- Hardware & Software IT Services

- Workforce Management Market

Workforce Management Market Size, Share, and Growth Forecast, 2026 - 2033

Workforce Management Market by Offering (Software, Services), Deployment (On-Premises, Cloud-Based, Hybrid), Enterprise Size (Small & Medium Enterprises (SMEs), Large Enterprises), Industry, and Regional Analysis for 2026 - 2033

Workforce Management Market Size and Trends Analysis

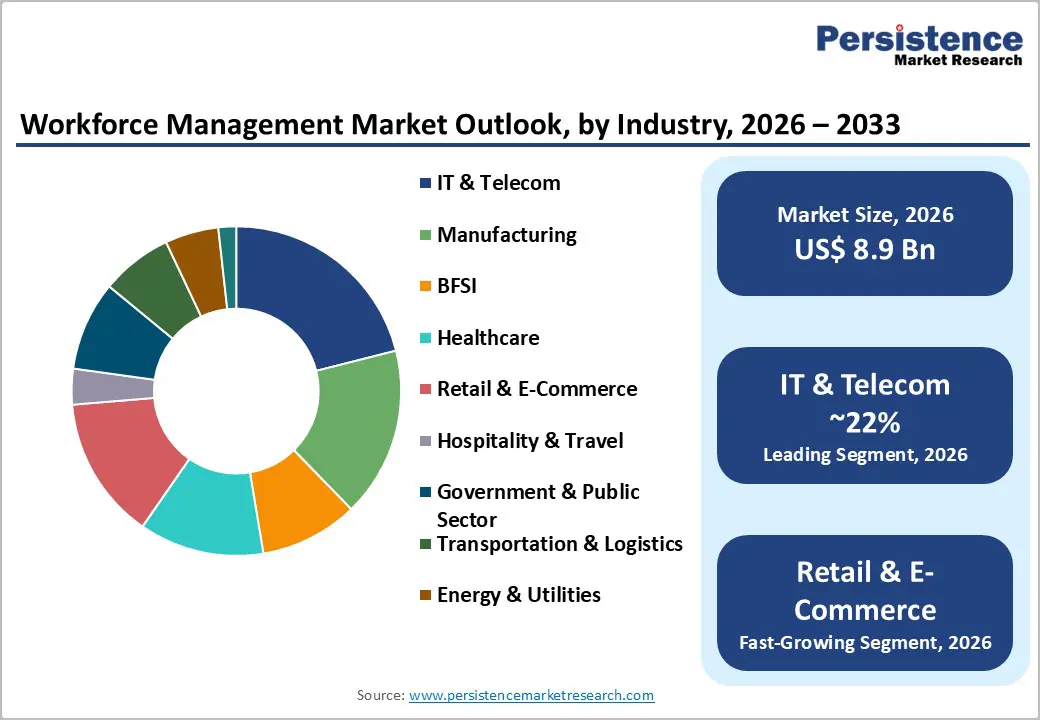

The global Workforce Management Market size is projected to rise from US$8.9 billion in 2026 to US$17.5 billion by 2033. It is anticipated to witness a CAGR of 10.2% during the forecast period from 2026 to 2033.

This robust expansion reflects the growing demand for labor compliance automation, real-time workforce visibility, and AI-driven scheduling optimization across global enterprises. Organizations increasingly recognize workforce management solutions as strategic tools for reducing operational costs, improving employee engagement, and maintaining regulatory compliance. Digital transformation initiatives, hybrid workforce proliferation, and stricter labor regulations drive sustained adoption across manufacturing, healthcare, IT & telecom, and retail sectors.

Key Industry Highlights:

- Leading Offering: Software accounting for over 65% share in 2026 with a value exceeding US$ 5.8 Bn, driven by demand for integrated WFM suites that reduce data silos and streamline scheduling, attendance, and compliance. Services are the fastest-growing segment at 14.1% CAGR, fueled by the rising need for implementation, integration, consulting, and managed services as organizations adopt AI-driven and cloud-based WFM platforms.

