- Medical Devices

- MRI Monitoring Devices Market

MRI Monitoring Devices Market Size, Share, and Growth Forecast, 2025 - 2032

MRI Monitoring Devices Market by Product Type (Basic MRI Monitoring Devices, Advanced MRI Monitoring Devices), End-user (Hospitals, Ambulatory Surgical Centres, Diagnostics Centres, Emergency Medical Services, Others), and Regional Analysis for 2025 - 2032

MRI Monitoring Devices Market Size and Trends Analysis

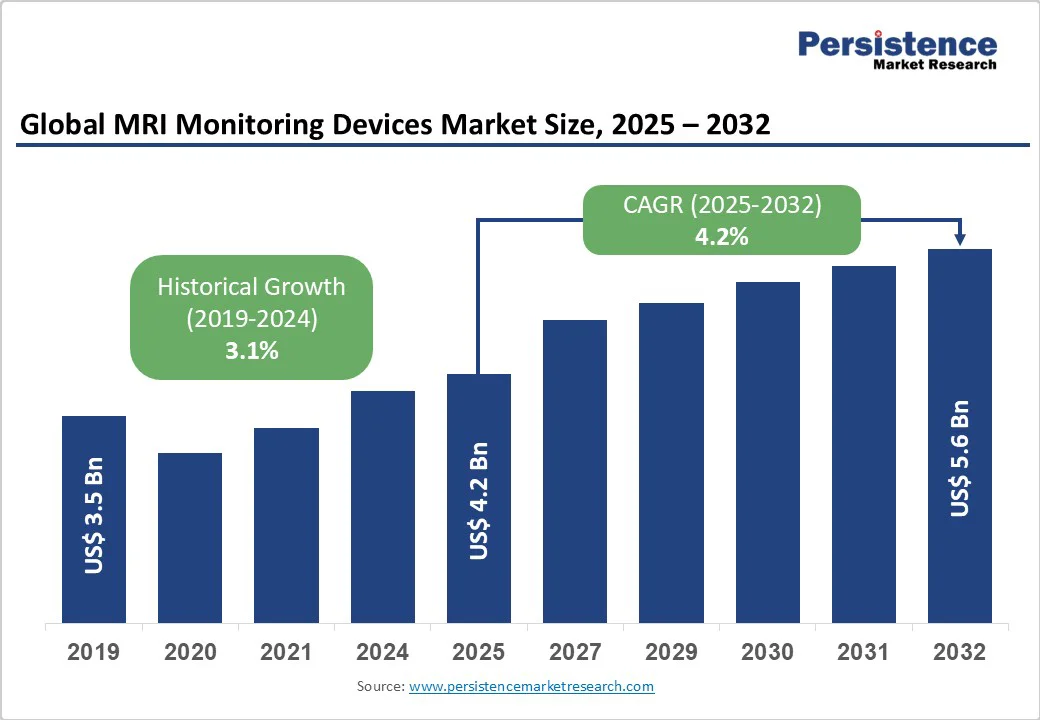

