- Pharmaceuticals

- Venous Thromboembolism Treatment Market

Venous Thromboembolism Treatment Market Size, Share, and Growth Forecast, 2026 – 2033

Venous Thromboembolism Treatment Market by Product Type (Thrombectomy Devices, Compression Systems, Others), Disease Indication (Deep Venous Thrombosis, Pulmonary Embolism), End-user (Hospitals, Others), and Regional Analysis 2026 - 2033

Venous Thromboembolism Treatment Market Size and Trends Analysis

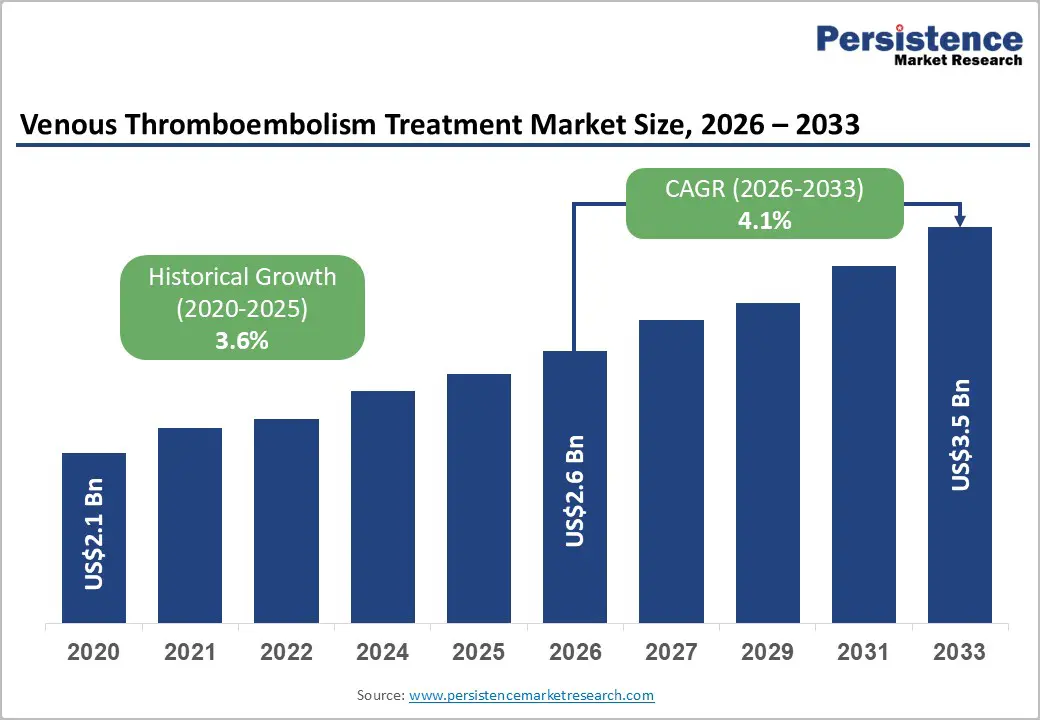

The global venous thromboembolism treatment market size is likely to be valued at US$2.6 billion in 2026 and is expected to reach US$3.5 billion by 2033, growing at a CAGR of 4.1% during the forecast period from 2026 to 2033, driven by advancements in minimally invasive thrombectomy devices that accelerate treatment efficacy and reduce recovery times for patients.

Rising awareness of VTE risks post-surgery propels demand for prophylactic compression systems. Integration of AI-driven diagnostics enhances early intervention protocols across hospitals. These dynamics position the market for sustained expansion amid aging populations and improved reimbursement frameworks. Technological integration in compression systems is projected to improve patient compliance and long-term recovery outcomes. Rising healthcare expenditure in emerging economies is set to expand access to specialized venous care.

