- Medical Devices

- Aesthetic Medical Devices Market

Aesthetic Medical Devices Market Size, Share, and Growth Forecast 2026 - 2033

Aesthetic Medical Devices Market by Technology (Laser-Based, Light-Based, Electromagnetic Energy-Based, Ultrasound-Based, Cryolipolysis, Suction-Based, Plasma Energy-Based), by Component (Facial Skin Resurfacing, Fat Reduction and Body Contouring, Skin Tightening, Cellulite Reduction, Photorejuvenation, Hair Removal, Feminine Rejuvenation, Tattoos and Pigmentation, Acne and Acne Scars, Others), End-user (Dermatology and Cosmetic Clinics, Hospitals and Clinics, Medical Spas, Others), by Regional Analysis, 2026-2033

Aesthetic Medical Devices Market Share and Trends Analysis

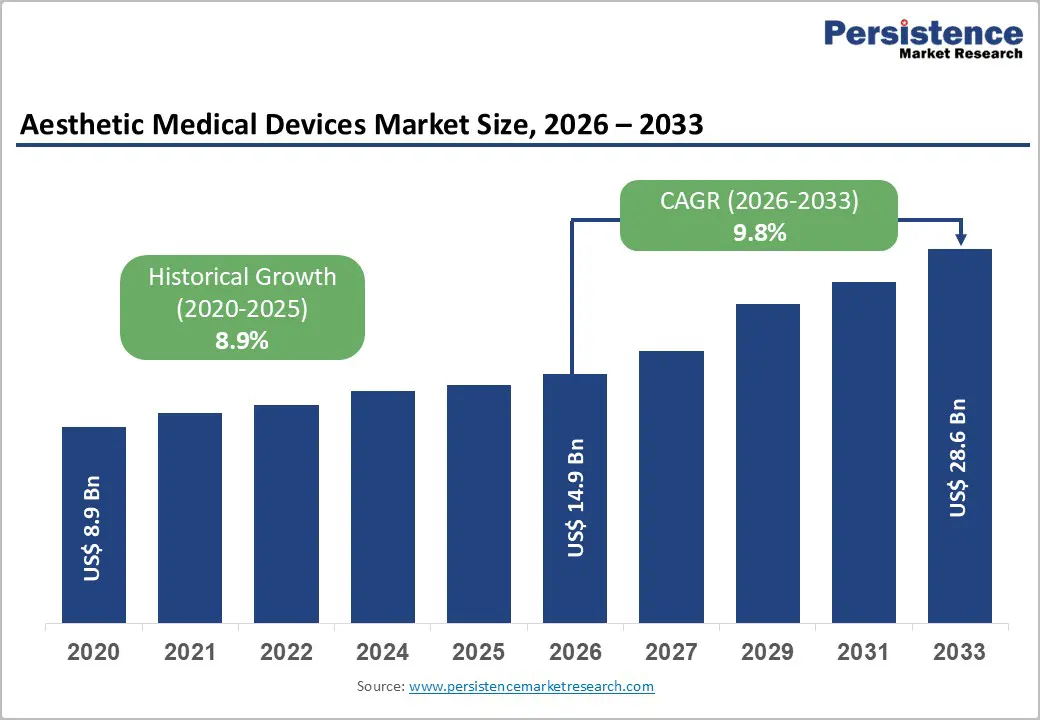

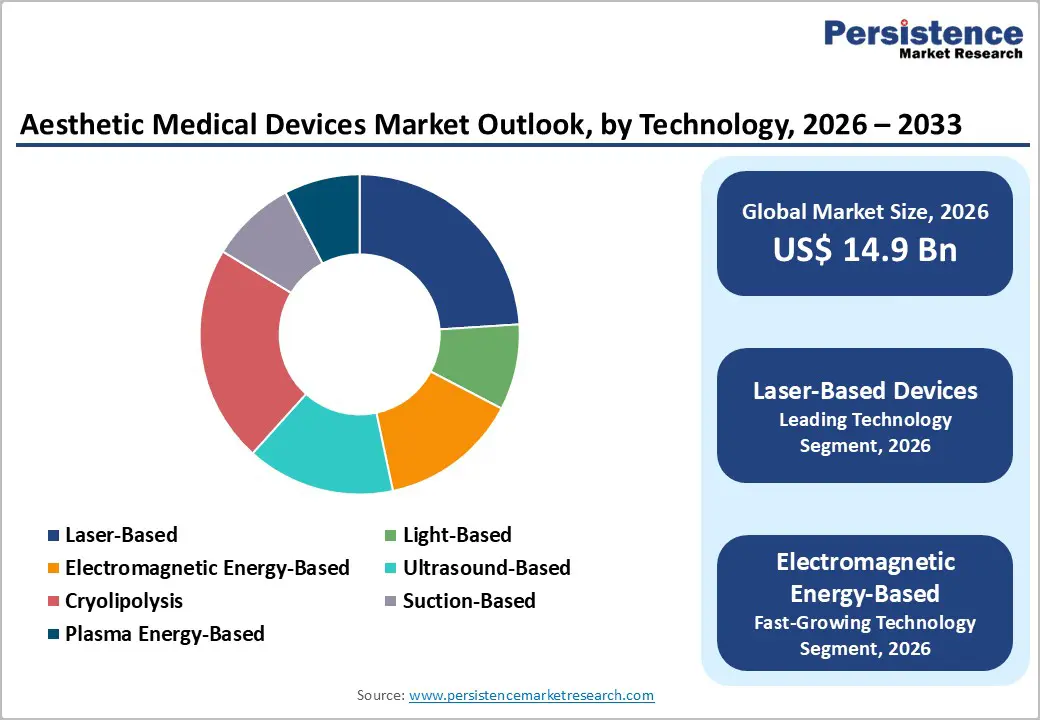

The global aesthetic medical devices market size is expected to be valued at US$ 14.9 billion in 2026 and projected to reach US$ 28.6 billion by 2033, growing at a CAGR of 9.8% between 2026 and 2033. The market's sustained