- Pharmaceuticals

- Bleeding Control Tablets Market

Bleeding Control Tablets Market Size, Share, and Growth Forecast, 2026 - 2033

Bleeding Control Tablets Market by Application (Menorrhagia, Hemophilia, Dysfunctional Uterine Bleeding, Others), End-User (Hospitals, Specialty Clinics, Retail Pharmacies, Online Pharmacies), Drug Class (Antifibrinolytics, Hemostatic Agents, Desmopressin), and Regional Analysis for 2026 - 2033

Bleeding Control Tablets Market Share and Trends Analysis

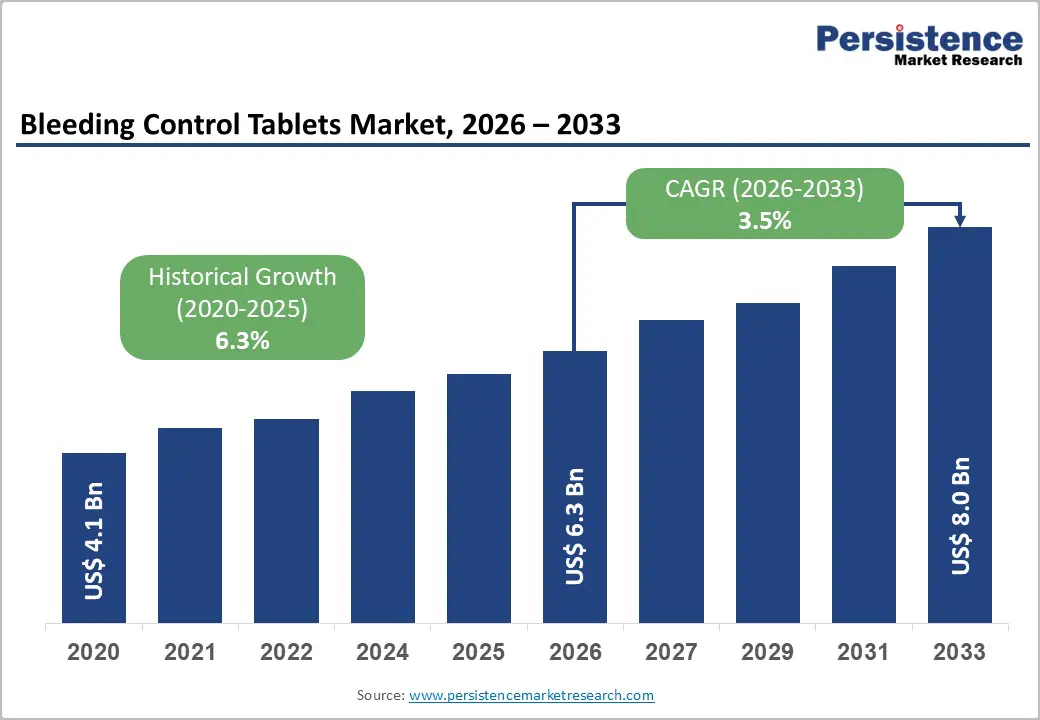

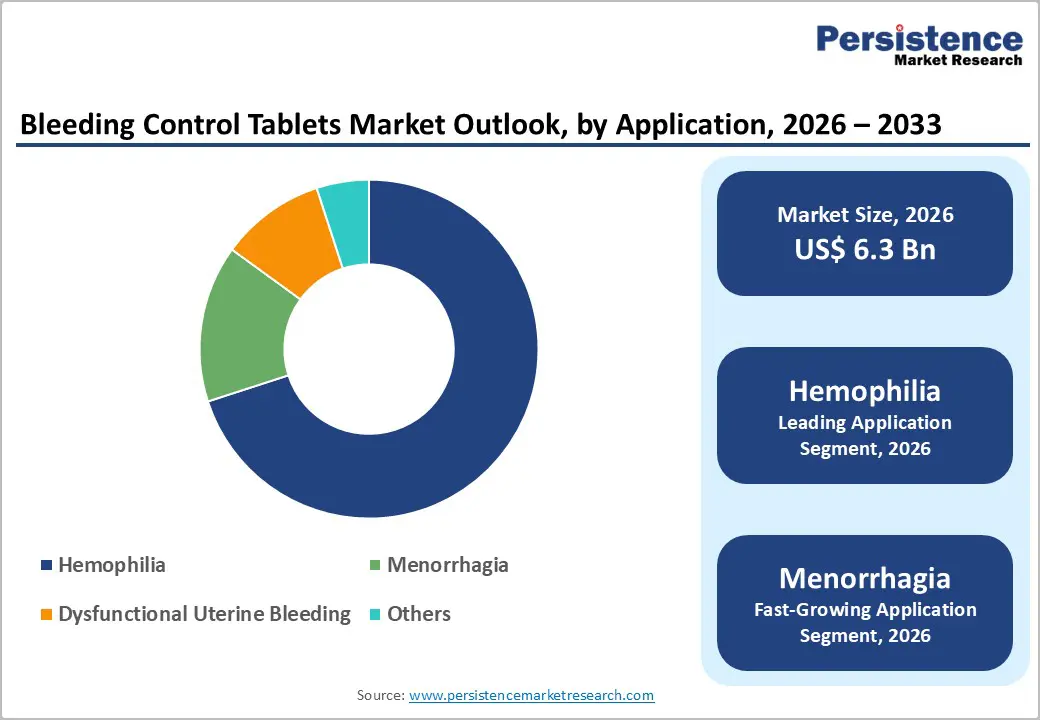

The global bleeding control tablets market size is likely to be valued at US$ 6.3 billion in 2026, and is projected to reach US$ 8.0 billion by 2033, growing at a CAGR of 3.5% during the forecast period 2026 - 2033.

The market has demonstrated consistent expansion, underpinned by escalating global trauma incidence, broadening emergency preparedness mandates, and accelerating first-responder training initiatives worldwide. Rising civilian and military demand for portable hemostatic solutions has positioned bleeding control tablets as a critical component of pre-hospital care protocols.

Key growth enablers include the widening adoption of Stop the Bleed and similar public-access hemorrhage control programs across North America and Europe, alongside heightened procurement activity from defense and emergency medical services (EMS) sectors. Simultaneously, ongoing R&D investments are improving product efficacy, biocompatibility, and shelf life, making these tablets increasingly viable for diverse end-user settings.

Key Industry Highlights

- End-User Leadership: Hospitals are poised to command approximately 58% revenue share in 2026, and online pharmacies are likely to grow the fastest during the 2026 - 2033 forecast period.

- Application Dominance: Hemophilia is set to dominate with nearly 75% revenue share in 2026, while menorrhagia is expected to be the fastest-growing segment through 2033.