- Leading Deployment: On-premises lead with over 47% market share in 2026, valued above US$ 4.2 Bn, for greater data control, regulatory compliance, customization, and integration with legacy ERP and HR systems. Cloud-based deployment is the fastest-growing, registering 15.3% CAGR, driven by scalability, subscription pricing, rapid deployment, and reduced IT maintenance overhead.

- Leading Enterprise Size: Large enterprises dominate with over 62% market share in 2026, valued at more than US$ 5.5 Bn, due to complex workforce structures, multi-location operations, and stringent compliance requirements. SMEs represent the fastest-growing segment at 14.9% CAGR, supported by the adoption of cost-efficient, cloud-based, and mobile-enabled workforce management solutions.

- Leading Industry: IT & Telecom holds the largest share, exceeding 22% in 2026 with a value above US$ 2.0 Bn, driven by 24/7 operations, distributed teams, and the need for advanced scheduling and predictive workforce analytics. Retail & E-Commerce is among the fastest-growing industries, supported by seasonal workforce scaling, high employee turnover, and demand for real-time labor optimization.

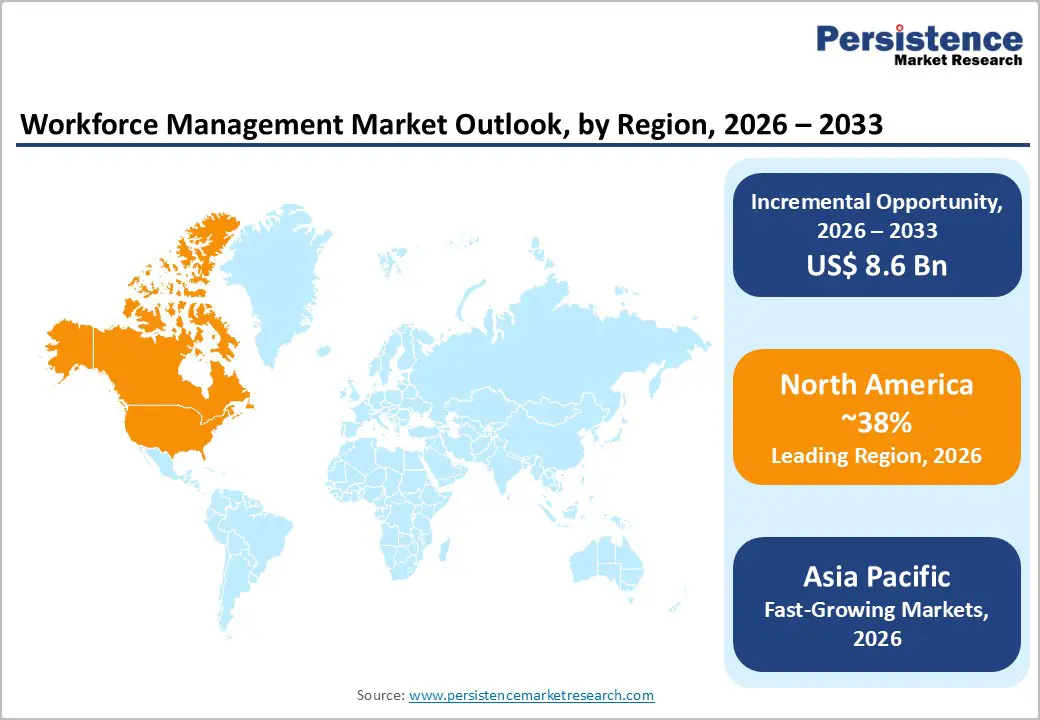

- Leading Region: North America leads the global market with over 38% share in 2026, valued at US$ 3.4 Bn, driven by advanced technology adoption, regulatory complexity, and strong vendor presence, with the U.S. alone surpassing US$ 2.6 Bn. Asia Pacific is the fastest-growing region at 15.6% CAGR, driven by industrial expansion, labor law reforms in India, manufacturing growth in China, and workforce shortages in Japan. Europe is projected to hold over 28% share by 2033, valued above US$ 2.5 Bn, supported by stringent GDPR compliance and labor protection regulations.

