- Biotechnology

- Biosensor Technologies Market

Biosensor Technologies Market Size, Share, and Growth Forecast, 2026 – 2033

Biosensor Technologies Market by Product Type (Wearable Biosensors, Others), Technology Type (Electrochemical Biosensors, Optical Biosensors, Thermal Biosensors, Others), Application (Medical & Healthcare, Agriculture, Others), and Regional Analysis for 2026 - 2033

Biosensor Technologies Market Share and Trends Analysis

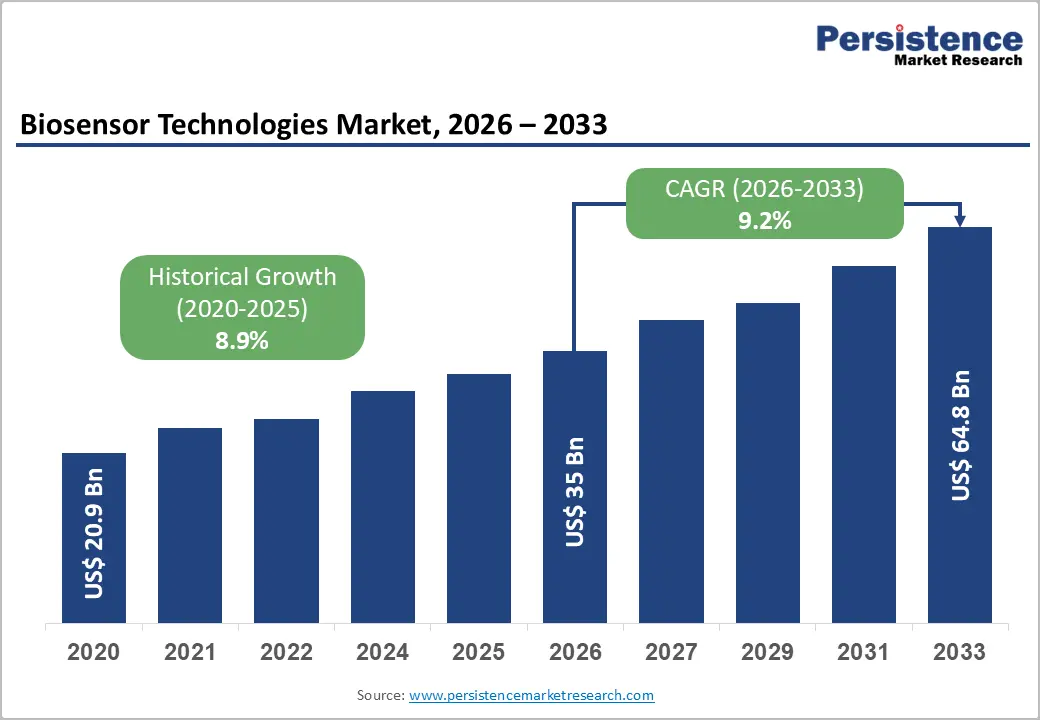

The global biosensor technologies market size is likely to be valued at US$35 billion in 2026 and is estimated to reach US$64.8 billion by 2033, growing at a CAGR of 9.2% during the forecast period 2026−2033, driven by increasing demand for real-time diagnostics and decentralized healthcare solutions, alongside the rising prevalence of chronic diseases and the need for continuous patient monitoring.

Aging populations are further driving the adoption of minimally invasive biosensor technologies. In addition, integration with mobile applications, cloud-based analytics, and artificial intelligence is improving diagnostic accuracy and enabling predictive healthcare capabilities. Government-backed digital health initiatives and expanding screening programs are also accelerating market adoption by enhancing treatment adherence and helping reduce hospitalization costs across healthcare systems.

Key Industry Highlights:

- Leading Technology Type: Electrochemical biosensors are set to hold around 45% revenue share in 2026, driven by high sensitivity, cost efficiency, and strong clinical validation in point-of-care diagnostics.

- Fastest-growing Technology Type: Optical biosensors are projected to be the fastest-growing segment, driven by label-free detection and high-precision biomarker analysis.

