1. Executive Summary

1.1. Global MRI Systems Market Snapshot, 2025 and 2032

1.2. Market Opportunity Assessment, 2025 – 2032, US$ Bn

1.3. Key Market Trends

1.4. Future Market Projections

1.5. Premium Market Insights

1.6. Industry Developments and Key Market Events

1.7. PMR Analysis and Recommendations

2. Market Overview

2.1. Market Scope and Definition

2.2. Market Dynamics

2.2.1. Drivers

2.2.2. Restraints

2.2.3. Opportunity

2.2.4. Key Trends

2.3. Macro-Economic Factors

2.3.1. Global Sectorial Outlook

2.3.2. Global GDP Growth Outlook

2.4. COVID-19 Impact Analysis

2.5. Forecast Factors – Relevance and Impact

3. Value Added Insights

3.1. Strength Adoption Analysis

3.2. Regulatory Landscape

3.3. Value Chain Analysis

3.4. Install Base Scenario

3.5. PESTLE Analysis

3.6. Porter’s Five Force Analysis

4. Price Analysis, 2025A

4.1. Key Highlights

4.2. Key Factors Impacting Strength Prices

4.3. Pricing Analysis, By Strength

4.4. Regional Prices and Strength Preferences

5. Global MRI Systems Market Outlook

5.1. Key Highlights

5.1.1. Market Volume (Units) Projections

5.1.2. Market Size (US$ Bn) and Y-o-Y Growth

5.1.3. Absolute $ Opportunity

5.2. Market Size (US$ Bn) and Volume (Units) Analysis and Forecast

5.2.1. Historical Market Size (US$ Bn) and Volume (Units) Analysis, 2019-2023

5.2.2. Current Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, 2025 – 2032

5.3. Global MRI Systems Market Outlook: Strength

5.3.1. Introduction / Key Findings

5.3.2. Historical Market Size (US$ Bn) and Volume (Units) Analysis, By Strength, 2019 – 2023

5.3.3. Current Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Strength, 2025 – 2032

5.3.3.1. <0.5T

5.3.3.2. 1.5T

5.3.3.3. 3T

5.3.3.4. >3T

5.3.4. Market Attractiveness Analysis: Strength

5.4. Global MRI Systems Market Outlook: Architecture

5.4.1. Introduction / Key Findings

5.4.2. Historical Market Size (US$ Bn), By Architecture, 2019 – 2023

5.4.3. Current Market Size (US$ Bn) Analysis and Forecast, By Architecture, 2025 – 2032

5.4.3.1. Open

5.4.3.2. Closed

5.4.4. Market Attractiveness Analysis: Architecture

5.5. Global MRI Systems Market Outlook: End User

5.5.1. Introduction / Key Findings

5.5.2. Historical Market Size (US$ Bn) Analysis, By End User, 2019 – 2023

5.5.3. Current Market Size (US$ Bn) Analysis and Forecast, By End User, 2025 – 2032

5.5.3.1. Hospitals

5.5.3.2. Ambulatory Surgical Centers

5.5.3.3. Diagnostic Centers

5.5.3.4. Academic and Research Institutes

5.5.3.5. Others

5.5.4. Market Attractiveness Analysis: End User

6. Global MRI Systems Market Outlook: Region

6.1. Key Highlights

6.2. Historical Market Size (US$ Bn) and Volume (Units) Analysis, By Region, 2019 – 2023

6.3. Current Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Region, 2025 – 2032

6.3.1. North America

6.3.2. Europe

6.3.3. East Asia

6.3.4. South Asia and Oceania

6.3.5. Latin America

6.3.6. Middle East and Africa

6.4. Market Attractiveness Analysis: Region

7. North America MRI Systems Market Outlook

7.1. Key Highlights

7.2. Historical Market Size (US$ Bn) Analysis, By Market, 2019 – 2023

7.2.1. By Country

7.2.2. By Strength

7.2.3. By Architecture

7.2.4. By End User

7.3. Current Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 – 2032

7.3.1. U.S.

7.3.2. Canada