Key Industry Highlights:

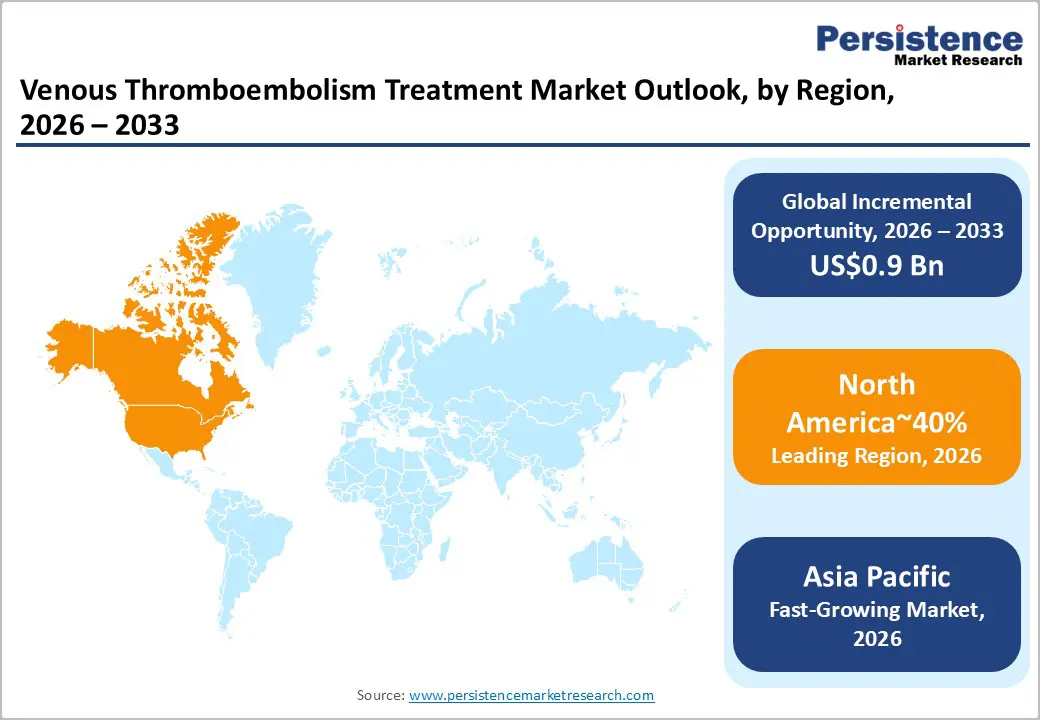

- Leading Region: North America is projected to lead, accounting for approximately 40% share in 2026, supported by robust healthcare infrastructure, high adoption of mechanical thrombectomy, and favorable reimbursement policies.

- Fastest-growing Region: Asia Pacific is anticipated to grow the fastest, driven by rapid urbanization, expanding geriatric populations, and significant investments in healthcare modernization.

