- Beverages

- Non-Alcoholic Beverages Market

Non-Alcoholic Beverages Market Size, Share, and Growth Forecast 2026 - 2033

Non-Alcoholic Beverages Market by Product Type (Carbonated Soft Drinks, Juices & Nectars, Bottled Water, Energy & Sports Drinks, Dairy-based Beverages, Plant-based Beverages, RTD Tea and Coffee, Others), Packaging Type, Distribution Channel, and Regional Analysis, 2026 - 2033

Non-Alcoholic Beverages Market Size and Trend Analysis

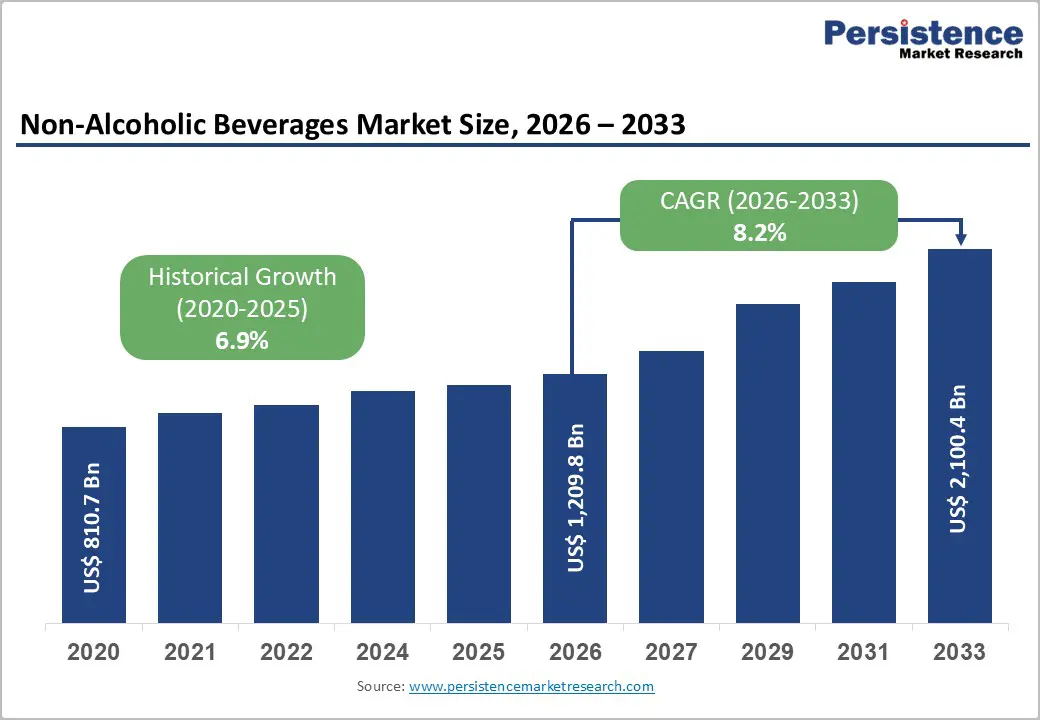

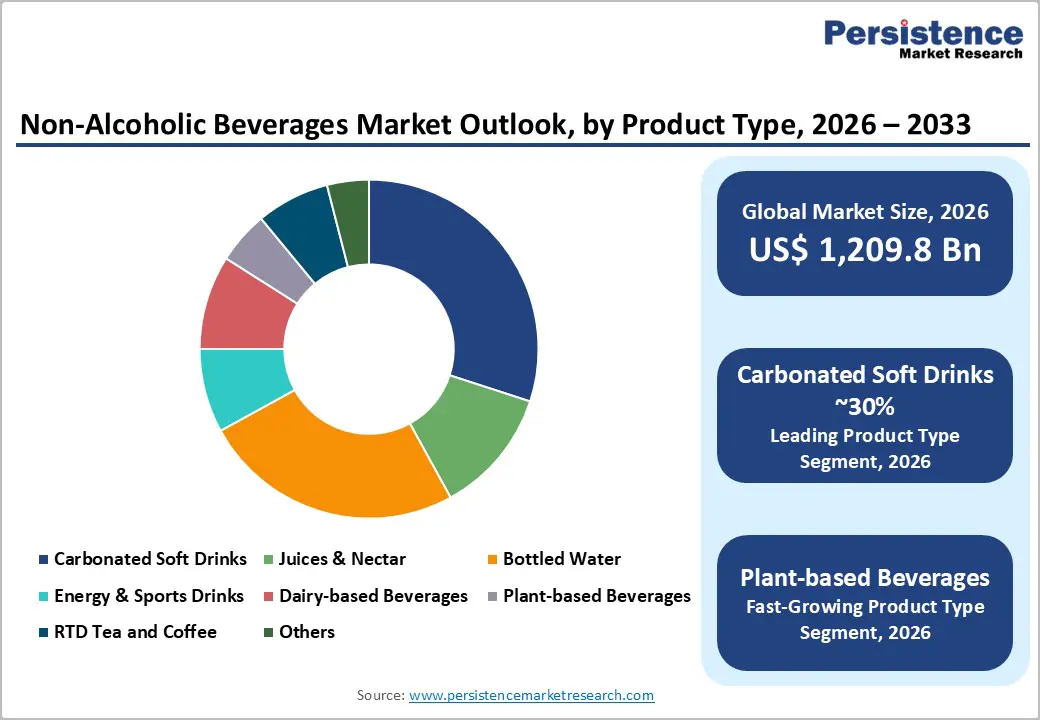

The global non-alcoholic beverages market size is expected to be valued at US$ 1,209.8 billion in 2026 and projected to reach US$ 2,100.4 billion by 2033, growing at a CAGR of 8.2% between 2026 and 2033.

