- Medical Devices

- Body & Extremities Aesthetic Procedure Market

Body & Extremities Aesthetic Procedure Market Size, Share, and Growth Forecast, 2026 - 2033

Body & Extremities Aesthetic Procedure Market by Procedure Type (Abdominoplasty, Liposuction, Upper Arm Lift / Arm Lift, Buttock Augmentation, Labiaplasty, Thigh Lift, Penile Enlargement Procedures, Others), Age Group (18–30 Years, 31–45 Years, 46–60 Years, Above 60+ Years), End-User (Hospitals, Specialty Dermatology Clinics, Ambulatory Surgical Centers, Others), and Regional Analysis for 2026 - 2033

Body & Extremities Aesthetic Procedure Market Share and Trends Analysis

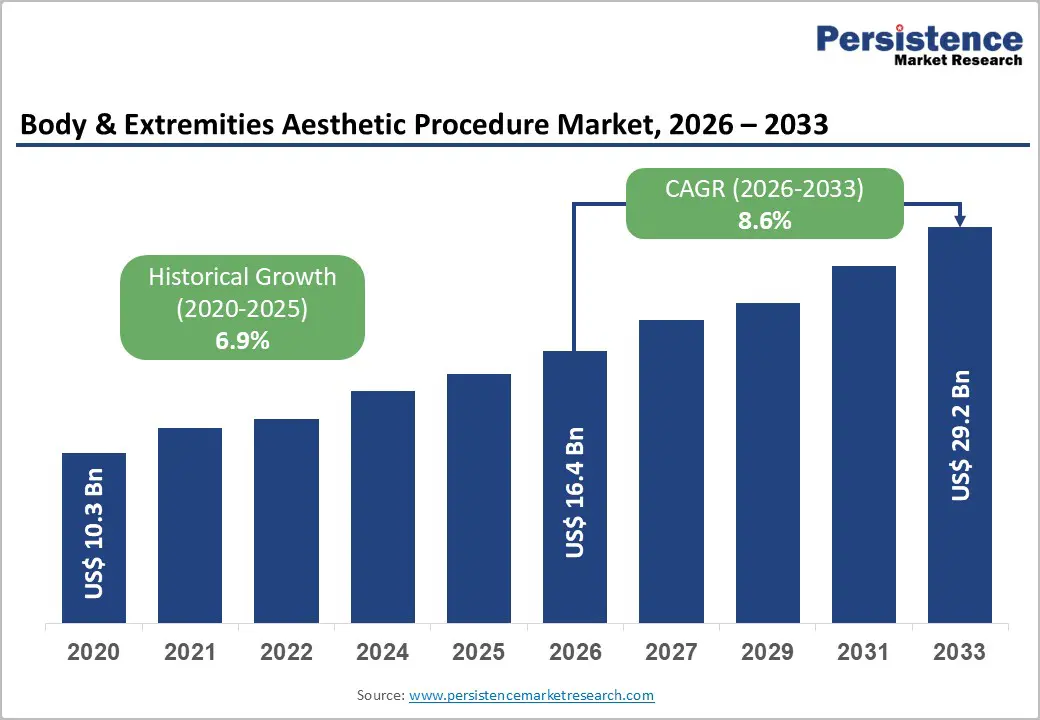

The global body & extremities aesthetic procedure market size is likely to be valued at US$ 16.4 billion in 2026, and is projected to reach US$ 29.2 billion by 2033, growing at a CAGR of 8.6% during the forecast period 2026−2033.

Market growth is driven by rising clinical adoption of body and extremities aesthetic procedures, supported by increasing patient confidence in safety and effectiveness through education on minimally invasive and surgical treatments. Integration of advanced imaging, laser-assisted techniques, and precision-guided surgical tools enhances outcomes and efficiency, attracting more patients. Aging populations, higher urban disposable income, and a focus on preventive and corrective treatments expand the addressable market. Digital platforms facilitate information, consultation, and access to services, while specialized clinics and surgical centers expand treatment availability.