growth is driven primarily by escalating consumer demand for minimally invasive aesthetic procedures, advancing energy-based device technologies, and rising global disposable incomes.

Demographic shifts toward an aging population, combined with heightened social media influence on beauty standards, have created unprecedented demand for non-surgical aesthetic solutions. Additionally, expanding healthcare infrastructure in emerging markets and favorable regulatory environments across key regions continue to drive market growth, as technological innovations enable safer, faster procedures with shorter recovery times.

Key Industry Highlights:

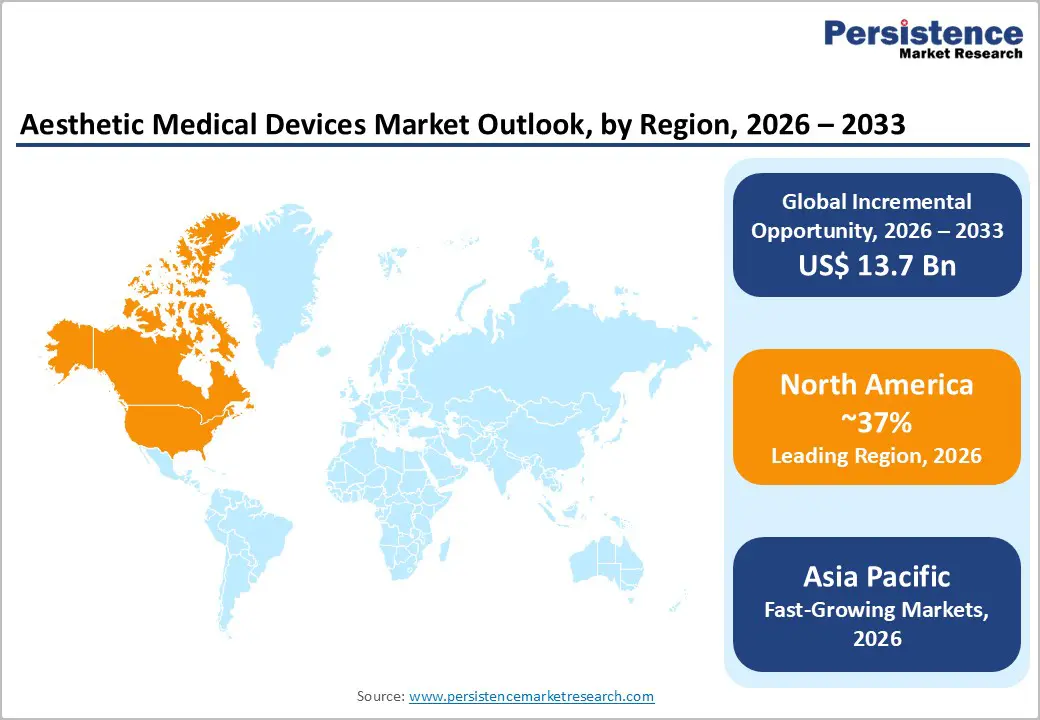

- North America dominates the aesthetic medical devices market with approximately 37% market share in 2025, supported by mature healthcare infrastructure, high consumer disposable incomes, advanced regulatory frameworks, and widespread adoption of minimally invasive aesthetic procedures across diverse demographic groups.

