- Medical Devices

- Intravenous Solutions Market

Intravenous Solutions Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Intravenous Solutions Market by Type (Total Parenteral Nutrition and Peripheral Parenteral Nutrition), by Composition (Carbohydrates, Vitamins and Minerals, Single-dose Amino Acids, Parenteral Lipid Emulsion, and Others), by Application (Nutritional Support, Blood Transfusion, Fluid and Electrolyte Balance, and Others) by End User (Clinical Laboratories, Academic & Research Institutes, Pharmaceutical & Biotechnology Companies, and Contract Research Organizations (CRO's)), and Regional Analysis from 2026 to 2033

Intravenous Solutions Market Share and Trend Analysis

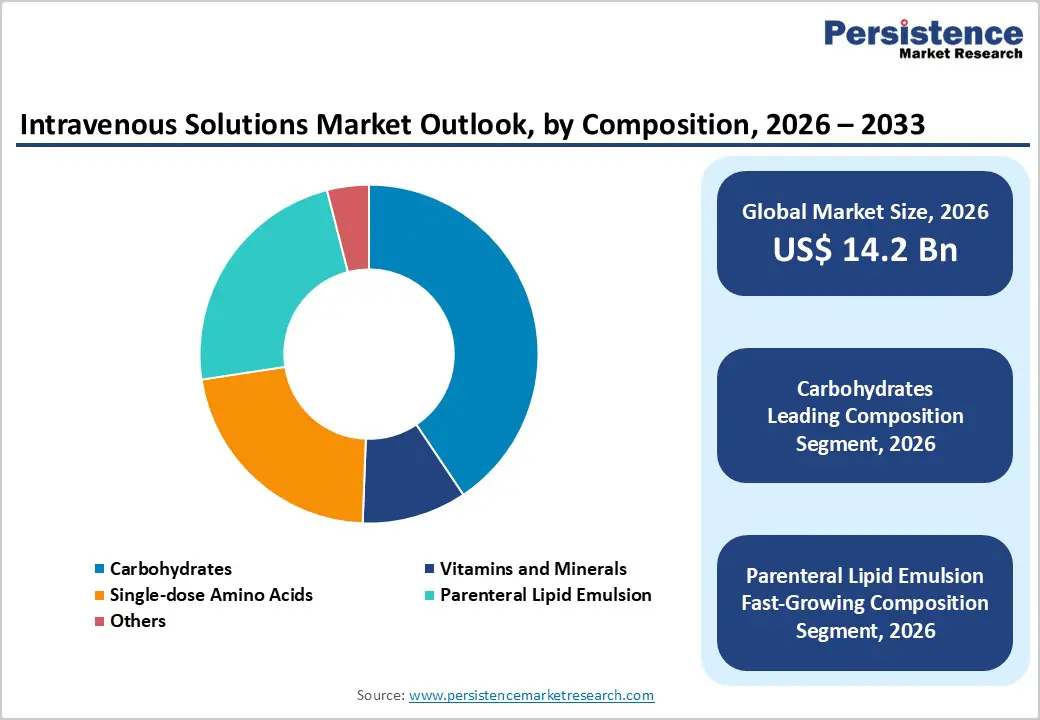

The global intravenous solutions market size is estimated to grow from US$ 14.2 Bn in 2026 to US$ 23.3 Bn by 2033. The market is projected to record a CAGR of 5.5% during the forecast period from 2026 to 2033.

Global demand for intravenous solutions is increasing steadily, driven by rising hospital admissions, expanding surgical procedures, and growing reliance on intravenous therapy for fluid management, nutritional support, and drug delivery. Increasing prevalence of chronic diseases, trauma cases, and critical care requirements is supporting sustained market growth across both developed and emerging healthcare systems. Higher volumes of inpatient treatments, intensive care utilization, and long-term management of malnutrition and dehydration, coupled with rising healthcare expenditure, are further accelerating demand. Continuous improvements in formulation stability, sterility assurance, and ready-to-use packaging are enhancing safety, ease of administration, and clinical efficiency. In addition, growing adoption of home infusion therapy, outpatient care models, and infection-prevention-focused IV systems is further propelling the global intravenous solutions market.

