- Processed Food

- Vegan Belgian Chocolate Market

Vegan Belgian Chocolate Market Size, Share, and Growth Forecast, 2026 - 2033

Vegan Belgian Chocolate Market by Product Type (Dark Chocolates, Milk Chocolates), Packaging Type (Boxed, Bagged, Foil Wrapped, Bulk Packaging), End-user (Food Processing Industry, Food Service Industry, Retail/Household), and Regional Analysis for 2026 - 2033

Vegan Belgian Chocolate Market Size and Trends Analysis

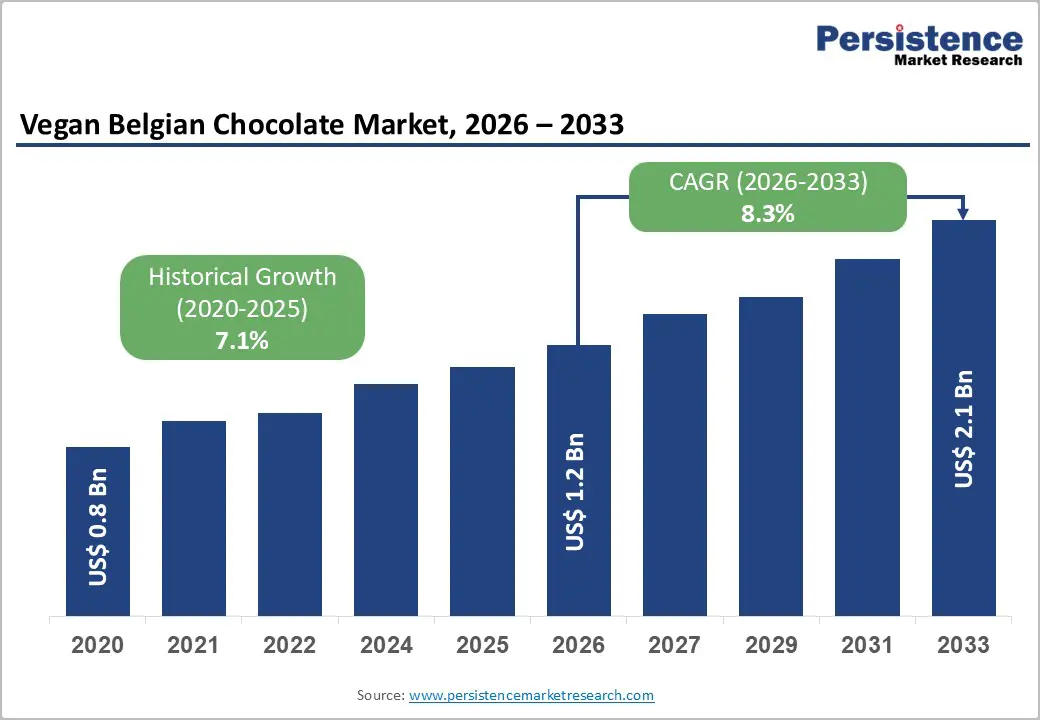

The global vegan Belgian chocolate market size is likely to be valued at US$1.2 billion in 2026, and is expected to reach US$2.1 billion by 2033, growing at a CAGR of 8.3% during the forecast period from 2026 to 2033, driven by rising vegan population, increasing demand for premium plant-based confectionery, and Belgium’s strong reputation for high-quality chocolate.

Increasing consumer preference for dairy-free, ethical, and indulgent Belgian chocolate remains a major driver of the vegan Belgian chocolate market growth.

Key Industry Highlights:

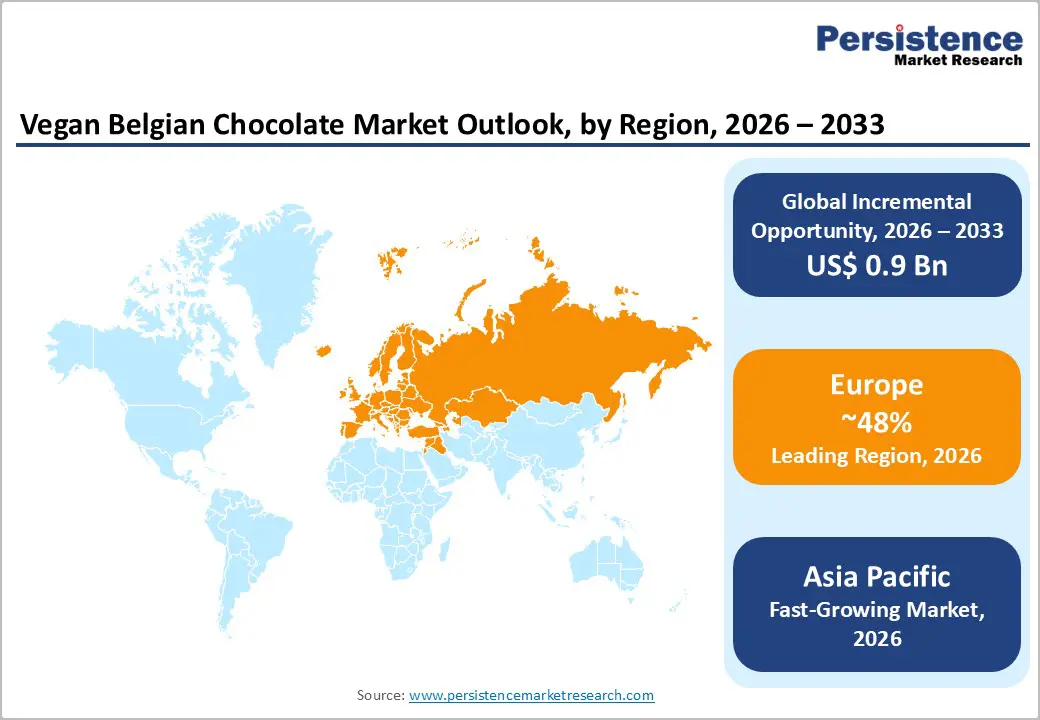

- Leading Region: Europe, anticipated to account for a 48% market share in 2026, driven by strong vegan awareness and traditional chocolate expertise in Belgium.

- Fastest-growing Region: Asia Pacific, fueled by rising vegan adoption and premium chocolate demand in China and India.

- Dominant Product Type: Dark chocolates, to hold approximately 65% of the market share, due to natural vegan compatibility and rich flavor.

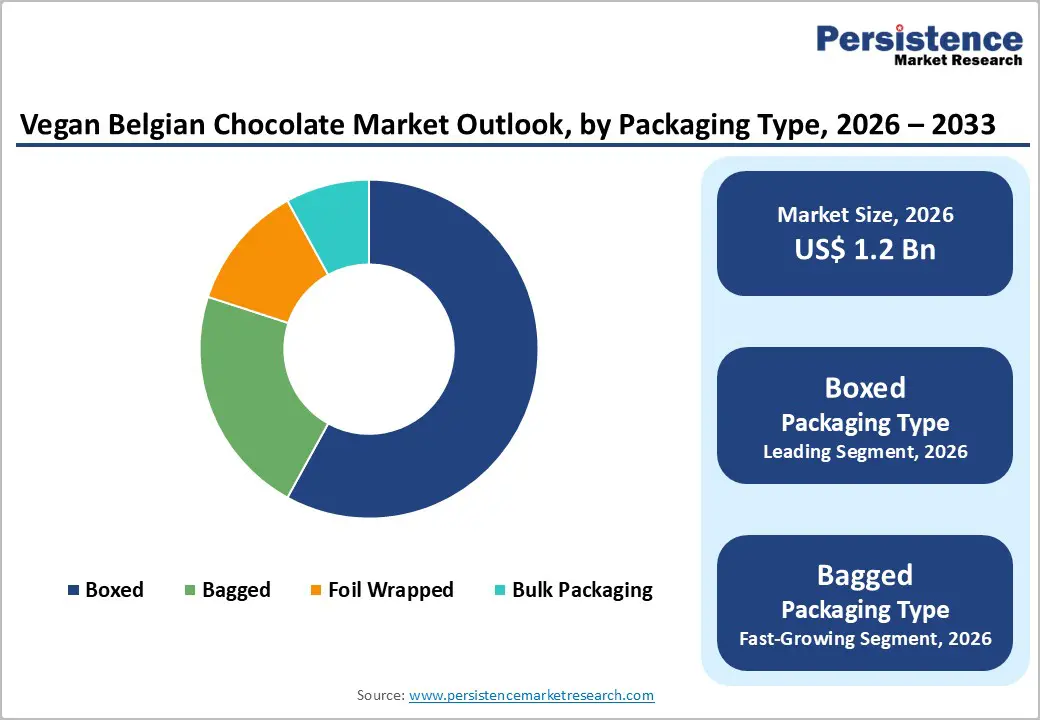

- Leading Packaging Type: Boxed is expected to dominate with 60% share in 2026, for gifting and premium presentation.