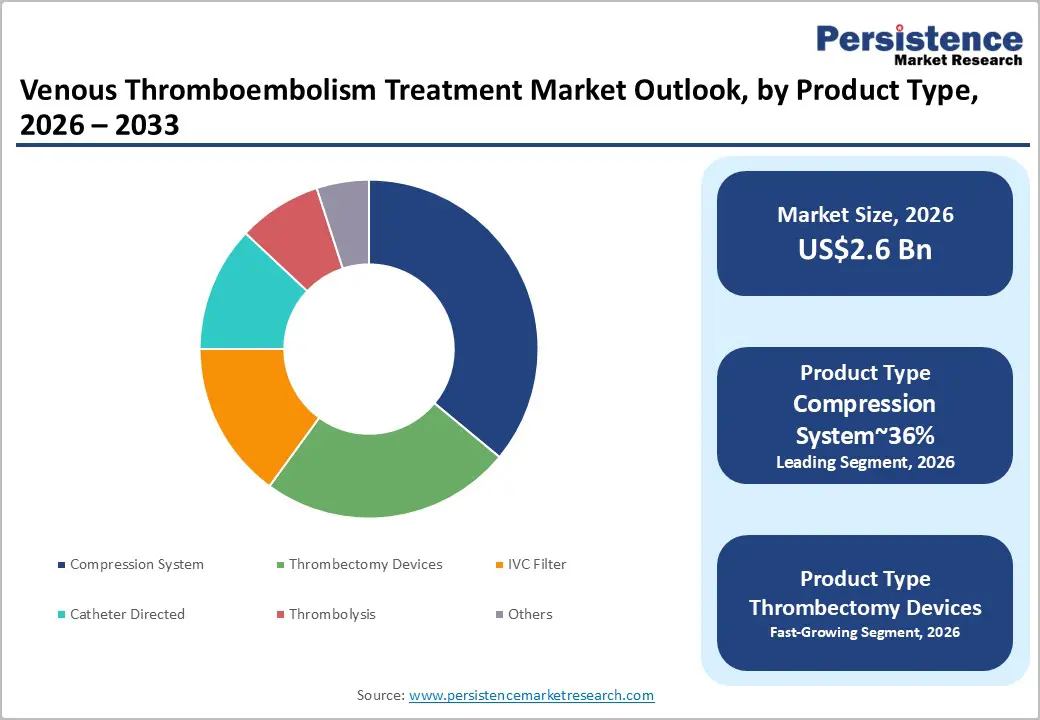

- Leading Product Analysis: Compression System is expected to lead, accounting for approximately 36% share in 2026, anchored by its critical role in prophylaxis and non-invasive treatment protocols.

- Leading Disease Indication: Deep Venous Thrombosis (DVT) is projected to dominate, holding approximately 66% share in 2026, driven by high prevalence rates and increasing post-surgical complications.

| Key Insights | Details |

|---|---|

|

Venous Thromboembolism Treatment Market Size (2026E) |

US$2.6 Bn |

|

Market Value Forecast (2033F) |

US$3.5 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.1% |

|

Historical Market Growth (CAGR 2020 to 2025) |

3.6% |

DRO Analysis

Driver Analysis – Increasing Adoption of Mechanical Thrombectomy in Acute Care

Expanding clinical evidence for rapid clot removal is projected to drive demand for mechanical interventions. Traditional pharmaceutical approaches are likely to face competition from immediate physical extraction techniques in hospitals. Surgeons are expected to prioritize mechanical solutions to reduce the risk of post-thrombotic syndrome. Improved catheter designs are anticipated to enhance the safety profile of complex venous procedures. Faster recovery times are expected to encourage hospital administrators to invest in advanced interventional equipment. Advancements in catheter engineering are improving navigability, thereby lowering procedural risk in complex venous anatomies. Enhanced safety profiles are influencing reimbursement considerations, supporting broader institutional adoption across tertiary care centers. Patients are projected to benefit from reduced reliance on long-term systemic thrombolytic drug regimens.

Innovation from Inari Medical’s FlowTriever is accelerating the shift toward large-bore mechanical thrombectomy procedures. These specialized devices are expected to improve outcomes for patients with high-risk pulmonary embolism. Device innovation is increasingly aligned with regulatory emphasis on safety, efficacy, and reduced systemic complications. Clinical trial frameworks are evolving to demonstrate cost-effectiveness against traditional pharmacological standards of care. Penumbra’s Indigo System, by contrast, reflects the continuous aspiration thrombectomy model, which offers finer control and is often preferred in more distal or organized thrombi. Precision engineering is anticipated to minimize blood loss during the removal of organized venous thrombus. Strategic clinical trials are expected to validate the cost-effectiveness of mechanical methods over standard care. These technological milestones are positioned to sustain high growth rates across the acute intervention segment.

Rising Geriatric Populations and Chronic Vascular Disease Prevalence

Expanding elderly demographics are projected to drive clinical demand for effective venous clot management. Chronic conditions such as obesity and hypertension elevate systemic risks for vascular complications. Greater awareness of pulmonary embolism risks is expected to accelerate early-stage intervention across primary care. Enhanced diagnostic accuracy through ultrasound is positioned to improve patient identification within high-risk clinical groups. Healthcare providers are anticipated to prioritize preventative measures to reduce long-term hospitalization costs for patients. Growing surgical volumes are set to increase the utilization of prophylaxis across diverse therapeutic areas.

Standardized care protocols from Cardinal Health with Kendall SCD address rising prophylaxis requirements across clinical settings. These compression systems remain essential for preventing deep venus thrombosis in immobile patients. Integrated monitoring features from Enovis with VenaFlow Elite are expected to enhance patient adherence in home settings. Digital connectivity is projected to allow clinicians to track compression therapy effectiveness in real time. Advanced manufacturing will lower the price points for high-quality sequential compression garments. These factors are expected to maintain the leading position of the compression product segment.