7.4. Current Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Strength, 2025 – 2032

7.4.1. <0.5T

7.4.2. 1.5T

7.4.3. 3T

7.4.4. >3T

7.5. Current Market Size (US$ Bn) Analysis and Forecast, By Architecture, 2025 – 2032

7.5.1. Open

7.5.2. Closed

7.6. Current Market Size (US$ Bn) Analysis and Forecast, By End User, 2025 – 2032

7.6.1. Hospitals

7.6.2. Ambulatory Surgical Centers

7.6.3. Diagnostic Centers

7.6.4. Academic and Research Institutes

7.6.5. Others

7.7. Market Attractiveness Analysis

8. Europe MRI Systems Market Outlook

8.1. Key Highlights

8.2. Historical Market Size (US$ Bn) Analysis, By Market, 2019 – 2023

8.2.1. By Country

8.2.2. By Strength

8.2.3. By Architecture

8.2.4. By End User

8.3. Current Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 – 2032

8.3.1. Germany

8.3.2. France

8.3.3. U.K.

8.3.4. Italy

8.3.5. Spain

8.3.6. Russia

8.3.7. Türkiye

8.3.8. Rest of Europe

8.4. Current Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Strength, 2025 – 2032

8.4.1. <0.5T

8.4.2. 1.5T

8.4.3. 3T

8.4.4. >3T

8.5. Current Market Size (US$ Bn) Analysis and Forecast, By Architecture, 2025 – 2032

8.5.1. Open

8.5.2. Closed

8.6. Current Market Size (US$ Bn) Analysis and Forecast, By End User, 2025 – 2032

8.6.1. Hospitals

8.6.2. Ambulatory Surgical Centers

8.6.3. Diagnostic Centers

8.6.4. Academic and Research Institutes

8.6.5. Others

8.7. Market Attractiveness Analysis

9. East Asia MRI Systems Market Outlook

9.1. Key Highlights

9.2. Historical Market Size (US$ Bn) Analysis, By Market, 2019 – 2023

9.2.1. By Country

9.2.2. By Strength

9.2.3. By Architecture

9.2.4. By End User

9.3. Current Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 – 2032

9.3.1. China

9.3.2. Japan

9.3.3. South Korea

9.4. Current Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Strength, 2025 – 2032

9.4.1. <0.5T

9.4.2. 1.5T

9.4.3. 3T

9.4.4. >3T

9.5. Current Market Size (US$ Bn) Analysis and Forecast, By Architecture, 2025 – 2032

9.5.1. Open

9.5.2. Closed

9.6. Current Market Size (US$ Bn) Analysis and Forecast, By End User, 2025 – 2032

9.6.1. Hospitals

9.6.2. Ambulatory Surgical Centers

9.6.3. Diagnostic Centers

9.6.4. Academic and Research Institutes

9.6.5. Others

9.7. Market Attractiveness Analysis

10. South Asia & Oceania MRI Systems Market Outlook

10.1. Key Highlights

10.2. Historical Market Size (US$ Bn) Analysis, By Market, 2019 – 2023

10.2.1. By Country

10.2.2. By Strength

10.2.3. By Architecture

10.2.4. By End User

10.3. Current Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 – 2032

10.3.1. India

10.3.2. Southeast Asia

10.3.3. ANZ

10.3.4. Rest of South Asia & Oceania

10.4. Current Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Strength, 2025 – 2032

10.4.1. <0.5T

10.4.2. 1.5T

10.4.3. 3T

10.4.4. >3T

10.5. Current Market Size (US$ Bn) Analysis and Forecast, By Architecture, 2025 – 2032

10.5.1. Open

10.5.2. Closed

10.6. Current Market Size (US$ Bn) Analysis and Forecast, By End User, 2025 – 2032

10.6.1. Hospitals

10.6.2. Ambulatory Surgical Centers

10.6.3. Diagnostic Centers

10.6.4. Academic and Research Institutes

10.6.5. Others

10.7. Market Attractiveness Analysis

11. Latin America MRI Systems Market Outlook

11.1. Key Highlights

11.2. Historical Market Size (US$ Bn) Analysis, By Market, 2019 – 2023

