- Medical Devices

- Bleeding Control Kit Market

Bleeding Control Kit Market Size, Share, and Growth Forecast, 2026-2033

Bleeding Control Kit Market by Product Type (Basic, Advanced, Customized, Individual, Training), Component Type (Tourniquets, Hemostatic Agents, Dressings, Gloves, Tools, Instructional Aids), Application (Emergency, Surgical, Military, Consumer, Public Safety), and Regional Analysis for 2026-2033

Bleeding Control Kit Market Share and Trends Analysis

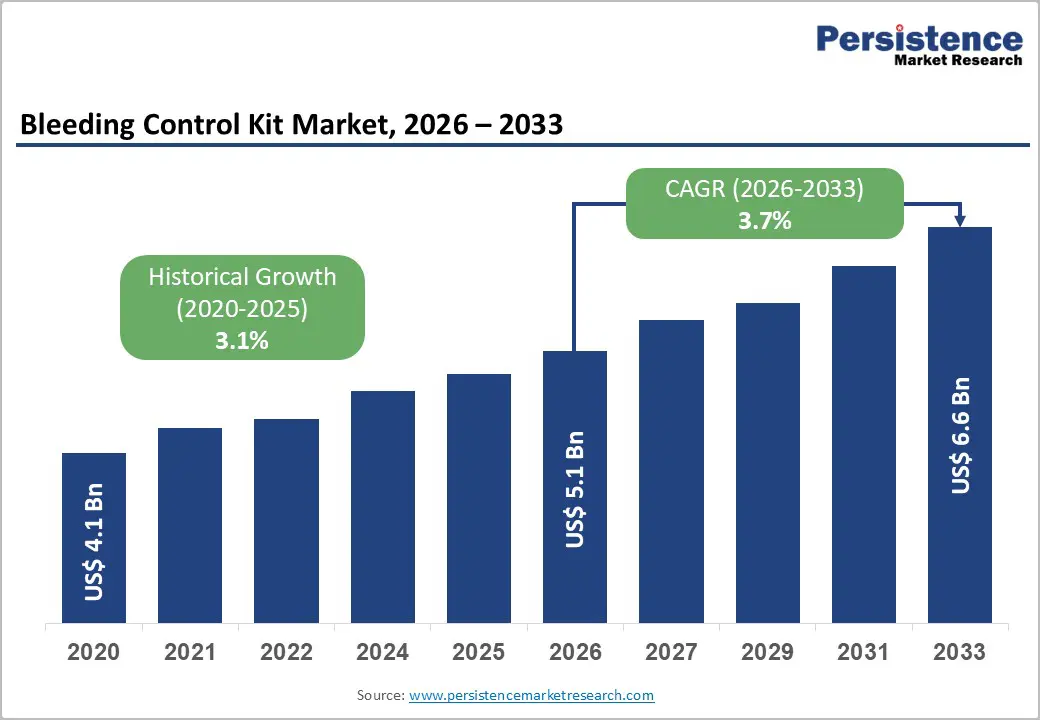

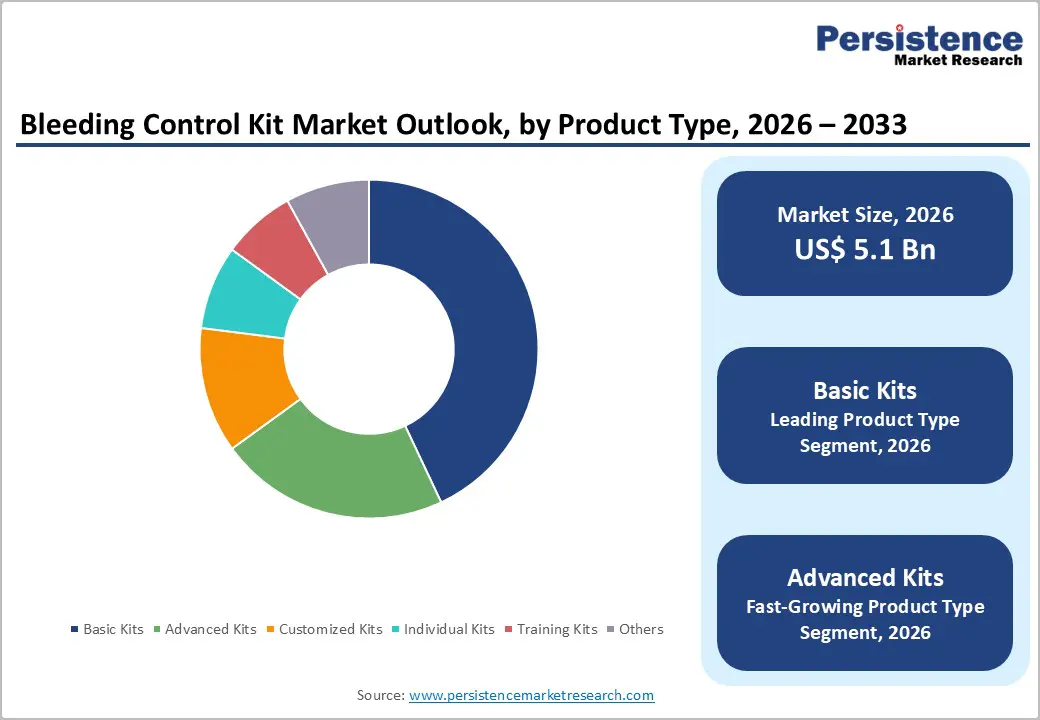

The global bleeding control kit market size is likely to be valued at US$ 5.1 billion in 2026, and is projected to reach US$ 6.6 billion by 2033, growing at a CAGR of 3.7% during the forecast period 2026-2033.

This growth is propelled by the increasing frequency of emergency trauma incidents, including road accidents, industrial injuries, and natural disasters, which create a critical demand for immediate hemorrhage control. Governments and health organizations actively promote ‘Stop the Bleed’ initiatives, driving broader adoption of bleeding control kits among both professional responders and the general public.

The integration of advanced hemostatic technologies, such as rapid-acting clotting agents and modular trauma kits, enhances user effectiveness and response speed. Regulatory mandates for public access to bleeding control kits further expand deployment in schools, workplaces, and transportation hubs, while tourniquets and hemostatic agents remain indispensable components for rapid, lifesaving intervention.

Key Industry Highlights

- Dominant Product Types: Basic kits are set to command around 43% of the market volume in 2026, while advanced kits are likely to grow the fastest at 5.1% CAGR through 2033, driven by institutional adoption.

- Leading Components: Tourniquets are expected to lead with 39% value share in 2026, while instructional aids are likely to register the fastest growth during 2026–2033, reflecting emphasis on rapid hemorrhage control.

- Dominant Applications: Emergency and public safety applications are anticipated to hold 46% share in 2026, while military and consumer segments are projected to grow the fastest through 2033, fueled by stringent regulatory mandates.