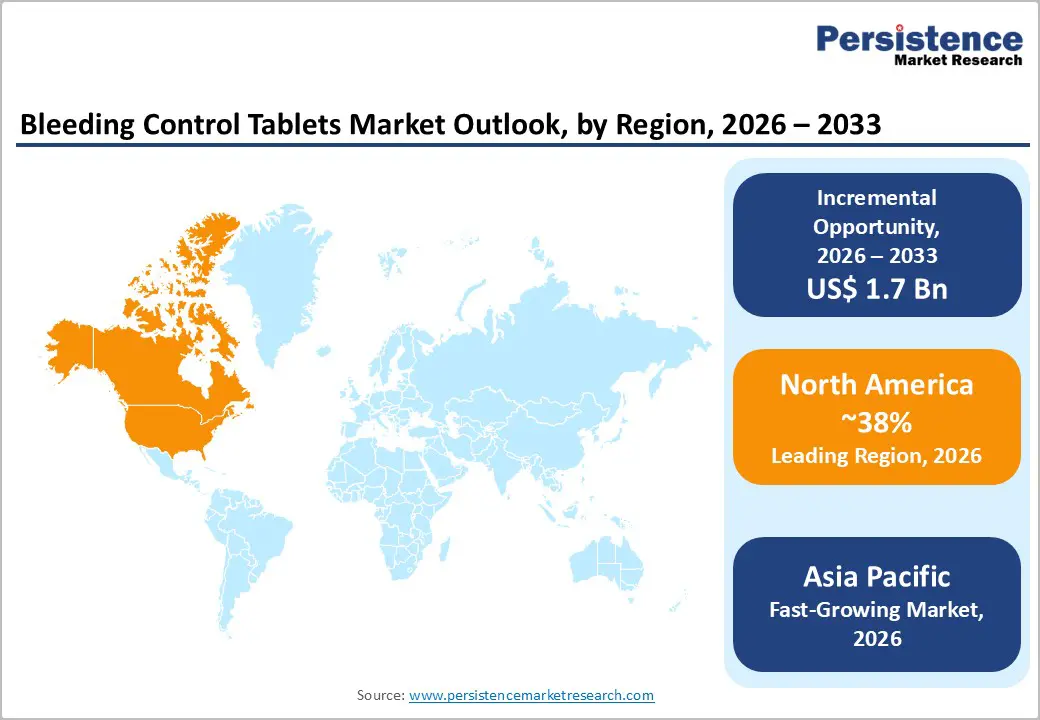

- Regional Dynamics: North America is anticipated to secure about 38% market share in 2026, supported by advanced emergency healthcare systems.

- Fastest-growing Market: The Asia Pacific market is slated to be the fastest-growing during the 2026 - 2033 forecast period, owing to the expansion of EMS networks that equip response teams effectively.

| Key Insights | Details |

|---|---|

| Bleeding Control Tablets Market Size (2026E) | US$ 6.3 Bn |

| Market Value Forecast (2033F) | US$ 8.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 3.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Increase in Fatalities Induced by Trauma Injuries Worldwide

Traumatic injuries remain a major cause of preventable mortality worldwide, with about 4.4 million deaths each year according to the World Health Organization (WHO). Uncontrolled bleeding accounts for a large share of these fatalities. Health authorities are emphasizing rapid hemorrhage control because early intervention significantly improves survival rates. Rising incidents such as road traffic accidents, workplace trauma, and mass casualty emergencies are increasing demand for practical hemostatic solutions. Products such as bleeding-control tablets are gaining attention because they enable an immediate response in emergency situations. National preparedness frameworks in countries including the U.S., the U.K., and Australia are incorporating these agents into emergency response protocols, which is expanding access for both civilians and trained responders.

Public health agencies are strengthening training programs that teach rapid bleeding management and proper use of hemostatic materials. Healthcare providers are increasing inventory levels of these products in hospitals, ambulances, and remote medical facilities. Manufacturers are also improving tablet formulations and portable emergency kits to deliver faster clotting performance and easier field deployment. Public awareness initiatives encourage households, schools, and workplaces to include bleeding control tools in first aid supplies. As adoption of bleeding control tablets expands across healthcare systems and community safety programs, they are becoming an important component of modern trauma preparedness and emergency response strategies.

Growing Public Emergency Preparation Programs and Regulatory Support

Governments and public health institutions are increasing investment in community emergency preparedness, which is strengthening demand for bleeding control tablets. Agencies such as the Federal Emergency Management Agency (FEMA) and the American College of Surgeons (ACS) are promoting nationwide bleeding control training programs that teach rapid hemorrhage response. In Europe, the European Commission (EC) is funding first aid capacity through the EU4Health program. These initiatives are strengthening local emergency response systems and expanding access to practical lifesaving tools. Bleeding control tablets are gaining attention as they require minimal training and enable rapid intervention outside hospital environments. Regulatory authorities are also simplifying approval procedures to accelerate the availability of advanced hemostatic solutions.

Regulatory reforms are improving product commercialization timelines. The U.S. Food and Drug Administration (FDA) is enabling faster market entry through the 510(k) clearance pathway for medical devices with demonstrated safety and effectiveness. This framework is encouraging manufacturers to develop improved tablet formulations and delivery systems. Public institutions are also integrating bleeding control kits into schools, workplaces, and community facilities to strengthen emergency readiness. Policymakers are expected to expand access further by linking hemostatic supplies to national health preparedness programs. Manufacturers are exploring specialized formats for educational institutions, while partnerships with non-governmental organizations (NGOs) are improving distribution in rural and underserved regions.

