- Specialty & Fine Chemicals

- Chromatography Resin Market

Chromatography Resin Market Size, Share, and Growth Forecast for 2025 - 2032

Chromatography Resin Market by Product Type (Natural Resins, Synthetic Resins, and Inorganic Resins), Chromatography Technique (Ion exchange, Affinity, Hydrophobic Interaction, Size Reduction, Mixed Mode, and Others), Application (Pharmaceuticals, Biotechnology, Others), and Regional Analysis from 2025 to 2032

Chromatography Resin Market Size and Share Analysis

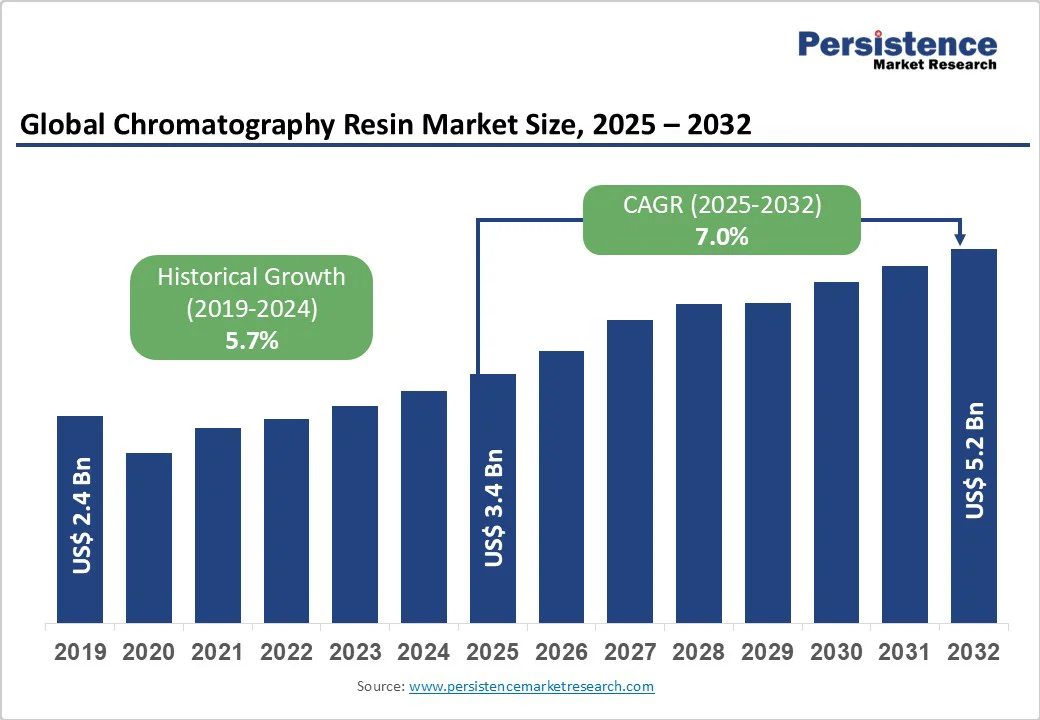

The global chromatography separation resin market size is likely to value at US$ 3.4 billion in 2025 and is projected to reach US$ 5.2 billion by 2032, growing at a CAGR of 7.2% between 2025 and 2032.

Growing demand for biopharmaceuticals, increasing regulatory requirements for high-purity drug substances, and the growing adoption of advanced chromatography techniques across the pharmaceutical and biotechnology industries are some key factors driving the global chromatography separation resin market.

Key Industry Highlights:

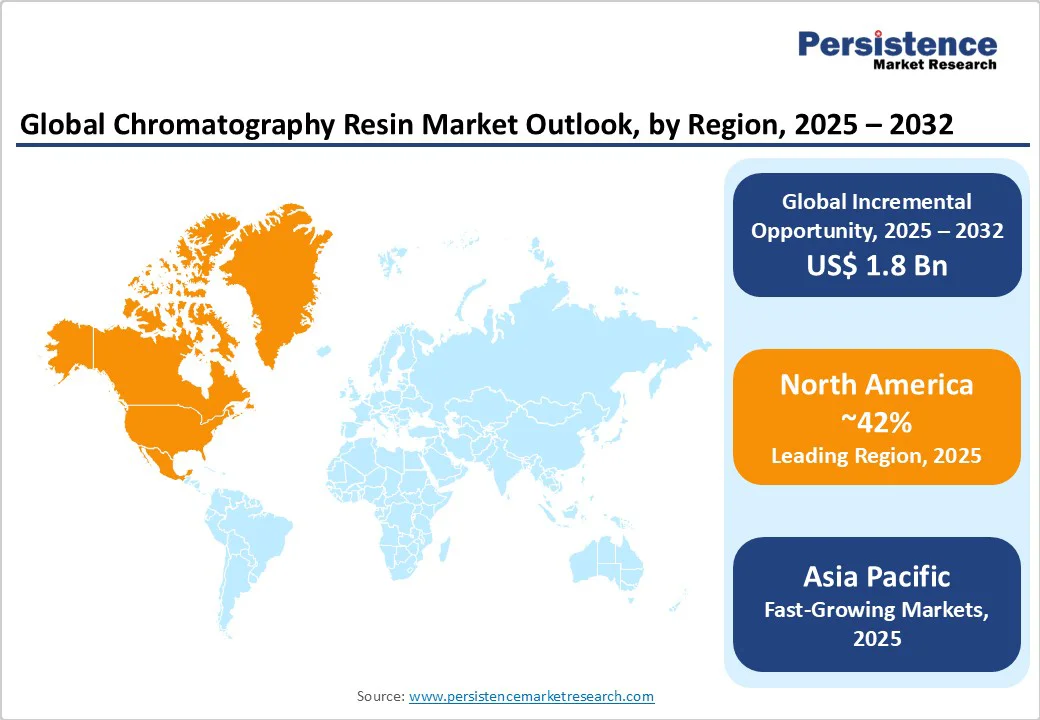

- Regional Leaders: North America dominates the global market with a 42% share in 2024, underpinned by its advanced biopharmaceutical infrastructure, stringent regulatory frameworks, and strong CDMO presence.

- Leading Segments: Synthetic resins lead with a 42% share, driven by their mechanical stability, chemical resistance, and scalable performance essential for large-scale biopharmaceutical manufacturing.

- Technology Performance: Ion-exchange chromatography holds a 32% market share, favored for its proven efficacy in removing host cell impurities, regulatory familiarity, and robust validation protocols.

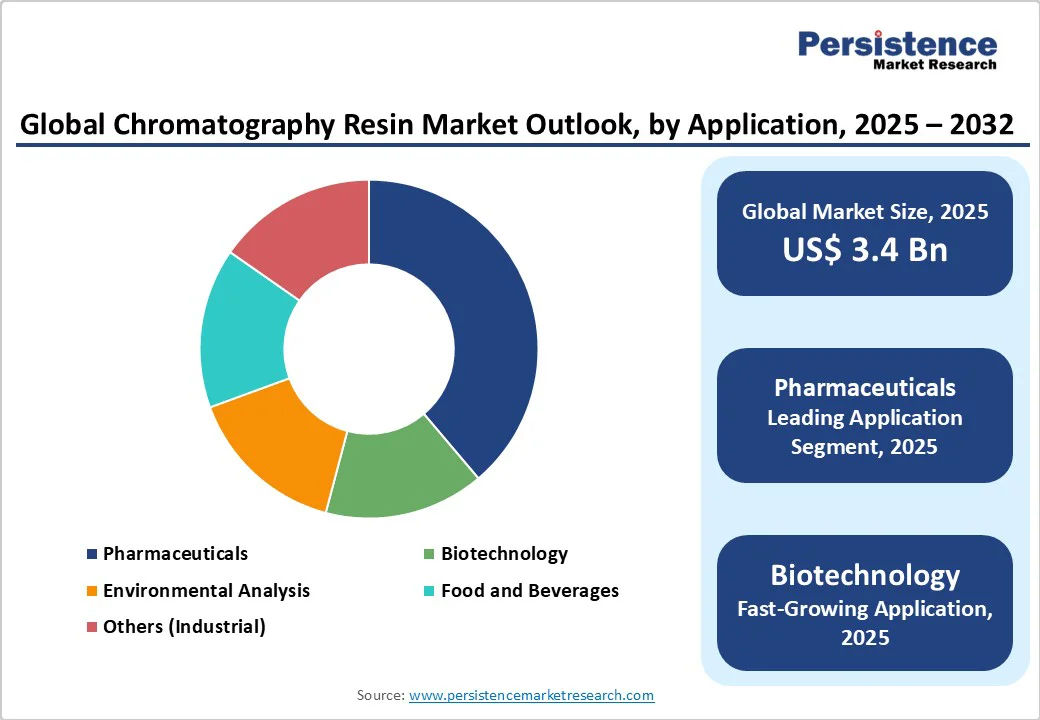

- Industry Applications: The pharmaceuticals sector accounts for 40% of resin consumption, driven by rigorous purity requirements in monoclonal antibody production, vaccine manufacturing, and recombinant protein purification.