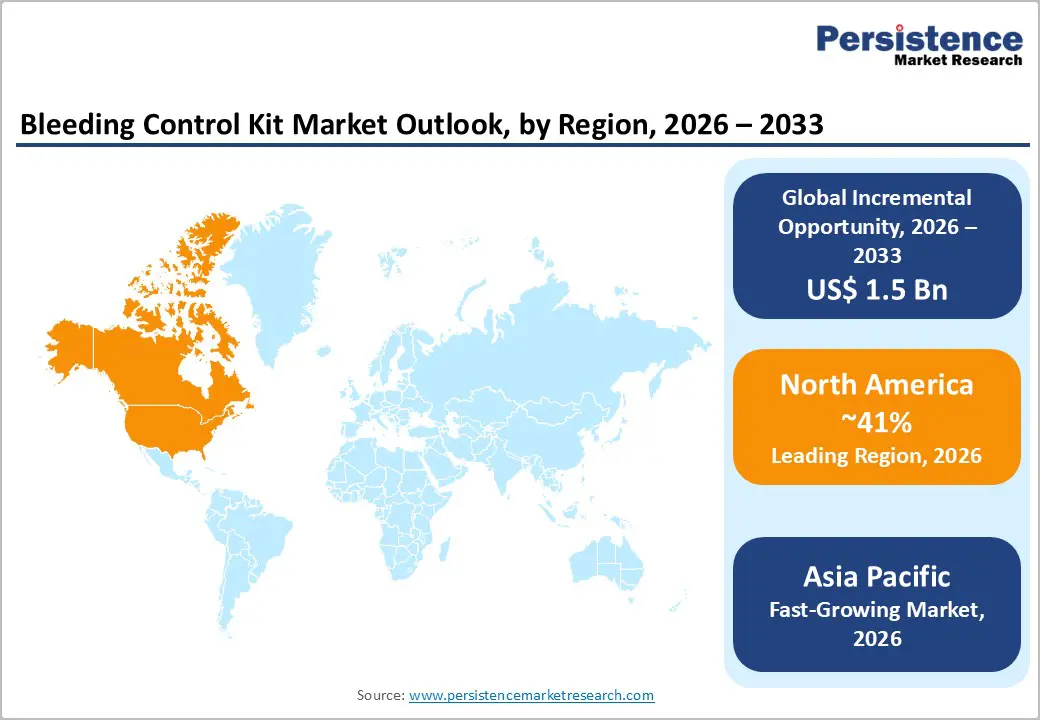

- Regional Leadership: North America is poised to lead with 41% share in 2026, whereas Asia Pacific is likely to register the fastest growth at 6% CAGR through 2033, driven by rising trauma cases and government safety initiatives.

- Competitive Environment: Product innovation, global expansions, strategic M&A deals, and digital training integration are driving market differentiation and strengthening leadership positions.

| Key Insights | Details |

|---|---|

|

Bleeding Control Kit Market Size (2026E) |

US$ 5.1 Bn |

|

Market Value Forecast (2033F) |

US$ 6.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

3.7% |

|

Historical Market Growth (CAGR 2020 to 2025) |

3.1% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Trauma Incidents and Emergency Preparedness

Globally, trauma from road accidents, industrial incidents, natural disasters, and violent conflicts continues to contribute significantly to preventable deaths, with uncontrolled bleeding accounting for over 30–40% of pre-hospital trauma fatalities. This acute challenge underlines the essential need for rapid hemorrhage control tools, making bleeding control kits crucial across both professional and lay settings. Governments, public health bodies, and first responders are emphasizing trauma readiness more than ever, elevating the importance of accessible, effective hemorrhage control solutions. Adoption is further supported by widespread awareness campaigns and first-responder training programs that teach practical hemorrhage management.

This policy momentum materialized in 2025 with Connecticut’s House Bill 7200, which mandates bleeding control kit placement and training in all public buildings, and Missouri’s Stop the Bleed Act, now requiring kits in schools starting in 2026. Local health departments, such as in Iowa County, have also distributed kits and training to emergency personnel under public health preparedness funding. Private sector initiatives, including corporate safety programs hosting community training, are helping increase public familiarity with bleeding control procedures. These real-world actions are driving broader adoption of tourniquets, hemostatic agents, and clear instructional aids, especially in high-risk environments such as workplaces, transit hubs, and educational institutions.

Technological Innovation and Regulatory Support

Continuous innovation in bleeding control technology is transforming the market by improving usability, effectiveness, and user confidence. Advanced solutions such as rapid apply tourniquet systems, enhanced hemostatic dressings, one-hand application tools, and modular trauma kits are making hemorrhage control more accessible for both trained responders and lay first-aid providers. A notable example from March 2026 is the introduction of a U.S. Food and Drug Administration (FDA) registered automatic tourniquet system with guided audio visual instructions designed for bystanders, demonstrating how technology evolution is directly shaping product demand and user adoption. These developments also enable kit manufacturers to differentiate through specialized modular configurations for schools, workplaces, and military applications.

Regulatory emphasis on hemorrhage readiness continues to accelerate market growth. Beyond state legislation, broader policy frameworks in North America and parts of Europe increasingly encourage bleeding control kit deployment in public spaces, workplaces, and educational institutions. Training and certification programs are being integrated into safety protocols, and corporate safety initiatives are hosting community training events to increase public proficiency. This dual momentum of tech innovation and regulatory support is expanding the market’s commercial reach while improving emergency response infrastructure globally. Increasing public awareness campaigns are also generating higher engagement with non-professional end-users, broadening the consumer market for kits and training.

High Product Costs and Budgetary Constraints

Advanced bleeding control kits, particularly those featuring sophisticated hemostatic technologies, modular components, and instructional aids, carry higher unit costs compared to basic first-aid supplies. This price differential can create affordability barriers for smaller healthcare facilities, schools, and community organizations, especially in budget-constrained regions. Even when funding exists, purchasing decisions may prioritize essential medical supplies over advanced trauma kits, slowing broader adoption. Price sensitivity can dampen interest in customized or high-end solutions despite proven clinical benefits and improved outcomes.