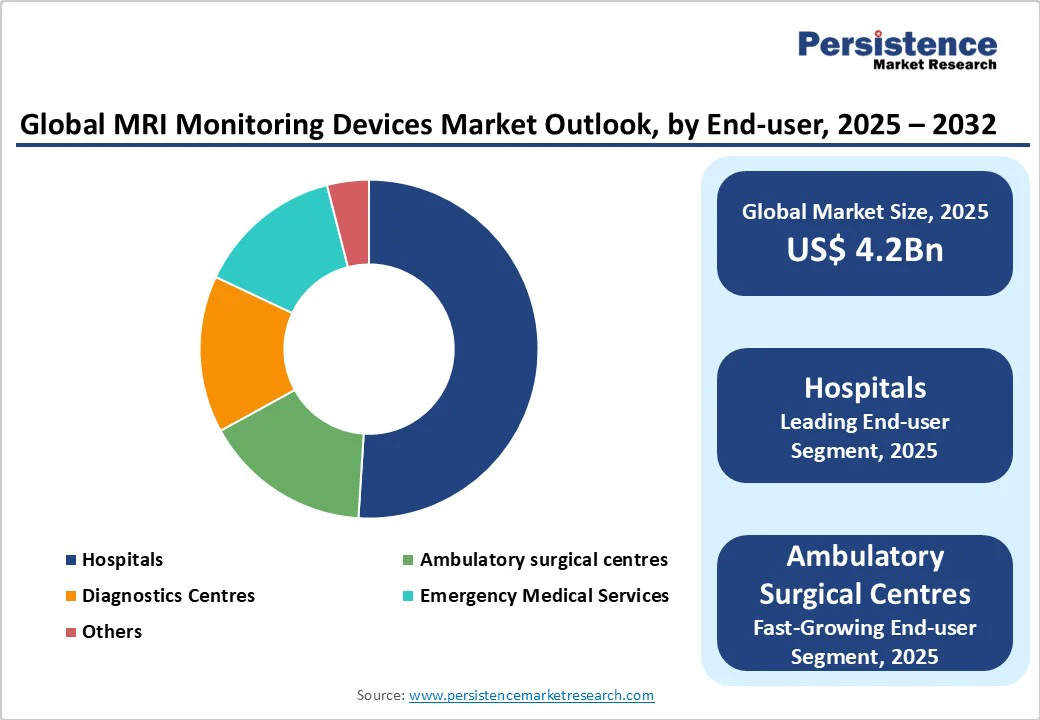

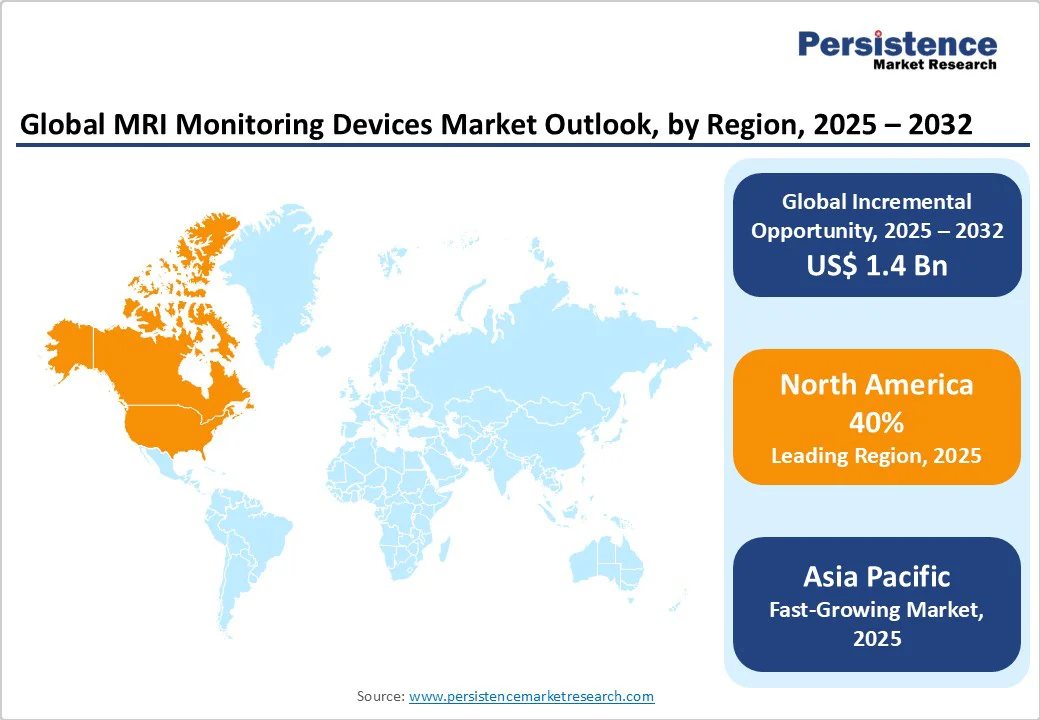

The global MRI monitoring devices market size is likely to value at US$4.2 Bn in 2025 and expected to reach US$5.6 Bn by 2032, registering a robust CAGR of 4.2% during the forecast period from 2025 to 2032, fueled by the increasing demand for safe patient monitoring during MRI procedures, advancements in non-magnetic technologies, and a global push toward enhancing diagnostic infrastructure and patient safety.

