- Food Ingredients & Additives

- Stevia Market

Stevia Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Stevia Market by Stevia Type (Steviol Glycosides, Whole Leaf, Crude Extract, and Others), Form (Powder and Liquid), Application (Beverages, Dairy, Bakery & Confectionery, Tabletop Sweeteners, and Others) End-user (Food & Beverage Manufacturers, Pharmaceutical Companies, Nutraceutical Companies, Hypermarkets, Convenience Stores, and Others), and Regional Analysis from 2026 - 2033

Stevia Market Share and Trend Analysis

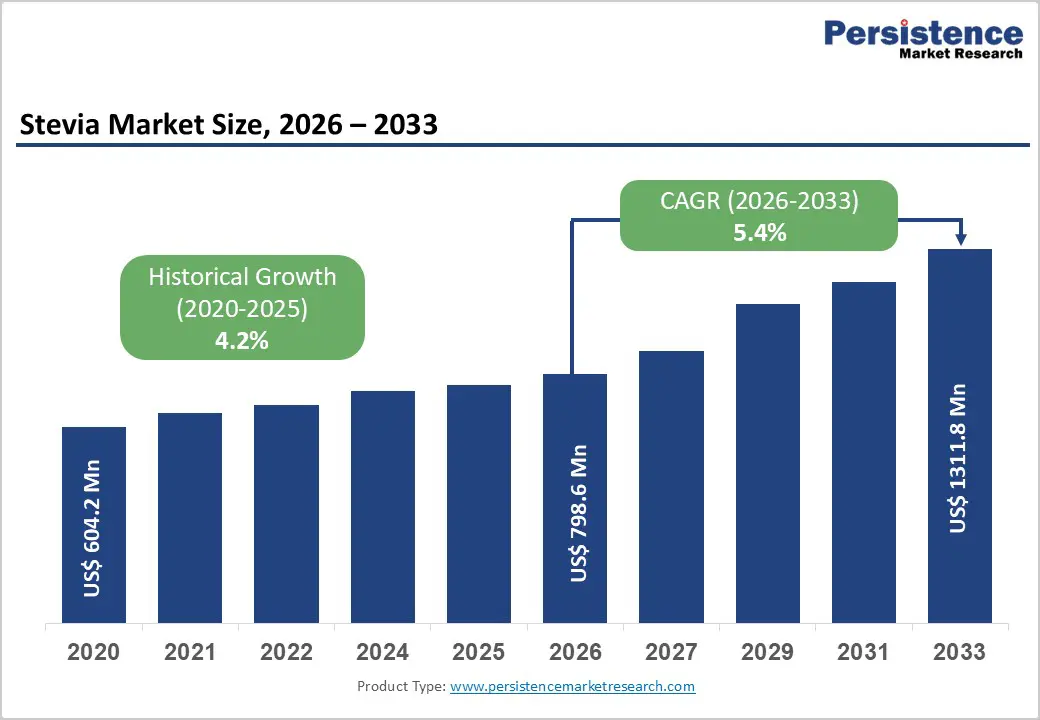

The global stevia market size is estimated to grow from US$ 798.6 Mn in 2026 to US$ 1311.8 Mn by 2033. The market is projected to record a CAGR of 5.4% during the forecast period from 2026 to 2033.

Rising preference for plant-based, low-calorie sweeteners is accelerating stevia adoption across food, beverage, and nutraceutical sectors, as consumers reduce sugar intake due to concerns around diabetes, obesity, and metabolic health. Its zero-calorie profile and natural origin make it a preferred alternative in carbonated drinks, flavored waters, dairy, and packaged foods, while also gaining traction in dietary supplements and functional products. Ongoing advancements in steviol glycoside purification, fermentation, and taste-modulation technologies have improved flavor and reduced bitterness, enabling wider application. Coupled with expanding supply chains and strategic collaborations, stevia is increasingly central to global sugar reduction and clean-label product development.