| Key Insights | Details |

|---|---|

| Vegan Belgian Chocolate Market Size (2026E) | US$1.2 Bn |

| Market Value Forecast (2033F) | US$2.1 Bn |

| Projected Growth CAGR (2026 - 2033) | 8.3% |

| Historical Market Growth (2020 - 2025) | 7.1% |

DRO Analysis

Driver Analysis - Rising Vegan and Plant-Based Diet Adoption

Consumer eating habits are shifting toward plant-based lifestyles due to growing awareness of health, environmental sustainability, and animal welfare. Many individuals are reducing or eliminating animal-derived products in favor of plant-based alternatives that are perceived as healthier and more ethically produced. Diets rich in plant ingredients are often associated with lower risks of chronic conditions such as heart disease, obesity, and diabetes, which further encourages adoption.

Environmental concerns also play a significant role, as plant-based diets generally require fewer natural resources and generate lower greenhouse gas emissions compared to traditional animal-based food systems. This aligns with the preferences of environmentally conscious consumers who seek to minimize their ecological footprint. The increasing availability and variety of plant-based products, including dairy-free chocolates, meat substitutes, and functional snacks, have made the transition easier and more appealing. Food manufacturers are continuously innovating to improve taste, texture, and nutritional value, reducing the gap between conventional and plant-based options.

Innovation in Flavors and Product Offerings

Manufacturers are moving beyond traditional flavor profiles by introducing combinations such as sea salt caramel, chili-infused chocolate, berry blends, and exotic fruit infusions. These unique offerings cater to evolving consumer preferences for indulgent yet distinctive experiences, helping brands stand out in a competitive landscape.

In addition to flavor diversity, product innovation is expanding into various formats, including snack bars, spreads, filled chocolates, ready-to-eat desserts, and functional treats enriched with nutrients. This variety allows consumers to choose products that align with their lifestyles, whether for convenience, health benefits, or occasional indulgence. Texture enhancement has also become a focus area, with improvements designed to closely replicate or even surpass traditional counterparts. Premiumization is another key aspect, with companies emphasizing high-quality ingredients, clean-label formulations, and artisanal production techniques. Limited-edition and seasonal launches further drive consumer excitement and repeat purchases. Moreover, brands are increasingly incorporating global culinary influences to attract adventurous consumers seeking novel taste experiences.

Restraint Analysis - High Product Costs

Elevated pricing remains a significant barrier to wider adoption, particularly in price-sensitive markets. Plant-based and specialty food products often require high-quality raw materials such as cocoa alternatives, nut-based ingredients, and natural sweeteners, which are typically more expensive than conventional inputs. Smaller production scales and limited supply chains contribute to higher manufacturing and distribution costs.

Advanced processing techniques and continuous product innovation further increase overall expenses, as companies invest in research, formulation, and quality improvement to meet consumer expectations. Packaging and certification requirements, including organic or vegan labeling, can also add to the final price.

Limited Consumer Awareness

A lack of widespread understanding about plant-based and specialty products continues to hinder their adoption across many regions. Many consumers remain unfamiliar with the ingredients, nutritional benefits, and taste profiles of these alternatives, which creates hesitation in trying them. Misconceptions about flavor, quality, or effectiveness compared to traditional products further contribute to this gap.

In several markets, limited marketing reach and inadequate product visibility in retail channels reduce exposure, especially in smaller cities and rural areas. Without clear communication and education, potential buyers may not fully recognize the value or suitability of these offerings for their dietary needs.

Opportunity Analysis - Rising Global Vegan Population

The number of individuals adopting vegan lifestyles has been steadily increasing across both developed and emerging regions, driven by a combination of health, ethical, and environmental motivations. People are becoming more conscious of the impact of their food choices on personal well-being, leading many to eliminate animal-derived products in favor of plant-based alternatives. Concerns about animal welfare have also encouraged a shift toward cruelty-free consumption patterns.