| Key Insights | Details |

|---|---|

|

Workforce Management Market Size (2026E) |

US$8.9 Bn |

|

Market Value Forecast (2033F) |

US$17.5 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

10.2% |

|

Historical Market Growth (CAGR 2020 to 2025) |

7.5% |

Market Dynamics

Driver - AI-Driven Forecasting and Labor Optimization

Artificial intelligence and machine learning are revolutionizing through predictive scheduling, demand forecasting, and intelligent task allocation. AI-driven analytics optimize shift planning by considering historical sales, employee skills, availability, and customer demand, enhancing productivity and reducing staff burnout. Approximately 70% of healthcare organizations and numerous manufacturing enterprises are adopting AI to improve labor efficiency, manage multi-shift operations, and lower labor costs. Generative AI and autonomous agents now enable predictive workforce orchestration, resolving scheduling conflicts and approving time-off in real time, as demonstrated by innovations from Workday and UKG in 2024–2025. These capabilities allow organizations to simulate “what-if” scenarios, optimizing labor spend without compromising service quality, making AI indispensable for enterprise decision-making.

Increasing Regulatory Compliance Requirements and Labor Law Complexity

Stricter global labor regulations are driving demand for advanced workforce management solutions. GDPR in Europe enforces stringent employee data protection, with penalties up to €20 million or 4% of global revenue, while India’s new labor codes require tracking of work hours, overtime, benefits, and compliance. Manufacturing sectors face enhanced safety and reporting obligations, and remote work rules in regions like Ireland and Abu Dhabi demand formal request and approval workflows. Automated compliance monitoring, audit trails, and real-time reporting embedded in modern systems help organizations mitigate audit risks and avoid penalties, fueling sustained market adoption across industries and geographies.

Restraint - Implementation Complexity and Change Management Resistance

Deploying enterprise-grade workforce management solutions involves significant change management and technical challenges. Large organizations with complex legacy systems face long implementation timelines, integration issues, and extensive training needs, while SMEs often lack IT expertise and change management capabilities. Employee resistance, workflow disruptions during transition, and ongoing maintenance demands further constrain adoption. These barriers particularly affect enterprises with legacy infrastructure, limited IT budgets, or low digital literacy, limiting market growth in these segments.

Data Security Concerns and Privacy Compliance Complexity

Workforce management systems handle sensitive employee data such as timekeeping records, location, performance metrics, and biometric information, necessitating stringent security and privacy measures like encryption, access controls, and anonymization. Multinational organizations face added complexity with cross-border data compliance e.g., GDPR, while cybersecurity threats pose regulatory, financial, and reputational risks. Managing security across cloud platforms, third-party integrations, and mobile access requires continuous investment in infrastructure, training, and monitoring, creating high operational costs that can limit adoption, especially among smaller enterprises with constrained IT budgets.

Opportunity - Convergence with Employee Experience (EX) Platforms

The workforce management market is evolving from a compliance-focused tool to an employee experience (EX) enabler, driving retention and engagement. Vendors capitalize on this by offering worker-centric features like shift bidding, earned wage access (EWA), and automated shift swaps, giving employees more control over work-life balance. Integrating wellness modules and sentiment analysis helps mitigate frontline burnout, allowing WFM solutions to access broader HR budgets beyond operations and IT, thereby expanding their total addressable market.

Healthcare Industry Digital Transformation and Staffing Optimization

The healthcare workforce management market is poised for significant growth, driven by an expected global shortage of 11 million healthcare professionals by 2030 and critical staffing challenges. Providers are adopting AI-driven scheduling, predictive staffing analytics, and mobile-enabled, cloud-based solutions to optimize staff allocation across hospitals, urgent care centers, and clinical departments, reduce burnout, and improve patient care. Geographic workforce disparities, such as Texas 224 counties designated as Health Professional Shortage Areas, further highlight the need for intelligent workforce management. Regulatory compliance and ongoing demand for operational efficiency create recurring software revenue opportunities, reflecting strong investment willingness among healthcare organizations.