11.2.1. By Country

11.2.2. By Strength

11.2.3. By Architecture

11.2.4. By End User

11.3. Current Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 – 2032

11.3.1. Brazil

11.3.2. Mexico

11.3.3. Rest of Latin America

11.4. Current Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Strength, 2025 – 2032

11.4.1. <0.5T

11.4.2. 1.5T

11.4.3. 3T

11.4.4. >3T

11.5. Current Market Size (US$ Bn) Analysis and Forecast, By Architecture, 2025 – 2032

11.5.1. Open

11.5.2. Closed

11.6. Current Market Size (US$ Bn) Analysis and Forecast, By End User, 2025 – 2032

11.6.1. Hospitals

11.6.2. Ambulatory Surgical Centers

11.6.3. Diagnostic Centers

11.6.4. Academic and Research Institutes

11.6.5. Others

11.7. Market Attractiveness Analysis

12. Middle East & Africa MRI Systems Market Outlook

12.1. Key Highlights

12.2. Historical Market Size (US$ Bn) Analysis, By Market, 2019 – 2023

12.2.1. By Country

12.2.2. By Strength

12.2.3. By Architecture

12.2.4. By End User

12.3. Current Market Size (US$ Bn) Analysis and Forecast, By Country, 2025 – 2032

12.3.1. GCC Countries

12.3.2. Egypt

12.3.3. South Africa

12.3.4. Northern Africa

12.3.5. Rest of Middle East & Africa

12.4. Current Market Size (US$ Bn) and Volume (Units) Analysis and Forecast, By Strength, 2025 – 2032

12.4.1. <0.5T

12.4.2. 1.5T

12.4.3. 3T

12.4.4. >3T

12.5. Current Market Size (US$ Bn) Analysis and Forecast, By Architecture, 2025 – 2032

12.5.1. Open

12.5.2. Closed

12.6. Current Market Size (US$ Bn) Analysis and Forecast, By End User, 2025 – 2032

12.6.1. Hospitals

12.6.2. Ambulatory Surgical Centers

12.6.3. Diagnostic Centers

12.6.4. Academic and Research Institutes

12.6.5. Others

12.7. Market Attractiveness Analysis

13. Competition Landscape

13.1. Market Share Analysis, 2025

13.2. Market Structure

13.2.1. Competition Intensity Mapping By Market

13.2.2. Competition Dashboard

13.3. Company Profiles (Details – Overview, Financials, Strategy, Recent Developments)

13.3.1. GE HealthCare

13.3.1.1. Overview

13.3.1.2. Segments and Strengths

13.3.1.3. Key Financials

13.3.1.4. Market Developments

13.3.1.5. Market Strategy

13.3.2. Esaote SPA

13.3.3. Siemens Medical Solutions USA, Inc.

13.3.4. FUJIFILM

13.3.5. Naugra Medical Lab

13.3.6. Bruker

13.3.7. Koninklijke Philips N.V.

13.3.8. Magnetica Ltd

13.3.9. CANON MEDICAL SYSTEMS CORPORATION

13.3.10. United Imaging Healthcare Co., Ltd.

13.3.11. SternMed GmbH

13.3.12. Aspect Imaging Ltd.

13.3.13. HYPERFINE, INC.

13.3.14. AMTZ

13.3.15. Meditech Healthcare Systems

13.3.16. Scintica Instrumentation, Inc.

13.3.17. Hitachi, Ltd.

13.3.18. NordicNeuroLab

13.3.19. MR Solutions

13.3.20. Shimadzu Corporation

13.3.21. MinFound Medical Systems Co., Ltd

13.3.22. Neusoft Medical Systems Co., Ltd.

13.3.23. FONAR Corp.

13.3.24. ASG Superconductors spa

13.3.25. Synaptive Medical

14. Appendix

14.1. Research Methodology

14.2. Research Assumptions

14.3. Acronyms and Abbreviations

- Medical Devices

- MRI Systems Market

MRI Systems Market Size, Share, and Growth Forecast from 2025 - 2032

MRI Systems Market by Strength (<0.5T, 1.5T, 3T, >3T), Architecture (Open, Closed), End User (Hospitals, Ambulatory Surgical Centers, Diagnostic Centers, Academic and Research Institutes), and Regional Analysis from 2025 to 2032

