- Advanced Materials

- Reverse Phase Chromatography Market

Reverse Phase Chromatography Market Size, Share, Trends, Growth, Regional Forecasts 2025 - 2032

Reverse Phase Chromatography Market by Column Type (C18 Columns, C8 Columns, C4 Columns, and Others), Resin Type (Silica Based and Polymer Based), Particle Size (1-5m, 6-10m, and 11m or Higher), Application and Regional Forecasts for 2025 - 2032

Reverse Phase Chromatography Market Size and Share Analysis

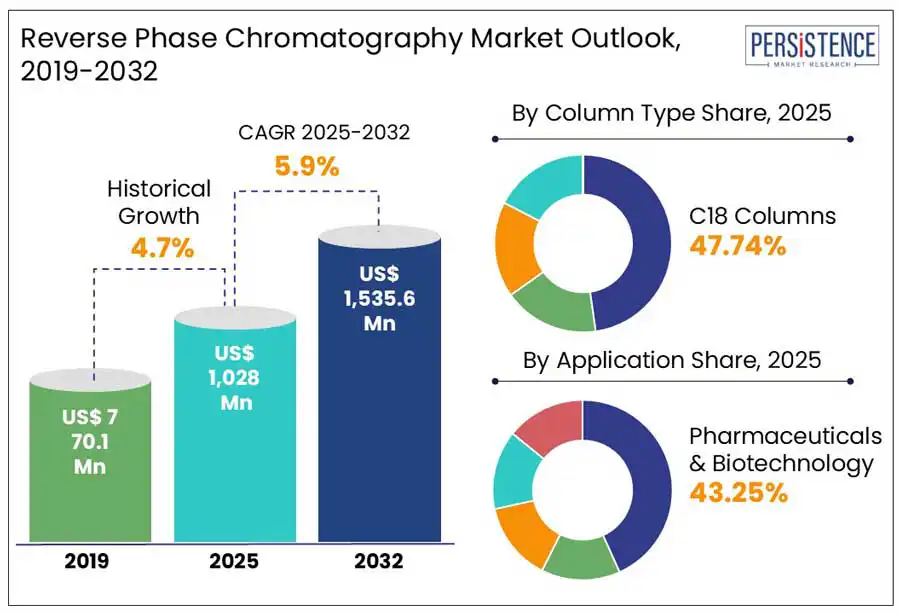

The global reverse phase chromatography market is anticipated to reach a value of US$1,028.0 million in 2025 and witness a CAGR of 5.9% from 2025 to 2032. The market will likely attain a value of US$1,535.6 million by 2032.

The reverse phase chromatography market plays an important role in separating and studying different substances in a mixture. It is a widely used method in liquid chromatography, where a non-polar material (stationary phase) holds the mixture, and a polar liquid (mobile phase) moves to help separate the components. The liquid chromatography method is widely pursued in many industries, such as pharmaceuticals, environmental testing, food safety, and biochemistry.

Reverse-phase chromatography is commonly applied in high-performance liquid chromatography (HPLC) systems. It is known for its ability to separate substances based on differences in polarity, since various stationary phase types, such as C18, C8, and C4, are each suited for specific analytical needs. C18 columns are particularly prominent due to their efficiency in separating nonpolar to moderately polar molecules, making them a versatile choice for many laboratory and industrial applications. The market is poised to grow, driven by demand for accurate, reliable compound analysis across various sectors.

Key Industry Highlights

- Reverse-phase chromatography is widely used in drug development, biologics purification, and quality control applications.

- Technological innovations improve resolution, sensitivity, and efficiency in analytical procedures.

- Rising pharmaceutical manufacturing and R&D activities fuel regional growth.

- Strict quality standards in pharma production boost demand for reliable analytical methods.

|

Global Market Attribute |

Key Insights |

|

Reverse Phase Chromatography Market Size (2025E) |

US$ 1,028.0 Mn |

|

Market Value Forecast (2032F) |

US$ 1,535.6 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

5.9% |

|

Historical Market Growth (CAGR 2019 to 2024) |

4.7% |

Market Dynamics

Driver - Growing demand for quality control and pharmaceutical R&D boosts the market

The global reverse phase chromatography market is strongly driven by the increasing need for quality control in industries such as pharmaceuticals, food safety, and environmental monitoring. As the demand for high-purity products rises, especially in drug development, companies are investing more in analytical technologies. Additionally, pharmaceutical R&D funding has seen a significant boost, fueling the adoption of advanced chromatography system techniques like reverse-phase chromatography. There's also a growing recognition of chromatography’s vital role in ensuring product safety, consistency, and regulatory compliance.

Educational and institutional research initiatives are further encouraging the use of reverse-phase chromatography in life sciences and biotechnology. The widespread versatility of the technique, capable of handling a broad range of compound polarities, makes it a preferred choice across multiple applications. As industries increasingly adopt HPLC systems, the demand for reverse-phase columns continues to rise, making it a crucial component of modern analytical and purification workflows.