Category-wise Analysis

Offering Analysis

Software dominates the global market, capturing more than 65% market share in 2026 with a value exceeding US$ 5.8 billion. Integrated workforce management suites represent the largest software sub-segment, commanding over 56% share as organizations prefer integrated solutions, minimizing data silos, reducing integration complexity, and simplifying system administration. Time and attendance management software captures more than 28% share of the standalone software category, reflecting demand for specialized solutions addressing core timekeeping requirements.

Services demonstrate the highest growth rate at 14.1% CAGR due to the increasing demand for expert implementation, integration, and ongoing support of complex WFM solutions. Organizations are seeking managed services, consulting, and training to optimize workforce scheduling, compliance, and productivity without heavy in-house IT investments. The shift toward cloud-based and AI-driven WFM systems further drives the need for professional services to ensure seamless deployment, customization, and continuous system updates, enabling businesses to respond quickly to dynamic staffing needs.

Deployment Insights

On-premises hold over 47% market share in 2026, with a value exceeding US$ 4.2 billion as organizations prioritize greater control over sensitive employee and operational data, ensuring compliance with internal policies and industry regulations. Large enterprises with complex workforce structures often require highly customizable systems that integrate seamlessly with existing ERP and HR platforms. On-premise deployments offer enhanced security, reliability, and offline functionality, addressing critical needs for mission-critical operations and reducing dependency on external networks.

Cloud-based deployments are expected to grow at the highest rate, with a CAGR of 15.3%, driven by cost advantages, operational flexibility, and ease of integration with modern HR technology stacks. Subscription-based pricing models reduce large upfront capital expenditures, aligning software costs with business value realization. Automatic updates, built-in security patches, and seamless feature enhancements minimize IT maintenance overhead and reduce operational complexity. Scalability enabling rapid user expansion supports organizational growth without infrastructure investment.

Enterprise Size Insights

Large enterprises command the largest market share at over 62% in 2026, with a value exceeding US$ 5.5 billion, due to their complex operational structures, large employee base, and diverse workforce requirements. They require advanced scheduling, real-time attendance tracking, and predictive analytics to optimize productivity and reduce labor costs. Compliance with labor laws, shift management across multiple locations, and integration with HR and payroll systems drive their adoption of comprehensive workforce management solutions.

Small & medium enterprises (SMEs) are expected to grow at a CAGR of 14.9%, due to their increasing need for cost-efficient and scalable solutions. SMEs face challenges in managing labor costs, scheduling, and compliance with labor regulations, driving adoption of automated workforce management tools. Cloud-based and mobile-enabled systems allow SMEs to optimize staffing, reduce errors, and improve productivity without heavy IT infrastructure. The rising focus on employee engagement and retention compels SMEs to implement solutions that streamline operations and support flexible work arrangements.

Industry Insights

IT & Telecom maintains a dominant market position with over 22% share in 2026 and value exceeding US$ 2.0 billion due to high demand for efficient workforce utilization across large, distributed teams. Rapid digital transformation, 24/7 operations, and complex project-based work necessitate advanced scheduling, real-time monitoring, and predictive staffing solutions. The sector’s reliance on skilled technical staff and the need to reduce attrition and operational costs drive the adoption of automated workforce management systems. These tools help ensure service continuity, optimize resource allocation, and enhance employee productivity.

Retail & e-commerce is expected to grow at significant rates, driven by the need for rapid scaling of staff during peak seasons, flash sales, and promotional events. Businesses increasingly rely on advanced scheduling and real-time labor analytics to optimize employee deployment across multiple stores and fulfillment centers. High employee turnover and demand for flexible shift management further drive adoption. Integrating AI-driven forecasting ensures inventory and customer service needs are met efficiently, enhancing operational agility.