- Asia-Pacific represents the fastest-growing global region with a projected 14.1% CAGR through 2035, driven by expanding middle-class populations, rising beauty consciousness through social media influence, cultural emphasis on youthful appearance, and favorable government healthcare initiatives in China, India, Japan, and Southeast Asian countries.

- Laser-based aesthetic devices maintain a dominant market position with 24% market share in 2025, reflecting established clinical validation, extensive FDA approvals, and proven efficacy for hair removal, skin rejuvenation, and photorejuvenation across diverse patient populations and skin types.

- Electromagnetic energy-based aesthetic devices represent the fastest-growing technology segment with highest CAGR projected through 2032, driven by expanding non-invasive skin tightening and body contouring applications, enhanced safety profiles for diverse skin phototypes, and emerging clinical evidence supporting efficacy across multiple aesthetic indications.

| Key Insights | Details |

|---|---|

| Aesthetic Medical Devices Market Size (2026E) | US$ 14.9 billion |

| Market Value Forecast (2033F) | US$ 28.6 billion |

| Projected Growth CAGR (2026-2033) | 9.8% |

| Historical Market Growth (2020-2025) | 8.9% |

Market Dynamics

Drivers - Rising Prevalence of Skin Disorders and Aesthetic Consciousness

The global population faces an escalating burden of skin conditions, with 30-70% of individuals worldwide estimated to suffer from some form of skin disorder. This growing prevalence has catalyzed heightened aesthetic consciousness, particularly among younger demographics influenced by digital beauty trends and social media platforms. The International Society of Aesthetic Plastic Surgery (ISAPS) Global Survey 2024 documented that aesthetic procedures reached approximately 38 million cases worldwide, representing a 40% increase from 2020. This surge reflects not only therapeutic demand for treating acne, rosacea, and pigmentation disorders but also preventive and maintenance-focused aesthetic procedures. The normalization of cosmetic enhancements across age groups, coupled with increasing affordability through emerging market accessibility, continues to expand the addressable patient population. Non-invasive and minimally invasive procedures now account for approximately 54% of all aesthetic procedures globally, with botulinum toxin injectables surpassing 7.8 million procedures and hyaluronic acid fillers exceeding 6.3 million procedures annually, demonstrating sustained consumer preference for technologies that deliver visible results without surgical risks or significant downtime.

Technological Advancements in Energy-Based Aesthetic Devices

Innovation in aesthetic device technology has fundamentally transformed treatment efficacy and safety profiles, driving accelerated market adoption. Advanced laser platforms utilizing multi-wavelength and synchronized delivery systems now address multiple skin concerns simultaneously while minimizing adverse effects across diverse skin types. The U.S. Food and Drug Administration (FDA) approved breakthrough technologies including fractional laser systems for hair loss treatment and next-generation hyaluronic acid injectable formulations with enhanced longevity, expanding the scope of clinical applications. Recent developments, such as SPLENDOR X's dual-wavelength BLEND X technology approved in April 2025 by Lumenis Be Ltd., demonstrate clinical efficacy for hair removal across all Fitzpatrick skin types, addressing previously underserved darker skin population.

Innovations in picosecond and nanosecond laser technologies have revolutionized tattoo removal and pigmentation correction with reduced post-inflammatory hyperpigmentation, particularly benefiting ethnic populations. Radiofrequency, ultrasound, and plasma energy-based systems provide non-invasive skin tightening alternatives, while cryolipolysis technology continues to advance for targeted fat reduction. These technological progressions reduce procedure duration, minimize recovery periods, and enhance clinical outcomes, compelling healthcare providers and medical spas to upgrade equipment and expand service offerings. Integration of artificial intelligence and machine learning algorithms for treatment personalization and real-time monitoring represents the frontier of aesthetic device innovation, promising to further accelerate market growth.

