- Processed Food

- Alcoholic Ice Cream Market

Alcoholic Ice Cream Market Size, Share and Growth Forecast, 2026 - 2033

Alcoholic Ice Cream Market by Alcohol Type (Spirit-Based, Wine-Based, Beer-Based), Alcohol Content ((Low (<1–5%), Medium (5–10%), High (>10%)), Consumer Demographic (Millennials, Gen Z, Premium Urban Consumers, Health-Conscious Consumers, Occasional Buyers), and Regional Analysis for 2026 - 2033

Alcoholic Ice Cream Market Share and Trends Analysis

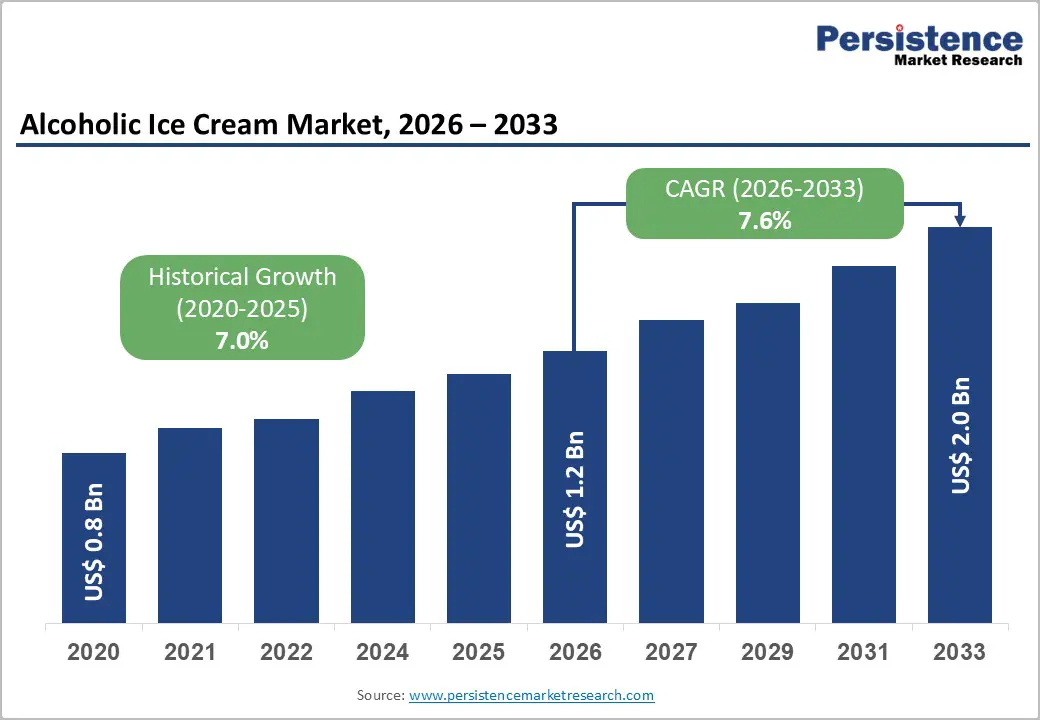

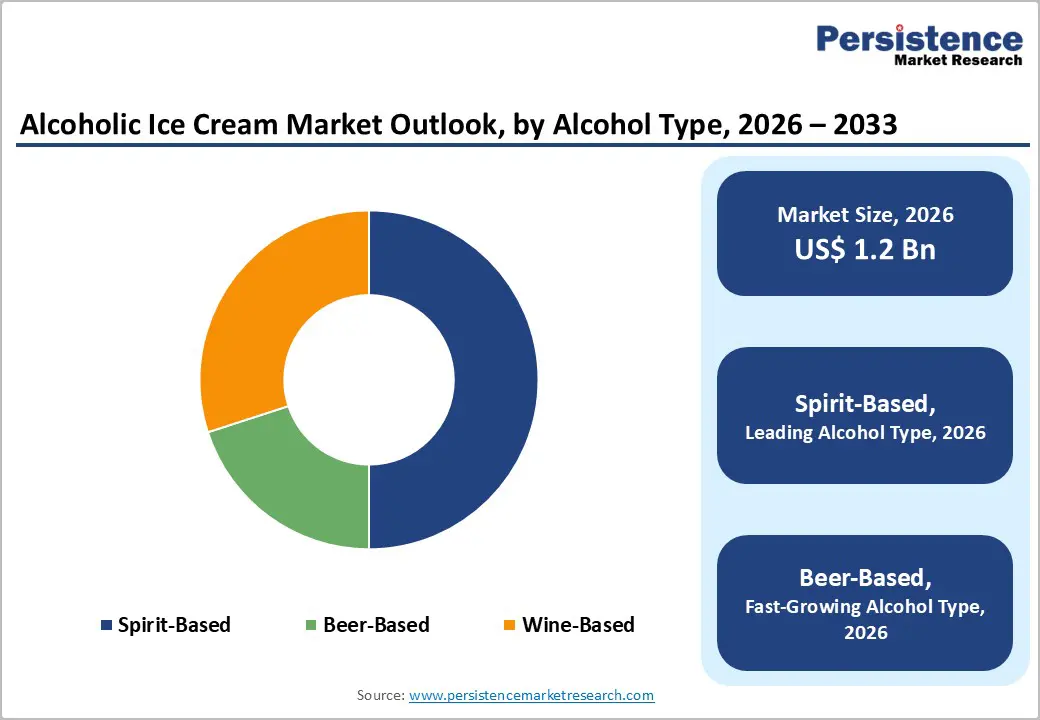

The global alcoholic ice cream market size is likely to be valued at US$ 1.2 billion in 2026 and is projected to reach US$ 2.0 billion by 2033, growing at a CAGR of 7.6% during the forecast period 2026–2033.

The market is expanding due to a clear shift in consumer preferences toward premium, experiential, and hybrid food products. Millennials and Gen Z increasingly seek indulgent desserts that combine novelty with social appeal, driving demand for alcohol-infused formats. The rise of artisanal and craft-based desserts, featuring unique flavors and premium ingredients, supports higher pricing and repeat consumption. Additionally, growing café culture, nightlife, and experiential dining trends position alcoholic ice cream as a social, shareable category. Functionally, it offers a dual-value proposition, dessert indulgence with controlled alcohol consumption, appealing across hospitality, retail, and events. Its adaptability to low–medium alcohol content (ABV) aligns with moderation trends, while urbanization and rising incomes in emerging markets further accelerate demand.

Key Industry Highlights

- Dominant Alcohol Type: Spirit-based variants are set to command around 50% of the revenue share in 2026, while beer-based products are likely to grow the fastest at a CAGR of 8.4% through 2033, supported by rising craft beer integration and consumer experimentation.

- Leading ABV Segment: Medium ABV (5–10%) is expected to lead with approximately 43% share in 2026, while low ABV variants are projected to be the fastest-growing at a CAGR of 8.1% during 2026–2033, driven by increasing health-conscious consumption trends.

- Key Consumer Demographics: Millennials are anticipated to dominate with nearly 38% share in 2026, whereas Gen Z is likely to emerge as the fastest-growing demographic segment at a CAGR of 8.7% through 2033, fueled by preference for novelty and experiential consumption.