Regional Insights

North America Workforce Management Market Trends

North America maintains market leadership with over 38% share in 2026, reaching US$ 3.4 billion value, with the U.S. market alone crossing US$ 2.6 billion by 2026. This region maintains market leadership through advanced technology adoption, strong IT infrastructure, and significant vendor presence. The regulatory environment, characterized by complex overtime regulations, wage transparency laws, and industry-specific labor standards, drives consistent WFM adoption. North America's innovation ecosystem attracts substantial R&D investment from leading vendors, supporting the development of advanced AI-driven and analytics-focused solutions. Investment in employee experience and engagement drives adoption of mobile-first, user-centric platforms offering self-service capabilities.

Asia Pacific Workforce Management Market Trends

Asia-Pacific emerges as the highest-growth region with 15.6% projected CAGR through 2033, driven by rapid industrial expansion, massive labor force growth, and accelerated digital transformation. China's manufacturing-driven economy and Industry 4.0 ambitions create workforce management demand across automotive, electronics, and industrial equipment sectors. Japan's labor shortage challenges, aging workforce demographics, and automation priorities drive workforce optimization through advanced workforce management solutions. India's labor code implementation across 36 states and union territories creates immediate compliance-driven demand for workforce management platforms addressing minimum wage tracking, overtime management, and social security compliance.

Europe Workforce Management Market Trends

Europe is expected to hold more than 28% share by 2033 with value exceeding US$ 2.5 Bn, driven by stringent regulatory requirements, labor protection emphasis, and workforce optimization focus. GDPR compliance requirements establishing strict employee data protection standards create universal demand for secure, privacy-compliant workforce management platforms across all European organizations. European labor law emphasizes employee rights, working time directives, and social security benefits, creating complex compliance requirements addressed through specialized workforce management solutions. Manufacturing sector significance across Germany, France, and U.K. combined with Industry 4.0 digital transformation initiatives, creates sustained demand for workforce management solutions integrating with production planning systems.

Competitive Landscape

The global workforce management market is moderately consolidated. A few large vendors dominate enterprise and regulated-industry deployments by leveraging integrated platforms, strong brand presence, and long-term client contracts. Vendors compete through continuous innovation in AI-enabled forecasting, compliance management, and advanced analytics, while using acquisitions and ecosystem partnerships to strengthen capabilities. High switching costs and deep system integration further reinforce the position of leading players.

Key Industry Developments:

- In November 2025, Workday completed the acquisition of Sana, an AI-powered enterprise knowledge platform, to strengthen its workforce and enterprise management capabilities. The integration positions Workday as a unified “front door for work,” enabling employees to access knowledge, automate tasks, and enhance productivity through AI-driven workflows.

- In October 2024, ADP announced the acquisition of WorkForce Software to strengthen and expand its global workforce management capabilities for large, multinational enterprises. The deal enhances ADP’s ability to deliver compliant, flexible, and innovative workforce management solutions, addressing evolving workforce needs while driving future innovation in the HCM space.

Companies Covered in Workforce Management Market

- Oracle Corporation

- SAP SE

- ADP, Inc.

- UKG Inc.

- Workday, Inc.

- Infor

- Verint Systems

- Workforce Software LLC

- NICE Ltd.

- ATOSS Software AG

- Replicon Inc.

- Paychex, Inc.

- Others

Frequently Asked Questions

The global workforce management market is projected to be valued at US$8.9 Bn in 2026.

Growing need for businesses to optimize labor costs, ensure regulatory compliance, and maintain productivity amid workforce shortages is a key driver of the market.

The market is expected to witness a CAGR of 10.2% from 2026 to 2033.

Rising adoption of AI-driven analytics and mobile workforce solutions that enable real-time scheduling, predictive staffing, and improved employee experience is creating strong growth opportunities.

Oracle Corporation, SAP SE, ADP, Inc., UKG Inc., Workday, Inc., and Infor are among the leading key players.