Key Industry Highlights

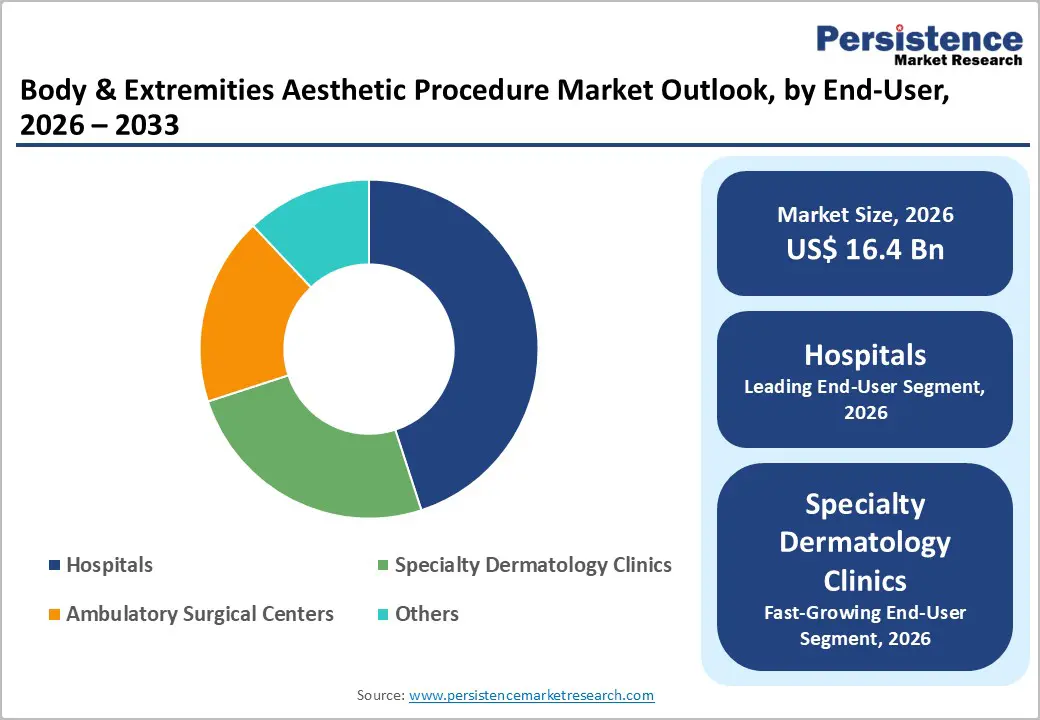

- End-User Dominance: Hospitals are poised to dominate, with around 45% revenue share in 2026, benefiting from integrated clinical expertise and the availability of infrastructure.

- Fastest-Growing End-User: Specialty dermatology clinics are expanding rapidly, driven by procedural specialization, technology adoption, and urban accessibility.