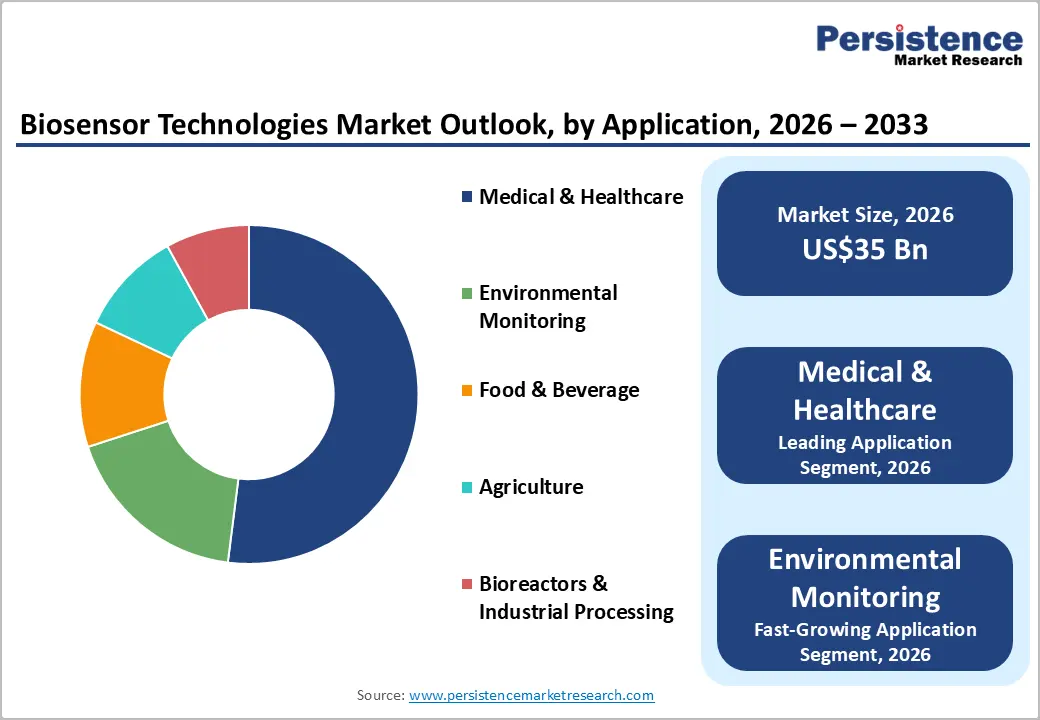

- Leading Application: The medical & healthcare segment is estimated to hold roughly 52% revenue share in 2026, driven by disease diagnosis and patient monitoring systems.

- Fastest-growing Application: Environmental monitoring is forecast to record the fastest growth, driven by pollution detection and regulatory compliance needs.

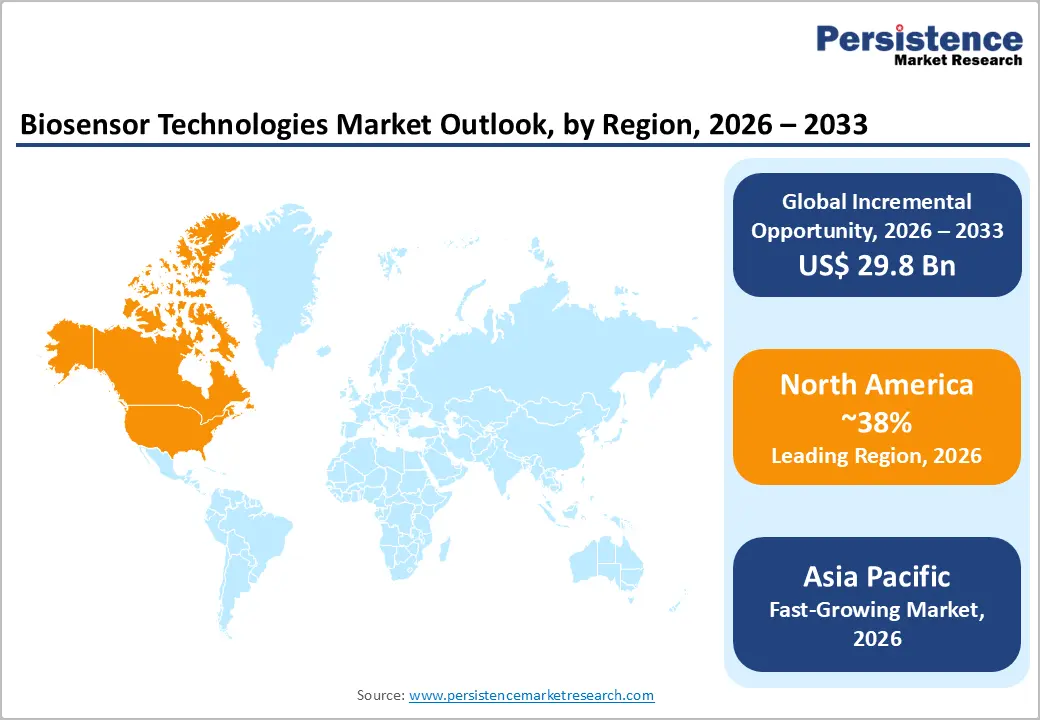

- Regional Leadership: North America is projected to capture around 38% market share by 2026, while Asia Pacific is expected to register the fastest growth, driven by healthcare expansion and digital health adoption.

