- Biotechnology

- Chromatography Systems Market

Chromatography Systems Market Size, Share, and Growth Forecast, 2025 - 2032

Chromatography Systems Market By Product Type (Liquid, Gas, Supercritical Fluid, Thin-layer), Modality (Single Use, Multiple Use, Continuous, High-performance), Usage (Process Development, Commercial), End-user, and Regional Analysis for 2025 - 2032

Chromatography Systems Market Size and Trends Analysis

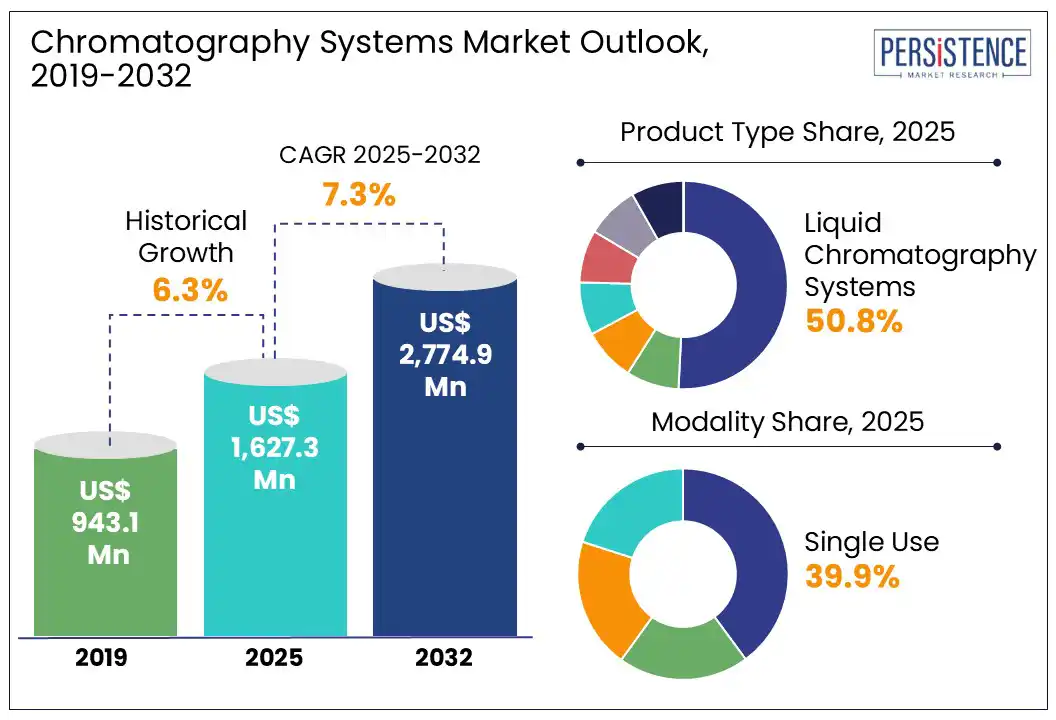

The global chromatography systems market size is projected to rise from US$ 1,627.3 Mn in 2025 to US$ 2,774.9 Mn by 2032. It is anticipated to witness a CAGR of 7.3% during the forecast period from 2025 to 2032. Chromatography systems have become indispensable tools in drug discovery, disease diagnostics, and therapeutic manufacturing, transforming into a cornerstone of precision medicine.

As of 2024, over 70% of biopharmaceutical companies in North America and Europe are using novel chromatography platforms for quality control and bioanalytical testing that comply with regulatory standards. The increasing complexity of biologics, the rise of cell and gene therapies, and the high demand for rapid analytics are driving this trend.

Key Industry Highlights:

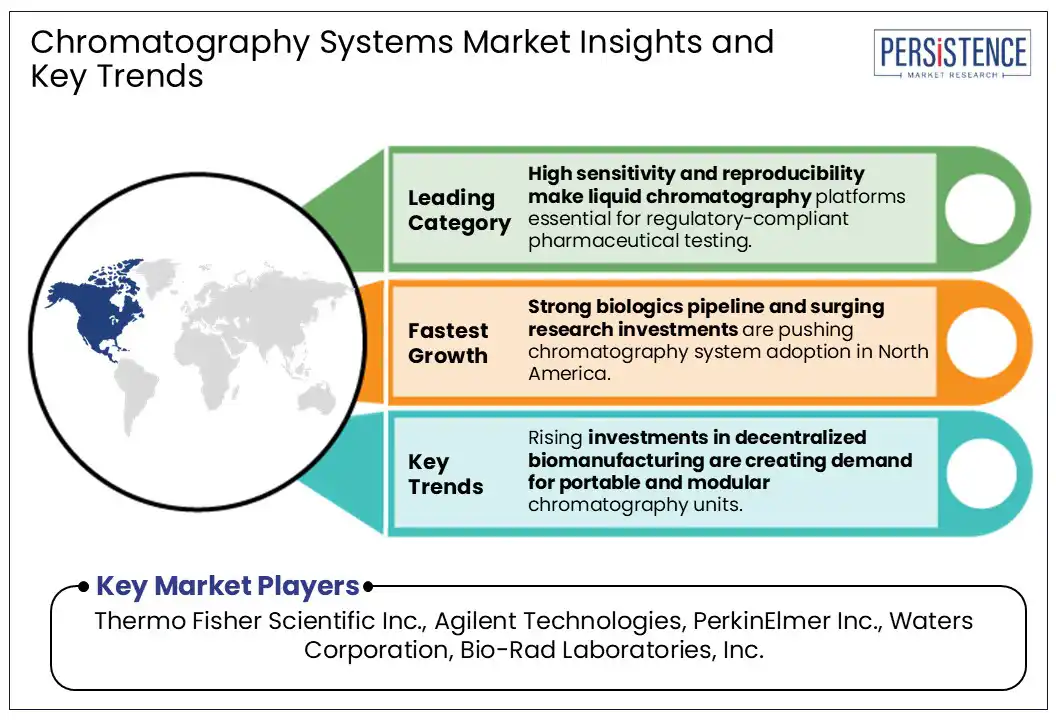

- Dominant Region: In North America, stringent FDA quality standards are prompting investments in high-resolution, GMP-compliant analytical systems.

- Dominant Modality Type: Single-use systems are expected to account for nearly 39.9% share in 2025, due to their ability to reduce cross-contamination risk in multi-product biologics facilities.

- Leading Product Type: Liquid chromatography is highly preferred as it enables precise analysis of large, non-volatile biologics such as monoclonal antibodies and peptides.

- Regulatory Scenario: Increasing regulatory scrutiny on impurity profiling is pushing pharmaceutical companies to adopt high-performance chromatography systems.

- Rise in Chronic Diseases: The rising prevalence of chronic diseases is expanding the use of chromatography in biomarker discovery and validation.

- Adoption of Complex Biologics: Surge in clinical trials for complex biologics boosts the demand for robust and reproducible chromatography solutions.

|

Global Market Attribute |

Key Insights |

|

Chromatography Systems Market Size (2025E) |

US$ 1,627.3 Mn |

|

Market Value Forecast (2032F) |

US$ 2,774.9 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

7.3% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.3% |

Market Dynamics

Driver - Automated Sample Prep and Data Handling to Accelerate Demand

The increasing adoption of automated sample preparation and data analysis is significantly propelling the chromatography systems market growth. Automation reduces human errors, enhances throughput, and ensures data integrity, all of which are key requirements in highly regulated environments such as cGMP-compliant labs and FDA-audited manufacturing facilities. Clinical laboratories are increasingly deploying fully automated chromatography systems to cope with the growing test volume and complexity of assays.

The Mayo Clinic Laboratory, for example, recently incorporated LC-MS systems with robotic sample prep to streamline therapeutic drug monitoring and toxicology screening. The integration reduced the turnaround time by 35% and significantly lowered inter-technician variability. These integrations are now becoming standard in high-throughput healthcare labs managing chronic disease diagnostics and personalized medicine assays. Additionally, automation is fostering remote and decentralized analytical setups in hospital research labs and CROs.

Restraint - High Sensitivity to Contaminants Restricts Chromatography Adoption

In the healthcare sector, the extreme sensitivity of chromatography systems to contaminants is predicted to hamper widespread adoption. High-performance systems such as UPLC and LC-MS/MS are capable of detecting trace levels of impurities. This often makes them prone to false positives or system errors if slight contamination occurs. In clinical bioanalysis, for instance, residual detergent from sample vials or plasticizers from tubing can lead to baseline drifts or ghost peaks, compromising the reliability of patient diagnostics.