Key Industry Highlights:

- Leading Region: North America is expected to hold a 40% market share in 2025, driven by advanced healthcare infrastructure, widespread adoption of innovative monitoring solutions, and significant investments in medical device research.

- Fastest-growing Region: Asia Pacific, propelled by increasing prevalence of diagnostic advancements, urbanization, and expanding healthcare access in countries such as China and India.

- Dominant Product Type: Advanced MRI Monitoring Devices account for approximately 38% of the global MRI monitoring devices market share in 2025, owing to their critical role in precise vital signs capture and advancements in wireless designs.

- Leading End-user: Hospitals with a 51% share, reflecting their critical role in procedural safety and expansion procedures.

| Key Insights | Details |

|---|---|

|

MRI Monitoring Devices Market Size (2025E) |

US$4.2 Bn |

|

Market Value Forecast (2032F) |

US$5.6 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

4.2% |

|

Historical Market Growth (CAGR 2019 to 2024) |

3.1% |

Market Dynamics

Driver - Rising Demand for Patient Safety amid Increasing MRI Procedures and Technological Advancements

The global rise in demand for enhanced patient safety is a major driver of the MRI monitoring devices market. According to the World Health Organization, billions of diagnostic imaging procedures, including MRI scans, are performed each year worldwide, and the volume of MRI procedures continues to increase, making vital signs monitoring essential for high-risk patients and advanced diagnostic systems. This trend is compounded by the rising burden of chronic diseases and lifestyle-related health issues, with MRI environments becoming a critical area for safety innovation.

In response, governments and healthcare providers are investing heavily in advanced monitoring infrastructure, with the United States leading in the adoption of non-ferrous devices designed to ensure compliance with strict regulatory standards. In Europe, growing MRI installation activity and initiatives such as the EU’s Medical Device Regulation emphasize the importance of fiber-optic monitoring technologies.

The hospital sector, which represents a significant share of global diagnostic expenditure, is increasingly depending on MRI-compatible monitoring devices to overcome the challenges of electromagnetic interference, especially in regions with limited scanning capacity. The growing complexity of imaging applications will further intensify the requirements for precision, data integration, and quality of care delivery. In the Asia Pacific, aging populations fuel demand for reliable monitoring solutions such as wireless ECG and pulse oximetry. Rising investments in AI-driven imaging research are enabling the development of advanced monitoring platforms. With the expanding adoption of MRI worldwide and the shift toward hybrid imaging suites, the demand for interoperable, real-time monitoring solutions is expected to accelerate, positioning MRI monitoring devices as a cornerstone of patient safety.

Restraint - High Costs of Production and Stringent Regulatory Compliance

High costs linked with the development and deployment of comprehensive MRI monitoring systems remain a key restraint to market growth. Healthcare providers, especially in resource-limited regions, struggle with budgetary pressures when investing in advanced non-magnetic solutions that require seamless integration with existing MRI infrastructure. The customization of monitoring platforms to address varied procedural demands further elevates expenses. Regulatory compliance, including approvals in the U.S. and Europe, adds complexity and financial strain, as well as non-compliance risks, recalls and liabilities. Interoperability challenges, driven by the lack of standardized compatibility protocols across imaging vendors, slow down adoption and increase implementation costs.

Ongoing maintenance and system updates to align with evolving safety standards add to the burden, discouraging smaller providers from scaling operations. Supply chain disruptions for specialized fiber-optic components also create volatile pricing, affecting affordability in emerging economies. Additionally, integrating legacy systems in older hospitals requires significant consulting support, which inflates timelines and costs. Consequently, many facilities resort to partial rather than comprehensive monitoring solutions, restricting the industry’s broader potential.