MRI Systems Market Size and Share Analysis

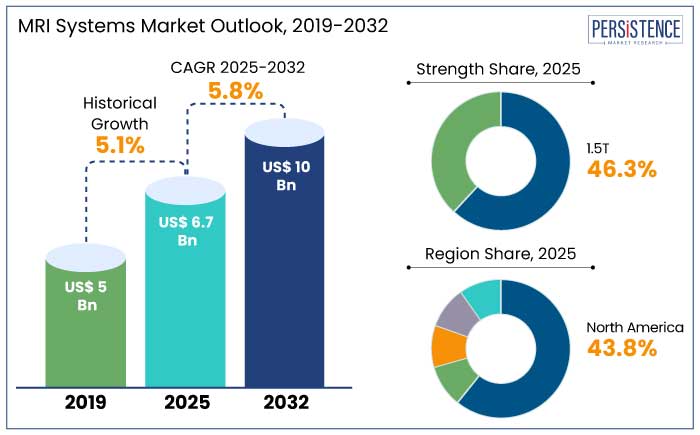

The global MRI systems market is predicted to reach a size of US$ 6.7 Bn by 2025. It is anticipated to showcase a CAGR of 5.8% during the forecast period to attain a value of US$ 10 Bn by 2032.

AI integration in MRI systems enables real-time image analysis, improves accuracy, and minimizes diagnostic times. AI-based MRI systems are estimated to reduce scan times by 50%, enhancing patient throughput.

Development of lightweight and portable MRI systems is a growing trend, especially for point-of-care diagnostics in rural and remote areas. Silent MRI systems, which reduce acoustic noise during scanning, are gaining traction to improve patient comfort and compliance. Prominent players like GE Healthcare and Siemens Healthineers have launched systems with noise levels as low as 77 dB compared to traditional levels of 110 to 120 dB.

Key Highlights of the Industry

- Hybrid MRI systems that combine MRI with other modalities are witnessing increased adoption for their ability to provide comprehensive diagnostic information.

- Introduction of ultra-high field 7T MRI systems are driving developments in research and clinical diagnostics, especially in neurology and musculoskeletal imaging.

- Rising integration of digital technologies in MRI systems for enhanced imaging and faster diagnostics.

- Increased prevalence of cancer, neurological disorders, and cardiovascular diseases is accelerating demand.

- Growing elderly population worldwide leads to higher requirement for diagnostic imaging.

- FDA approved 7T MRI systems for clinical use in 2017 and their adoption is predicted to grow significantly during the forecast period.

- Based on strength, the 1.5T segment is likely to hold a share of 46.3% in 2025 as these provide high quality images.

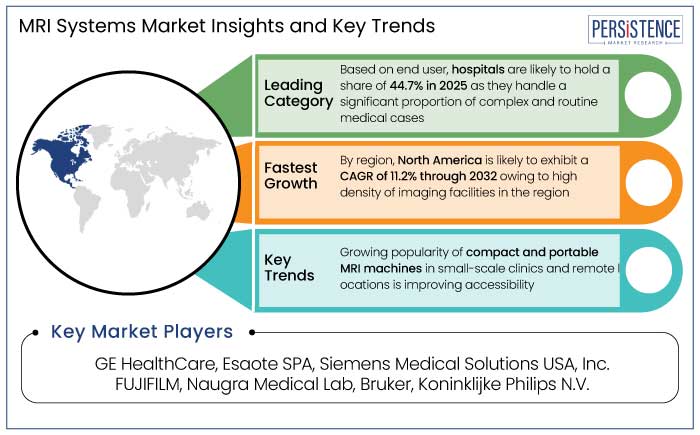

- In terms of end user, the hospitals segment is predicted to hold a share of 44.7% in 2025 as these handle a significant proportion of complex medical cases.