The global market includes a wide range of drinks such as carbonated soft drinks, bottled water, juices, energy and sports drinks, dairy-based beverages, plant-based alternatives, and ready-to-drink tea and coffee. This market is driven by rising consumer demand for convenience, hydration, and healthier beverage options. Increasing urbanization, changing lifestyles, and growing disposable incomes are further supporting market expansion. Innovation in flavors, functional ingredients, and low- or zero-sugar formulations is reshaping product offerings. Additionally, expanding distribution channels, including supermarkets and online platforms, are enhancing product accessibility, making the market highly competitive and rapidly evolving globally.

Key Highlights:

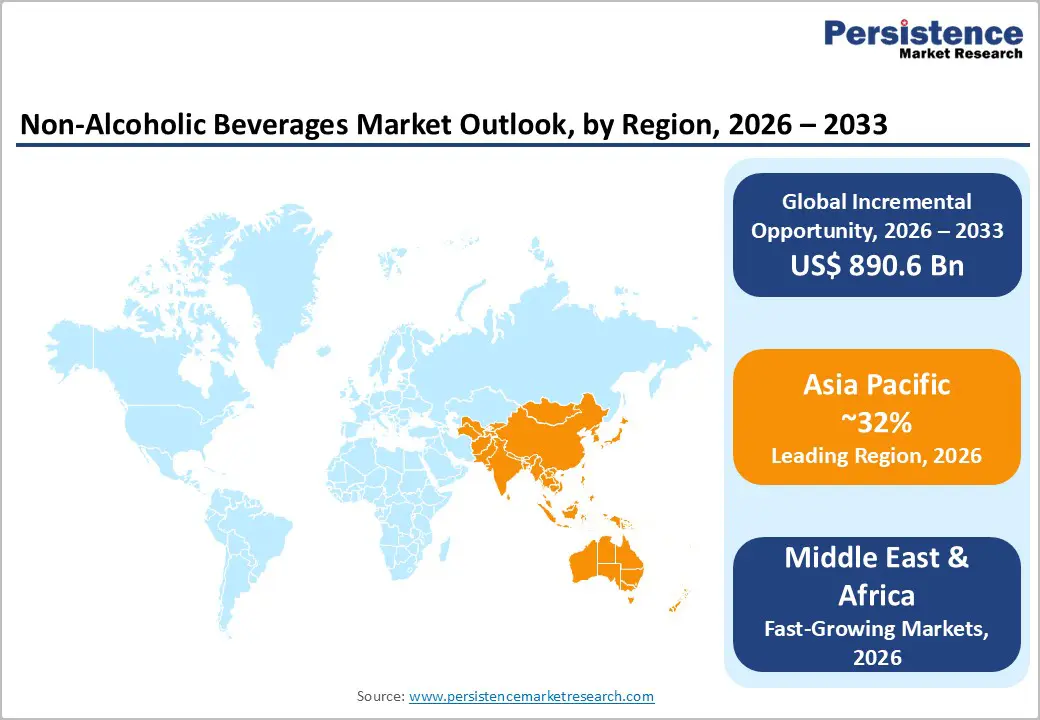

- Leading Region: Asia Pacific dominates the non-alcoholic beverages market due to large population, rising incomes, and strong bottled water and soft drink consumption growth.