Restraint - High equipment challenges growth

Despite its widespread applications, the reverse phase chromatography market faces several notable challenges. One major barrier is the high cost of advanced chromatography equipment and systems, which can be prohibitive for small and medium-sized enterprises or academic institutions. In addition to expensive setup and maintenance costs, the cost of columns, particularly high-quality reverse-phase columns like C18, adds significantly to overall expenditure. These columns often need frequent replacement depending on usage, further increasing operational costs.

Moreover, the shortage of skilled professionals who operate and interpret data from sophisticated chromatography systems disturbs the industry growth. These instruments require precision and technical expertise, lacked by several organizations. Additionally, stringent regulatory requirements, in pharmaceutical and clinical applications, complicate workflows and delay product development. The complexity of method development also poses challenges, especially for organizations without in-house analytical capabilities. These factors hinder broader adoption, particularly in resource-limited regions.

Opportunity - Expanding applications in biologics and biosimilar development

The rising focus on biologics and biosimilars presents a significant opportunity for the reverse phase chromatography market. As pharmaceutical companies shift toward developing protein-based drugs, monoclonal antibodies, and other complex biologics, there is a growing need for precise and reliable separation methods. Reverse phase chromatography is increasingly being used in the purification and characterization of peptides, proteins, and other biomolecules, making it highly relevant in this segment.

Moreover, the global expansion of the biosimilars market, driven by patent expirations of blockbuster biologics, demands advanced analytical tools for ensuring product equivalency and safety. Reverse phase chromatography offers high-resolution separation and reproducibility, which are essential for regulatory approval processes. In addition, collaborations between biotech firms and academic institutions for biologics research are further expanding the use of this technique. These trends position reverse-phase chromatography as a valuable tool in the evolving landscape of biopharmaceutical development.

Category-Wise Analysis

Column Type Insights

In reverse-phase chromatography, C18 columns dominate due to their strong hydrophobic interactions, making them ideal for separating a wide range of nonpolar and moderately polar compounds. C8 columns, with slightly less hydrophobicity, offer faster elution times and are preferred for compounds that are less retained on C18. C4 columns are mainly used for larger biomolecules like peptides and proteins due to their shorter alkyl chains, which reduce retention and improve peak shape. The “Others” category includes specialty columns like phenyl or cyano phases, used for niche applications requiring unique selectivity or interaction mechanisms.

Application Insights

The global reverse phase chromatography market is witnessing significant growth across various application segments, with pharmaceuticals and biotechnology emerging as the dominant applications. This segment benefits from the widespread adoption of RP-HPLC in drug discovery, biologics purification, and quality control processes. The increasing emphasis on environmentally friendly analytical techniques is further driving demand for RPC resins, enhancing safety and reducing ecological impact.

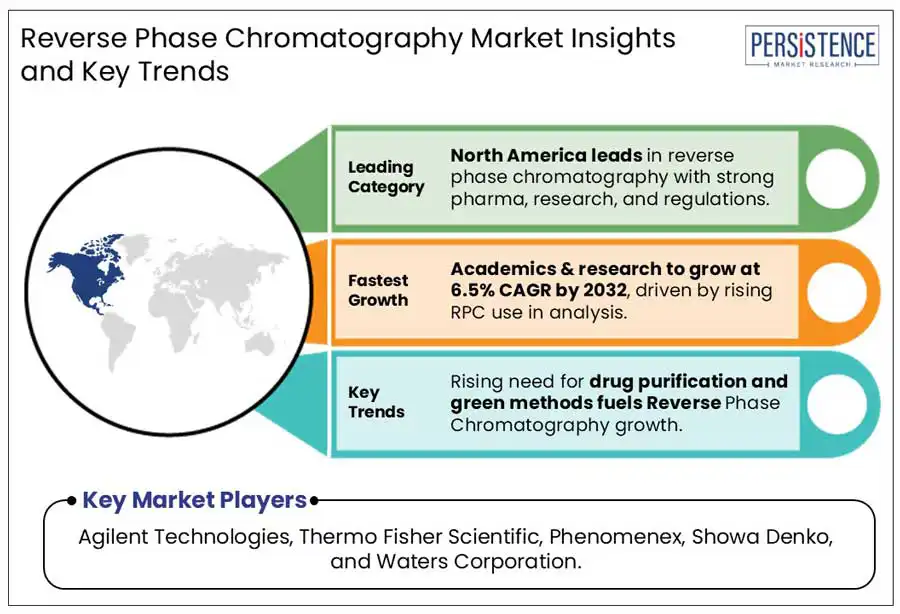

Moreover, the academic and research sector is projected to experience the most rapid growth, driven by the flexibility of RPC in separating compounds according to their polarity. Its use of a non-polar stationary phase and a polar mobile phase makes it highly effective for analyzing diverse molecular structures. As RPC plays a critical role in both routine analysis and complex molecular separations, its utility in laboratories and research institutions continues to expand, contributing to the overall growth of the market. These trends reflect RPC’s essential role across analytical and purification applications.