Key Industry Highlights

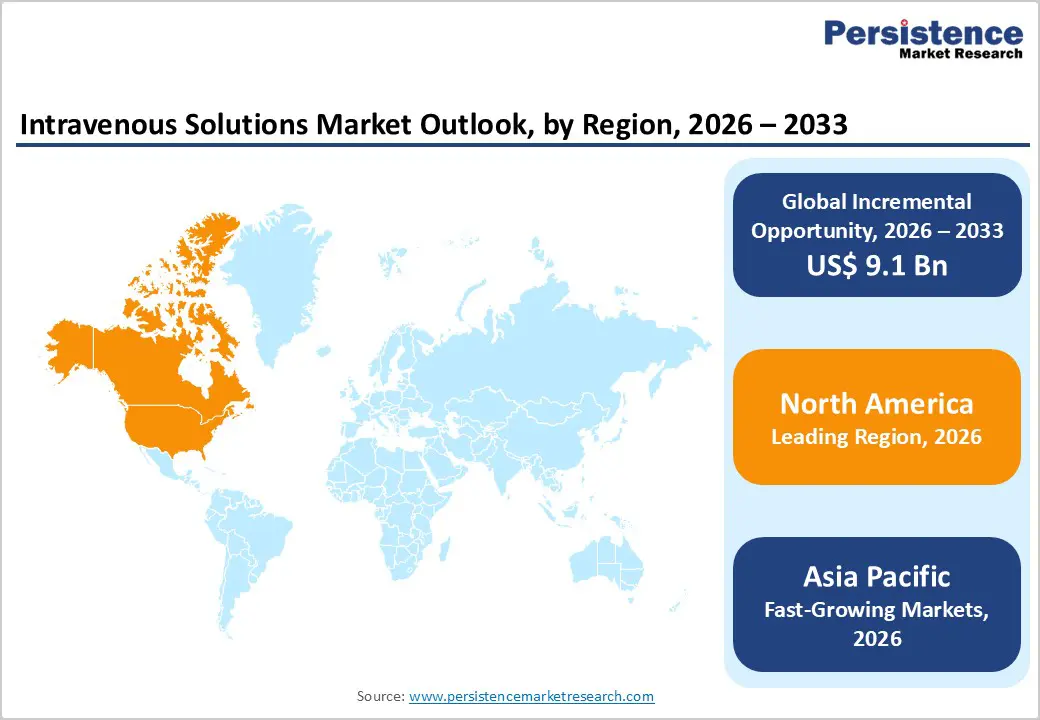

- Leading Region: North America holds the largest share at 46.7%, supported by advanced healthcare infrastructure, high hospitalization rates, strong adoption of standardized IV therapy protocols, and the presence of major intravenous solution manufacturers.

- Fastest-Growing Region: Asia Pacific is expanding fastest due to rapid hospital infrastructure development, rising surgical volumes, increasing chronic disease burden, and growing healthcare investments by governments.

- Leading Type Segment: Total parenteral nutrition dominates the market due to its recurring and long-term use in critically ill, oncology, neonatal, and post-surgical patients requiring comprehensive intravenous nutritional support.

- Fastest-Growing Type Segment: Peripheral parenteral nutrition is expanding rapidly as demand increases for short-term, lower-intensity intravenous nutrition in outpatient, step-down, and home care settings.

- Leading Application Segment: Nutritional support remains the top application, driven by widespread use of intravenous nutrition for malnourished, critically ill, and gastrointestinal-compromised patients.