- Fastest-growing Region: Middle East & Africa is rapidly expanding, driven by urbanization, young population, rising incomes, and high bottled water consumption dominating beverage preferences.

- Dominant Product: Carbonated soft drinks lead with around 30% share, supported by strong global brands, extensive distribution networks, and continuous innovation in flavors and zero-sugar variants.

- Fastest-growing Product: Plant-based beverages and functional RTD drinks grow fastest, driven by health awareness, dairy alternatives demand, and increasing preference for convenient ready-to-drink formats.

- Key Opportunity: Digital and omni-channel distribution, including e-grocery, subscriptions, and quick commerce, is unlocking new revenue streams with strong double-digit growth in online beverage sales.

| Key Insights | Details |

|---|---|

| Global Non-Alcoholic Beverages Market Size (2026E) | US$ 1,209.8 billion |

| Market Value Forecast (2033F) | US$ 2,100.4 billion |

| Projected Growth CAGR (2026 - 2033) | 8.2% |

| Historical Market Growth (2020 - 2025) | 6.9% |

Market Dynamics

Drivers - Health and wellness shift away from sugary drinks

A major driver for non-alcoholic beverages is the global pivot toward health and wellness, with consumers actively reducing sugar intake and prioritizing hydration and functional benefits. World Health Organization (WHO) data show that more than 116 countries apply excise taxes on sugar-sweetened beverages (SSBs), signalling growing regulatory pressure on high-sugar soft drinks and encouraging reformulation and portfolio shifts toward low- and no-sugar alternatives. Empirical research has linked higher soft drink consumption with significantly increased prevalence of overweight and obesity, reinforcing public and clinical guidance to curb regular soda intake. In response, brands are rapidly expanding portfolios of zero-sugar colas, flavored waters, and lightly sweetened RTD teas and coffees, while bottled water and functional beverages gain share as everyday hydration and wellness choices.

The Growing Popularity of Sober-Curious Lifestyles is Positively Influencing the Demand for Non-Alcoholic Beverages

The rise of sober-curious lifestyles is significantly increasing the global demand for non-alcoholic beverages. More consumers are choosing to cut back on alcohol for health and personal reasons, leading to a shift in the beverage market. Events like Sober October and Dry July inspire alcohol-free living, raising awareness of non-alcoholic options. Campaigns such as the Irish Heart Foundation's "On the Dry" in January further encourage sobriety, transforming consumer habits. As these movements gain momentum, brands have exciting opportunities to develop innovative non-alcoholic drinks that cater to this growing market. This shift drives a wave of creativity, offering health-conscious alternatives that align with the sober-curious lifestyle.

Restraints - Sugar Content Limitations Affect the Taste Profile of Non-Alcoholic Beverages

Sugar content limitations pose a significant challenge for the non-alcoholic beverages market. As consumers grow more health-conscious and seek lower-sugar options, manufacturers face pressure to reduce sugar levels. While this shift promotes better health, it often compromises taste, making it difficult to deliver the flavor and sweetness consumers expect from traditional drinks.

To compensate, many brands turn to artificial sweeteners or natural alternatives like stevia, but these often fail to recreate the authentic experience. Striking a balance between flavor and compliance with sugar regulations is crucial. As regulatory pressures around sugar content intensify, the market faces the challenge of delivering satisfying, flavorful beverages without compromising on health-conscious ingredients, which could limit consumer appeal.

Opportunities - Companies Tap into the Growing Preference for Dairy-Free, Vegan-Friendly Nutritional Beverages

Companies in the non-alcoholic beverages market have a prime opportunity to capitalize on the growing demand for dairy-free and vegan-friendly drinks. As health-conscious consumers, particularly younger generations, increasingly seek plant-based alternatives, businesses can attract a diverse audience, including those with lactose intolerance and committed vegans.

A prime example is Zevia®, which offers beverages that are naturally sweetened with plant-based ingredients, free from artificial colors, flavors, and sweeteners. These drinks are also non-GMO verified, making them a perfect example of how companies can leverage clean, plant-based ingredients to meet growing consumer demands in the non-alcoholic beverage sector.