- Growth Indicators: Key growth indicators include the surge in monoclonal antibody approvals and biopharmaceutical production, stringent USP <665> and FDA/EMA extractables guidance, and the expanding biosimilar wave fueled by blockbuster patent expirations.

- Challenges: Intensifying competition from alternative purification technologies, such as membrane filtration, single-use systems, and emerging magnetic separation methods.

| Key Insights | Details |

|---|---|

| Chromatography Resin Market Size (2025E) | US$ 3.4 Bn |

| Projected Market Value (2032F) | US$ 5.2 Bn |

| Global Market Growth Rate (CAGR 2025 to 2032) | 7.0% |

| Historical Market Growth Rate (CAGR 2019 to 2024) | 5.7% |

Market Dynamics

Drivers - Accelerating Biopharmaceutical Production and Monoclonal Antibody Development

The exponential growth in biopharmaceutical manufacturing represents the most significant driver for chromatography separation resin demand. FDA approval data indicate that 13 monoclonal antibodies received regulatory clearance in 2024, marking the highest annual approval rate to date.

The rising prevalence of chronic diseases, including cancer and autoimmune disorders, has intensified the need for therapeutic antibodies, with oncology applications accounting for approximately 51% of therapeutic value in the biologics sector.

Protein A resins, essential for monoclonal antibody capture, have witnessed unprecedented demand as antibody titers exceed 10 g/L in manufacturing processes, pushing traditional resin beds to their capacity limits.

The expanding pipeline of bispecific antibodies and antibody-drug conjugates further amplifies purification requirements, while biosimilar production growth, driven by patent expirations of blockbuster drugs like Humira, Avastin, and Herceptin, continues to sustain resin consumption across both innovator and biosimilar manufacturing platforms.

Stringent Regulatory Standards and Quality Control Requirements

Increasingly strict regulatory frameworks enforced by the FDA, EMA, and other global health authorities are driving demand for high-performance chromatography resins that guarantee product safety and efficacy. The implementation of USP <665> guidance addressing plastic components in pharmaceutical manufacturing has heightened awareness of resin extractables and leachables profiles.

Biopharmaceutical manufacturers must demonstrate comprehensive process validation, with chromatography resins playing a critical role in removing process equipment-related leachables (PERLs) and meeting the purity standards required for therapeutic products.

FDA compliance programs specifically target chromatography resins for biotech applications, requiring thorough testing and validation protocols that boost demand for validated, regulatory-compliant resin products.

Restraint - Competition from Alternative Separation Technologies

The chromatography resin market faces increasing competitive pressure from alternative separation and purification technologies that offer potentially lower operational costs and simplified processing workflows. Membrane filtration technologies are gaining traction as cost-effective alternatives for certain applications, particularly in environments where high-resolution separations are not critical.

Continuous manufacturing processes and single-use bioprocessing systems are reshaping traditional chromatography workflows, potentially reducing resin consumption in favor of disposable membrane-based solutions.

Advanced filtration techniques, including ultrafiltration and diafiltration, provide viable alternatives for protein concentration and buffer exchange applications, while precipitation and crystallization methods offer cost-effective purification options for certain pharmaceutical compounds.

The emergence of novel purification technologies based on magnetic separation and expanded bed adsorption further diversifies the competitive landscape, compelling resin manufacturers to continuously innovate and demonstrate superior value propositions.

Opportunity - Expanding Biosimilar Market and Patent Expiration Wave

The impending patent cliff for major biologic drugs presents unprecedented opportunities for chromatography resin manufacturers as biosimilar production scales globally. Patent expirations for blockbuster monoclonal antibodies, including Humira (adalimumab), Avastin (bevacizumab), and Herceptin (trastuzumab), are driving substantial investments in biosimilar manufacturing capabilities worldwide.