Key Industry Highlights

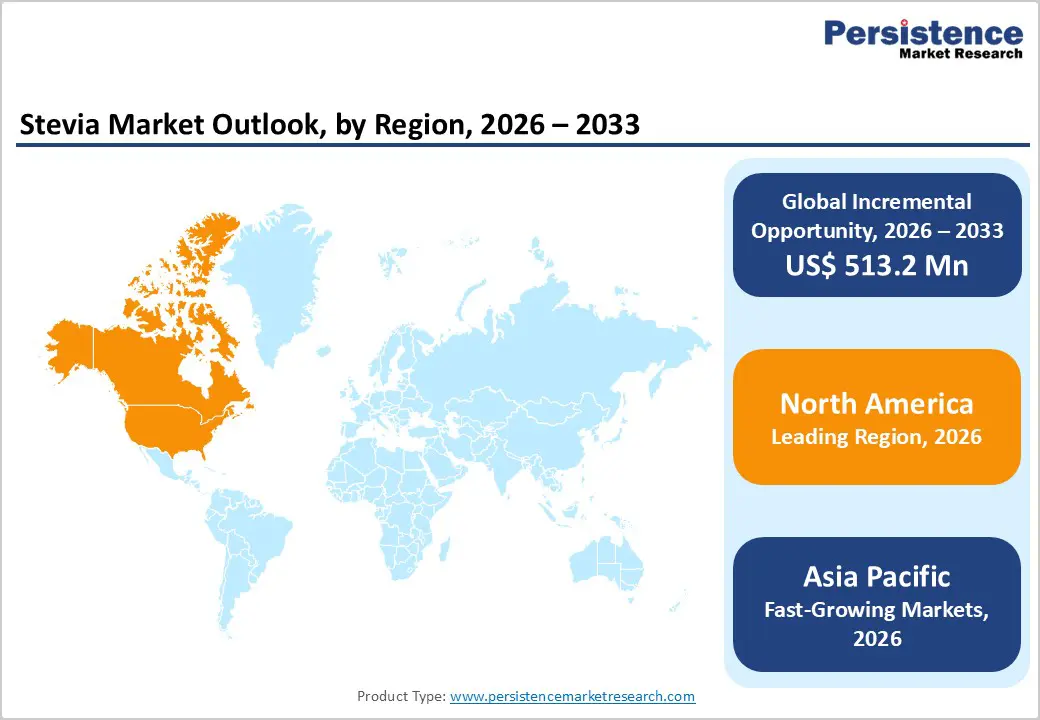

- Leading Region: North America holds the dominant share at 46.7%, driven by widespread product reformulation in beverages and packaged foods, strong presence of leading ingredient manufacturers, advanced R&D capabilities in high-purity glycosides, and high consumer awareness regarding sugar reduction and clean-label ingredients.

- Fastest-Growing Region: Asia Pacific is witnessing rapid expansion due to increasing health awareness, rising demand for low-calorie beverages, growth in food processing industries, and expanding adoption of natural sweeteners across emerging economies.

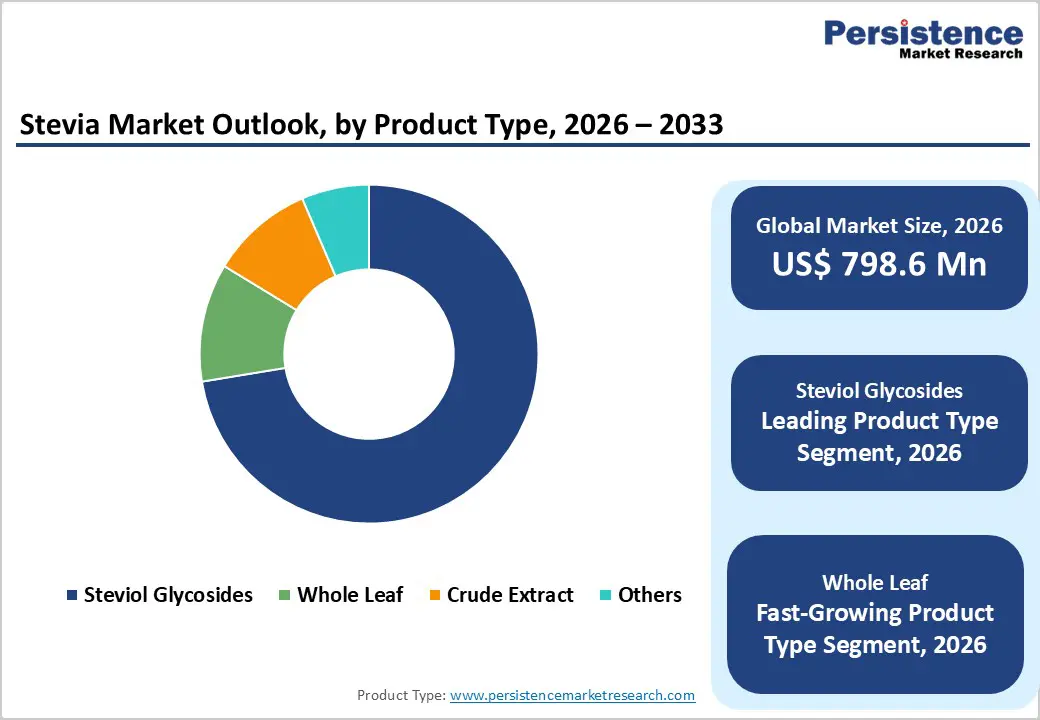

- Leading Type Segment: Steviol glycosides dominate with a 56.8% share, supported by their high sweetness intensity, zero-calorie nature, and extensive usage in beverages, dairy products, and tabletop sweeteners where taste and formulation stability are critical.