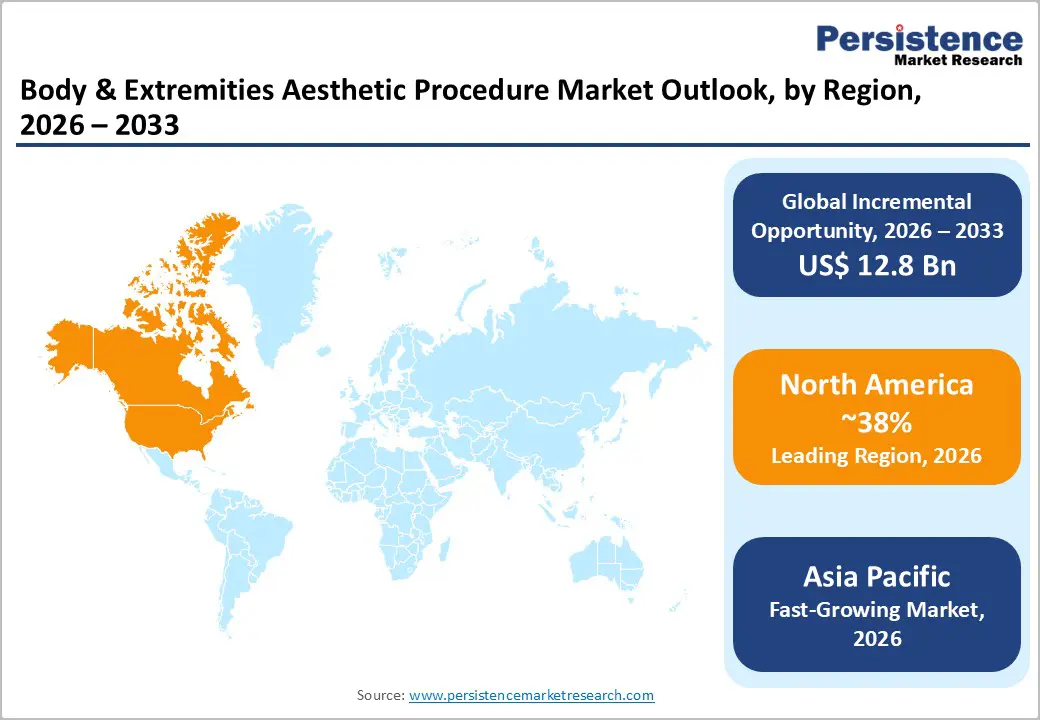

- Regional Leadership: North America is forecast to lead with about 38% market share in 2026, on the back of advanced healthcare infrastructure, while Asia Pacific is set to be the fastest-growing market 2026-2033, driven by rising incomes and digital medical technology adoption.

- Leading Procedure: Liposuction is expected to lead with an estimated 28% revenue share in 2026, driven by clinical acceptance and provider preference.

- Innovation Trends: Adoption of laser-assisted, robotic-guided, and AI-enabled technologies is enhancing procedural precision, reducing recovery time, and supporting service scalability across hospitals and clinics.

| Key Insights | Details |

|---|---|

|

Body & Extremities Aesthetic Procedure Market Size (2026E) |

US$ 16.4 Bn |

|

Market Value Forecast (2033F) |

US$ 29.2 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

8.6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

6.9% |

DRO Analysis

Improving Clinical Awareness and Progressive Acceptance

Clinical awareness and social acceptance continue to strengthen demand for aesthetic interventions across diverse patient groups. Education through certified medical channels improves understanding of procedural safety, expected outcomes, and recovery timelines. Medical professionals actively promote evidence-based treatment pathways, reducing uncertainty and perceived risk. Standardization of training and licensing frameworks enhances trust in providers and clinical settings. Public exposure through digital platforms normalizes treatment adoption and supports informed decision-making. In 2025, around 3–4% of adults in the United States underwent cosmetic procedures, reflecting growing acceptance of such interventions.

Improved communication between clinicians and patients supports personalized treatment planning and realistic expectations. Awareness initiatives highlight minimally invasive options with shorter recovery periods, aligning with modern lifestyle preferences. Regulatory oversight and clinical guidelines reinforce procedural credibility and patient safety standards. Expansion of consultation channels, including virtual platforms, improves access to expert advice and pre-procedure evaluation. Social perception continues to shift toward self-optimization and preventive care, encouraging early adoption of treatments. Healthcare providers emphasize transparency about risks and outcomes, strengthening long-term patient confidence and repeat-procedure rates across clinical settings.

Healthcare Infrastructure Expansion and Technological Integration

Expansion of clinical facilities and service networks improves procedural accessibility and patient throughput. A strong provider base supports higher procedure volumes across urban and emerging regions. Government-backed programs and hospital empanelment strengthen treatment reach. As of April 2025, 31,846 hospitals were empaneled under a national scheme, reflecting rapid capacity expansion and structured access to care. Growth in ambulatory centers and specialty clinics supports elective procedures with shorter turnaround times. Improved infrastructure enables standardized protocols, sterile environments, and multidisciplinary care, which increases procedural adoption across diverse patient segments.

The integration of advanced technologies enhances precision, safety, and clinical outcomes. Imaging systems, laser platforms, and minimally invasive tools support targeted interventions with reduced recovery time. Digital health systems streamline consultation, planning, and follow-up processes. Automation and AI-based diagnostics improve accuracy and workflow efficiency in clinical settings. Providers achieve better resource utilization and reduced procedural variability. Technology-driven differentiation supports premium service positioning and patient trust. Continuous innovation in devices and techniques expands treatment options, aligning with the rising demand for outcome-focused and personalized aesthetic interventions across clinical environments.

Strict Regulatory Requirements and Risk of Complications

Regulatory frameworks impose extensive approval pathways for aesthetic devices and procedures. Compliance requires clinical validation, safety documentation, and continuous monitoring. Approval timelines extend product commercialization cycles. Cost burdens increase for manufacturers and providers. Frequent updates in standards create operational uncertainty. Market entry barriers limit innovation flow and delay the adoption of advanced technologies. Providers face legal exposure under non-compliance scenarios. Licensing and accreditation requirements restrict the expansion of smaller clinics. Cross-border regulatory variation complicates global market strategies. Pricing pressure arises as compliance costs are passed on to end users, reducing overall procedure affordability and market penetration.