Stringent Regulatory Requirements and Approval Complexities

Regulatory oversight for bleeding control tablets varies significantly across global healthcare markets. Authorities classify these products under different frameworks depending on their composition and intended use. In the U.S., the FDA may regulate certain hemostatic agents as Class II medical devices, while other formulations are regulated as pharmaceutical products. In Europe, the European Medicines Agency (EMA) oversees approval for medicinal products, while Health Canada applies its own medical device and drug evaluation standards. Manufacturers must conduct extensive safety testing and documentation to meet these regulatory requirements. Large companies often manage these processes effectively, while smaller producers face higher compliance costs and slower product development cycles.

Differences in regulatory classifications create operational challenges for companies seeking to expand into international market. A product may receive approval in one region while facing additional evaluation or documentation requirements in another. This lack of alignment increases development expenses and delays commercial launches across global markets. Companies, therefore, prioritize entry into large markets such as the United States or Europe before expanding into additional regions. International health organizations such as the WHO are encouraging greater harmonization of safety and testing standards. Digital regulatory platforms and improved submission systems are also supporting more efficient review processes.

Competition from Injectable Hemostatic Alternatives

Bleeding control tablets face increasing competition from injectable hemostatic agents such as tranexamic acid (TXA) injections, fibrin sealants, and recombinant factor VIIa therapies. Injectable products often provide a faster systemic clotting response during severe hemorrhage, making them suitable for surgical procedures and critical care environments. Clinical adoption has strengthened following evidence from the CRASH 2 trial that demonstrated reduced trauma mortality with early TXA administration. The U.S. military has incorporated TXA into Tactical Combat Casualty Care (TCCC) protocols, building confidence in injectable hemostatic therapies among clinicians and emergency medical teams.

This shift is influencing procurement decisions in hospitals and defense medical programs where clinical outcome data strongly affects purchasing strategies. Growing familiarity among EMS personnel with injectable treatment protocols is also reducing earlier barriers to administration. As a result, tablet manufacturers face increasing pricing pressure in institutional procurement processes. To maintain competitiveness, producers are focusing on clinical validation and emphasizing advantages that injectable therapies cannot easily provide, including portability, rapid accessibility, and simple use by non-clinical responders in community or pre hospital emergency situations.

Technological Innovation in Next-Generation Hemostatic Formulations

Researchers and medical device manufacturers are developing advanced hemostatic formulations using materials such as chitosan, zeolite-enhanced compounds, and recombinant proteins. These technologies are designed to accelerate clot formation and improve clinical outcomes compared with conventional agents. Product developers are also introducing new delivery formats, including effervescent tablets and water-activated systems that trigger a rapid hemostatic response during trauma emergencies. As laboratory research progresses into preclinical and clinical evaluation, manufacturers are preparing to position these next-generation products for high-value segments such as military medicine, emergency surgery, and advanced trauma care.

Commercial development is strengthening through collaboration among industry participants, academic medical institutions, and government research agencies. In the United States, the Defense Advanced Research Projects Agency (DARPA) supports innovation programs that connect laboratory discovery with field-ready medical technologies. These partnerships are helping manufacturers generate stronger clinical evidence and accelerate regulatory submissions. As the global hemostatic research ecosystem expands, companies that invest early in collaborative development models are strengthening their competitive position by securing procurement opportunities.

Integration into Public Safety and Corporate Emergency Preparedness Programs

Public facilities are increasingly adopting emergency preparedness models similar to the deployment of automated external defibrillators (AEDs). This approach is creating new opportunities for bleeding control tablets in workplaces, schools, airports, and other high-traffic environments. Organizations such as the American Heart Association (AHA) and the National Safety Council (NSC) are advocating wider availability of bleeding control kits to improve immediate response during trauma incidents. Institutions are recognizing the operational value of accessible hemostatic tools that enable rapid intervention before professional medical teams arrive. The success of AED placement programs is encouraging policymakers and safety planners to adopt similar strategies for hemorrhage control resources.

Legislative and public health initiatives are strengthening this trend as policymakers evaluate requirements for bleeding control equipment in public spaces. Safety organizations are highlighting gaps in current first aid infrastructure and recommending standardized kit deployment across commercial and educational settings. Governments are expected to introduce guidelines that promote the wider availability of hemostatic supplies in locations with large public gatherings. In response, manufacturers are developing durable and simplified kits designed for use by individuals with minimal medical training. As these policies expand, organizations will integrate bleeding control tablets alongside AEDs within comprehensive emergency response systems.