Restraint Analysis – High Capital Costs Limiting Thrombectomy Device Adoption in Emerging Markets

Elevated upfront costs for mechanical thrombectomy systems deter procurement in resource-constrained facilities worldwide. Strategic pricing from Inari Medical’s FlowTriever is projected to remain a critical factor for adoption. Complex capital equipment demands substantial infrastructure investments for maintenance and training. Supply chain dependencies on specialized components inflate pricing amid global disruptions. These factors constrain access in mid-tier hospitals serving underserved populations. Hospital procurement teams are projected to demand rigorous cost-benefit analyses before approving new equipment. Pricing pressures are anticipated to impact the profit margins of manufacturers in competitive regional markets. Reimbursement gaps exacerbate financial pressures on providers evaluating upgrades. Structural barriers slow penetration into price-sensitive regions effectively.

Downstream impacts force manufacturers like Inari Medical’s FlowTriever and Stryker with Trevo to prioritize high-volume centers over broad distribution. Distributors face margin squeezes that limit inventory stocking in emerging hubs. End-users rationalize procedures to justify investments amid competing priorities. Boston Scientific, with AngioJet, faces similar hurdles in scaling beyond tier-1 facilities. Balanced strategies emphasize leasing models to mitigate adoption friction. Forward outlook requires cost optimizations to unlock latent demand volumes. Manufacturers are anticipated to develop tiered product offerings to address varying levels of affordability. These economic factors are expected to remain a primary restraint for the fastest-growing segments.

Opportunity Analysis – Expansion of Home-Based Post-Operative Thromboprophylaxis Solutions

Rising preference for home-based recovery significantly expands demand for portable venous thromboprophylaxis systems. Post-operative patients increasingly opt for domestic care settings following vascular and orthopedic interventions. Telehealth integration enables continuous remote monitoring of venous health during critical recovery phases. Advancements in lightweight, battery-powered compression devices enhance mobility and improve therapy adherence rates. Payers increasingly support home-based care models to reduce hospital readmissions and associated treatment costs. Regulatory frameworks gradually adapt to accommodate decentralized care delivery and remote therapeutic supervision. Technology democratization facilitates access to clinical-grade prophylaxis beyond traditional hospital environments. Care pathways evolve toward distributed models emphasizing patient autonomy and continuity of post-discharge management.

Innovations from Tactile Medical’s Flexitouch Plus and DJO Global VenaFlow Elite reflect segment transformation. These systems deliver clinical-grade compression therapy tailored for chronic venous insufficiency management. User-centric interface design enhances patient self-management and reduces dependency on clinical supervision. Wearable integration supports seamless incorporation of therapy into routine daily activities post-surgery. Digital connectivity enables data-driven monitoring, strengthening feedback loops between patients and providers. Distribution strategies increasingly incorporate direct-to-patient channels, reshaping traditional medical device logistics. Manufacturers align product development with evolving reimbursement structures, favoring outpatient recovery models.

Bioengineered Clot Dissolvers for Resistant VTE Cases

Drug-resistant thrombi present unmet needs for targeted enzymatic dissolvers in recurrent PE patients. Biotechnology advances enable precise delivery, minimizing systemic exposure risks. Workflow gaps in chronic cases drive R&D toward sustained-release formulations. Emerging policies incentivize orphan indications with accelerated pathways. These inflection points will unlock premium niches in refractory populations. High-margin potential attracts venture investments into novel agents.

Inari Medical’s ClotTriever and BTG with Ekos illustrate 2024 bioengineered adjuncts enhancing mechanical efficacy. Acquisitions by larger firms accelerate clinical progression for resistant subtypes. Vendor strategies emphasize combo-device approvals to broaden indications. Addressable dynamics are shifting toward personalized regimens in specialty centers. Opportunities amplify with genomic profiling for patient selection. Trajectory positions innovators for leadership in precision VTE management.

Category–wise Analysis

Product Analysis Insights

The compression system is expected to lead, accounting for approximately 36% share in 2026, underpinned by its essential role in long-term prophylaxis and non-invasive care. These systems continue to serve as the primary standard for preventing clot formation in post-surgical patients. Widespread adoption across both hospital and home settings is projected to sustain consistent revenue streams. Innovation from Cardinal Health with Kendall SCD is expected to improve the comfort and efficiency of sequential compression.

Integrated pressure sensors from Enovis with VenaFlow Elite are expected to ensure optimal therapeutic delivery for diverse patients. The low risk of complications associated with compression therapy is anticipated to maintain its dominance over invasive alternatives. Advanced fabric technologies are set to enhance the breathability and wearable ergonomics of compression garments.

