provide a significant cost benefit for regional pectin extraction. Moreover, the burgeoning pharmaceutical industry in India is increasingly incorporating pectin in liquid formulations and chewable supplements, reflecting the region's dynamic shift toward functional wellness products.

Market Competitive Landscape

The global citrus pectin market is moderately consolidated, with a few tier-1 players like CP Kelco, Cargill, and IFF controlling nearly 45% of the global output. These market leaders employ strategies of backward integration securing long-term contracts with citrus growers in Brazil and Mexico to mitigate raw material price risks.

There is a strong emphasis on R&D for modified and specialty pectins that can function in challenging environments, such as low-pH dairy alternatives. Emerging players are increasingly adopting circular economy business models, focusing on zero-waste extraction processes to appeal to environmentally conscious brand owners.

Key Developments:

- In July 2025, CEAMSA reinforced its commitment to innovation in natural-origin ingredients through its participation in IFT FIRST 2025 in Chicago, USA. The presence highlighted CEAMSA’s expanding global footprint and underscored its strategic role in delivering functional, value-added ingredient solutions to the food and beverage industry.

Companies Covered in Citrus Pectin Market

- Cargill Inc.

- IFF

- Givaudan

- Tate & Lyle

- Ceamsa

- Herbstreith & Fox KG Pektin-Fabriken

- Yantai Andre Pectin Co. Ltd.

- Silvateam S.p.a.

- Florida Food Products, Inc.

- Herbafood Ingredients GmbH

- Fiberstar, Inc.

- Lucid Colloids Ltd.

- Others

Frequently Asked Questions

The global Citrus Pectin market is projected to be valued at US$ 138.6 Mn in 2026.

Expansion in Nutraceutical and Pharmaceutical Formulations is driving demand for Citrus Pectin market.

The Global Citrus Pectin market is poised to witness a CAGR of 5.1% between 2026 and 2033

Emergence of Personalized Nutrition and Functional Gummies is key opportunity for key players in the market.

The market is led by global giants such as Cargill Inc., IFF, Tate & Lyle, and specialized manufacturers like Ceamsa and Herbstreith & Fox.