Particularly, China, India, and South Korea is experiencing rapid biologics manufacturing expansion, with companies establishing new production facilities to capture biosimilar market opportunities. Contract Development and Manufacturing Organizations (CDMOs) are witnessing increased outsourcing from both innovator and biosimilar companies, creating sustained demand for high-capacity chromatography resins that support multi-product manufacturing platforms.

Technological Advancement in Continuous Bioprocessing and Single-Use Systems

The industry transformation toward continuous bioprocessing and single-use technologies represents a significant growth opportunity for specialized chromatography resin applications. Periodic counter-current chromatography (PCC) and other continuous processing technologies are gaining adoption among biopharmaceutical manufacturers seeking to improve productivity and reduce manufacturing footprints.

Single-use technologies (SUT) adoption is accelerating, with pharmaceutical companies increasingly favoring pre-packed columns and membrane resins to reduce cleaning validation requirements and turnaround times. The development of high-flow resins compatible with continuous chromatography systems addresses the industry's need for process intensification while maintaining separation performance.

Mixed-mode resins offer opportunities to simplify multi-step purification processes, potentially combining capture, intermediate purification, and polishing steps into streamlined workflows that reduce overall processing time and facility requirements.

Category-wise Insights

Product Type Analysis

Synthetic Resins dominate the chromatography separation resin market, accounting for approximately 42% of global market share, driven by their superior performance characteristics and manufacturing scalability. Synthetic polymer-based resins, particularly those utilizing styrene-divinylbenzene and acrylic matrices, offer exceptional mechanical stability, chemical resistance, and reproducible separation performance essential for large-scale biopharmaceutical manufacturing.

Purolite Corporation and other leading manufacturers have developed crosslinked polystyrene-based cation and anion exchangers with uniform spherical bead form that provide consistent separation results across diverse applications.

The synthetic segment's dominance reflects the industry's preference for engineered materials that deliver predictable performance, regulatory compliance, and cost-effective manufacturing economics across pharmaceutical, biotechnology, and industrial applications.

Chromatography Technique Analysis

Ion-Exchange chromatography technique holds 32% share, reflecting its widespread application in protein purification and biomolecule separation processes. Cation exchange chromatography and anion exchange chromatography are extensively utilized in biopharmaceutical manufacturing for removing host cell proteins (HCPs), DNA, endotoxins, and protein aggregates during monoclonal antibody production.

Ion chromatography (IC) applications in biopharmaceutical processing continue expanding, with Thermo Fisher Scientific innovations enabling analysis of anions, organic acids, cations, amino acids, and oligosaccharides without derivatization requirements.

The ion-exchange segment benefits from regulatory familiarity and established validation protocols, making it the preferred choice for commercial-scale manufacturing where process consistency and regulatory compliance are paramount.

Application Analysis

Pharmaceuticals represent the dominant application, accounting for approximately 40% of chromatography separation resin consumption, driven by the industry's rigorous purity requirements and expanding biologics portfolio.

Biopharmaceutical companies extensively utilize chromatography resins for monoclonal antibody purification, vaccine production, recombinant protein manufacturing, and gene therapy applications, where achieving 99%+ purity levels is essential for patient safety and therapeutic efficacy.

Contract research organizations (CROs) and contract development and manufacturing organizations (CDMOs) are experiencing increased demand for chromatography services, with outsourcing trends driving sustained resin consumption across multiple therapeutic programs.

Regional Insights

North America Chromatography Separation Resin Market Trends

North America maintains its position as the leading regional market, commanding approximately 42% of global market share in 2024, driven by the region's advanced biopharmaceutical infrastructure and robust regulatory framework.

The U.S. serves as the primary growth engine, hosting the world's largest concentration of biotechnology companies and pharmaceutical manufacturers, including major players such as Bio-Rad Laboratories, Thermo Fisher Scientific, and Danaher Corporation (Cytiva).

FDA regulatory leadership in establishing chromatography resin standards and validation requirements has created a favorable environment for premium resin adoption, with manufacturers prioritizing validated, high-performance products that ensure regulatory compliance.

Contract development and manufacturing organizations (CDMOs) are experiencing unprecedented growth, with major expansions announced by leading service providers to meet increasing outsourcing demand from both innovator and biosimilar companies.