- Fastest-Growing Application Segment: Fluid and electrolyte balance is scaling quickly as hospitals and emergency care facilities increasingly rely on IV solutions for rapid stabilization, dehydration management, and perioperative care.

| Key Insights | Details |

|---|---|

| Intravenous Solutions Market Size (2026E) | US$ 14.2 Bn |

| Market Value Forecast (2033F) | US$ 23.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.3% |

Market Dynamics

Driver – Rising Hospitalization Rates and Increasing Dependence on Intravenous Therapy in Acute and Chronic Care

Growth is primarily supported by the increasing reliance on intravenous solutions as a frontline therapy across hospitals, emergency departments, and long-term care settings. IV solutions are essential for rapid fluid resuscitation, electrolyte correction, nutritional supplementation, and drug delivery in patients unable to tolerate oral administration. The global rise in chronic diseases such as cancer, diabetes, renal disorders, and gastrointestinal conditions has significantly expanded the patient pool requiring prolonged IV therapy. In parallel, growing surgical volumes, trauma cases, and intensive care admissions are driving consistent demand for crystalloid solutions, parenteral nutrition, and blood-compatible fluids.

Aging populations further amplify this trend, as elderly patients frequently require hydration management, electrolyte stabilization, and nutritional support during hospitalization and recovery. Advances in clinical protocols emphasizing early intervention, perioperative fluid optimization, and critical care management continue to reinforce routine IV usage. Additionally, increasing access to healthcare services in emerging economies is leading to higher hospital admissions and procedural volumes, directly supporting market expansion. Together, these factors position intravenous solutions as indispensable components of modern medical care, sustaining steady long-term demand.

Restraints – Cost Pressures, Supply Chain Vulnerability, and Stringent Quality Requirements

Market expansion is moderated by persistent pricing pressure and operational challenges associated with manufacturing and distributing sterile intravenous solutions. IV products are often categorized as essential commodities, limiting pricing flexibility despite rising raw material, energy, and transportation costs. Manufacturers must comply with stringent regulatory standards related to sterility assurance, contamination control, and packaging integrity, increasing production complexity and capital requirements. Any deviation from quality norms can result in recalls, shortages, or regulatory action, posing reputational and financial risks.

In addition, the market has historically faced supply disruptions due to manufacturing shutdowns, natural disasters, and geopolitical factors, highlighting vulnerabilities in global supply chains. Hospitals and healthcare systems increasingly demand uninterrupted availability, placing additional pressure on suppliers to maintain redundancy and inventory buffers. Cost containment initiatives by healthcare providers and group purchasing organizations further restrict margin expansion. In developing regions, limited cold-chain infrastructure and distribution inefficiencies can affect product stability and access. Collectively, these economic, regulatory, and logistical challenges constrain profitability and create barriers for smaller or new market entrants.

Opportunity – Expansion of Home Infusion Therapy, Ready-to-Use Formulations, and Emerging Healthcare Markets

Significant growth opportunities are emerging from the shift toward outpatient care and home-based infusion therapy. As healthcare systems aim to reduce hospital stays and overall treatment costs, demand for intravenous solutions suitable for home administration is increasing, particularly for parenteral nutrition, hydration therapy, and long-term medication delivery. This trend is driving innovation in ready-to-use, pre-mixed, and closed-system IV formulations that enhance safety, convenience, and ease of administration. Technological improvements in packaging, such as multi-chamber bags and extended shelf-life solutions, are further supporting adoption beyond traditional hospital settings. Emerging economies represent another major opportunity, as governments invest in hospital infrastructure, emergency care capacity, and universal healthcare coverage.

Rising awareness of clinical nutrition and critical care standards in these regions is expanding the addressable market. Additionally, increasing focus on patient safety and infection prevention is accelerating demand for advanced IV delivery systems and contamination-resistant solutions. As manufacturing capabilities expand and cost efficiencies improve, suppliers are well positioned to capture incremental demand across both developed and developing healthcare markets.