Restraints - High Capital Investment and Regulatory Compliance Burden

Aesthetic device manufacturers and healthcare practitioners face substantial barriers related to stringent regulatory requirements and elevated capital expenditure demands. In developed markets like the United States, European Union, and Australia, comprehensive FDA approval, CE marking compliance, and state-specific licensing impose resource-intensive clinical trials, safety documentation, and post-market surveillance obligations. These compliance mechanisms, while essential for patient safety and product credibility, significantly extend product commercialization timelines and inflate research and development budgets, disadvantaging smaller enterprises and emerging manufacturers.

In emerging markets such as India, China, and Brazil, navigating fragmented regulatory frameworks presents additional complexities; the Indian Medical Devices Rules (MDR) 2017 mandate stringent manufacturing standards and compliance certifications that challenge importers and smaller domestic manufacturers. Global trade dynamics, including import tariffs and duties on aesthetic devices, inflate equipment costs and influence healthcare provider adoption rates, particularly in price-sensitive regions. The capital-intensive nature of aesthetic device businesses, requiring significant upfront investments for equipment acquisition, staff training, and facility infrastructure, constrains facility expansion, especially among smaller dermatology clinics and medical spas operating on moderate margins. This regulatory and financial burden disproportionately disadvantages emerging players, consolidating market share among established manufacturers with established regulatory pathways and substantial financial resources.

Patient Safety Concerns and Procedure Complication Risks

Despite advances in non-invasive technologies, persistent safety concerns and the potential for adverse complications remain significant market restraints. Complications, including post-inflammatory hyperpigmentation, thermal burns, paradoxical hair growth with certain laser systems, and vascular or neurological injuries, have been documented, particularly when procedures are administered by insufficiently trained practitioners. The proliferation of non-physician practitioners and under-trained aestheticians in unregulated settings, especially in emerging markets, has amplified patient safety concerns and inconsistent clinical outcomes. Additionally, consumer anxiety regarding long-term safety profiles of novel technologies, injectable fillers, and energy-based devices persists despite extensive clinical validation.

Regulatory bodies worldwide increasingly scrutinize adverse event reporting, with growing awareness of complications driving cautious consumer adoption. In 2024-2025, regulatory agencies, including the FDA, intensified post-market surveillance of aesthetic devices, leading to periodic product warnings and use restrictions that create consumer hesitation. Furthermore, the rise of counterfeit and substandard aesthetic devices in unregulated markets, particularly in Southeast Asia and parts of Africa, compromises clinical safety and undermines consumer confidence in aesthetic procedures. These safety concerns necessitate comprehensive training protocols, quality assurance mechanisms, and informed consent processes that increase operational costs for providers and may limit procedure accessibility in resource-constrained settings.

Opportunities - Integration of Digital Health and Telemedicine in Aesthetic Consultations

The integration of telemedicine platforms and digital health technologies with aesthetic medicine represents a significant market expansion opportunity, particularly for pre-consultation, post-procedure monitoring, and remote treatment planning. The World Health Organization (WHO) foundation partnerships established in 2025 with dermatological beauty organizations emphasize expansion of healthcare access through digital platforms, creating momentum for telemedicine adoption in aesthetic fields. Advanced digital platforms enabling virtual consultations, photo documentation systems for treatment planning, and mobile applications for appointment management and follow-up monitoring are expanding patient access to specialized dermatologists beyond geographic limitations. This digital integration aligns with broader telemedicine adoption trends, with healthcare systems increasingly incorporating virtual aesthetic consultations to reduce wait times and enhance patient convenience.

Emerging markets particularly benefit from telemedicine expansion, addressing the documented deficit of trained dermatologists; studies indicate over one-third of countries have fewer than one dermatologist per 100,000 population, leaving 3.5 billion individuals in dermatological deserts. Manufacturers developing aesthetic devices with integrated digital monitoring capabilities, artificial intelligence-enabled treatment optimization, and cloud-connected documentation systems are positioned to capture market share as healthcare providers increasingly digitize operations. Subscription-based aesthetic maintenance packages, enabled through digital appointment systems and automated treatment reminders, represent emerging business models generating recurring revenue streams and enhanced patient loyalty. The convergence of telemedicine accessibility and minimally invasive aesthetic procedures promises to democratize aesthetic treatment access globally while generating substantial device demand.