Mechanical thrombectomy is projected to be the fastest-growing segment, driven by the emerging unmet need for rapid and complete clot removal in acute cases. This technology inflection point is projected to reduce the reliance on systemic thrombolytics that carry high bleeding risks. Surgeons are anticipated to adopt large-bore aspiration systems to treat massive pulmonary embolisms more effectively. Product upgrades from Inari Medical’s FlowTriever are expected to set new benchmarks for procedural speed and safety.

Enhanced aspiration algorithms from Penumbra with Indigo System are likely to optimize blood preservation during mechanical intervention. Clinical evidence favoring mechanical removal is projected to drive rapid adoption in high-volume trauma centers. Technological refinements are set to make these procedures safer for a wider range of patient demographics.

Disease Type Insights

Deep venous thrombosis (DVT) is projected to lead, accounting for approximately 66% share in 2026, anchored by the high global prevalence of lower limb venous obstructions. This segment is mostly to remain the primary focus of both prophylactic and therapeutic interventions worldwide. Increasing rates of obesity and sedentary lifestyles are expected to maintain a steady pipeline of patients. Therapeutic solutions from Bayer with Xarelto are anticipated to continue as a primary treatment for stable DVT cases.

Established guidelines anchor DVT protocols in multilayer prophylaxis strategies. Ecosystem dynamics favor devices with adjustable gradients for iliofemoral extensions. Specialized stenting from BD with Venovo Venous Stent is projected to address complex iliac vein compressions. Robust clinical protocols for DVT management are expected to ensure high utilization of both drugs and devices. The recurring nature of chronic venous conditions is likely to drive long-term market stability.

Pulmonary embolism (PE) is anticipated to be the fastest-growing segment, driven by a workflow gap in the management of life-threatening acute obstructions. Increased focus on early intervention is expected to shift clinical focus toward aggressive PE treatment strategies. Improved diagnostic imaging is expected to lead to higher detection rates of sub-massive pulmonary embolisms. Innovation from Inari Medical’s FlowTriever is projected to revolutionize the emergency treatment of clotted pulmonary arteries.

Catheter-directed therapies from Boston Scientific with EkoSonic enable precise thrombolysis using lower drug dosages. Rising mortality concerns associated with untreated PE are expected to accelerate the adoption of specialized tools. Hospital systems are set to establish dedicated PE response teams to improve survival rates. Product launches emphasize RV function recovery metrics. Vendors are focusing on training modules to bridge adoption hurdles in ICUs effectively.

Regional Insights

North America Venous Thromboembolism Treatment Market Trends

North America is expected to remain the leading regional market, accounting for approximately 40% share in 2026, supported by high healthcare spending and early adoption of advanced mechanical thrombectomy. The region benefits from a dense network of specialized vascular centers and academic research institutions. The region benefits from a dense network of specialized vascular centers and academic research institutions. Favorable reimbursement codes are projected to encourage the utilization of premium medical devices across major hospital systems.

Innovation from Inari Medical’s FlowTriever is expected to see the highest initial penetration within this sophisticated market. Strong clinical guidelines for VTE prophylaxis are expected to maintain high demand for compression systems. The presence of major industry players is projected to drive continuous technological upgrades and product launches.

The U.S is expected to serve as the primary regional anchor for North American market momentum. Robust FDA regulatory pathways are liable to facilitate the introduction of next-generation catheter systems. High prevalence of risk factors such as sedentary lifestyles is projected to sustain demand for venous care.

Strategic marketing from Penumbra with Indigo System is set to influence clinical standards across American trauma centers. Investment flows into digital health are prone to enhancing the integration of AI in VTE diagnostics. The U.S. healthcare system is projected to lead the transition toward value-based care in vascular medicine. These domestic factors are set to maintain the region's overall market leadership.

Asia Pacific Venous Thromboembolism Treatment Market Trends

Asia Pacific is expected to register the fastest growth trajectory, as rapid urbanization and healthcare modernization expand the addressable patient population. The region is expected to see rising surgical volumes and increasing demand for VTE prophylaxis. Expanding middle-class populations are seeking higher-quality care and advanced treatment options. Localization of supply chains is improving the availability of products from Cardinal Health with Kendall SCD. Government initiatives to upgrade rural healthcare are expected to create new markets for venous treatments. The region is set to become a major destination for medical tourism in the vascular specialty.