Category-wise Analysis

Product Type Insights

Within product types, carbonated soft drinks (CSDs) remain the leading revenue-generating segment of the non-alcoholic beverages market, accounting for an estimated 30% share in 2026. Despite long-term per-capita declines in some mature markets, CSDs still command substantial household penetration and brand equity, with global soft drinks retail volume continuing to grow around 3% annually and carbonated soft drinks retaining a dominant position in many portfolios. Brand valuation analyses confirm that iconic CSD brands such as Coca-Cola, Pepsi, Dr. Pepper, and Sprite occupy most of the top global non-alcoholic drink brand rankings, reflecting their scale, marketing power, and distribution reach. At the same time, reformulation toward zero-sugar and reduced-sugar lines, limited-edition flavors, and cross-category innovations (for example, colas blended with coffee or functional ingredients) are helping CSDs maintain relevance even as consumer preferences shift toward healthier and more functional options.

Distribution Channel Insights

Across distribution channels, hypermarkets and supermarkets constitute the largest organized retail Hypermarkets and supermarkets remain the dominant organized retail channel for non-alcoholic beverages, driven by strong demand for multi-pack carbonated drinks, bottled water, juices, and family-sized formats. These large-format stores account for approximately 40-50% of total soft drink sales. Their leadership is supported by one-stop shopping convenience, promotional pricing, and a wide assortment of brands. This channel is particularly influential in developed markets such as North America and Europe, where it anchors off-trade sales and in-store marketing strategies. Convenience stores and forecourt outlets also play a vital role, especially for single-serve and on-the-go consumption, with notable growth in impulse purchases.

Online retail is emerging as the fastest-growing distribution channel, fueled by the expansion of e-grocery and direct-to-consumer models. Rapid digital adoption, strong growth in home delivery, and rising demand for functional and premium beverages are accelerating this shift. Online platforms are especially important for innovative brands and ready-to-drink beverages.

Regional Insights

North America Non-Alcoholic Beverages Market Trends and Insights

In North America, particularly the U.S., non-alcoholic beverages are undergoing a pronounced shift from traditional sugary sodas toward low- and zero-sugar soft drinks, bottled and flavored waters, energy drinks, and functional RTD beverages. Per-capita soft drink consumption in the U.S. has been on a gradual long-term decline, with estimates showing per-capita soft drink consumption of around 41.9 gallons in 2025 and an annualized contraction of about 0.4% between 2020 and 2025, reflecting heightened awareness of obesity and diabetes risks linked to high sugar intake. At the same time, demand for premium energy drinks, performance hydration products, and RTD coffees and teas is robust, with functional and wellness-positioned beverages capturing a growing share of shelf space and marketing budgets.

The region is also a hotbed of innovation and regulatory experimentation. U.S. federal authorities and leading medical organizations continue to spotlight excess sugar consumption, while several states and municipalities have explored or implemented soda taxes and marketing restrictions, reinforcing industry-wide reformulation and portion-control strategies. Major players such as The Coca-Cola Company and PepsiCo, Inc. are investing heavily in zero-sugar colas, enhanced waters, sports and energy drinks, and protein or prebiotic beverages, alongside portfolio extensions into hybrid formats such as colas with coffee and functional RTD coffees. Strong e-commerce penetration and sophisticated retail media networks further support innovation and premiumization in the North American non-alcoholic beverages landscape.

Asia Pacific Non-Alcoholic Beverages Market Trends and Insights

Asia Pacific is the largest and one of the most dynamic regions for non-alcoholic beverages, underpinned by rapid urbanization, rising middle-class incomes, and diverse local beverage traditions. Regional statistics show that soft drinks especially non-carbonated soft drinks and bottled water are the largest non-alcoholic categories, with bottled water alone accounting for roughly half of the non-alcoholic beverage market in China, driven by concerns over tap water quality. In India, non-alcoholic beverages spanning bottled water, RTD teas, fruit juices, energy drinks, and plant-based beverages are experiencing robust demand as urban consumers, particularly millennials and Gen Z, seek convenient, functional, and natural ingredient-based products; the Indian non-alcoholic beverages market expanded steadily in recent years on the back of rising health awareness and modern retail and e-commerce penetration.