Opportunity - Innovation in Formulations and E-commerce Expansion

Opportunities in the MRI monitoring devices market are strongly driven by advancements in wireless and AI-enabled technologies that enhance real-time patient oversight. The rapid expansion of ambulatory care and digital health services fuels demand for portable, fiberless, and biometric-integrated monitoring systems. Emerging solutions, such as non-invasive optical sensing, create new avenues in diagnostics and emergency care. In contrast, the rise of value-based care models increases the need for scalable, cost-efficient platforms. Vendors offering modular, API-driven systems that integrate seamlessly with existing imaging workflows are likely to benefit the most.

Patient-centric technologies, including remote vital signs telemetry, improve safety during scans without affecting imaging quality, attracting adoption in high-volume markets such as North America. Integration with telemedicine ecosystems also opens opportunities for innovative monitoring in virtual consultations, potentially creating new revenue streams. Public sector digitization initiatives in emerging economies further encourage the adoption of affordable solutions, supporting long-term contracts. Strategic partnerships between device manufacturers and MRI scanner providers can yield suite-optimized platforms, addressing interoperability gaps and reducing interference risks, ultimately driving sustained global market expansion.

Category-wise Analysis

Product Type Insights

The MRI monitoring devices market is segmented into basic and advanced MRI monitoring devices. Advanced MRI Monitoring Devices dominate, holding approximately 38% of market share in 2025, due to their proven efficacy in real-time vital capture, high precision, and integration into standard imaging protocols. Advanced devices are widely used in hospital suites, offering non-interfering telemetry that reduces procedural risks.

Basic MRI Monitoring Devices are the fastest-growing segment, driven by increasing demand for cost-effective solutions in ambulatory settings. Basic devices provide versatile deployment as entry-level options, with advancements in simplified designs and durability making them suitable for long-term use in resource-limited populations.

End-user Insights

The global MRI monitoring devices market is segmented into hospitals, ambulatory surgical centres, diagnostic centres, emergency medical services, and others. Hospitals hold approximately 51% share in 2025, due to their proven efficacy in procedural oversight, capacity support, and integration into clinical protocols. Hospitals are widely used in high-volume imaging, offering comprehensive controls that reduce adverse events.

Ambulatory surgical centres are the fastest-growing segment, driven by increasing demand for outpatient safety in elective procedures. These applications provide reliable monitoring as core systems, with advancements in portable tech and quick setup making them suitable for long-term use in dynamic populations.

Regional Insights

North America MRI Monitoring Devices Market Trends

North America dominates the global MRI monitoring devices market, expected to account for 40% share in 2025, driven by a robust healthcare ecosystem, high infrastructure investments, and a cultural emphasis on diagnostic innovation and safety. The United States, as the industry leader within the region, benefits from stringent regulations such as FDA Class II clearances that mandate advanced monitoring adoption across healthcare sectors.

The rapid proliferation of MRI facilities, which require sophisticated non-magnetic integration to ensure patient safety and procedural efficiency, is a major driver. Facilities in urban hubs such as Boston and San Francisco are leading adoption, investing in AI-enhanced devices to address procedural complications. The region’s mature R&D ecosystem further supports innovation in fiber-optic monitoring, while government initiatives such as NIH imaging safety grants accelerate uptake among hospitals.

Challenges such as reimbursement pressures remain significant, pushing providers toward bundled monitoring solutions to manage costs effectively. At the same time, the emphasis on continuous safety improvements fosters reliance on advanced platforms capable of seamless integration into complex imaging environments. Overall, North America’s procedure-intensive healthcare landscape and strong regulatory framework position it as the epicenter of monitoring evolution, with emerging trends leaning toward wireless technologies and real-time analytics for improved diagnostic outcomes.

Europe MRI Monitoring Devices Market Trends

Europe represents a mature yet evolving landscape in the MRI monitoring devices market, with countries such as Germany, the UK, and France driving regional growth through rigorous medical standards. Germany’s MedTech initiatives are fueling demand for monitoring solutions in diagnostics, with an emphasis on secure integrations for chronic care. The UK’s NHS digital strategy prioritizes compatible monitoring systems to improve procedural efficiency, while France leads in ambulatory digitization through its national imaging network, underscoring the region’s focus on interoperability.