These budgetary limitations are especially pronounced in regions with low public health investment and strained emergency care funding. For example, India’s public health expenditure remained low at approximately 0.29% of GDP in 2025-26, limiting investment in emergency preparedness and safety equipment procurement across public institutions. Such funding shortfalls make it more difficult for local governments and community systems to allocate resources for advanced bleeding control kits. Consequently, high costs remain a structural restraint, concentrating adoption among large institutions or higher-income markets while restricting global penetration.

Lack of Awareness and Training Gaps

Despite increasing regulatory and advocacy focus on public safety, substantial knowledge gaps persist in effective hemorrhage control techniques across many regions. Surveys and safety reports indicate that a significant proportion of workers and community members lack basic first-aid and emergency response skills, including the ability to manage acute bleeding effectively. Without adequate training, the presence of bleeding control kits alone does not ensure their effective use in real emergencies. This gap reduces overall readiness and may limit the life-saving impact of deployed kits, particularly where user confidence is low.

Regional disparities in emergency response capability also highlight broader training deficits. In Nigeria, for example, local news outlets and health experts reported that poor emergency response skills are hindering accident survival, emphasizing that many bystanders and even first responders lack practical trauma care capabilities. Public campaigns such as National Stop the Bleed Month and expanded curricula aim to bridge this gap, but certified, standardized training programs remain unevenly distributed, especially in parts of Asia Pacific, Latin America, and Africa. These persistent awareness and training gaps continue to restrain market growth by limiting effective utilization across diverse end-user groups.

Massive Enhancements in Trauma Care in Developing Economies

Emerging economies are increasingly investing in healthcare infrastructure, trauma care modernization, and emergency response systems, creating significant growth potential for bleeding control kits. Countries such as China, Brazil, and Mexico are expanding institutional purchasing through public health programs, hospital network upgrades, and emergency preparedness initiatives, reflecting rising demand for reliable hemorrhage control solutions. Modernization of trauma care systems and first-aid education programs further enhance kit adoption in these regions, providing opportunities for both volume growth and increased market penetration. The growing focus on workplace and school safety also drives institutional kit procurement, creating steady demand streams.

Targeted government initiatives and strategic investments in emergency preparedness have improved access to trauma care solutions across emerging markets. For example, China has rolled out regional trauma training centers and distributed kits to urban hospitals, while Brazil has integrated bleeding control modules into community health programs. Such programs open avenues for localized manufacturing partnerships, cost-effective distribution, and faster deployment. Hospitals, schools, and corporate safety programs are expected to be key adoption drivers, positioning these emerging markets as critical growth regions for both basic and advanced bleeding control kits.

Digital Integration and Public Access Deployment

Integration of bleeding control kits with digital training platforms, emergency medical system (EMS) dispatch systems, and interactive instructional tools is enhancing usability, confidence, and effectiveness among both professional responders and lay users. QR-linked training modules, mobile guidance applications, and video tutorials allow users to learn skills efficiently, creating value-added service opportunities. Bundling kits with these digital solutions also enables recurring revenue streams through subscription-based training and certification programs. These digital capabilities also facilitate remote learning in underserved areas, expanding the kit’s reach beyond traditional clinical or workplace environments.

Recent initiatives illustrate this opportunity in action. The American College of Surgeons Stop the Bleed program trained over 5 million people globally by mid-2025 and introduced enhanced visually-guided courses for wider community accessibility. Local campaigns, such as Ventura County Public Health’s deployment of kits in government buildings and the FDNY’s targeted community training in Brooklyn, demonstrate practical public access expansion. Partnerships with NGOs, insurance companies, and corporate safety programs further reinforce adoption. These efforts show that digital integration and awareness campaigns can significantly increase adoption among non-professional end users and strengthen the market’s long-term growth trajectory.

Category-wise Analysis

Product Type Insights

Basic kits are expected to control approximately 43% of the bleeding control kit market revenue share in 2026, due to their simplicity, cost-efficiency, and wide applicability across workplaces, schools, industrial sites, and public venues. These kits typically include manual tourniquets, gauze dressings, pressure bandages, and protective gloves, capable of managing most common traumatic bleeding effectively. Adoption is projected to continue growing as emergency preparedness initiatives and institutional programs expand, reinforcing their foundational role in trauma response.