Hospitals and mid-tier diagnostic labs in developing countries often lack access to ultra-pure solvents, certified reference standards, or cleanroom-level environments. This raises maintenance costs and increases downtime due to frequent troubleshooting or column replacement. In the context of biologics and biosimilars, contaminant interference leads to delays in batch release or batch rejection. For example, monoclonal antibody production often involves protein A affinity chromatography, where trace contaminants in the elution buffer can mask or distort purity profiles.

Opportunity - Environmental Pressures Prompt Companies to Pilot Green Chromatography

The development of green chromatography is generating new opportunities within the healthcare sector, as regulatory authorities and pharmaceutical companies intensify efforts to reduce environmental impact without compromising analytical accuracy. A key area of innovation involves reducing the use of toxic solvents, which are conventionally used in high volumes for mobile phases in High-Performance Liquid Chromatography (HPLC) and Gas Chromatography (GC) workflows. Companies are now investing in systems designed to operate with aqueous or ethanol-based solvents that are less hazardous.

Recently, Agilent Technologies launched LC systems under its InfinityLab Eco portfolio, which reduce solvent use by up to 50%. This helps in directly addressing sustainability concerns in pharmaceutical quality control labs. Moreover, green chromatography aligns with the growing trend toward continuous manufacturing in the healthcare sector. Recently, Pfizer’s clinical manufacturing unit in the U.S. piloted a green chromatography platform using supercritical fluid chromatography for chiral separations. It significantly reduced solvent waste and turnaround time. The trial showed that sustainable methods can be scaled for high-throughput pharmaceutical environments without compromising on regulatory compliance.

Category-wise Analysis

Product Type Insights

By product type, the market is divided into liquid, gas, supercritical fluid, thin-layer chromatography columns, auto-sampling systems, and consumables and accessories. Out of these, liquid chromatography systems are predicted to hold approximately 50.8% of the chromatography systems market share in 2025, due to their superior ability to separate, identify, and quantify structurally complex and thermally unstable compounds. It enables analysis of peptides, proteins, monoclonal antibodies, and other biomolecules without chemical modification or degradation. This is important in the development and quality control of biologics.

Gas chromatography systems are expected to witness steady growth through 2032, with their unmatched precision in volatile compound analysis. The requirement for rigorous residual solvent testing as mandated by ICH Q3C guidelines is another key driver. With the rise in outsourcing of pharmaceutical manufacturing to Contract Development and Manufacturing Organizations (CDMOs), gas chromatography has become a significant tool for verifying compliance with solvent thresholds before batch release.

Modality Insights

Based on modality, the chromatography systems market is divided into single use, multiple use, continuous, and high-performance. Among these, single-use systems are estimated to hold nearly 39.9% of market share in 2025, due to their ability to reduce cross-contamination risks, accelerate turnaround times, and enhance operational flexibility. These eliminate the requirement for rigorous cleaning validation between production batches, a process that is both time-consuming and costly. It is particularly advantageous in multiproduct facilities or clinical trial manufacturing units where frequent changeovers are required.

High-performance systems are playing a key role in healthcare owing to their ability to analyze complex biologics, detect trace-level impurities, and ensure regulatory compliance in pharmaceutical development. As the molecular complexity of therapeutics increases, conventional systems often fall short in resolution and throughput. As a result, healthcare and biopharma companies are upgrading to high-performance platforms capable of separating closely related compounds with exceptional sensitivity and speed.

Regional Insights

North America Chromatography Systems Market Trends

In 2025, North America is expected to capture around 40.5% of the market share, driven by growth in biologics manufacturing, stringent FDA regulations, and a stronger emphasis on quality assurance in pharmaceutical production. The U.S. chromatography systems market is expected to lead the region, backed by biopharmaceutical research and development activities as well as the expansive network of CDMOs. According to the Congressional Budget Office, biologics account for nearly 40% of all prescription drug spending in the U.S. as of 2024.

It significantly influences the adoption of HPLC and GC in quality control and characterization workflows. The U.S. has also witnessed a marked rise in chromatography use for biosimilar development, primarily after the Inflation Reduction Act (2022) introduced measures to control drug pricing. It propelled pharmaceutical companies to accelerate biosimilar pipelines. Thermo Fisher Scientific, for instance, extended its chromatography system capabilities in its North Carolina biologics site in 2023. It aimed to support both small-molecule and large-molecule drug development under cGMP standards.