- Fastest-Growing Type Segment: Whole leaf is gaining traction as consumers increasingly prefer minimally processed, plant-based ingredients, particularly in nutraceuticals and premium health-focused formulations.

- Leading Application Segment: Beverages lead with a 38.9% share, driven by strong global demand for sugar-free and reduced-calorie drinks, including soft drinks, flavored waters, and functional beverages.

- Fastest-Growing Application Segment: Dairy is expanding at a notable pace as manufacturers introduce low-sugar yogurts, flavored milk, and functional dairy products targeting health-conscious consumers.

| Key Insights | Details |

|---|---|

| Stevia Market Size (2026E) | US$ 798.6 Mn |

| Market Value Forecast (2033F) | US$ 1311.8 Mn |

| Projected Growth (CAGR 2026 to 2033) | 5.4% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.2 % |

Market Dynamics

Driver - Increasing Shift Toward Natural, Zero-Calorie Sweeteners in Food and Beverage Formulations

Rising health consciousness and global efforts to reduce sugar consumption are significantly accelerating the adoption of plant-derived sweeteners such as stevia. Consumers are becoming more aware of the health risks associated with excessive sugar intake, including obesity, diabetes, and cardiovascular conditions, which is prompting a transition toward low-calorie and natural alternatives. Stevia, derived from plant sources, is gaining strong traction due to its zero-calorie profile and high sweetness intensity without contributing to glycemic load. Food and beverage manufacturers are actively reformulating products, particularly soft drinks, flavored beverages, dairy items, and packaged foods, to align with evolving dietary preferences and regulatory pressures aimed at sugar reduction.

Additonally, clean-label trends are encouraging companies to eliminate artificial sweeteners and replace them with natural ingredients that offer transparency and perceived health benefits. Stevia fits well within this positioning, supporting its widespread incorporation across both mainstream and premium product categories. Continuous advancements in steviol glycoside purification and fermentation-based production have improved taste profiles, reducing bitterness and enhancing consumer acceptance. These developments, combined with growing global demand for healthier food options, are reinforcing stevia’s role as a key ingredient in next-generation reduced-sugar formulations.

Restraints - Taste Challenges, Cost Factors, and Supply Chain Limitations Impacting Large-Scale Adoption

The lingering aftertaste associated with earlier generations of steviol glycosides, which can limit its use in products requiring a clean sugar-like flavor profile. Although newer variants such as Reb M have improved sensory performance, they often involve higher production costs due to complex extraction or fermentation processes. This creates pricing pressures for manufacturers, particularly when competing with low-cost artificial sweeteners or sugar itself. Supply chain constraints also play a role, as stevia production depends on agricultural cultivation, primarily concentrated in specific regions. Variability in crop yield, climatic conditions, and raw material availability can influence supply stability and pricing.

Additionally, achieving consistent purity levels and maintaining quality standards require advanced processing technologies, increasing operational complexity. Regulatory differences across regions regarding acceptable usage levels and labeling requirements further add to market challenges. Manufacturers must invest in formulation strategies such as blending with other sweeteners or flavor modifiers to overcome taste limitations, which can increase development costs and time-to-market.

Opportunity - Expansion of High-Purity Glycosides and Growth in Functional, Clean-Label Product Segments

Emerging innovations in steviol glycoside production and increasing demand for healthier food alternatives are creating substantial growth opportunities across the value chain. Next-generation compounds such as Reb M and Reb D are gaining attention due to their improved taste profile and closer resemblance to sugar, enabling broader application in beverages, dairy, and confectionery products. Advances in fermentation and bioconversion technologies are allowing manufacturers to produce these high-purity glycosides at scale, reducing reliance on traditional leaf extraction and improving supply consistency.