For example, in November 2025, the World Health Organization (WHO) hosted an Emergency Trauma Bag Training of Trainers program, equipping professionals to deploy kits and train others. This initiative illustrates how basic and tactical kits are expected to remain essential tools for public and professional responders in the near term.

Advanced kits are projected to be the fastest-growing product category, with an estimated CAGR of 5.1% through 2033, driven by hospitals, EMS units, industrial sites, and other high-risk institutions seeking comprehensive trauma solutions. These kits feature enhanced hemostatic agents, modular tools, and guided instructional aids, catering to complex trauma scenarios and professional user requirements. Growth is expected to accelerate due to innovations such as the AutoTQ automatic tourniquet system introduced in 2026, combining guided application with usability for non-medical personnel.

As organizations increasingly adopt next-generation safety standards, these advanced kits are likely to capture a larger share of high-value purchases over the forecast period.

Component Type Insights

Tourniquets are projected to represent around 39% of the bleeding control kit market value in 2026, due to their critical role in controlling severe bleeding rapidly. Tourniquets are essential for extremity hemorrhage, while hemostatic agents accelerate clot formation in wounds that cannot be compressed manually. Adoption is expected to continue expanding with increasing emphasis on institutional and community preparedness. For example, the “Bleed Safe Community Workshop” in California in 2025 trained participants on proper use of tourniquets and dressings, highlighting the real-world reliance on these components. This demonstrates that tourniquets and hemostatic agents are likely to sustain leadership in kit composition.

Instructional aids are expected to be the fastest-growing component segment, with a projected CAGR of 6.2% through 2033, driven by increasing demand for user-friendly, effective, and educational components. This includes digital guides, QR-linked modules, ergonomic trauma shears, and safety gloves that improve confidence and performance for both professional responders and lay users. Growth is further supported by training-of-trainers initiatives, which equipped personnel to teach proper use of instructional aids and advanced tools. As awareness of hands-on trauma response grows, these components are projected to experience strong adoption across community, institutional, and professional settings over the forecast period.

Regional Insights

North America Bleeding Control Kit Market Trends

North America is estimated to hold around 41% of the bleeding control kit market share in 2026, supported by robust regulatory frameworks, high public safety spending, and significant institutional procurement of bleeding control kits. The United States continues to lead adoption, with state-level legislation driving kit deployment across public venues, schools, and workplaces. For instance, in April 2025, Virginia passed House Bill 1700, requiring bleeding control kits in all public elementary and high schools and integrating training programs to improve emergency readiness before EMS arrival.

Public awareness campaigns and first responder training programs further reinforce adoption, ensuring that kits are used effectively during emergencies. Combined, these factors sustain demand and underline North America’s position as a mature, policy-driven market for bleeding control solutions.

Institutional budgets are increasingly allocated for both basic and advanced kits in hospitals, corporate facilities, and government buildings, supported by mature EMS networks and a dense manufacturer presence. Public safety campaigns continue to educate citizens, reinforcing demand for accessible trauma solutions. North America also benefits from rapid adoption of digital training modules and integration with EMS dispatch systems, enhancing the usability of kits in real-life emergencies. These combined factors underpin a stable growth through 2033, reflecting mature demand, steady policy reinforcement, and innovation adoption across private and public sectors.

Europe Bleeding Control Kit Market Trends

Europe’s market is supported by European Union (EU)-wide regulatory harmonization and mandatory safety equipment standards in public and occupational environments. Germany, the UK, and France are integrating bleeding control kits into hospitals, transportation networks, schools, and corporate settings. The European Commission (EC)’s 2025–26 Preparedness Union Strategy emphasized stockpiling essential emergency supplies for citizens, including medical and first-aid equipment, to improve readiness for disasters or health emergencies.

Regional collaborations, such as EU4Health programs, support cross-border training, infrastructure strengthening, and emergency response coordination. These combined measures provide a consistent growth foundation for bleeding control kit adoption across the continent.