- Competitive Environment: The market reflects a moderately fragmented structure, with companies such as Abbott Laboratories, Medtronic plc, F. Hoffmann-La Roche Ltd, Siemens Healthineers AG, and Bio-Rad Laboratories, Inc., driven by innovation and regulatory strength.

- Innovation Trends: Integration of artificial intelligence, miniaturized wearable biosensors, and nanotechnology-enabled diagnostics is shaping next-generation real-time monitoring solutions.

DRO Analysis

Driver - Rising Burden of Chronic Diseases and Preventive Healthcare Adoption

Market growth is driven by the rising burden of chronic diseases, which fuels demand for biosensor technologies. Diabetes, cardiovascular conditions, and respiratory ailments affect 1.8 billion adults globally as per 2025 World Health Organization data, creating a large base of patients requiring continuous monitoring. Biosensors deliver real-time glucose, blood pressure, and oxygen readings, supporting early detection of fluctuations and helping patients avoid severe complications. Integration into wearables enables daily tracking, shifting preventive healthcare toward early intervention and proactive self-management.

Preventive healthcare adoption accelerates biosensor deployment as programs emphasize routine screening and lifestyle-centric interventions supported by biosensor-enabled point-of-care testing in clinics and homes. Portable, user-friendly designs expand accessibility and drive uptake in primary care settings where economic pressures favor scalable, outpatient-oriented solutions. Payers increasingly incentivize adoption to curb long-term expenditure, and structural shifts prioritize remote monitoring, which shortens treatment cycles and improves efficiency.

Restraint - High Development Costs and Complex Regulatory Approval Processes

Significant cost pressures arise from intensive research, prototyping, and validation requirements across biosensor development. Advanced materials, micro-fabrication processes, and integration with digital platforms increase capital intensity throughout product lifecycles. Clinical testing requires extensive data generation to demonstrate accuracy and reliability, extending timelines and raising expenses. High upfront investment limits participation from smaller firms and startups, reducing competitive diversity and slowing innovation cycles across product development pipelines.

Regulatory approval processes impose strict compliance standards related to safety, performance, and data integrity. Manufacturers allocate substantial resources to documentation, quality assurance, and post-market surveillance systems. Approval delays disrupt launch schedules and limit competitive positioning. Smaller firms face constrained financial capacity, reducing innovation pace and entry rates. Variability in global regulatory frameworks increases operational burden, requiring region-specific adaptations that elevate costs and extend development cycles across international markets.

Opportunity - Technological Convergence with Artificial Intelligence (AI) and Personalized Medicine

Market growth is being supported by the integration of biosensors with artificial intelligence (AI) and personalized medicine. AI-powered analytics help convert continuous biosensor data into useful clinical insights, improving early disease detection and risk assessment for chronic diseases and cancer care. This increases the value of biosensor-generated data for healthcare providers and insurers that aim to reduce hospital admissions through predictive monitoring. The U.S. Food and Drug Administration cleared 295 AI or machine learning-enabled medical devices in 2025, reflecting growing institutional support and accelerating the commercialization of AI-integrated biosensor platforms.

Integration with personalized medicine workflows strengthens demand expansion and operational efficiency. Providers calibrate treatment intensity and monitoring frequency using real-time biomarker trends, reducing unnecessary utilization and improving adherence. Chronic care programs, cancer surveillance pathways, and preventive health initiatives rely on continuous biosensor inputs to tailor interventions, driving sustained volume demand for sensors and digital infrastructure. Payers prioritize scalable outpatient solutions that limit long term expenditure, while alignment with digital health ecosystems supports recurring revenue models.

Category-wise Analysis

Product Type Insights

Wearable biosensors are anticipated to secure around 48% of the biosensor technologies market share in 2026, reflecting strong integration into consumer health and clinical monitoring ecosystems. Devices such as Fitbit Charge 6 and Dexcom G7 continuous glucose monitoring system enable continuous tracking of glucose, heart rate, and activity. Non-invasive design and portability improve patient acceptance and adherence. Integration with mobile applications and cloud platforms enhances accessibility and data insights. Preventive healthcare trends and corporate wellness programs sustain demand growth.

