- Medical Devices

- MRI Guided Focused Ultrasound Devices Market

MRI Guided Focused Ultrasound Devices Market Size, Trends, Share, Growth, and Regional Forecast, 2025 - 2032

MRI Guided Focused Ultrasound Devices Market by Product Type (Magnetic Resonance Guided, Ultrasound Guided, Magnetic Resonance & Ultrasound Guided), Indication (Uterine Fibroids, Prostate Diseases, Liver Cancer, Glaucoma, Bone metastases, Breast Cancer, Brain, Others), Distribution Channel, and Regional Analysis from 2025 - 2032

MRI Guided Focused Ultrasound Devices Market Share and Trends Analysis

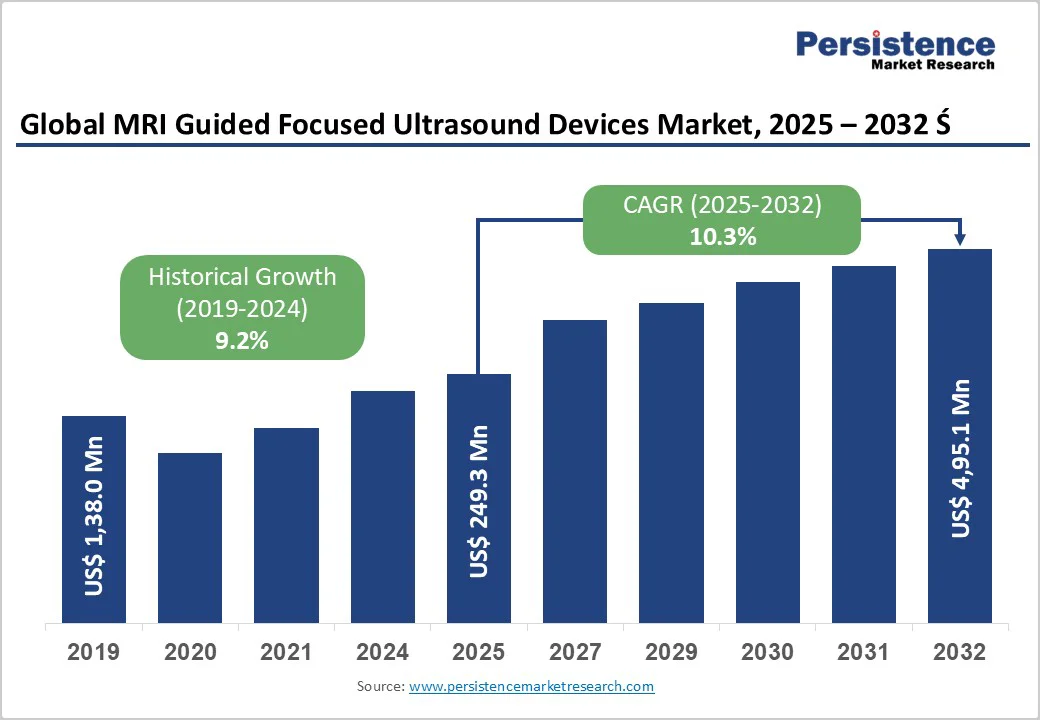

The global MRI guided focused ultrasound devices market size is likely to grow from US$ 249.3 Mn in 2025 and is projected to reach US$ 495.1 Mn by 2032, growing at a CAGR of 10.3% during the forecast period from 2025 to 2032. The global MRI guided focused ultrasound devices market is expanding steadily, driven by rising demand for non-invasive therapies, technological advancements in imaging precision, and growing applications in neurology, oncology, and women’s health. North America dominates with established infrastructure, while Asia Pacific emerges fastest, supported by healthcare investments, clinical trials, and wider therapy acceptance.