The region also offers significant manufacturing and innovation advantages. Many global beverage companies have established large-scale bottling, co-packing, and ingredient sourcing operations in Asia Pacific to serve both domestic and export markets efficiently. Governments in several countries are combining sugar-reduction strategies with industrial policy, encouraging reformulation, local fruit and dairy value chains, and investments in sustainable packaging. Simultaneously, the expansion of modern retail, convenience stores, and fast-growing online grocery platforms across China, Japan, India, and ASEAN countries is widening access to premium bottled waters, functional drinks, and RTD coffees and teas. These dynamics, combined with a young, digitally engaged consumer base, underpin Asia Pacific’s leadership in global non-alcoholic beverages growth.

Competitive Landscape

The global non-alcoholic beverages market is highly competitive, featuring several global giants alongside an increasing number of regional brands and startups. This dynamic environment is being driven by growing foreign direct investment (FDI), strategic distribution partnerships, and increased investments in sustainability initiatives. Companies are actively innovating in eco-friendly packaging and developing cleaner, healthier formulations in response to consumer demand. Additionally, government regulations particularly those targeting sugar reduction are shaping product reformulation strategies. These evolving factors, combined with rapid innovation and shifting consumer preferences, are redefining the market's direction.

Key Developments:

- In March 2026, George Clooney, along with nightlife entrepreneur Rande Gerber and Mike Meldman, introduced Crazy Mountain, a new non-alcoholic beverage line featuring a lager and a lime-flavored beer. The products are set to roll out in select markets this week and are already available through the brand’s official website.

- In November 2025, India-based beverage company Varun Beverages Limited (VBL), a key bottling partner of PepsiCo, was reported by ET Retail to be in advanced talks with its long-standing collaborator to enter the alcoholic beverages segment in India.

- In April 2025, Nestlé announced the expansion of its Nescafé Ready-to-Drink cold coffee range to India, the Middle East and North Africa (MENA) region, and Brazil. This move aims to cater to the rising demand from young consumers seeking convenient, flavorful, and on-the-go beverage options that match their fast-paced, modern lifestyles.

- In March 2025, PepsiCo, Inc. announced a definitive agreement to acquire Poppi, a rapidly growing prebiotic soda brand, for $1.95 billion. This strategic move underscores PepsiCo’s commitment to expanding its functional beverage portfolio and strengthening its position in the gut-health and better-for-you drinks segment.

- In March 2025, Red Bull unveiled its first-ever U.S. Spring Edition energy drink, introducing a refreshing Grapefruit & Blossom flavor. This limited-time offering is available in both sugar and sugar-free variants, reflecting the brand’s effort to cater to evolving consumer preferences for seasonal and flavorful energy drink options.

- In February 2025, Coca-Cola expanded its functional beverage portfolio by launching a new prebiotic soda brand, Simply Pop. The move marks the company's strategic entry into the rapidly growing prebiotic soda category, directly challenging established players.

Companies Covered in Non-Alcoholic Beverages Market

- The Coca-Cola Company

- PepsiCo, Inc.

- Keurig Dr Pepper Inc.

- Del Monte Pacific Limited

- Nestlé S.A.

- Danone S.A.

- Monster Beverage Corporation

- Red Bull GmbH

- SunOpta Inc.

- Starbucks Corp.

- Asahi Group Holdings

- Suntory Holdings Limited

- Almarai

- Nongfu Spring

- Parle Agro

- Hector Beverages Private Limited

- Bisleri International Pvt. Ltd.

- AMUL

- Reliance Industries

- Refresco

- Others

Frequently Asked Questions

The global non-alcoholic beverages market is expected to reach around US$ 1,209.8 billion in 2026.

The growing popularity of sober curious lifestyles is positively influencing the demand for non-alcoholic beverages.

Asia Pacific leads the global non-alcoholic beverages market, benefiting from its large population, rapid urbanization, high bottled water and soft drink consumption, and growing middle class in countries such as China, India, and Southeast Asian economies.

Companies can tap into the growing preference for dairy-free, vegan-friendly nutritional beverages, is the key market opportunity for companies in the Global Non-Alcoholic Beverages market.

Key players in the Global Non-Alcoholic Beverages industry include The Coca-Cola Company, PepsiCo, Inc., Keurig Dr. Pepper Inc., Nestlé S.A., Danone S.A., Monster Beverage Corporation, and others.