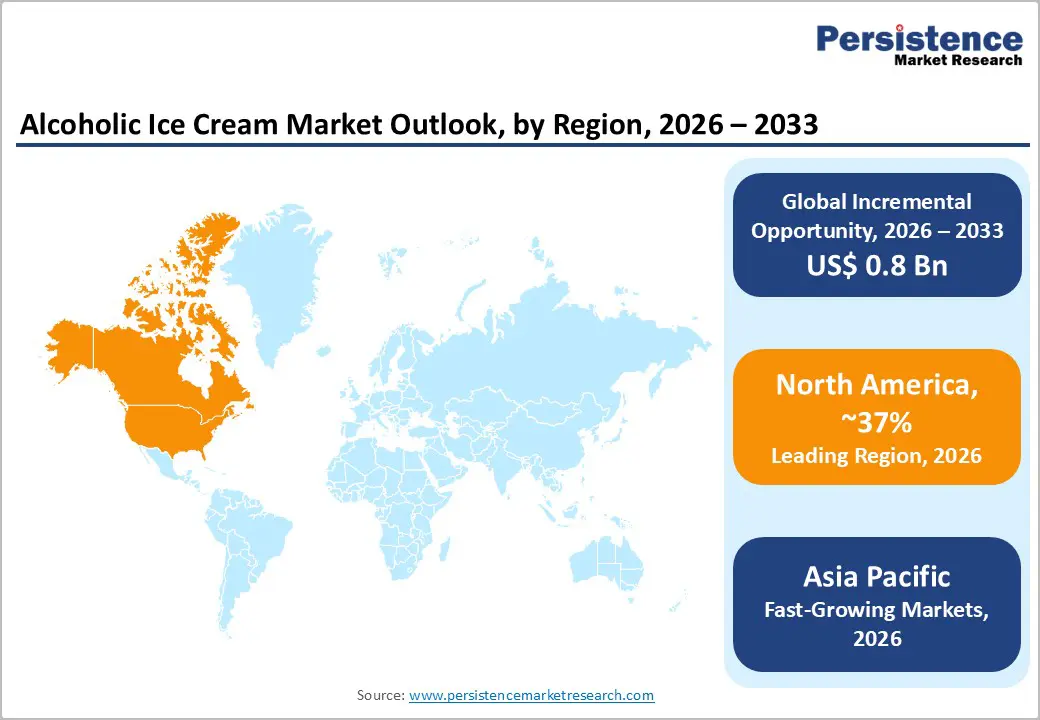

- Regional Leadership: North America is poised to lead with an estimated 37% market share in 2026, while Asia Pacific is projected to register the fastest growth at a CAGR of 8.9% through 2033, supported by urbanization and rising disposable incomes.

- Innovation Trends: Low-alcohol and premium product formats are increasingly dominating new product development, while innovative dessert formats are expected to witness strong growth through 2033, aligning with ongoing premiumization and evolving consumer preferences.

- Competitive Environment: Strategic partnerships and new product launches are playing a critical role in market expansion, with these approaches expected to drive sustained growth through 2033 by strengthening brand positioning and portfolio diversification globally.

| Key Insights | Details |

|---|---|

|

Alcoholic Ice Cream Market Size (2026E) |

US$ 1.2 Bn |

|

Market Value Forecast (2033F) |

US$ 2.0 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

7.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

7.0% |

DRO Analysis

Driver - Rising Demand for Premium and Experiential Desserts

The growing inclination toward premium dessert experiences is a major driver of the alcoholic ice cream market growth. Discretionary spending on premium food categories increased by over 5% annually between 2021 and 2025 in developed markets. Consumers are increasingly seeking multi-sensory indulgence, blending alcohol with desserts to create unique consumption experiences. This trend is particularly strong among urban populations with higher disposable incomes and exposure to global food trends, positioning alcoholic ice cream as a differentiated, high-value offering. It also reflects a broader shift toward premiumization across food and beverage categories.

This demand is further strengthened by the rise of café culture, nightlife, and experiential dining, where consumers prioritize novelty and shareable formats. The integration of craft spirits and artisanal production methods enhances perceived value and supports premium pricing strategies. As a result, manufacturers are focusing on innovative flavors and high-quality ingredients, which improve margins while reinforcing brand differentiation and repeat consumption. These evolving consumption patterns continue to expand the addressable market across both retail and foodservice channels.

Expanding Consumer Base and Retail Accessibility

Demographic shifts significantly influence alcoholic dessert demand, with Millennials and Gen Z together accounting for over 45% of global consumers in urban regions. These cohorts demonstrate a higher willingness to experiment with hybrid food-beverage products and favor social, experience-driven consumption. More than 60% of Gen Z consumers prefer unique flavor combinations, directly boosting demand for alcoholic ice cream, particularly in low-to-medium ABV formats aligned with moderation trends. Their strong digital engagement also amplifies product visibility and accelerates trend adoption.

Simultaneously, the expansion of organized retail infrastructure and online grocery platforms is improving product accessibility and distribution efficiency. E-commerce penetration in food and beverage increased by approximately 20–25% globally between 2020 and 2025, enabling brands to adopt direct-to-consumer models. Improved cold-chain logistics and evolving alcohol delivery regulations further support availability, reduce entry barriers for niche brands, and accelerate market scalability across urban centers. This enhanced accessibility is critical in sustaining consistent demand growth across diverse consumer segments.