China is expected to be the specific regional anchor, driven by massive investments in medical infrastructure and a growing geriatric population. The domestic regulatory environment is expected to favor manufacturers who establish local production and R&D facilities. High rates of venous conditions in urban centers are projected to drive the demand for mechanical thrombectomy. Strategic expansion from Boston Scientific with AngioJet mostly target the expanding network of Tier 1 and Tier 2 hospitals.

Increased awareness of vascular health is expected to lead to earlier diagnosis and treatment of VTE. Chinese technological firms are projected to partner with global leaders to enhance digital venous care solutions.

Europe Venous Thromboembolism Treatment Market Trends

Europe is expected to remain a mature and structurally stable regional market, approximating a significant share, with demand primarily anchored in established clinical protocols and replacement cycles. Stringent regulatory standards under MDR are projected to prioritize patient safety and long-term clinical efficacy. Pharmaceutical leadership from Bayer with Xarelto is expected to maintain a strong presence in the outpatient DVT segment. Public healthcare systems are poised to drive the adoption of cost-effective compression solutions for prophylaxis. Premiumization of venous care is anticipated to occur in high-income Western European nations.

Germany is expected to shape the regional momentum as a hub for vascular research and high-tech manufacturing. Regulatory clarity is projected to foster a stable environment for new medical device launches. Strategic presence of B. Braun with VenaTech Filter reflects the focus on high-quality surgical components. Robust insurance coverage is expected to ensure broad patient access to the latest venous treatment modalities. German clinical trials are likely to provide critical data for expanding VTE therapy applications across Europe. These factors are set to sustain the country's position as a regional anchor.

Competitive Landscape

The venous thromboembolism treatment market shows strong consolidation among leading device and pharmaceutical players. Market leaders sustain dominance through robust patent portfolios and established hospital procurement relationships. Competitive influence depends on offering integrated portfolios across prophylaxis and acute intervention solutions. Inari Medical’s FlowTriever sets performance benchmarks for mechanical thrombectomy systems. Firms build competitive moats using clinical evidence and structured physician training initiatives.

Competition is shifting toward vertical integration across comprehensive venous care solution ecosystems. Premium innovators focus on high-margin mechanical systems, while value players target compression segments. Boston Scientific, with AngioJet, expands capabilities through targeted acquisition strategies. Differentiation emerges through specialized catheter designs addressing complex anatomical treatment challenges. Tactile Medical with Flexitouch Plus strengthens positioning in home care therapy markets. Partnerships between device manufacturers and AI software firms are increasing across the value chain.

Key Industry Developments:

- In February 2026, Medtronic announced its intent to acquire CathWorks to expand its interventional cardiovascular pipeline. This strategic move bolsters Medtronic’s diagnostic and procedural capabilities for complex vascular conditions, including those underlying VTE risks.

- In February 2026, Bayer AG reported Phase III results showing its Factor XIa inhibitor, asundexian, reduced secondary stroke risk by 26% without increasing major bleeding. Although studied in stroke, these findings validate the Factor XIa pathway as a promising approach for safer, long-term anticoagulation in the VTE market, with potential to improve efficacy–safety balance versus current therapies such as apixaban and enoxaparin.

Companies Covered in Venous Thromboembolism Treatment Market

- Boston Scientific Corporation

- Penumbra, Inc.

- Inari Medical, Inc.

- Medtronic plc

- Stryker Corporation

- Johnson & Johnson

- Cardinal Health, Inc.

- Terumo Corporation

- Philips Healthcare

- Bayer AG

- Bristol Myers Squibb

- Pfizer Inc.

- Becton, Dickinson and Company

- B. Braun Melsungen AG

- Tactile Medical

- Enovis

Frequently Asked Questions

The main treatments include anticoagulant medications (such as heparin and warfarin), and newer Direct Oral Anticoagulants (DOACs) like rivaroxaban and apixaban, which simplify treatment with fixed dosing and minimal monitoring requirements.

Factors driving market growth include increasing awareness, advancements in treatment options, rising prevalence of risk factors, and supportive healthcare policies.

Innovations include personalized medicine approaches, advancements in diagnostic techniques, and ongoing research into new anticoagulant therapies.

Future trends include continued technological advancements, and the increased regulatory focus.

North America to account for the significant share in the market.