Moreover, the expansion of functional foods and nutraceutical products is opening new avenues for stevia incorporation. It is increasingly used in dietary supplements, protein powders, and health-focused snacks where sugar reduction is a key selling point. The rise of plant-based diets and clean-label product positioning is further strengthening demand, particularly in developed markets. Additionally, growing consumer interest in personalized nutrition and diabetic-friendly products is encouraging companies to innovate with stevia-based formulations. Emerging markets in Asia Pacific and Latin America also present untapped potential due to rising disposable incomes and shifting dietary habits. Collectively, these factors position stevia as a critical ingredient in the evolving global landscape of healthier and more sustainable food systems.

Category-wise Analysis

By Stevia Type, Steviol Glycosides Dominate Due to Superior Sweetening Efficiency and Clean Taste Profile

Steviol glycosides are projected to remain the leading product category in the global stevia market in 2026, accounting for 72.4% of total revenue. Their dominance stems from high-intensity sweetness, zero-calorie profile, and strong compatibility across a wide range of formulations. Food and beverage companies extensively utilize glycosides such as Reb A and emerging variants like Reb M in carbonated drinks, flavored beverages, dairy products, and tabletop sweeteners. These compounds deliver sugar-like taste with reduced bitterness compared to earlier generations, improving consumer acceptance. Beyond traditional applications, their usage is expanding into nutraceuticals and pharmaceuticals where sugar reduction is critical. Continuous advancements in bioconversion and fermentation technologies have improved purity levels and sensory performance. As global regulatory approvals expand and clean-label preferences intensify, steviol glycosides continue to serve as the primary commercial driver within the stevia ingredient landscape.

By Form, Powder Leads Owing to Ease of Handling and Stability in Industrial Processing

The powder segment is expected to hold the largest market share in 2026, contributing 93.6% of total revenue. Its dominance is attributed to superior shelf stability, ease of transportation, and compatibility with large-scale manufacturing processes. Powdered stevia is widely used in dry mixes, bakery formulations, dietary supplements, and beverage premixes where precise dosing and uniform blending are essential. Manufacturers prefer this format for its longer storage life and resistance to degradation under varying environmental conditions. Additionally, powdered variants allow easier incorporation into multi-ingredient formulations without altering texture or consistency. The format also supports bulk handling, making it highly suitable for industrial procurement. Technological improvements in drying and crystallization processes have further enhanced solubility and dispersion characteristics. While liquid stevia is gaining traction in specific beverage applications, powder remains the backbone of commercial supply due to its operational efficiency and scalability.

By Application, Beverages Lead Driven by Global Sugar Reduction and Reformulation Trends

The beverages segment is anticipated to account for 31.8% of total market revenue in 2026, making it the largest application area. Stevia is increasingly used in soft drinks, flavored waters, energy drinks, and ready-to-drink teas as manufacturers reformulate products to reduce sugar content without compromising sweetness. The growing incidence of diabetes and obesity has accelerated the shift toward low-calorie beverages, positioning stevia as a preferred alternative to artificial sweeteners. In addition to beverages, applications extend across dairy products, baked goods, and confectionery, where stevia helps achieve calorie reduction targets while maintaining taste. Tabletop sweeteners also contribute significantly, particularly among health-conscious consumers. Advances in flavor-masking technologies and blending strategies have improved the sensory profile of stevia-based formulations. As regulatory pressure on sugar reduction intensifies globally, beverage manufacturers continue to drive the largest share of stevia consumption.

Region-wise Insights

North America Stevia Market Trends

North America is projected to account for 46.7% of the global stevia market value in 2026, with the United States representing the largest contributor. The region’s leadership is supported by a highly developed food and beverage industry actively reformulating products to reduce sugar content. Major beverage manufacturers have widely adopted stevia in carbonated drinks, flavored waters, and functional beverages to align with evolving consumer preferences for low-calorie alternatives. Strong awareness regarding obesity, diabetes, and overall wellness has accelerated demand for natural sweeteners across retail and industrial segments.

Additionally, the presence of leading ingredient suppliers and advanced R&D infrastructure supports continuous innovation in high-purity steviol glycosides, particularly next-generation variants such as Reb M. Regulatory support from food safety authorities has further facilitated product approvals and commercialization. The region also benefits from well-established retail networks and high purchasing power, enabling widespread adoption of stevia-based tabletop sweeteners. Combined with strong investment in fermentation-based production technologies, North America continues to maintain a dominant position in the global stevia market.

Europe Stevia Market Trends

Europe represents a mature yet innovation-focused market for stevia, driven by strong regulatory frameworks and increasing demand for natural sugar substitutes. Countries such as Germany, France, the United Kingdom, Italy, and Spain are key contributors, supported by well-established food processing and nutraceutical industries. The region has witnessed a significant shift toward clean-label and plant-based ingredients, encouraging manufacturers to replace artificial sweeteners with stevia in a wide range of products. Beverage reformulation remains a key growth area, particularly in low-calorie soft drinks and functional beverages.