Restraints - Stringent Alcohol Regulations and Compliance Complexity

The alcoholic ice cream market faces regulatory challenges due to its dual classification as both a food and alcoholic product. Regulations vary widely across countries, affecting labeling, distribution, and permissible alcohol content. For instance, U.S. Alcohol and Tobacco Tax and Trade Bureau (TTB) guidelines impose strict controls on ABV thresholds and interstate distribution. Compliance costs can increase operational expenses by 10–15%, particularly for small and mid-sized manufacturers. This regulatory fragmentation limits international expansion and complicates supply chain standardization. It also creates uncertainty for companies attempting to scale across multiple jurisdictions and manage cross-border operations effectively.

Recent regulatory developments further highlight this complexity. In 2025–2026, updated alcohol regulations introduced stricter labeling, classification, and compliance timelines, including mandatory disclosure of alcohol content and standardized drink information. While these changes improve consumer transparency, they also increase compliance burdens and require operational adjustments in packaging, formulation, and distribution. Frequent amendments and phased implementation timelines add to uncertainty, forcing companies to continuously adapt to evolving regulatory frameworks. This ongoing regulatory evolution increases overall cost pressures and can delay innovation cycles and product launches.

Cold Chain and Shelf-Life Constraints

Alcoholic ice cream requires robust cold chain infrastructure to maintain product integrity. According to FAO cold chain logistics data, up to 30% of perishable food products face losses in developing markets due to inadequate storage and transportation. The presence of alcohol can alter freezing points, impacting texture stability. These factors increase logistics costs and reduce shelf life, particularly in emerging economies, thereby constraining market penetration and increasing operational risk. Maintaining consistent product quality across long distances remains a critical challenge for manufacturers and distributors.

Industry developments continue to emphasize the scale of this challenge, particularly in emerging markets where infrastructure gaps persist. Governments and food safety authorities have intensified focus on reducing post-harvest and perishable losses, highlighting inefficiencies in refrigerated transport and storage systems. Despite ongoing investments, uneven cold chain development and rising energy costs continue to impact distribution efficiency. These structural limitations restrict expansion beyond major urban centers, increase spoilage risks, and make logistics optimization a critical requirement. As a result, companies must invest significantly in supply chain resilience to sustain profitability and ensure product consistency.

Opportunities - Growth of Low-ABV, Health-Oriented, and Innovative Product Formats

The shift toward health-conscious consumption presents a strong opportunity. WHO data indicates a gradual decline in per capita alcohol consumption in several developed countries, coupled with increased demand for low-alcohol alternatives. This has led to innovation in low-ABV (<5%) alcoholic ice cream, which appeals to moderation-focused consumers. The segment is expected to capture a significant share of incremental revenue, particularly among health-conscious urban populations. It also aligns with broader wellness trends shaping purchasing decisions across food and beverage categories. This shift is encouraging brands to actively reformulate and diversify their product portfolios.

Recent industry movements reinforce this opportunity. In 2025–2026, large-scale music festivals and experiential events such as Coachella and Tomorrowland expanded premium food and beverage offerings, including alcohol-infused desserts and hybrid formats, reflecting strong consumer demand for novelty-driven consumption experiences. These events increasingly feature curated dessert bars and branded collaborations, highlighting a shift toward indulgent yet moderated consumption. This trend validates the growing demand for low-ABV, innovative formats and creates new avenues for alcoholic ice cream brands to position themselves within experiential consumption environments. It also opens up opportunities for brand visibility through event-based marketing and partnerships.

Expansion across Emerging Markets and Urban Consumer Hubs

Emerging economies in Asia Pacific and Latin America offer untapped growth potential. Rising middle-class populations and urbanization are increasing demand for premium desserts. According to World Bank estimates, Asia’s middle class will exceed 3.5 billion by 2030. This creates a large addressable market for premium alcoholic desserts, especially in metropolitan areas. The concentration of younger consumers in urban centers further accelerates adoption of experiential and premium food products. This demographic advantage strengthens long-term consumption potential across these regions.

Industry trends further support this expansion, with the rapid growth of music festivals, nightlife events, and urban entertainment hubs across markets such as India, Southeast Asia, and Latin America. Events such as Sunburn Festival in India and similar large-scale gatherings have seen increased integration of premium food stalls and alcohol-based experiential products, reflecting evolving consumption patterns among younger audiences. These developments create favorable conditions for alcoholic ice cream brands to expand through localized production, partnerships, and targeted urban distribution strategies. They also enable companies to directly engage with high-value consumers in immersive, experience-driven settings.