Category-wise Analysis

By Type, Total Parenteral Nutrition Leads Due to Continuous Use in Critical and Long-Term Care Settings

The total parenteral nutrition (TPN) segment is projected to dominate the global intravenous solutions market in 2026, accounting for a revenue share of 65.1%. This dominance is driven by its extensive and recurring use in critically ill patients who are unable to meet nutritional requirements through oral or enteral routes. TPN is widely administered in intensive care units, oncology wards, neonatal care, and post-surgical recovery, where comprehensive nutrient delivery is essential over prolonged treatment durations.

Unlike peripheral parenteral nutrition, TPN supports higher caloric and nutrient concentrations, resulting in greater solution volumes and higher per-patient consumption. Rising prevalence of cancer, gastrointestinal disorders, premature births, and severe trauma cases is further increasing demand. In addition, longer hospital stays, aging populations, and growing adoption of standardized nutrition protocols continue to reinforce sustained utilization of TPN, supporting its leadership within the intravenous solutions market.

By Application, Nutritional Support Leads Due to High Dependency in Hospitalized and Chronically Ill Patients

The nutritional support segment is expected to dominate the global intravenous solutions market in 2026, accounting for a revenue share of 55.6%. This leadership is primarily attributed to the widespread reliance on IV nutrition for patients with impaired gastrointestinal function, severe malnutrition, cancer-related cachexia, and post-operative recovery needs. Intravenous nutritional solutions are routinely used in ICUs, oncology departments, and neonatal units, where enteral feeding is contraindicated or insufficient.

Increasing surgical volumes, rising incidence of chronic illnesses, and extended hospitalizations are significantly driving demand. Moreover, advancements in lipid emulsions, amino acid formulations, and micronutrient blends have improved safety and efficacy, encouraging broader clinical adoption. The growing use of parenteral nutrition in home care settings for long-term patients further supports segment expansion. Collectively, these factors ensure nutritional support remains the most revenue-generating application segment.

By End User, Hospitals Lead Due to High Patient Footfall and Intensive IV Therapy Utilization

The hospitals segment is projected to dominate the global intravenous solutions market in 2026, accounting for a revenue share of 70.2%. Hospitals remain the primary point of care for acute, critical, and surgical patients requiring intravenous fluid management, nutritional support, blood transfusions, and electrolyte correction. High admission rates for trauma, cancer, cardiovascular disorders, and infectious diseases result in consistent and large-scale consumption of IV solutions.

In addition, hospitals are central hubs for complex surgeries, intensive care services, and emergency treatments, all of which rely heavily on continuous IV administration. The presence of specialized departments, advanced infrastructure, and trained clinical staff enables higher utilization volumes compared to outpatient settings. Furthermore, public and private hospital expansion, especially in emerging economies, along with increasing healthcare expenditure, continues to reinforce hospitals as the dominant end-user segment.

Region-wise Insights

North America Intravenous Solutions Market Trends

North America is expected to dominate the global intravenous solutions market with a value share of 46.7% in 2026, led primarily by the United States. The region benefits from a highly developed healthcare infrastructure, high hospital admission rates, and widespread adoption of advanced clinical care protocols. A strong prevalence of chronic diseases such as cancer, diabetes, and cardiovascular disorders drives sustained demand for IV fluids, parenteral nutrition, and electrolyte solutions. North America also records a high volume of surgical procedures, trauma cases, and critical care admissions, all of which significantly contribute to IV solution consumption.

Favorable reimbursement frameworks and standardized treatment guidelines support consistent utilization across hospitals and specialty clinics. In addition, the growing aging population increases dependency on long-term intravenous nutritional and fluid management therapies. Strong presence of leading manufacturers, continuous product innovation, and emphasis on patient safety, including ready-to-use and contamination-resistant formulations, further strengthen the region’s market leadership.

Europe Intravenous Solutions Market Trends

The Europe intravenous solutions market is expected to grow steadily, supported by well-established public healthcare systems, an aging population, and rising burden of chronic and degenerative diseases. Countries such as Germany, the U.K., France, Italy, and the Nordic nations exhibit strong demand for intravenous fluids and parenteral nutrition across hospitals and long-term care facilities. Increasing incidence of cancer, gastrointestinal disorders, and neurological conditions is driving the need for sustained IV nutritional and electrolyte support.