European consumers show a strong preference for transparency and ingredient traceability, which has prompted companies to invest in sustainable sourcing and high-quality extraction processes. In addition, regulatory oversight ensures consistent quality standards and safe consumption levels, enhancing consumer confidence. The pharmaceutical and nutraceutical sectors are also incorporating stevia into formulations aimed at diabetic and weight-management applications. Continuous product innovation and sustainability initiatives position Europe as a stable and technologically advanced stevia market.

Asia Pacific Stevia Market Trends

Asia Pacific is expected to be the fastest-growing region, expanding at a CAGR of approximately 7.3% between 2026 and 2033. The region’s growth is driven by rapid urbanization, increasing disposable incomes, and shifting dietary preferences toward healthier alternatives. Countries such as China, India, Japan, and South Korea are witnessing strong demand for low-calorie and sugar-free products across beverages, dairy, and packaged foods. China plays a critical role as a leading producer and exporter of stevia, supported by large-scale cultivation and processing capabilities.

Moreover, rising health awareness in India and Southeast Asia is accelerating adoption of stevia-based tabletop sweeteners and functional foods. Beverage manufacturers across the region are increasingly incorporating stevia to cater to growing demand for reduced-sugar drinks. Expanding nutraceutical industries are also utilizing stevia in diabetic-friendly and weight management formulations. Government initiatives promoting agricultural development and natural ingredient production further support market expansion. With its large population base and evolving health trends, Asia Pacific continues to emerge as the most dynamic growth engine for the global stevia market.

Competitive Landscape

The global stevia market is highly competitive, with strong participation from Cargill, Incorporated, GLG Life Tech Corporation, Archer-Daniels-Midland Company, Pyure Brands LLC, and Guilin Layn Natural Ingredients Corp., Ltd.. These companies leverage advanced steviol glycoside extraction, fermentation-based production, and global ingredient distribution networks to strengthen market presence while improving taste profiles, purity, and formulation stability across food, beverage, nutraceutical, and pharmaceutical applications.

Rising demand for natural, zero-calorie sweeteners is accelerating innovation. Manufacturers are expanding capacity, optimizing leaf sourcing, ensuring regulatory compliance, forming partnerships, and increasing R&D investments to develop next-generation high-purity stevia ingredients.

Key Industry Developments:

- In July 2025, Layn Natural Ingredients introduced SteviUp M2, a next-generation plant-based sweetener. The clean-label, highly soluble formulation is designed to provide a more sugar-like taste with reduced lingering sweetness compared to conventional steviol glycosides. The product has also been reviewed by the U.S. Food and Drug Administration (FDA) and recognized as Generally Recognized as Safe (GRAS) for use as a general-purpose sweetener in food and beverage applications.

- In August 2024, the Australia New Zealand Food Standards Authority approved a novel steviol glycoside sweetener developed by Sichuan Yingjia Hesheng Technology using genetically engineered E. coli through an enzymatic process. The product is now permitted as a food additive, highlighting increasing acceptance of biotechnology-driven sugar alternatives in the region.

Companies Covered in Stevia Market

- Cargill, Incorporated

- GLG Life Tech Corporation

- Archer-Daniels-Midland Company

- Pyure Brands LLC

- Guilin Layn Natural Ingredients Corp., Ltd.

- HOWTIAN Group

- Tate & Lyle PLC

- Ingredion Incorporated

- Sunwin Stevia International, Inc.

- Heartland Consumer Products LLC

- The Truvía Company, LLC

- Whole Earth Brands, Inc.

- GL Stevia Co., Ltd.

- Morita Kagaku Kogyo Co., Ltd.

- SweeGen, Inc.

- Othes

Frequently Asked Questions

The global stevia market is projected to be valued at US$ 798.6 Mn in 2026.

Rising demand for natural, zero-calorie sweeteners driven by increasing health awareness, diabetes prevalence, and global sugar reduction initiatives.

The global stevia market is poised to witness a CAGR of 5.4% between 2026 and 2033.

Expansion in next-generation steviol glycosides (Reb M/D), growing beverage reformulation, and increasing penetration in emerging markets and clean-label products.

Cargill, Incorporated, GLG Life Tech Corporation, Archer-Daniels-Midland Company, Pyure Brands LLC, and Guilin Layn Natural Ingredients Corp., Ltd. are some of the key players in the stevia market.