Key Industry Highlights

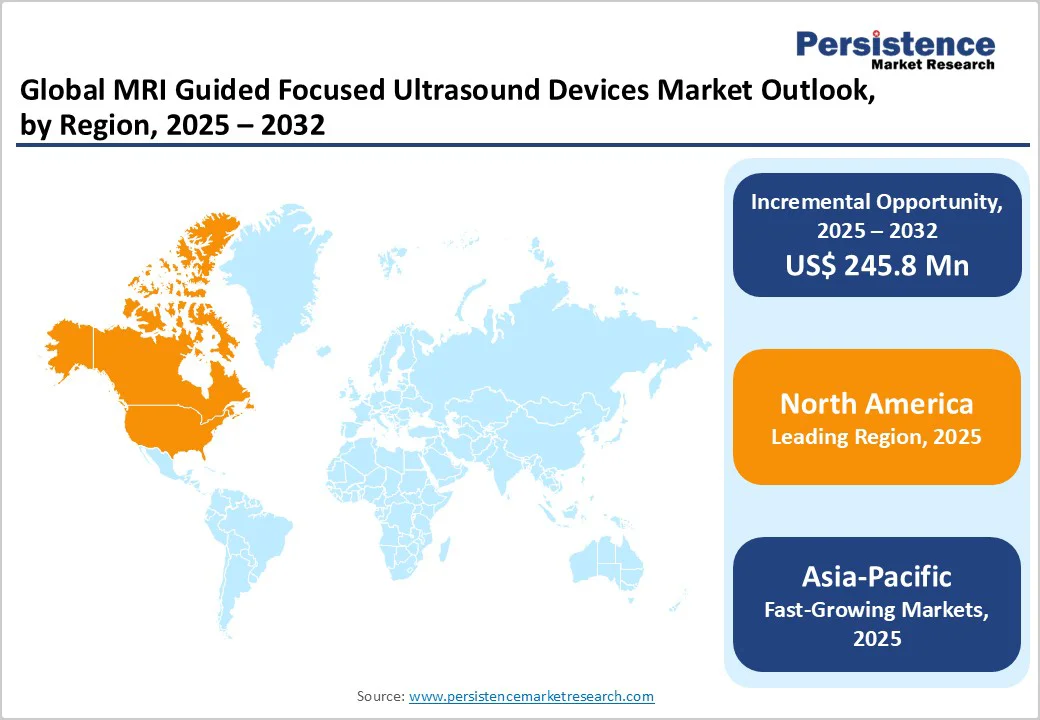

- Leading Region: North America, holding nearly 39.2% market share in 2025, driven by advanced MRI infrastructure, strong clinical adoption for neurological and oncological procedures, and favorable reimbursement for non-invasive therapies.

- Fastest-Growing Region: Asia Pacific, fueled by expanding healthcare investments, growing availability of MRI facilities, and rising demand for safer, incision-free treatment alternatives across China, Japan, and India.

- Investment Plans: Europe, focusing on cross-border clinical research collaborations, wider adoption of MR-guided systems in neurology and oncology centers, and supportive regulatory pathways for innovative focused ultrasound applications.

- Dominant Product: Magnetic Resonance Guided systems, capturing nearly 53.4% market share, owing to superior imaging precision, real-time thermometry, and growing use in brain and uterine fibroid treatments.

| Key Insights | Details |

|---|---|

|

MRI Guided Focused Ultrasound Devices Market Size (2025E) |

US$ 249.3 Mn |

|

Market Value Forecast (2032F) |

US$ 495.1Mn |

|

Projected Growth (CAGR 2025 to 2032) |

10.3% |

|

Historical Market Growth (CAGR 2019 to 2024) |

9.2% |

Market Dynamics

Driver - Rising Demand for Non-Invasive Treatments

The rising demand for non-invasive treatments is a clear driver in the MRI-guided focused ultrasound devices market. For example, a 2024 review described how high-intensity focused ultrasound (HIFU) enables targeted ablation of tissue guided by MRI or ultrasound without incisions or destruction of surrounding tissue.

The National Institute of Biomedical Imaging and Bioengineering (NIBIB) reports the development of wireless, wearable ultrasound patches for continuous non-invasive monitoring of chronic illness, signaling broader acceptance of non-invasive modalities. Together, these facts show that both clinicians and healthcare systems are shifting toward image-guided, non-invasive therapies for faster recovery, fewer complications, and broader use beyond traditional surgery, which underpins growing adoption of MRI-guided focused ultrasound devices.