Key drivers include the EU’s Medical Device Regulation, which encourages proactive upgrades and strengthens compliance across healthcare systems. Horizon Europe programs further expand opportunities for cross-border trials, supporting modular monitoring models that adapt to diverse clinical needs. Nordic countries such as Sweden stand out in developing sustainable devices for eco-friendly imaging suites, aligning with EU Green Deal goals. Challenges remain in achieving harmonized approvals, but collaborative efforts such as the European Medical Device Coordination Group are helping to establish standardized protocols. Overall, Europe’s market reflects a balance of precision and caution, with strong regulatory frameworks and innovation capacity positioning it for continued leadership in the evolution of MRI monitoring.

Asia Pacific MRI Monitoring Devices Market Trends

Asia Pacific is the fastest-growing region in the MRI monitoring devices market, driven by rapid healthcare modernization and rising diagnostic volumes in China, India, and Japan. China’s national healthcare initiatives are pushing hospitals to adopt advanced monitoring solutions, securing urban imaging infrastructures. In India, public health programs are creating strong demand for compatible and affordable devices across government facilities, broadening access for underserved populations. Japan, with its aging population, is advancing deployments in neurology, integrating biometric monitoring for precise cardiac and brain-related oversight.

Key drivers include the region’s expanding medical tourism sector, which necessitates robust end-user training and reliable monitoring technologies. Government investments across markets, including digital health and imaging safety programs, highlight a commitment to strengthening healthcare frameworks. Challenges such as varying import duties and uneven infrastructure persist, yet regional collaborations, including ASEAN’s medical device harmonization, are promoting cost-efficient innovation and market entry.

With a growing middle class and an expanding number of diagnostic procedures, the Asia Pacific is accelerating facility upgrades and the adoption of portable monitoring solutions for rural outreach, positioning the region as a dynamic growth hub in the global market.

Competitive Landscape

The global MRI monitoring devices market is moderately consolidated, with major medtech players and niche innovators competing through R&D, partnerships, and AI-driven fiber-optic platforms. Top vendors dominate advanced solutions, while smaller firms target portable, ambulatory applications. Strategic alliances with scanner manufacturers enhance integration, and emphasis on wireless, eco-compliant, and scalable designs intensifies competition. Mergers and regulatory pressures further shape market consolidation and leadership dynamics.

Key Developments

- October 2024: GE HealthCare unveiled a modular MRI monitoring device featuring cloud-enabled connectivity for remote data access. The platform supports customizable patient monitoring configurations, enabling hospitals to streamline workflows and reduce downtime during complex imaging procedures.

- May 2025: Iradimed Corporation (NASDAQ: IRMD), a world leader in cutting-edge medical devices for MRI environments, announced that its next-generation MRidium® 3870 IV Infusion Pump System has received 510(k) clearance from the U.S. Food and Drug Administration (FDA). This cutting-edge, MRI-compatible infusion pump strengthens Iradimed's distinct position as the only provider of non-magnetic MRI infusion pump devices worldwide, which was established in 2005 with our first-generation device.

Companies Covered in MRI Monitoring Devices Market

- Arcomed AG

- PULSION Medical Systems SE

- LiDCO Group PLC

- CAS Medical Systems

- Deltex Medical Group PLC

- Philips Medical Systems

- GE Healthcare

- Draeger Medical, Inc.

- Schwarzer Cardiotek GmbH

- Tensys Medical, Inc.

Frequently Asked Questions

The MRI monitoring devices market is projected to reach US$4.2 Bn in 2025.

Rising demand for procedural safety, technological advancements in non-magnetic designs, and government initiatives for imaging standards are key drivers.

The industry is poised to witness a CAGR of 4.2% from 2025 to 2032.

Innovations in wireless sensing and portable designs, such as AI-integrated monitors, present significant growth opportunities.

Arcomed AG, PULSION Medical Systems SE, Deltex Medical Group PLC, Philips Medical Systems, GE Healthcare, Draeger Medical, Inc., Schwarzer Cardiotek GmbH, and Tensys Medical, Inc. are among the leading players, known for their innovative monitoring solutions.