Category-wise Analysis

Alcohol Type Insights

The spirit-based segment dominates the alcoholic ice cream market, accounting for approximately 50% share in 2026, driven by strong consumer preference for flavors infused with whiskey, rum, and vodka. These variants offer higher perceived value, align with premium positioning strategies, and blend effectively with dessert textures while maintaining flavor intensity, making them widely adopted across North America and Europe. Strong collaborations with spirit producers enhance differentiation and shelf visibility, while higher margins support continued investment and innovation. Recent developments in 2025–2026 further reinforce this dominance, with beverage companies expanding spirit-based dessert extensions and foodservice players introducing spirit-infused menus, supported by improving regulatory clarity for flavored alcoholic products.

The beer-based segment is projected to be the fastest growing, expanding at a CAGR of approximately 8.4% through 2033, supported by the global craft beer movement and increasing consumer experimentation. Its relatively lower alcohol content improves accessibility and aligns with moderation trends, particularly among younger consumers. The segment benefits from the rising popularity of flavored and craft beers, which translate well into dessert formats, especially in emerging markets where affordability and familiarity drive adoption. Manufacturers are introducing seasonal and innovative variants to capture demand, while fewer regulatory constraints in certain regions support wider distribution. Events such as the Great American Beer Festival and London Craft Beer Festival featured expanded dessert pairings and experimental beer-infused food concepts, reflecting growing consumer interest in hybrid formats and reinforcing the segment’s strong growth trajectory.

Consumer Demographic Insights

Millennials represent the largest consumer segment, contributing approximately 38% of total demand in 2026, driven by their preference for experiential dining and premium products. Their inclination toward indulgent, shareable, and socially engaging formats makes alcoholic ice cream highly appealing, particularly in urban environments. Higher disposable income and strong digital engagement further support consistent consumption patterns and brand discovery. Companies actively target this group through influencer marketing, collaborations, and limited-edition offerings, strengthening brand loyalty and premium positioning. The large-scale food and lifestyle events, such as the Taste of London Festival and NYC Wine & Food Festival expanded curated dessert experiences and alcohol-infused tasting sessions, highlighting Millennials’ strong engagement with premium, experience-driven consumption formats.

Gen Z consumers are the fastest-growing demographic segment, projected to expand at a CAGR of approximately 8.7% through 2033, driven by their preference for novelty, aesthetic appeal, and shareable experiences. This group actively seeks innovative flavors, visually distinctive products, and sustainable packaging, shaping product development strategies across the market. Their behavior is strongly influenced by digital trends, peer recommendations, and experiential marketing, accelerating the adoption of hybrid dessert formats such as alcoholic ice cream. Additionally, their preference for moderation supports demand for low-to-medium ABV products. The youth-centric events such as Rolling Loud Festival and Lollapalooza, increasingly incorporate branded food zones and visually engaging dessert concepts, amplifying social media visibility and reinforcing Gen Z’s influence on emerging consumption trends.

Regional Insights

North America Alcoholic Ice Cream Market Trends

North America is the leading region in the alcoholic ice cream market, accounting for approximately 37% share in 2026, driven primarily by the United States. The region benefits from a well-established innovation ecosystem, high disposable income, and a strong presence of premium dessert and alcohol brands. Consumer openness to hybrid food-beverage formats further strengthens demand, particularly in urban centers. Regulatory frameworks provide clarity on product classification and distribution, although they require strict compliance. The mature retail landscape and high awareness levels support consistent consumption patterns. Additionally, strong brand recognition and premium positioning contribute to sustained market leadership.

The regional momentum was reinforced by the expansion of direct-to-consumer alcohol shipping laws in several U.S. states, as reported by leading policy and legal news sources, enabling broader distribution of alcohol-infused food products. Major supermarket chains also increased investments in premium frozen dessert aisles and private-label innovation, reflecting rising demand for differentiated offerings. Furthermore, collaborations between dairy producers and licensed alcohol manufacturers gained traction, streamlining compliance and accelerating product commercialization. These developments highlight how regulatory evolution and retail transformation continue to strengthen market growth across North America.