This regional strategy encourages wider adoption of hemorrhage control solutions by highlighting preparedness at both organizational and community levels. Cross-border collaborations, such as EU4Health programs, strengthen emergency response infrastructure, provide technical guidance, and support capacity building in member states. Ongoing investments in trauma and EMS training, combined with national public health campaigns, enhance end-user competence and kit utilization. These factors collectively support the Europe market’s projected CAGR of 5.2% through 2033, reflecting a measured yet consistent growth trajectory fueled by policy alignment, infrastructure resilience, and growing safety consciousness.

Asia Pacific Bleeding Control Kit Market Trends

Asia Pacific is projected to be the fastest-growing regional market for bleeding control kits, likely to showcase a 2026-2033 CAGR of approximately 6% through 2033, driven by rapid urban expansion, increasing trauma incidents from road and industrial accidents, and sustained investment in emergency response infrastructure. Governments across the region are strengthening emergency care systems and workforce readiness through collaborative initiatives. For example, in June 2025, WHO and Australia’s National Critical Care and Trauma Response Centre conducted hands-on emergency operations training for public health officials from 18 Western Pacific countries, enhancing coordinated response capabilities.

In addition to workforce development, Asia Pacific countries are advancing regional coordination mechanisms to improve emergency preparedness. In November 2025, Western Pacific health stakeholders endorsed the Joint Emergency Risk Management Action Plan (JERMAP) to strengthen coordinated response across nations, addressing multi-hazard risks and emergency scalability. Domestic EMS networks are expanding, and national policies increasingly integrate trauma and pre-hospital care into broader health systems. These developments, combined with strategic manufacturing advantages and growing public and private sector collaborations, position Asia Pacific as a major growth engine for bleeding control solutions, with demand growing across urban and semi-urban markets.

Competitive Landscape

The global bleeding control kit market structure is moderately consolidated, with top players such as Johnson & Johnson, 3M, Teleflex, Medtronic, and North American Rescue controlling over 50% of revenue. These companies leverage strong relationships with hospitals, EMS providers, and public safety organizations, while investing in R&D, advanced tourniquet systems, hemostatic agents, and digital training integration. Their focus on innovation and institutional procurement ensures leadership across both professional and consumer segments.

Regional and niche players, including QuikClot, C.A.T. Medical, and Z-Medica, target tactical, military, and customized industrial solutions. Regulatory compliance, supply chain complexity, and certification requirements create entry barriers, while software-supported training and smart kit technologies open growth opportunities. Market consolidation is expected as leading players acquire smaller vendors or collaborate with technology providers to expand geographically and enhance product portfolios.

Key Industry Developments

- In February 2026, a startup from National Institute of Technology (NIT) Rourkela, Miraqules MedSolutions, has received approval from the Central Drugs Standard Control Organisation (CDSCO) for its rapid hemorrhage control product StopBleed. The nano-biopolymer hemostat quickly absorbs blood plasma and forms a hydrogel seal to stop severe bleeding from trauma such as road accidents, gunshots, or blast injuries.

- In July 2025, SafetyBuyer launched an enhanced range of trauma and bleed-control kits in collaboration with Safety First Aid to improve emergency preparedness in workplaces and public settings. The new kits include advanced components such as TMT tourniquets, HypaStop gauze, and ChitoSAM 100 haemostatic dressings designed to control severe bleeding quickly.

- In June 2025, Rescue Essentials started StopTheBleed.com, a dedicated online platform that provides officially licensed bleeding control kits and mass-casualty response tools. The site offers curated kits for schools, workplaces, and public spaces to improve preparedness for severe bleeding emergencies.

Companies Covered in Bleeding Control Kit Market

- Johnson & Johnson

- 3M, Teleflex

- Medtronic

- North American Rescue, LLC

- TyTek Medical

- Tactical Medical Solutions, Inc.

- H&H Medical Corporation

- Z Medica, LLC

- PerSys Medical

- SAM Medical

- Safeguard Medical

- Emergency Medical Products, Inc.

- First Care Products Ltd

Frequently Asked Questions

The global bleeding control kit market is projected to reach US$ 5.1 billion in 2026.

Soaring number of trauma incidents, expanding public safety initiatives, and technological advances in hemostatic products are driving the market.

The market is poised to witness a CAGR of 3.7% from 2026 to 2033.

Expanding adoption in emerging markets and integration with digital training and EMS platforms present key opportunities.

Johnson & Johnson, 3M, Teleflex, Medtronic, and North American Rescue are among the leading players in the market.