- MRI systems market in North America is set to exhibit a CAGR of 11.2% through 2032 owing to high density of imaging facilities.

|

Market Attributes |

Key Insights |

|

MRI Systems Market Size (2025E) |

US$ 6.7 Bn |

|

Projected Market Value (2032F) |

US$ 10 Bn |

|

Global Market Growth Rate (CAGR 2025 to 2032) |

5.8% |

|

Historical Market Growth Rate (CAGR 2019 to 2023) |

5.1% |

Leading Manufacturers in North America are Propelling Technological Developments

North America MRI systems market is estimated to hold a share of 43.8% in 2025. The region has one of the most developed healthcare systems across the globe with a strong focus on diagnostic imaging.

- North America boasts a high density of imaging facilities, with over 12,000 MRI scanners installed in the U.S. alone as of 2023.

Increasing burden of chronic diseases in the region is propelling the demand for MRI systems. Over 6 million Americans live with Alzheimer’s disease, necessitating advanced imaging solutions like MRI for early detection.

- According to the American Cancer Society, an estimated 1.9 Mn new cancer cases are diagnosed in the U.S. in 2023.

The region is home to leading MRI system manufacturers, including GE Healthcare, Siemens Healthineers, and Philips, which are heavily investing in technological advancements. These companies are at the forefront of developing cutting-edge technologies like AI-enhanced imaging and 7T MRI systems.

1.5T is Mainly Preferred Owing to its High Affordability

1.5T is anticipated to hold a share of 46.3% in 2025. MRI systems with this strength are versatile and well-suited for imaging various clinical conditions, including neurological, musculoskeletal, cardiac, and abdominal disorders.

1.5T MRI systems provide high-quality images with adequate signal-to-noise ratios (SNR), making them ideal for general diagnostic imaging. Lower purchase and operational costs make 1.5T systems the preferred choice for smaller hospitals, outpatient centers, and developing healthcare markets.

- The average cost of a new 1.5T MRI system ranges between US$ 1 million and US$ 1.5 million, compared to US$ 2 million to US$ 3 million for a 3T system.

These MRI systems cater to a majority of imaging needs in the healthcare settings. They offer excellent performance without the added challenges of 3T systems, like heating issues or susceptibility to artifacts.

- According to a 2023 study, 1.5T systems account for 70% of global MRI installations, reflecting their widespread acceptance.

Hospitals are Better Positioned to Invest in Expensive MRI Systems

Hospitals are anticipated to hold a share of 44.7% in 2025. Hospitals handle a significant proportion of complex and routine medical cases, making them the largest consumers of diagnostic imaging technologies like MRI.

- According to a 2023 report by the Radiological Society of North America (RSNA), hospitals accounted for over 65% of all MRI procedures globally.

Increasing prevalence of chronic diseases like cancer, neurological disorders, and cardiovascular conditions has further driven MRI demand in hospitals.

- Neurological MRI scans grew by 8% annually from 2019 to 2023 owing to rising cases of strokes and Alzheimer's disease.

- Hospitals in North America and Europe purchase more than 70% of high-strength MRI systems (3T) owing to their ability to support advanced imaging needs.

Hospitals are often better positioned to invest in expensive MRI systems owing to their access to funding through government support, grants, or private investments. For instance,

- Hospitals in the U.S. received US$ 200 billion in federal funding in 2023 under the CARES Act, part of which was allocated to upgrading diagnostic imaging equipment, including MRI systems.

Market Introduction and Trend Analysis

Potential growth in the global MRI systems industry is predicted to be driven by increased demand for advanced imaging technologies. AI-driven imaging systems are estimated to enhance diagnostic accuracy and decrease operational costs. For example,

- A study revealed that 75% of new MRI systems predicted to incorporate AI features by 2032.

Emerging economies are anticipated to witness double-digit growth in MRI installations owing to improving healthcare access and government investments. Compact MRI systems are projected to witness rapid adoption, particularly in rural and underserved areas, with portable MRI segment projecting substantial growth.

Historical Growth and Course Ahead

The MRI systems market growth was steady at a CAGR of 5.1% during the historical period. Growth during this period was driven by increasing adoption of high-strength MRI systems, technological innovations, and expanded healthcare infrastructure in emerging economies.

Introduction of portable and compact MRI machines expanded the market, especially in remote areas with limited healthcare access. Advancements in functional MRI (fMRI) enabled better diagnosis of neurological disorders, fueling demand.