Clinical risk remains a critical concern in aesthetic interventions involving the body and extremities. Surgical and minimally invasive procedures carry potential for adverse outcomes such as infection, scarring, or asymmetry. Patient safety expectations remain high in elective treatments. Negative outcomes affect brand reputation and provider credibility. Litigation risk increases financial liability for practitioners and facilities. Variability in practitioner skill influences treatment consistency. Limited standardization across procedures affects outcome predictability. Patient hesitation rises due to perceived safety concerns. Insurance limitations increase patients' financial exposure, restricting the adoption of procedures across broader demographic segments.

Limited Access in Rural Areas and Insurance Coverage Gaps

The restricted availability of aesthetic procedure services in rural regions stems from infrastructure gaps and the uneven distribution of skilled professionals. Advanced equipment and trained specialists remain concentrated in urban centers. Smaller healthcare facilities face capital constraints, limiting investment in aesthetic technologies. Patient awareness remains low due to limited exposure to clinical education and digital engagement. Travel distance and associated costs discourage the adoption of procedures. Service standardization varies across regions, affecting patient trust.

Insurance coverage limitations arise from the classification of aesthetic procedures as elective interventions. Reimbursement frameworks prioritize medically necessary treatments, excluding most cosmetic services. Patients rely on out-of-pocket payments, which increases the financial burden and price sensitivity. High procedure costs reduce affordability for middle-income groups. Payer policies lack standardized inclusion criteria for reconstructive or functional cases. Variability in coverage guidelines creates uncertainty for both providers and patients. Financial risk perception influences treatment decisions and delays adoption. Limited financing options and absence of structured reimbursement pathways constrain procedure volumes and restrict overall market growth potential.

Digital Platforms for Consultation and Education

Digital channels are transforming patient engagement through wider access to information and consultation services. Rapid internet penetration supports this shift. India recorded about 958 million active internet users in 2025, reflecting strong digital reach across urban and rural regions. This scale enables patients to research procedures, compare treatment options, and connect with qualified professionals without geographic constraints. Online education improves understanding of risks, benefits, and expected outcomes. Structured digital content and virtual consultations strengthen decision confidence and reduce information gaps before clinical interaction.

Operational efficiency and service scalability improve through digital integration. Clinics use virtual consultations to streamline patient screening and optimize scheduling. Digital tools support personalized treatment planning through data-driven insights and remote assessment. Marketing strategies shift toward targeted digital outreach, improving patient acquisition and engagement rates. Teleconsultation reduces dependency on physical infrastructure for initial interaction, expanding reach into underserved areas. Continuous communication through digital platforms strengthens follow-up care and long-term engagement.

Growing Deployment of AI and Robotic Technologies

Integration of artificial intelligence (AI) and robotic systems creates measurable clinical value through precision, consistency, and data-driven decision support. Robotic-assisted platforms support controlled movements and reduce variability across procedures. AI-enabled imaging and analytics improve treatment planning and intraoperative guidance. These capabilities strengthen clinical confidence and patient outcomes. A 2025 data brief from a prominent industry platform revealed that 71% of non-federal acute-care hospitals used predictive AI tools by 2024, reflecting rapid institutional adoption and validation of clinical utility. Increased adoption supports scalability across specialized procedures and expands provider acceptance.

Operational efficiency and workflow optimization further strengthen this opportunity. Automated systems reduce procedure time and support resource utilization in high-demand clinical settings. Robotics enables minimally invasive approaches with shorter recovery periods, improving patient throughput. AI systems assist in preoperative assessment and post-procedure monitoring, enhancing continuity of care. Integration with digital platforms supports personalized treatment planning and patient engagement. Healthcare facilities leverage these technologies to differentiate service offerings and attract a broader patient base. Continuous innovation in machine learning and robotic engineering supports long-term capability expansion and aligns with evolving clinical standards.

Category-wise Analysis

Procedure Type Insights

Liposuction is anticipated to secure around 28% of the body & extremities aesthetic procedure market revenue share in 2026, reflecting widespread clinical acceptance and established procedural efficacy. Strong procedural standardization supports consistent outcomes across diverse clinical settings. Demand remains stable across age groups seeking body contouring solutions. Continuous device innovation improves safety profiles and operational efficiency. Shorter recovery timelines encourage higher patient turnover. Integration with complementary procedures enhances treatment value. Provider training programs strengthen procedural expertise. Increasing presence in outpatient facilities expands service reach. Favorable patient testimonials and digital visibility sustain demand growth and reinforce long-term adoption patterns.