Restraints - Complex System Integration and Workflow Challenges

In the MRI guided focused ultrasound devices market, one of the major restraints is complex system integration and workflow challenges. A peer-reviewed study found that when activating a focused-ultrasound transducer inside a 1.5 T MRI scanner, the signal-to-noise ratio (SNR) dropped significantly, requiring isolation of electronics and vibration mitigation to restore image quality by more than 3-fold. Likewise, during implementation of an MR-HIFU (MRI-guided High-Intensity Focused Ultrasound) program for uterine fibroids, a center identified a “learning-curve” of 25 treatments and noted that lacking SOPs, multidisciplinary workflows, and reimbursement pathways delayed full rollout. These findings highlight that the integration of high-field MRI, ultrasound transducers, patient-coupling systems, and real-time thermometry imposes operational hurdles such as long installation times, specialized training, interdisciplinary coordination, and workflow redesign, which slow broader adoption and raise cost and staffing barriers.

Opportunity - Integration with Artificial Intelligence and Image Analytics

Integration of artificial intelligence (AI) and image analytics presents a strong opportunity for MRI-guided focused ultrasound by improving target delineation, automating treatment planning, and enabling adaptive control during therapy. Regulatory data show rapid uptake of AI in medical devices about 950 AI/ML-enabled devices are authorized for clinical use in the U.S. as of mid-2024, with imaging tools representing the largest share, indicating the maturity of clinical imaging AI. AI methods have repeatedly improved diagnostic and segmentation accuracy in MRI and other modalities, supporting patient-specific plans and faster workflows.

Early feasibility work in focused-ultrasound imaging reported automated detection of ablated regions with ~93% accuracy, demonstrating practical gains for intra-procedural monitoring. Collectively, these trends suggest that embedding validated AI into MRgFUS systems can shorten procedure times, reduce operator variability, and expand candidacy by improving safety margins, making AI integration a high-impact growth vector for device manufacturers and care providers.

Category-wise Analysis

By Product Type, Magnetic Resonance Guided dominates the MRI Guided Focused Ultrasound Devices Market

The magnetic resonance guided dominates the market with 53.4% share in 2025, because MRI offers real-time thermometry and high soft-tissue contrast that enable precise, image-verified ablation with fewer complications than blind or ultrasound-only guidance. MR thermometry (proton-resonance-frequency shift methods) provides sensitive, real-time temperature maps critical for safe HIFU dosing. Regulatory adoption has followed clinical evidence: the first FDA approval for MR-guided focused ultrasound in the brain (essential tremor) was granted in 2016, validating MR-based workflows and driving hospital uptake. Systematic reviews and program reports (e.g., 29 studies/617 patients for essential tremor) demonstrate consistent efficacy and acceptable safety, which encourages investment in MR-integrated platforms over standalone ultrasound devices.

By Indication, Uterine Fibroids dominate the MRI Guided Focused Ultrasound Devices Market

The indication of MRI guided focused ultrasound (MRgFUS) for Uterine Fibroids dominates due to its early regulatory approval and strong clinical evidence in this area. The U.S. Food and Drug Administration approved the therapy specifically for uterine fibroids in 2009, making it one of the first non-invasive MRgFUS applications. Clinical studies report significant fibroid shrinkage; one Indian study noted a mean 30 % ± 11 % volume reduction at six months for 50 women. Seven-year follow-up data show only 33 % of patients needed further intervention, supporting durability. Because of this depth of clinical adoption and mature indication, uterine fibroids has become the largest share within the MRgFUS devices market.

Regional Insights

North America MRI Guided Focused Ultrasound Devices Market Trends

Europe is a dominant accounting for a 39.2% share in 2025, due to its dense MRI infrastructure, strong regulatory adoption, and deep healthcare spending, enabling faster clinical uptake. The United States has among the highest MRI units per million people, supporting device integration and procedural volume. The FDA’s premarket approval for MR-guided focused ultrasound in essential tremor catalyzed hospital investment and specialist training. Medicare/CMS coding and local coverage guidance (Category III/CPT tracking and LCDs) created billing pathways that reduce financial barriers for providers. Moreover, U.S. healthcare spending about $4.8 trillion in 2023 gives hospitals greater capital capacity to acquire high-cost MRgFUS systems and support multidisciplinary programs, reinforcing North American dominance. Academic centers and research funding further accelerate adoption and clinical evidence.