Category-wise Insights

Technology Insights

The laser-based aesthetic devices segment maintains dominant market leadership, commanding approximately 24% market share in 2025 with sustained expansion projected through the forecast period. Laser-based systems' continued leadership reflects decades of clinical validation, extensive FDA approvals across multiple indications, and established treatment protocols for hair removal, skin rejuvenation, and pigmentation correction. The Nd: YAG, alexandrite, and diode laser wavelengths remain gold standards for non-invasive skin tightening due to their proven ability to stimulate collagen remodeling and tissue remodeling with minimal downtime. Advanced multi-wavelength platforms combining synchronized delivery mechanisms enhance treatment versatility, enabling practitioners to address diverse patient concerns within single consultation sessions.

Clinical evidence demonstrating non-ablative fractional laser effectiveness for epidermal thickening in Asian photodamage cases has expanded laser adoption across diverse ethnic populations. However, the electromagnetic energy-based devices segment emerges as the fastest-growing technology category, projected to achieve the highest CAGR through 2032, driven by expanding applications in non-invasive skin tightening, cellulite reduction, and body contouring. Radiofrequency and microwave energy devices offer advantages including broader wavelength coverage, reduced operator dependence, and enhanced safety profiles for darker skin types. Ultrasound-based systems, including high-intensity focused ultrasound (HIFU) technology, represent another rapidly expanding segment with increasing adoption for non-surgical face and body tightening. Emerging plasma energy-based devices are gaining momentum for innovative skin rejuvenation applications, supported by recent FDA clearances and expanded clinical validation. This technology diversification reflects market maturation, with practitioners increasingly adopting multi-technology approaches to deliver comprehensive aesthetic solutions.

Component Insights

Facial skin resurfacing represents the dominant component segment, benefiting from consistent demand for anti-aging treatments addressing wrinkles, photoaging, and texture irregularities. Laser resurfacing procedures, including ablative and non-ablative fractional laser treatments, remain core offerings in dermatology and aesthetic clinics globally. Fat reduction and body contouring emerge as the fastest-growing component segment, driven by increasing consumer focus on body image, lifestyle modifications, and non-invasive body sculpting alternatives. Cryolipolysis, non-surgical radiofrequency-assisted liposuction, and ultrasound-based fat reduction technologies have expanded treatment accessibility beyond surgical liposuction, attracting broader patient populations.

Hair removal maintains substantial market significance, with laser and intense pulsed light (IPL) systems sustaining high procedure volumes globally. Recent innovations, including FDA-cleared picosecond laser systems and diode laser platforms with enhanced melanin selectivity, have improved safety profiles for diverse skin types. Skin tightening applications, historically dominated by radiofrequency and microneedling devices, are experiencing technology diversification with ultrasound and plasma energy devices offering alternative mechanisms. Photorejuvenation and pigmentation correction components represent high-value segments, particularly in Asian markets where melasma, post-inflammatory hyperpigmentation, and vascular lesions drive sustained demand.

End-user Insights

Dermatology and cosmetic clinics remain the leading end-user segment, accounting for significant market share through their concentration of trained aesthetic practitioners, advanced device adoption, and patient referral networks. Specialized dermatology clinics benefit from practitioner expertise, established reputations, and premium patient demographics supporting higher treatment costs. Hospital and general clinic settings represent substantial end-user segments, particularly in developed markets where aesthetic procedures are increasingly integrated within comprehensive dermatology departments. Medical spas constitute a rapidly growing end-user category, expanding from 8,899 facilities in the United States in 2022 to approximately 10,488 facilities by 2023, reflecting sustained growth momentum in the medical spa industry over the past 15 years.

Medical spas' accessibility advantages, diverse practitioner models, and convenient scheduling appeal to younger, value-conscious consumers seeking routine aesthetic maintenance. The fastest-growing end-user category comprises specialty dermatology clinics, advancing at 13.5% CAGR, driven by healthcare infrastructure upgrades, proliferation of small dermatology businesses, and expanded practitioner availability. India's aesthetic medical practice landscape demonstrates particularly dynamic growth, with rising numbers of specialty dermatology clinics capitalizing on increasing per-capita incomes and growing aesthetic procedure awareness. The fragmentation of end-user settings creates device demand diversification, with manufacturers developing scalable, portable, and cost-tiered systems suitable for clinic sizes ranging from solo practitioner settings to hospital-integrated departments. This end-user diversification generates sustained market expansion across device price ranges and technological sophistication levels.