Regional Insights

North America Reverse Phase Chromatography Market Trends

North America continues to lead the global reverse phase chromatography (RPC) resins market, primarily due to strong pharmaceutical infrastructure and robust R&D activities. The demand for innovative drug development, particularly to combat viral diseases such as Ebola and Zika, has contributed to the region's dominance. The increasing application of monoclonal antibodies in therapeutic areas is another key growth factor. According to the Pharmaceutical Research and Manufacturers of America (PhRMA), U.S. biopharmaceutical companies invested over $102 billion in R&D in 2021, reinforcing the region's commitment to innovation.

Additionally, rising healthcare expenditure and the shift from traditional separation methods (like distillation and filtration) to more precise chromatographic techniques are driving adoption. The presence of a skilled workforce and ongoing research initiatives in biotechnology further support market expansion. Increasing demand for high-efficiency purification systems for biologics and the need for analytical consistency continue to shape the RPC market trend in the region.

Europe Reverse Phase Chromatography Market Trends

Europe holds a significant share fueled by the advancements in pharmaceutical manufacturing and biotechnology research. Countries such as Germany, the UK, and Switzerland are key markets recognized for their strict regulatory standards and high-quality therapeutic production. The European Medicines Agency (EMA) continue to emphasize analytical rigor in biologic and biosimilar approvals, which has increased the use of advanced chromatographic tools such as RPC. Growing investment in life sciences and diagnostics, along with EU-backed R&D programs such as Horizon Europe (2021–2027), funded with €95.5 billion, has further accelerated technological adoption.

Moreover, increased demand for targeted therapeutics, particularly in oncology and immunology, has led to greater reliance on chromatography for accurate separation and purification. The region also demonstrates rising interest in resin-based methods to support environmentally sustainable processes, reflecting innovation and regulatory alignment in product development.

Asia Pacific Reverse Phase Chromatography Market Trends

Asia Pacific is emerging as the fastest-growing market. The growth is driven by increased demand for rapid diagnostic and analytical tools across the healthcare and pharmaceutical sectors. Countries such as China, India, and South Korea are heavily investing in biotechnology and vaccine production capabilities. The post-COVID-19 era witnessed surge in the application of chromatography, including breath-based COVID detection using gas chromatography-ion mobility spectrometry (GC-IMS), which helped in faster, non-invasive diagnosis.

The Government of India's scheme National Biopharma Mission, and China's 14th Five-Year Plan for biotechnology emphasize R&D and capacity building, creating new opportunities for RPC technologies. Moreover, growing awareness about precision medicine and expansion of generic drug manufacturing further fuel the need for reliable purification methods. Local production of biosimilars and vaccines along with favorable government policies and increased funding is expected to sustain the high growth trajectory in this region.

Competitive Landscape

The global reverse phase chromatography market features a highly competitive environment, with numerous key players striving to secure market share. Companies in this space prioritize innovation, continuous product development, and strategic actions to strengthen their market position. Industry leaders like Thermo Fisher Scientific Inc., Agilent Technologies, Waters Corporation, Sigma-Aldrich (a Merck Group company), and Phenomenex Inc. are instrumental in influencing market trends and driving growth.

Key Industry Developments

- In July 2024, Tosoh Bioscience entered into a strategic partnership with ProSep Ltd. to enhance chromatography solutions, emphasizing the commercialization of the Phoenix system for purifying small molecules.

- In June 2022, Agilent partnered with MilliporeSigma (Merck KGaA) to improve Process Analytical Technologies (PAT) for downstream processing, with a focus on enhancing real-time monitoring and control in bioprocessing operations.

Companies Covered in Reverse Phase Chromatography Market

- Agilent Technologies

- Thermo Fisher Scientific

- Phenomenex

- Showa Denko

- Waters Corporation.

- Tosoh

- Dionex

- Jordi Flp

- Cytiva

- MERCK KGAA.

- Tosoh Corporation

- Avantor, Inc.

- Purolite

- Shimadzu Corporation.

- Mitsubishi Chemical Corporation

- Others

Frequently Asked Questions

The global industry is estimated to increase from US$ 1,028.0 million in 2025 to US$ 1,535.6 million in 2032.

Increasing demand for efficient drug purification, growing pharmaceutical R&D, and advancements in chromatography technologies drive market growth.

The market is projected to record a CAGR of 5.9% during the forecast period from 2025 to 2032.

Agilent Technologies, Thermo Fisher Scientific, Phenomenex, Showa Denko, Waters Corporation, and Others.

Rising adoption in academic research and the expanding biologics sector offer significant growth opportunities.