Asia Pacific MRI Guided Focused Ultrasound Devices Market Trends

Asia Pacific is emerging as the fastest-growing market for MRI-guided focused ultrasound devices due to major investments in healthcare modernization and a sharp rise in non-invasive treatment adoption. Countries like China, Japan, and India are expanding MRI access. China alone has installed over 20,000 MRI scanners as of 2023, according to the National Health Commission of China. Japan maintains one of the world’s highest MRI densities, with over 55 units per million populations as per the OECD. Additionally, regional governments are prioritizing local production and technology transfer for precision medicine and image-guided therapies. Growing awareness of uterine fibroid and prostate disease treatment options through non-surgical means further supports adoption, making the Asia Pacific a key growth hub.

Europe MRI Guided Focused Ultrasound Devices Market Trends

Europe plays a crucial role in the MRI-guided focused ultrasound devices market due to its robust infrastructure, strong regulatory harmonization, and growing adoption of digital health frameworks. For instance, some European countries, such as Germany, report 35.3 MRI units per million population among the highest globally. The continent’s unified regulatory ecosystem is reflected by the recently adopted European Health Data Space (EHDS), which enables cross-border access to interoperable health records and supports innovative therapies and device data reuse. Moreover, countries like Germany have granted reimbursement status for MR-guided focused ultrasound in movement disorders, boosting clinical access. Together, these factors position Europe as a strategic market for focused ultrasound device manufacturers and care networks.

Competitive Landscape

The global MRI guided focused ultrasound devices market is expanding as hospitals adopt non-invasive, image-guided therapies for cancer, neurological, and gynecological conditions. Leading manufacturers emphasize precision imaging, improved targeting accuracy, and real-time thermal monitoring. Rising prevalence of uterine fibroids, brain disorders, and prostate diseases, coupled with advanced MRI infrastructure, continues to drive global growth.

Key Industry Developments:

- In July 2025, Insightec announced that it had received approval from the U.S. Food and Drug Administration (FDA) for its staged bilateral focused ultrasound treatment for patients with Parkinson’s disease. The approval allowed treatment on both sides of the brain in two separate sessions, enabling improved symptom control and patient safety.

- In April 2025, The U.S. Food and Drug Administration (FDA) granted Breakthrough Device designation to a Korean-developed Focused Ultrasound (FUS) system designed for non-invasive brain treatments. The recognition aimed to expedite the review and development of this innovative technology, which uses MRI guidance to deliver precise ultrasound energy for neurological disorders.

- In December 2024, Profound Medical and Siemens Healthineers announced a collaboration to provide a comprehensive MRI-guided solution for prostate therapy. The partnership combined Profound Medical’s TULSA-PRO® system with Siemens Healthineers’ advanced MRI technology, offering a fully integrated approach to minimally invasive prostate treatment.

Companies Covered in MRI Guided Focused Ultrasound Devices Market

- Profound Medical

- Insightech

- EpiSonica

- Kona Medical

- Mirabilis Medical

- SonaCare Medical

- Beijing Yuande Bio-Medical Engineering

- Chongquing HIFU Medical Tech. Co. Ltd.

- Shanghai A&S Science Technology Development Co., Ltd.

- FUS Instruments Inc.

- Others

Frequently Asked Questions

The global MRI guided focused ultrasound devices market is projected to be valued at US$ 249.3 Mn in 2025.

Rising demand for non-invasive therapies, precision imaging advances, cancer treatment expansion, and increased adoption in neurology and gynecology drive growth.

The global MRI guided focused ultrasound devices market is poised to witness a CAGR of 10.3% between 2025 and 2032.

Integration with AI imaging, expanding oncology applications, government support for non-invasive care, and increased MRI infrastructure create strong opportunities.

Profound Medical, Insightec, EpiSonica, Kona Medical, Mirabilis Medical, SonaCare Medical, and Others.