Category-wise Analysis

Application Insights

Hemophilia is projected to lead with nearly 75% of the bleeding control tablets market revenue share in 2026. Patients with Hemophilia A and Hemophilia B require lifelong management of recurrent bleeding episodes, which creates stable demand for bleeding control therapies. Healthcare systems in high income regions are supporting this need through specialized hemophilia treatment centers (HTCs) that integrate hemostatic products into routine care pathways. Strong clinical evidence and established reimbursement programs across North America and Europe are reinforcing the adoption of these therapies. As a result, manufacturers benefit from predictable procurement volumes linked to chronic disease management programs.

Menorrhagia is expected to showcase the fastest growth from 2026 to 2033. Heavy menstrual bleeding among women of reproductive age represents a large and historically underserved medical need. Expanded gynecological screening programs and improved awareness of women’s health are increasing diagnosis rates and treatment-seeking behavior. Healthcare providers are recommending oral hemostatic therapies as accessible first-line options because they provide non-invasive management of excessive bleeding. In many healthcare systems, these treatments offer a practical alternative where surgical procedures such as endometrial ablation remain costly or limited in availability.

End-User Insights

Hospitals are set to dominate in 2026, holding about 58% of the bleeding control tablets market share. Their dominance reflects the central role hospitals play in managing both acute and chronic bleeding disorders. Procurement systems typically rely on formulary-based purchasing that supports a steady supply for emergency departments, surgical units, hematology wards, and gynecology clinics. Physicians and clinical specialists within hospital networks strongly influence prescribing patterns, which reinforces institutional demand for validated hemostatic tablet formulations. In many high income countries, established reimbursement frameworks are also supporting sustained purchasing through public and private healthcare programs.

Online pharmacies are projected to grow the fastest during the 2026-2033 forecast period as healthcare retail becomes increasingly digital. Telemedicine platforms are enabling patients to move directly from remote consultations to online medication ordering, thereby simplifying access to treatment. This model benefits individuals managing conditions such as hemophilia or menorrhagia who require regular therapy. E-commerce providers are also introducing subscription-based delivery services that ensure consistent medication supply and improve adherence to treatment plans. As digital health infrastructure expands, online pharmacies are becoming an important distribution channel for bleeding control therapies.

Regional Insights

North America Bleeding Control Tablets Market Trends

North America is anticipated to account for an estimated 38% of the bleeding control tablets market value in 2026. The United States leads in terms of revenue generation on the back of its advanced trauma care systems and strong regulatory oversight from the FDA Center for Devices and Radiological Health. Government programs such as the Stop the Bleed initiative, supported by the Department of Homeland Security (DHS) and the Department of Defense (DOD), are promoting community training and wider availability of bleeding control tools. Military medical units, EMS, law enforcement agencies, and public institutions are adopting these products to strengthen emergency preparedness. Canada is also contributing to regional demand by implementing provincial safety regulations that require standardized first-aid equipment in schools, workplaces, and public facilities.

The region also pioneers bleeding-control technologies. North America hosts a large concentration of manufacturers, biotechnology companies, and medical device developers that are investing heavily in research and development (R&D). Venture capital funding and government grants are supporting startups developing advanced hemostatic materials and drug-delivery systems. Major biotechnology clusters in the northeastern and western United States are accelerating product development and regulatory submissions. These factors are creating a strong pipeline of next-generation hemostatic formulations approaching regulatory approval and commercial launch.

Europe Bleeding Control Tablets Market Trends

Europe is the second-largest market for bleeding control tablets, owing to its well-structured emergency healthcare systems and coordinated public safety policies. Germany, the U.K., and France are generating strong demand through national emergency response networks. The United Kingdom National Health Service (NHS) has integrated bleeding control measures into trauma care protocols, which supports consistent procurement across hospitals and ambulance services. In Germany, organizations such as the German Red Cross (DRK) and ADAC emergency services equip response teams with hemostatic products to improve rapid intervention capacity. France and Spain are also expanding investment in emergency preparedness and first-aid infrastructure, which is strengthening regional demand for accessible bleeding-control solutions.