Europe Alcoholic Ice Cream Market Trends

Europe represents a significant and mature market for alcoholic ice cream, supported by strong consumption across Germany, the U.K., France, and Spain. The region benefits from regulatory harmonization under EU frameworks, which facilitates cross-border trade and simplifies market entry. Consumer preference for premium, artisanal, and high-quality food products plays a key role in driving demand. Established retail networks and high product awareness further support market penetration. The cultural acceptance of alcohol in culinary applications also enhances the adoption of alcoholic ice cream. Additionally, premiumization trends continue to shape purchasing behavior across key markets.

The European market saw increased support from EU-backed agri-food innovation programs promoting value-added dairy products and sustainable processing methods. Governments across Germany and the Netherlands also introduced incentives for local food manufacturing and cold-chain modernization, improving distribution efficiency for perishable premium products. In parallel, leading grocery retailers expanded premium private-label dessert ranges with alcohol-inspired flavors, reflecting evolving consumer tastes. These developments underscore how policy support, sustainability focus, and retail innovation are collectively strengthening Europe’s market landscape.

Asia Pacific Alcoholic Ice Cream Market Trends

Asia Pacific is projected as the fastest-growing region, projected to expand at a CAGR of 8.9% through 2033, driven by rapid urbanization and rising disposable incomes. Countries such as China, Japan, India, and ASEAN nations are at the forefront of this growth, supported by expanding middle-class populations. Increasing exposure to global food trends and premium products is accelerating consumer adoption of alcoholic desserts. The region’s large and young population base further strengthens demand potential. Growing retail infrastructure and digital commerce platforms are enhancing product accessibility. These factors collectively position the Asia Pacific as a high-growth market.

Industry developments highlight strong regional momentum, particularly through large-scale urban events and evolving retail ecosystems. Events such as Tokyo Food Expo 2026 and Singapore Food Festival 2025 showcased innovative dessert concepts, including alcohol-infused offerings tailored to local tastes. In India, the expansion of premium retail chains and curated food events such as India Cocktail Week 2026 reflected rising consumer interest in experiential consumption. Additionally, increasing investments in cold chain logistics and local manufacturing are improving supply chain efficiency. These trends collectively support rapid market expansion and localized innovation across the Asia Pacific.

Competitive Landscape

The global alcoholic ice cream market is moderately fragmented, with established players such as Unilever, Diageo, and Häagen-Dazs leveraging strong brand equity and distribution networks. These companies focus on premiumization, flavor innovation, and collaborations with alcohol brands to strengthen market positioning. Investment in branding, packaging, and direct-to-consumer channels further enhances their competitive advantage. Their scale and global reach enable consistent product development and market expansion.

Niche players such as Tipsy Scoop, BuzzBar, and Mercer’s Dairy emphasize artisanal production and unique flavor offerings to differentiate themselves. Regulatory complexities and cold chain requirements create moderate entry barriers, limiting new competitors. However, e-commerce and evolving retail models are enabling smaller brands to scale efficiently. Market competition is expected to intensify through partnerships, innovation, and selective acquisitions.

Key Industry Developments

- In March 2026, Tipsy Scoop accelerated its expansion through a franchise-driven “barlour” model, opening a new outlet in Baltimore and targeting high-traffic urban markets such as Miami, Dallas, and Boston. This asset-light approach enables rapid scaling with minimal on-site production, strengthening its footprint in metropolitan consumption hubs.

- In November 2025, Unilever spun off its ice cream division into The Magnum Ice Cream Company (TMICC) after increasing investments in premium formats and adult-oriented offerings. The strategy focused on indulgent, evening-consumption products and innovation (e.g., bite-sized formats), aligning with growing demand for premium and experiential dessert categories.

Companies Covered in Alcoholic Ice Cream Market

- Tipsy Scoop

- Häagen-Dazs

- Unilever

- Diageo

- Ben & Jerry’s

- BuzzBar

- Mercer’s Dairy

- Snobar

- Arctic Buzz

- Frozen Pints

- Brewskey

- Baileys

- Ample Hills Creamery

Frequently Asked Questions

The global alcoholic ice cream market is projected to reach US$ 1.2 billion in 2026.

Rising demand for premium desserts, increasing preference for low-ABV indulgence, and expanding urban consumer base drive the market.

The alcoholic ice cream market is expected to grow at a CAGR of 7.6% from 2026 to 2033.

Growth in emerging markets, innovation in low-ABV variants, and premium product diversification create key opportunities.

Tipsy Scoop, Unilever, Häagen-Dazs, Diageo, and Mercer’s Dairy are key players in the market.