Demand in the forecast period is likely to be driven by advancements in imaging technologies and an increasing demand for non-invasive diagnostic tools. The period is likely to witness increased adoption of 3T and 7T MRI systems as they offer superior image quality and detailed diagnostics.

Market Growth Drivers

Emergence of Customization and Modular MRI Systems

Modular MRI systems enable healthcare facilities to focus on specific diagnostic areas instead of investing in general-purpose MRI machines. For instance, orthopedic-focused MRI systems are gaining popularity owing to their lower cost and specialized imaging capabilities. Custom-built MRI systems assist in decreasing initial capital investment by avoiding unnecessary features. This flexibility is particularly appealing to small to medium-sized clinics.

- Cost-efficient diagnostic solutions are predicted to contribute to 40% of modular MRI purchases by 2032.

Modular systems provide a scalable approach, enabling facilities to upgrade components such as coils or software without replacing the entire system. This reduces downtime and extends the system's lifecycle.

- A survey by healthcare equipment vendors showed that 65% of healthcare providers prefer scalable systems, citing operational continuity and long-term cost savings.

Rising Demand for Portable and Point-of-care MRI Systems

Portable MRI systems enable diagnostic imaging in remote or underserved areas with limited access to healthcare infrastructure.

- According to the World Health Organization (WHO), 45% of the global population lacks access to basic diagnostic imaging. Portable systems aim to bridge this gap.

Point-of-Care MRI systems provide immediate imaging in emergency departments and intensive care units (ICUs). This enhances diagnostic accuracy and patient outcomes during critical situations. For instance,

- The BrainScope portable MRI system, widely used in trauma centers, has reduced diagnostic time for head injuries by 40%, according to clinical trials.

Mobile imaging solutions equipped with portable MRU systems are being deployed for onsite diagnostics in rural clinics and industrial settings. These systems are designed to be compact and lightweight, making them easy to transport and set up in various locations. For instance,

- The Hyperfine Swoop Portable MRI, weighing just 1,400 pounds, can be transported to different rooms or locations, expanding its usability in diverse clinical environments.

Market Restraining Factors

Risk of Claustrophobia and Noise Levels

Enclosed designs of conventional MRI systems can induce claustrophobia, anxiety, and panic in patients. For instance,

- A study published by The British Journal of Radiology revealed that 10% to 15% of patients experience severe claustrophobia during an MRI scan.

- Claustrophobia-related issues account for 1.2% to 10.5% of incomplete scans annually, depending on the population and healthcare setting.

- Studies reveal that 25% of patients report moderate anxiety when undergoing a traditional closed MRI scan.

MRI scanners generate loud noises owing to their rapid magnetic field changes and gradient coil vibrations. These sounds can reach an uncomfortable level at some point. Extended exposure to such high noise levels can pose risks, especially for children.

- Noise generated by an MRI machine can range from 80 to 130 decibels (dB), comparable to the sound of a jackhammer or a low-flying jet.

- Research shows that 35% of patients report noise-related discomfort during MRI scans.

Market Growth Opportunities

Increasing Utilization in Neurological and Musculoskeletal Imaging

Rising prevalence of neurological disorders is propelling demand for MRI systems. For example,

- According to the World Stroke Organization, approximately 12.2 million new stroke cases are reported globally each year, with MRI being the gold standard for early detection and treatment planning.

Musculoskeletal disorders are the leading cause of disability worldwide. These conditions are often diagnosed and managed using MRI.

- A study by the American Academy of Orthopaedic Surgeons found that MRI use in sports medicine increased by 35% from 2018 to 2023.

MRI systems offer a non-invasive and radiation-free alternative for detailed imaging of the brain, spinal cord, joints, and soft tissues. This is especially crucial for neurological patients where avoiding radiation exposure is critical for long-term monitoring.

Rising Adoption of AI and ML Integration

AI-driven MRI systems significantly decrease scan times, addressing one of the primary challenges in MRI procedures. Studies showcase that AI algorithms can cut MRI scan times by 50%, making the process more patient-friendly and cost-effective. For instance,

- Siemens Healthineers' AI-based software, Deep Resolve, accelerates image reconstruction while maintaining high-quality output.