Europe Chromatography Systems Market Trends

The market in Europe is being shaped by a strong regulatory framework, rising biologics production, and increasing investments in personalized medicine. The European Medicines Agency (EMA)’s rigorous standards for impurity profiling, genotoxicity assessment, and bioequivalence studies are directly boosting the adoption of novel chromatography systems. Germany remains the hub of chromatography usage in healthcare, mainly due to its concentration of pharmaceutical giants and clinical research institutes.

In 2023, for example, Merck KGaA introduced its Milli-Q HR Lab Water Purification system with integrated LC-MS compatibility to support biopharmaceutical QC laboratories. Similarly, Sartorius continued to scale its chromatography resin and equipment solutions made for continuous bioprocessing. The U.K.’s investment in precision oncology through the NHS Genomic Medicine Service has further led to the surging use of chromatography-mass spectrometry for biomarker validation in clinical settings.

Asia Pacific Chromatography Systems Market Trends

Asia Pacific is anticipated to showcase rapid growth due to ongoing biologics manufacturing, rising clinical trial activity, and government-backed pharmaceutical industrialization. China, India, South Korea, and Singapore are investing heavily in domestic drug development and vaccine production infrastructure. In such settings, chromatography plays a key role in impurity profiling, Active Pharmaceutical Ingredient (API) validation, and stability testing.

China’s National Medical Products Administration (NMPA), for example, revised its drug review framework in 2023. It mandated strict analytical validation, resulting in a high demand for GMP-compliant chromatography platforms. India, one of the world’s leading producers of generics and biosimilars, is increasingly using chromatography systems for pharmacokinetics and bioequivalence studies. According to data from the Indian Clinical Trials Registry, the number of registered trials rose by 28% in 2023 compared to the previous year. In response, companies are extending their local manufacturing and training centers to focus on method development for monoclonal antibodies using UPLC systems.

Competitive Landscape

The global chromatography systems market is characterized by strategic consolidation, heavy investments in innovation, and diversification across application areas. Leading players are leveraging proprietary technologies, bundled service offerings, and strong global distribution networks to maintain their positions. They are increasingly focusing on modular and automated systems made for high-throughput applications in pharmaceutical quality control. Surging participation from niche players and regional manufacturers, especially in Asia Pacific, is another significant factor. Companies in this region are gaining impetus by offering cost-effective alternatives and customized solutions for drug development.

Key Industry Developments:

- In March 2025, Axcend introduced its small footprint, full-stack chromatography system. It enables scientists to perform HPLC Anywhere. The system is based on the Axcend Focus LC platform and includes a 40-vial/96-well plate autosampler, a full-spectrum diode array detector, and an in-line process analytical technology monitoring system.

- In May 2024, Agilent Technologies Inc. launched its latest 8850 Gas Chromatograph (GC) System. It is a small, single-channel GC that combines the legacy of the 6850 GC with the capability and system intelligence of the 8890 GC. It expects to revolutionize labs across diverse markets, including pharmaceuticals, food, and energy.

Companies Covered in Chromatography Systems Market

- Thermo Fisher Scientific Inc.

- Agilent Technologies

- PerkinElmer Inc.

- Waters Corporation

- Bio-Rad Laboratories, Inc.

- Merck KGaA

- Sartorius AG

- Tosoh Corporation

- Shimadzu Corporation

- KNAUER Wissenschaftliche Geräte GmbH

- Repligen Corporation

- Bruker

- Biobase Biodusty (Shandong), Co., Ltd.

- O.I. Corporation

- Gilson Incorporated

- Malvern Panalytical Ltd

- CAMAG

- YMC CO., LTD.

Frequently Asked Questions

The chromatography systems market is projected to reach US$ 1,627.3 Mn in 2025.

Increasing preference for hybrid systems and rising adoption of green chromatography methods are the key market drivers.

The chromatography systems market is poised to witness a CAGR of 7.3% from 2025 to 2032.

Emerging applications in breathomics and high demand for chromatography in vaccine quality testing are the key market opportunities.

Thermo Fisher Scientific Inc., Agilent Technologies, and PerkinElmer Inc. are a few key market players.