Europe also demonstrates high adherence to clinical guidelines and safety standards, encouraging the use of high-quality, regulated IV formulations. Government-funded healthcare systems ensure broad patient access, contributing to consistent market demand. In addition, growing focus on reducing hospital-acquired infections is promoting adoption of ready-to-administer and closed-system IV solutions. Expansion of home healthcare services and outpatient infusion programs further supports market growth across the region.

Asia Pacific Intravenous Solutions Market Trends

The Asia Pacific intravenous solutions market is expected to register a relatively higher CAGR of around 7.9% between 2026 and 2033, driven by rapid healthcare infrastructure development and rising patient volumes. Large populations, increasing incidence of chronic diseases, malnutrition, and trauma cases across China, India, Japan, and Southeast Asia are significantly boosting demand for IV fluids and parenteral nutrition. Governments in the region are investing heavily in hospital expansion, emergency care capacity, and critical care services, directly supporting market growth.

Rising medical tourism, particularly in India and Thailand, is further increasing consumption of intravenous solutions. Cost-sensitive markets are encouraging local manufacturing and adoption of affordable IV formulations. Additionally, improving access to healthcare services in rural and semi-urban areas is expanding patient reach. Growing awareness of clinical nutrition and increasing adoption of home infusion therapies are expected to sustain long-term growth across Asia Pacific.

Market Competitive Landscape

The global intravenous solutions market is highly competitive, with strong participation from companies such as AdvaCare Pharma, Amanta Healthcare, Axa Parenterals, B. Braun SE, and Baxter International. These players leverage extensive global manufacturing and distribution networks, strong brand equity, and continuous product innovation across parenteral nutrition, electrolyte solutions, and sterile fluid formulations to address a wide range of acute, chronic, and critical care requirements.

Rising demand for hospital-based treatments, surgical procedures, chronic disease management, and nutritional support, along with the growing shift toward outpatient and home infusion therapies, is driving portfolio expansion and product differentiation. Manufacturers are increasingly focusing on ready-to-use formulations, improved sterility and packaging safety, cost-efficient production, and extended shelf-life solutions. Strategic priorities include strengthening partnerships with hospitals and healthcare providers, expanding penetration in emerging healthcare markets, and investing in R&D to support advanced IV formulations and sustain long-term market growth.

Key Industry Developments:

- In November 2024, Baxter International announced the release of its first 1-liter intravenous solution products manufactured following the hurricane at its North Cove, North Carolina facility. The company noted that the restart occurred earlier than initially anticipated, reflecting the strong commitment and resilience of the North Cove workforce and Baxter’s broader teams.

Companies Covered in Intravenous Solutions Market

- AdvaCare Pharma

- Amanta Healthcare

- Axa Parenterals

- B. Braun SE

- Baxter International

- Fresenius Kabi

- Grifols

- ICU Medical

- JW Life Science

- Otsuka Pharmaceutical

- Sino-Swed Pharmaceutical Corp., Ltd

- Hospira

- Amanta Healthcare

- Terumo Corporation

- Others

Frequently Asked Questions

The global intravenous solutions market is projected to be valued at US$ 14.2 Bn in 2026.

The global intravenous solutions market is driven by rising hospitalizations, increasing surgical procedures, growing chronic disease burden, and expanding use of IV therapy in critical and long-term care.

The global intravenous solutions market is poised to witness a CAGR of 5.8% between 2026 and 2033.

Key opportunities lie in the expansion of home-based infusion therapy, demand for ready-to-use and customized IV formulations, and rapid healthcare infrastructure growth in emerging markets.

AdvaCare Pharma, Amanta Healthcare, Axa Parenterals, B. Braun SE, Baxter International. are some of the key players in the intravenous solutions market.