Abdominoplasty is expected to be the fastest-growing segment during the 2026–2033 forecast period, propelled by rising demand for post-weight-loss body contouring and reconstructive interventions. Rising focus on physical appearance supports procedure adoption among diverse demographics. Advancements in surgical techniques improve safety and reduce complication rates. Growing medical tourism activity increases procedural volumes in cost-effective regions. Enhanced recovery protocols improve patient experience and satisfaction levels. Integration of digital tools enables better treatment planning and monitoring. Strong referral networks support consistent patient inflow. Increasing availability of skilled professionals strengthens service delivery and scalability across healthcare facilities.

End-User Insights

Hospitals are likely to be the leading segment with a projected 45% of the body & extremities aesthetic procedure market share in 2026 due to integrated clinical expertise, procedural credibility, and infrastructure availability. Multidisciplinary teams enable comprehensive patient evaluation and treatment planning. Availability of intensive care units supports management of complex cases. Standardized clinical protocols ensure consistent safety and outcome quality. Investment capacity enables adoption of advanced surgical technologies. Strong brand reputation strengthens patient trust and referral inflow. Integration with diagnostic services improves procedural efficiency. Higher case volumes support clinician experience and operational optimization across departments, reinforcing sustained segment dominance.

Specialty dermatology clinics are anticipated to be the fastest-growing segment from 2026 to 2033, fueled by procedural specialization, technological adoption, and accessibility in urban and semi-urban areas. Clinics maintain shorter appointment cycles, improving patient throughput and service efficiency. Personalized treatment approaches enhance patient satisfaction and retention. Lower infrastructure costs support competitive pricing strategies. Rapid integration of innovative devices strengthens service differentiation. Expansion through franchise and chain models increases geographic reach. Skilled practitioners focus on targeted procedures, improving outcome consistency. Strong online presence and patient reviews enhance visibility and credibility, supporting sustained growth in competitive markets.

Regional Insights

North America Body & Extremities Aesthetic Procedure Market Trends and Insights

North America is expected to lead with an estimated 38% of the body & extremities aesthetic procedure market value in 2026, supported by advanced clinical infrastructure and high procedural standardization across United States and Canada. Strong presence of board-certified surgeons ensures consistent treatment quality and safety benchmarks. Early integration of laser-assisted and image-guided technologies improves precision and efficiency. High procedure volumes enable operational optimization and cost control across facilities. Favorable reimbursement frameworks for select reconstructive cases support procedural demand. Strong medical device ecosystem accelerates innovation and commercialization cycles. High digital penetration enables informed decision-making and streamlined patient pathways, strengthening procedural uptake across diverse demographic segments.

Sustained dominance is driven by high consumer spending capacity and strong cultural acceptance of aesthetic enhancement in United States and Canada. Structured training programs ensure continuous skill development among practitioners. Integrated care models support seamless coordination across consultation, procedure, and follow-up stages. Strong presence of corporate clinic chains enhances service accessibility and brand visibility. Regulatory clarity supports faster adoption of approved devices and techniques. High investment in marketing and patient education strengthens engagement and awareness. Demand for preventive and corrective treatments remains stable across age groups, supporting consistent revenue generation and high utilization rates across clinical settings.

Europe Body & Extremities Aesthetic Procedure Market Trends and Insights

Europe demonstrates stable growth driven by established healthcare systems and strong clinical governance across Germany, France, and United Kingdom. Standardized treatment protocols and stringent safety regulations enhance procedural credibility and patient confidence. High adoption of minimally invasive technologies supports efficient treatment delivery and shorter recovery timelines. Presence of experienced surgeons and accredited facilities ensures consistent outcome quality. Demand is influenced by aging demographics seeking corrective and maintenance procedures. Integration of digital consultation tools improves patient engagement and preoperative planning. Public and private healthcare coordination supports infrastructure availability and steady procedural volumes.