Europe Chromatography Separation Resin Market Trends

Europe represents the second-largest regional market, accounting for approximately 28% of global market share, characterized by strong regulatory harmonization and advanced manufacturing capabilities across key countries, including Germany, the UK, France, and Spain.

Germany leads European market development, hosting Merck KGaA's global headquarters and the company's €300 million investment in an Advanced Research Center in Darmstadt, focusing on biopharmaceutical manufacturing technologies and chromatography innovation.

The European Medicines Agency (EMA) regulatory framework closely aligns with FDA standards, creating a consistent quality environment that supports premium resin adoption across the region.

European Union sustainability initiatives and green chemistry programs are driving demand for environmentally friendly chromatography resins, with manufacturers increasingly focused on developing biodegradable and renewable resource-based products that align with regional environmental objectives.

Asia Pacific Chromatography Separation Resin Market Trends

Asia Pacific emerges as the fastest-growing regional market, projected to achieve a CAGR of 8.1% through 2032, driven by rapid industrialization, expanding healthcare infrastructure, and increasing biologics manufacturing capabilities.

China leads regional growth with substantial government investments in biopharmaceutical manufacturing, supported by Evergreen New Material's $1.4 billion investment in a styrenics complex designed to enhance regional resin supply chain security.

India is experiencing significant market expansion, with the country's pharmaceutical industry projected to reach $130 billion by 2030, creating substantial opportunities for chromatography resin suppliers.

The Asia-Pacific region benefits from semiconductor-grade ultrapure water demand growth, with Taiwan, South Korea, and Mainland China chip fabrication facilities requiring specialized ion-exchange resins capable of removing boron and trace metals to single-digit parts-per-trillion specifications.

Competitive Landscape for the Chromatography Resin Market

The chromatography separation resin market exhibits a moderately consolidated structure, with the major players controlling approximately 55-60% of global market share, while the remaining 40-45% comprises regional manufacturers and specialized suppliers. There is a growing emphasis among manufacturers on developing advanced chromatography resin technologies to meet the evolving needs of the biopharmaceutical and biotechnology industries.

Companies are increasingly focusing on single-use technologies, continuous bioprocessing compatibility, and alkaline-stable formulations that support extended operational lifecycles, with market differentiation achieved through superior binding capacities, flow rate characteristics, and regulatory support documentation.

Recent Industry Developments

- In May 2024, JNC Corporation exhibited its Cellufine™ chromatography media and introduced the new product line "MLP" at PREP 2024, the 36th International Symposium on Preparative and Process Chromatography, held in Philadelphia, USA, from May 28.

- On June 05, 2023, Waters Corporation and Sartorius announced an expanded collaboration to integrate software and hardware between Waters™ PATROL™ Ultra Performance Liquid Chromatography (UPLC™) Process Analysis System and Sartorius™ Resolute® BioSMB™ multi-column chromatography platform. The collaboration aims to provide bioprocess engineers with more comprehensive analytical data, improving yields, reducing waste, and lowering bio-manufacturing costs through better integration and process control.

- On February 6, 2024, Purolite, an Ecolab company, and Repligen Corporation announced the commercial launch of Praesto® CH1, a groundbreaking 70μm agarose-based affinity resin designed for the purification of specialized monoclonal antibodies (mAbs), including bispecifics and recombinant antibody fragments. This new resin, developed through a multi-year strategic partnership with Repligen, integrates Purolite’s patented Jetted beads manufacturing process with Repligen’s advanced ligand technology.

Companies Covered in Chromatography Resin Market

- Bio-Rad Laboratories

- JNC Corp

- Merck KGaA

- Purolite Corporation

- Danaher Corporation (Cytiva)

- Tosoh Corporation

- Thermo Fisher Scientific Inc.

- Sartorius AG

- Repligen Corporation

- Avantor, Inc.

- W. R. Grace & Co.

- Bestchrom Biosciences Ltd.

- Samyang Corporation

- Sepragen

- Mitsubishi Chemical Corporation

Frequently Asked Questions

The chromatography resin market is set to reach US$ 5.2 Bn by 2032.

North America and Asia Pacific are expected to create significant growth opportunities at the end of 2032.

India is projected to witness a CAGR of 6.7% during the forecast period, 2025 to 2032.

Danaher Corporation (Cytiva) and Bio-Rad Laboratories are considered the leading players.

Pharmaceutical application is estimated to lead the global market in 2025.