Implantable biosensors are expected to be the fastest-growing segment, propelled by advancements in biocompatible materials and long-term monitoring capabilities. Devices such as Eversense E3 continuous glucose monitoring system and the Medtronic Reveal LINQ insertable cardiac monitor enable precise, continuous biomarker tracking. High accuracy, minimal calibration, and minimally invasive implantation support clinical adoption, while personalized medicine expands long-term demand.

Technology Type Insights

Electrochemical biosensor extracts are poised to dominate with a forecast market share of over 45% in 2026, powered by high sensitivity, cost-efficiency, and widespread clinical validation. Devices such as Accu-Chek Guide Blood Glucose Meter and Abbott FreeStyle Libre System support reliable point-of-care diagnostics. Scalable manufacturing, retail access, and digital integration strengthen adoption in home-based monitoring and preventive healthcare.

Optical biosensors are estimated to be the fastest-growing segment, fueled by advancements in photonic technologies and increasing demand for high-precision diagnostics. Platforms such as Biacore T200 Surface Plasmon Resonance System and Horiba Aqualog Fluorescence Spectrometer enable label-free, high-specificity biomarker analysis. Expanding research use, non-invasive diagnostics, and nanophotonics innovation accelerate adoption.

Application Insights

Medical & healthcare is likely to be the leading segment with a projected 52% of the biosensor technologies market share in 2026, due to strong clinical demand for diagnostic and monitoring solutions. Devices such as Abbott i-STAT System and Dexcom G6 Continuous Glucose Monitoring System enhance detection and monitoring. Regulatory validation, telemedicine integration, and early diagnosis improve outcomes and cost-efficiency.

Environmental monitoring is anticipated to be the fastest-growing segment, fueled by increasing focus on pollution control and sustainability initiatives. Solutions such as YSI EXO2 Multiparameter Sonde and Aeroqual Series 500 Air Quality Monitor enable real-time contaminant detection. Regulatory policies, industrial compliance needs, and digital monitoring platforms accelerate adoption.

Regional Insights

North America Biosensor Technologies Market Trends

North America is expected to lead with an estimated 38% of the biosensor technologies market share in 2026, supported by strong regulatory alignment through the U.S. Food and Drug Administration and high clinical adoption of connected diagnostics. Advanced reimbursement frameworks enable rapid commercialization. Concentration of innovation hubs and venture funding accelerates product pipelines. Integration with digital health platforms strengthens real-time monitoring uptake across clinical and homecare settings.

U.S. Biosensor Technologies Market Insights

The U.S. accounts for the largest share within North America in 2026, supported by strong commercialization capacity and high adoption of point-of-care diagnostics, with contribution exceeding 80% of regional biosensor revenue based on industry distribution trends. Advanced healthcare infrastructure, rapid regulatory clearances by the U.S. Food and Drug Administration, and high chronic disease burden drive demand. In 2024, FDA clearance of over-the-counter continuous glucose monitoring systems such as Dexcom Stelo and Abbott Lingo expanded consumer access and accelerated market penetration.

Canada Biosensor Technologies Market Insights

Canada contributes a smaller but stable share within North America, accounting for approximately 6% of global biosensor revenue, reflecting moderate regional positioning. Growth is supported by rising diabetes prevalence and strong adoption of point-of-care diagnostics in public healthcare systems. Federal healthcare funding frameworks improve accessibility to diagnostic technologies. In 2024, the expansion of electrochemical biosensor applications in clinical diagnostics strengthened commercialization and adoption trends.

Europe Biosensor Technologies Market Trends

Europe is expected to hold a significant share near 25% in 2026, driven by stringent regulatory frameworks under the European Commission and strong public healthcare systems. High adoption of point-of-care diagnostics supports early disease detection. Collaborative research programs under Horizon Europe accelerate biosensor innovation. Emphasis on environmental monitoring and food safety expands applications across industrial and public health domains.

Germany Biosensor Technologies Market Insights

Germany leads the European biosensor technologies market with an estimated 43% regional share in 2026, supported by strong medical device engineering and advanced diagnostics infrastructure. Key companies include Siemens Healthineers, Robert Bosch GmbH, Infineon Technologies, First Sensor AG, and STRATEC SE. Strong R&D ecosystem led by institutes such as Fraunhofer Institute drives innovation in biosensing technologies.