European regulatory frameworks and public health initiatives are reinforcing market stability. Programs such as the EU4Health initiative are funding emergency training programs and the distribution of first aid kits across communities. Cross-border procurement structures allow suppliers with established distribution networks to supply hospitals and emergency agencies across multiple countries. Policymakers are also evaluating broader deployment of bleeding control tools in public spaces such as schools, transportation hubs, and civic buildings. Manufacturers are adapting product design with features such as multilingual instructions to serve diverse populations. Collaboration with rescue organizations and medical institutions also supports field testing of new hemostatic technologies to improve the effectiveness of emergency responses.

Asia Pacific Bleeding Control Tablets Market Trends

Asia Pacific is projected to become the fastest-growing market for bleeding control tablets through 2033, as governments strengthen emergency healthcare systems and disaster preparedness programs. China and India are driving regional expansion through defense modernization and broader EMS networks that equip first responders with trauma management tools. China is also expanding civilian first-aid training programs to improve responses to urban accidents and natural disasters. India is supporting domestic production through the Atmanirbhar Bharat initiative, which promotes self-reliance in medical supply chains. Japan and South Korea are maintaining steady adoption due to advanced healthcare infrastructure and structured disaster response strategies for earthquakes and severe weather events. Several ASEAN members are also increasing healthcare budgets and improving emergency response capacity.

The region is strengthening its role in global production of bleeding control products. China and India offer competitive manufacturing costs and strong active pharmaceutical ingredient (API) supply capabilities, attracting international medical device and pharmaceutical companies. Many global firms are establishing regional manufacturing facilities to improve supply chain efficiency and access to growing local markets. This expansion is increasing competition and encouraging the development of products adapted to regional conditions, such as heat-resistant packaging for tropical climates. Governments are also launching awareness programs that promote the placement of bleeding control kits in schools, industrial facilities, and transportation hubs.

Competitive Landscape

The global bleeding control tablets market structure is moderately consolidated, with leading companies such as Z Medica, Teleflex Incorporated, Biolife, Tricol Biomedical, and Medline Industries controlling between 55% and 60% of the total market share. Competition among these firms revolves around product performance, validated hemostatic mechanisms, and regulatory approvals across major healthcare markets. Established manufacturers emphasize clinical evidence and compliance with medical standards, which strengthens credibility among hospitals, military medical units, and emergency response agencies.

Mid-tier and emerging companies compete through cost advantages, regional distribution networks, and targeted product applications. These firms focus on segments such as civilian first aid kits, workplace safety equipment, and community emergency preparedness programs. This competitive structure encourages product innovation while expanding accessibility beyond traditional clinical settings. Premium products supported by strong clinical validation drive value growth, while competitively priced offerings enable broader adoption in emerging healthcare markets.

Key Industry Developments

- In August 2025, an article from the American Journal of Obstetrics & Gynecology examines the efficacy of novel bleeding control tablets in managing postpartum hemorrhage. It reports that these orally administered hemostatic agents significantly reduced blood loss by 45% compared to standard treatments in a randomized trial of 250 patients, with no major adverse events.

Companies Covered in Bleeding Control Tablets Market

- Z-Medica LLC

- Teleflex Incorporated

- Biolife LLC

- Tricol Biomedical Inc.

- Medline Industries, LP

- SAM Medical Products

- Prometheus Medical Ltd.

- RevMedx Inc.

- Baxter International Inc.

- Entegrion Inc.

- Coda Octopus Products

- Abbott Laboratories

- Cardinal Health, Inc.

Frequently Asked Questions

The global bleeding control tablets market is projected to reach US$ 6.3 billion in 2026.

Surging trauma cases from accidents, and intensifying military conflicts are pushing up the demand for rapid hemostasis solutions in EMS and combat use.

The market is poised to witness a CAGR of 3.5% from 2026 to 2033.

Major opportunities lie in integration with digital health tools, which can fuel the demand for smart, trackable hemostatic products.

Z-Medica LLC, Teleflex Incorporated, Biolife LLC, Tricol Biomedical Inc., and Medline Industries, LP are some of the key players in the market.