Growth potential is shaped by increasing preference for outpatient procedures and cost-efficient treatment pathways across Italy and Spain. Expansion of specialized clinics strengthens service accessibility and competitive positioning. Cross-border treatment demand supports procedural inflow driven by pricing variations and service differentiation. Continuous investment in medical devices enhances precision and safety standards. Patient awareness remains high through structured clinical communication and targeted marketing strategies. Training programs and professional certifications maintain practitioner competence. Demand for body contouring and extremity-focused procedures aligns with evolving lifestyle trends and wellness priorities, supporting consistent utilization rates.

Asia Pacific Body & Extremities Aesthetic Procedure Market Trends and Insights

Asia Pacific is forecasted to be the fastest-growing market for body & extremities aesthetic procedure market between 2026 and 2033, stimulated by rapid urban expansion and increasing consumer focus on appearance-driven wellness. Rising middle-income population supports higher discretionary healthcare spending. Digital ecosystems accelerate patient education and consultation access. China and India demonstrate strong procedure demand due to expanding private healthcare networks and improving affordability. Japan and South Korea show high procedural sophistication supported by advanced clinical technologies. Growth in outpatient facilities increases service availability and procedural throughput across urban clusters.

Market acceleration is supported by increasing medical tourism inflows and competitive pricing structures across key countries. Private providers expand capacity through clinic chains and franchise models. Technology adoption remains rapid, with strong uptake of non-invasive and hybrid procedures. Skilled workforce expansion improves service quality and procedural consistency. Regulatory pathways for device approvals remain structured, enabling faster commercialization cycles. Digital marketing strategies enhance patient engagement and conversion rates. Strategic location of clinics in high-density zones improves accessibility and patient flow, strengthening procedural volumes and revenue generation across diverse service providers.

Competitive Landscape

The global body & extremities aesthetic procedure market structure reflects moderate consolidation, with major participants such as Allergan Aesthetics, Cynosure, Hologic, Lumenis, and Sientra securing significant revenue share. Competitive strength is supported by advanced product portfolios, regulatory compliance, and strong clinical validation. Established distribution networks enable wide market reach. Continuous investment in research and development strengthens innovation cycles. Brand positioning and procedural reliability influence provider preference and purchasing decisions.

Competitive intensity increases with participation from Cutera, Venus Concept, and Syneron Medical, alongside regional providers. Market fragmentation persists across developing areas with cost-focused service models. Providers emphasize accessibility and targeted procedure offerings to capture demand. Technology integration and digital engagement platforms support differentiation strategies. Expansion into new geographies and service diversification strengthen competitive positioning across both established and emerging healthcare environments.

Key Industry Developments

- In March 2026, Scotland passed new legislation to tighten regulation of non-surgical cosmetic procedures, banning treatments like Botox and liquid Brazilian butt lifts for under-18s and restricting them to approved medical settings. The law mandates qualified practitioner oversight and introduces safety, hygiene, and licensing standards to address risks from largely unregulated practices.

- In March 2026, Aesthetics International launched a medical-grade abdominoplasty program aimed at addressing chronic back pain by combining cosmetic surgery with functional health benefits.

The initiative positions aesthetic procedures as therapeutic interventions, expanding their role beyond appearance-focused treatments into broader medical applications. - In July 2025, Mumbai’s Cama and Albless Hospital announced plans to launch Maharashtra’s first government-run gyno-cosmetic unit, offering intimate procedures at highly subsidized rates to improve accessibility. The unit will provide both surgical and non-surgical treatments, addressing post-childbirth and aesthetic concerns, with strict medical protocols in place.

Companies Covered in Body & Extremities Aesthetic Procedure Market

- Allergan Aesthetics

- Cynosure

- Hologic

- Lumenis

- Sientra

- Cutera

- Venus Concept

- Syneron Medical

- BTL Industries

- Zimmer MedizinSysteme

- Alma Lasers

- Medtronic

- InMode

- Hugel, Inc.

- REVO Aesthetics

Frequently Asked Questions

The global body & extremities aesthetic procedure market is projected to reach US$ 16.4 billion in 2026.

Rising demand for minimally invasive body contouring, increasing aesthetic awareness, advancing technologies, and expanding disposable income are driving the market.

The market is poised to witness a CAGR of 8.6% from 2026 to 2033.

Growth in non-invasive procedures, integration of advanced technologies, expanding demand for personalized treatments, and rising adoption in emerging markets represent key market opportunities.

Some of the key market players include Allergan Aesthetics, Cynosure, Hologic, Lumenis, and Sientra.