AI and ML enhance the sensitivity and specificity of MRI interpretation by identifying subtle patterns and anomalies that may be missed by radiologists.

- A research study published in the Journal of the American Medical Association (JAMA) in 2022 found that AI-assisted MRI systems improved diagnostic accuracy for neurological conditions like brain tumors by 30% compared to traditional methods.

AI-powered solutions streamline workflows by automating repetitive tasks such as image segmentation, lesion detection, and volumetric measurements.

- A 2023 study revealed that radiology departments using AI-enabled MRI systems experienced a 20% to 25% increase in efficiency, enabling radiologists to focus on complex cases.

Competitive Landscape for the MRI Systems Market

Companies in the MRI systems market are developing innovative MRI technologies with better imaging capabilities, faster scan times, and improved patient comfort. Siemens Healthineers invested heavily in developing novel 3T MRI systems like the Magnetom Lumina, which integrates AI and accelerates scan times.

Businesses are adopting AI to improve diagnostic accuracy, automate workflows, and decrease scan times. Philips Healthcare launched its AI-powered ‘SmartSpeed’ technology for faster MRI scans.

Manufacturers are developing patient centric solutions to address concerns regarding patient comfort and enhance satisfaction. Companies like Hitachi and GE Healthcare offer open-bore and wide-bore MRI systems to reduce patient anxiety.

Recent Industry Developments

- In April 2024, the University of Nottingham announced the final selection of suppliers to design and build the UK’s most powerful magnetic resonance imaging (MRI) scanner. Tesla Engineering Ltd and Philips UK and Ireland have been selected to construct the elements of the ultra-high field MRI scanner.

- In May 2024, Chennai-headquartered Fischer Medical Ventures (FMVL) domestically manufactured MRI systems in the Andhra Pradesh MedTech Zone (AMTZ) in Visakhapatnam.

- In November 2023, FONAR Corporation entered into an exclusive distributionship of SwiftMR™ from AIRS Medical, Inc. SwiftMR™ is an FDA 510(k) approved software which uses AI-powered denoising and sharpening to enhance MRI images quality and reduce MRI scan times by up to 50%.

- In August 2023, Voxelgrids Innovations Pvt Ltd launched Indigenously developed Ultrafast, High Field (1.5 Tesla), Next Generation Magnetic Resonance Imaging (MRI) Scanner in New Delhi, India

- In April 2023, Siemens Healthineers inaugurated MRI machine manufacturing facility in Bengaluru approved under the Radiology and Imaging Medical Devices segment of the Production Linked Incentive (PLI) Scheme by the Government of India (GoI) and the Department of Pharmaceuticals (DoP).

- In February 2023, Swoop® Portable MR Imaging® System from Hyperfine, Inc. received CE approval under the comprehensive New EU MDR Regulations. The Swoop® system is the world's first FDA-cleared portable MRI system.

Companies Covered in MRI Systems Market

- GE HealthCare

- Esaote SPA

- Siemens Medical Solutions USA, Inc.

- FUJIFILM

- Naugra Medical Lab

- Bruker

- Koninklijke Philips N.V.

- Magnetica Ltd

- CANON MEDICAL SYSTEMS CORPORATION

- United Imaging Healthcare Co., Ltd.

- SternMed GmbH

- Aspect Imaging Ltd.

- HYPERFINE, INC.

- AMTZ

- Meditech Healthcare Systems

- Scintica Instrumentation, Inc.

- Hitachi, Ltd.

- NordicNeuroLab

- MR Solutions

- Shimadzu Corporation

- MinFound Medical Systems Co., Ltd

- Neusoft Medical Systems Co., Ltd.

- FONAR Corp.

- ASG Superconductors spa

- Synaptive Medical

Frequently Asked Questions

The market is anticipated to reach a value of US$ 10 Bn by 2032.

Open and close are the two main types.

North America is anticipated to emerge as the leading region with a share of 43.8% in 2025.

Prominent players in the market include GE HealthCare, Esaote SPA, and Siemens Medical Solutions USA, Inc.

The market is predicted to witness a CAGR of 5.8% throughout the forecast period.