Regional Insights

North America Aesthetic Medical Devices Market Trends and Insights

North America dominates the global aesthetic medical devices market, maintaining approximately 37% market share in 2025, anchored by mature healthcare infrastructure, high consumer disposable incomes, and well-established aesthetic medicine practices. The region benefits from established regulatory frameworks with the U.S. Food and Drug Administration (FDA) providing clear pathways for device approval, promoting continued innovation and market entry. Digital beauty trends, social media influence, and celebrity culture have normalized cosmetic enhancements across demographic groups, with younger cohorts increasingly adopting preventive and maintenance-focused aesthetic procedures rather than wait-and-see approaches to aging. Blepharoplasty procedures achieved 41.8% incidence increase and 63.9% expenditure growth between 2020-2022, exemplifying sustained demand for facial rejuvenation. Advanced healthcare infrastructure, high concentrations of certified practitioners, and strong consumer awareness ensure North American market resilience and continued technology adoption.

Asia Pacific Aesthetic Medical Devices Market Trends and Insights

Asia Pacific emerges as the fastest-growing global region for aesthetic medical devices, with projected market expansion exceeding 14.1% CAGR through 2035, driven by the convergence of demographic shifts, rising disposable incomes, and cultural beauty consciousness. China maintains dominance as Asia-Pacific's largest market, commanding substantial device demand driven by a 1.4 billion population a rapidly expanding middle class, and cultural emphasis on youthful appearance. Urban centers , including Beijing, Shanghai, and Guangzhou, demonstrate exceptional aesthetic procedure penetration. Japan and South Korea represent mature aesthetic markets with sustained high penetration rates and continued equipment upgrading. Thailand experiences rapid aesthetic tourism growth fueled by advanced clinical infrastructure and competitive pricing, attracting international patients.

Competitive Landscape

The competitive landscape of the aesthetic medical devices market is moderately fragmented yet intense, shaped by technological innovation and strategic consolidation. A handful of well-established players hold significant shares through diversified portfolios spanning energy-based, laser, RF, ultrasound, and body contouring platforms, investing heavily in R&D, global distribution, and regulatory approvals. Mergers, acquisitions, and partnerships are common to strengthen product breadth and geographic reach.

Key Developments:

- In August 2025, South Korea-based HIRONIC, a leading provider of aesthetic medical devices, obtained certification from the Indonesian Ministry of Health (KEMENKES RI) for its flagship product, New Doublo 2.0 a state-of-the-art device that combines 4th-generation High-Intensity Focused Ultrasound (HIFU) and Radiofrequency (RF) technologies in a single treatment platform.

Companies Covered in Aesthetic Medical Devices Market

- Alma Lasers

- Merz Pharma

- Bausch Health Companies Inc.

- Lumenis Be Ltd.

- Venus Concept

- Candela Corporation

- Cutera Inc.

- Fotona

- InMode

- Asclepion Laser Technologies GmbH

- Quanta System

- BTL

- Lutronic

- LASEROPTEK

Frequently Asked Questions

The global aesthetic medical devices market size is expected to be valued at US$ 14.9 billion in 2026.

The aesthetic medical devices market is driven by multiple factors including escalating prevalence of skin disorders affecting 30-70% of global populations, rising aesthetic consciousness influenced by social media and digital beauty trends, aging populations seeking anti-aging and rejuvenation solutions, technological advancements enabling safer procedures with minimal downtime, expanding healthcare infrastructure in emerging markets, and normalization of aesthetic procedures across demographic groups. ISAPS data documenting 38 million aesthetic procedures in 2024 demonstrates sustained consumer demand, with botulinum toxin and hyaluronic acid procedures exceeding 14 million combined annually, indicating robust market fundamentals.

North America dominates the aesthetic medical devices market with approximately 37% market share in 2025, anchored by the United States market valued at US$ 4.68 billion in 2025, supported by mature healthcare infrastructure, high consumer disposable incomes, well-established aesthetic medicine practices, advanced regulatory frameworks with clear FDA approval pathways, and widespread adoption of minimally invasive procedures.

Asia Pacific represents the most compelling market opportunity, with projected expansion exceeding 14.1% CAGR through 2035, driven by China's dominance as largest market with 6.2% growth, India's fastest-growing status with 4.5% CAGR, rising middle-class populations, cultural beauty emphasis, medical tourism expansion, manufacturing cost advantages, and government healthcare initiatives.

Alma Lasers, Merz Pharma, Bausch Health Companies Inc., Lumenis Be Ltd., Venus Concept.