U.K. Biosensor Technologies Market Insights

The U.K. is expected to account for 20% of Europe's biosensor revenue in 2026, reflecting strong positioning in digital diagnostics and wearable monitoring adoption. Growth is supported by National Health Service (NHS) digital health programs and rising chronic disease monitoring demand. Strong research ecosystem led by institutions such as University of Cambridge and Imperial College London drives biosensor innovation. In 2024, Defence and Security Accelerator programs advanced wide-area biosensor technologies for rapid biological detection.

Asia Pacific Biosensor Technologies Market Trends

Asia Pacific is forecast to be the fastest-growing market for biosensor technologies, stimulated by rapid healthcare infrastructure expansion and rising chronic disease burden. The estimated regional share approaches 29% in 2026, supported by strong manufacturing ecosystems in China and India. Government-led digital health programs and cost-efficient production accelerate the adoption of point-of-care and wearable biosensor solutions.

Japan Biosensor Technologies Market Insights

Japan represents a dominant contributor within Asia Pacific biosensor revenue, contributing an estimated 30% of the regional market share in 2026, supported by advanced diagnostics infrastructure and strong domestic manufacturing capabilities. Aging population trends and rising diabetes prevalence increase demand for continuous monitoring devices. Regulatory support from the Pharmaceuticals and Medical Devices Agency accelerates approvals. In 2024, the expansion of continuous glucose monitoring technologies strengthened real-time diagnostics and clinical integration.

China Biosensor Technologies Market Insights

China represents the leading contributor within Asia Pacific, accounting for an estimated 35% share of regional biosensor revenue in 2026, driven by large-scale healthcare investments and rapid diagnostic adoption. National strategies such as Healthy China 2030 and Made in China 2025 accelerate domestic innovation and manufacturing scale. In 2025, the expansion of AI-integrated biosensor platforms and point-of-care diagnostics strengthened real-time monitoring capabilities across hospital networks.

Competitive Landscape

The global biosensor technologies market reflects a moderately fragmented structure with participation from global leaders and regional innovators. Key companies such as Abbott Laboratories, Medtronic plc, and F. Hoffmann-La Roche Ltd maintain strong positioning through diversified portfolios and advanced biosensor technologies, enabling broad clinical and commercial reach.

Competitive dynamics emphasize innovation, regulatory alignment, and global distribution strength. Players including Siemens Healthineers AG and Bio-Rad Laboratories, Inc. focus on precision diagnostics, digital integration, and continuous product development to strengthen market presence and expand application scope.

Key Industry Developments:

- In April 2026, a doctor-led AI-enabled platform integrating wearable biosensor patches and wristband devices was launched in Chennai to enable real-time patient monitoring and continuous vital tracking, advancing remote healthcare delivery and biosensor-based diagnostics.

- In May 2025, Nuclera and Cytiva entered a collaboration integrating biosensor-based protein characterization and eProtein Discovery systems with surface plasmon resonance technology, accelerating drug discovery workflows and enabling rapid transition from protein expression to validation within integrated biosensor-driven platforms.

- In April 2025, Medtronic received FDA approval for the Simplera Sync™ biosensor integrated with the MiniMed™ 780G system, strengthening real-time glucose monitoring and advancing automated insulin delivery within next-generation biosensor-driven diabetes management platforms.

Companies Covered in Biosensor Technologies Market

- Abbott Laboratories

- Medtronic plc

- F. Hoffmann-La Roche Ltd

- Siemens Healthineers AG

- Bio-Rad Laboratories, Inc.

- Danaher Corporation

- Thermo Fisher Scientific Inc.

- Nova Biomedical

- Dexcom, Inc.

- Senseonics Holdings, Inc.

- Biosensors International Group

- Universal Biosensors, Inc.

Frequently Asked Questions

The biosensor technologies market is projected to reach US$35 billion in 2026.

Rising demand for real-time disease monitoring, expansion of personalized healthcare, and integration of biosensors with digital and wearable technologies drive the biosensor technologies market.

The biosensor technologies market is poised to witness a CAGR of 9.2% from 2026 to 2033.

Expansion of point-of-care diagnostics, integration with artificial intelligence-enabled healthcare systems, and growing adoption in environmental and food safety monitoring create key market opportunities for biosensor technologies.

Some of the key market players include Abbott Laboratories, Medtronic plc, F. Hoffmann-La Roche Ltd, Siemens Healthineers AG, and Bio-Rad Laboratories, Inc.