Environmental awareness is another major factor, as individuals recognize the role of food systems in climate change, resource depletion, and biodiversity loss. Choosing plant-based diets is often seen as a practical step toward reducing one’s environmental footprint. This shift is further supported by growing access to information through digital platforms, documentaries, and social media, which amplify awareness and influence dietary decisions. Urbanization and changing lifestyles have also contributed to this trend, with younger consumers showing a stronger inclination toward sustainable and ethical consumption. Food companies and restaurants are responding by expanding vegan options, making such diets more accessible and appealing.

Product Innovation and Diversification

Continuous development of new products and expansion across categories are reshaping the competitive landscape, particularly in the plant-based and specialty food sectors. Companies are introducing a wide range of offerings, from confectionery and beverages to snacks and ready-to-eat meals, ensuring they cater to diverse consumer preferences and consumption occasions. This broad portfolio approach helps brands reach multiple target segments, including health-conscious consumers, flexitarians, and those seeking convenient food options.

Innovation is also evident in ingredient selection and formulation, with manufacturers exploring alternatives such as plant-based proteins, natural sweeteners, and functional additives that enhance nutritional value. Efforts to improve taste, texture, and shelf life are making these products more comparable to traditional options, thereby increasing consumer acceptance. Diversification further extends to packaging formats and portion sizes, allowing for better convenience and on-the-go consumption. Companies are also experimenting with region-specific flavors and culturally relevant offerings to strengthen market penetration in different geographies.

Category-wise Analysis

Product Type Insights

Dark chocolates are anticipated to dominate and be the fastest-growing, accounting for 65% of the share in 2026, due to their strong appeal among health-conscious consumers. They are often perceived as a healthier alternative to milk chocolates, as they typically contain higher cocoa content and lower sugar levels. This aligns with the increasing demand for clean-label and functional indulgence products.

Dark chocolate pairs well with innovative flavors such as fruits, nuts, and spices, enhancing its popularity. Lindt EXCELLENCE 90% Cocoa Dark Chocolate highlights how brands are focusing on higher cocoa content and minimal ingredients to meet evolving consumer demand for healthier indulgence. Products with higher cocoa percentages are preferred due to their lower sugar content and higher antioxidant levels, making them more attractive to wellness-focused buyers.

End-user Industry

Retail/household is anticipated to dominate with over 55% share in 2026, due to surging consumer demand for plant-based indulgences. Health-conscious flexitarians and vegans prioritize clean-label products such as dairy-free dark chocolate, driving sales through supermarkets, specialty stores, and e-commerce platforms. In Belgium, premium positioning amplifies this, as households stock up on convenient, ethically sourced treats amid rising vegan adoption. Barry Callebaut, a leading Belgian chocolate manufacturer, introduced its Plant Craft dairy-free chocolate range and launched online retail pop-up stores to directly engage household consumers. This initiative highlights the rising trend of at-home consumption of plant-based indulgent products.

The food service segment is likely to be the fastest growing due to shifting consumer lifestyles and increasing demand for convenience. Rapid urbanization and busy work schedules are encouraging people to eat out more frequently or rely on ready-to-eat meals. The expansion of quick-service restaurants, cafés, and cloud kitchens has significantly improved accessibility and variety. The rise of online food delivery platforms has made ordering food easier than ever. Green & Black’s, partnered with Moo Free in 2025 to develop premium vegan chocolate offerings, aiming to expand their presence across both retail and food service channels.

Regional Insights

North America Vegan Belgian Chocolate Market Trends

North America is experiencing a refined shift in vegan Belgian chocolate consumption, shaped by premium preferences and evolving taste expectations. Consumers are increasingly drawn to high-cocoa, low-sugar formulations, as dark chocolate naturally aligns with vegan requirements while offering a richer taste profile. This has encouraged brands to highlight cocoa origin, bean quality, and artisanal craftsmanship to differentiate their offerings.

There is a growing demand for clean-label indulgence, where buyers actively check for simple ingredient lists, absence of artificial additives, and use of natural sweeteners. Many consumers are also showing interest in chocolates made with alternative plant-based ingredients such as oat milk, almond butter, or coconut cream, enhancing both texture and flavor complexity. Another notable development is the shift toward experiential consumption, where packaging, storytelling, and brand identity play a key role. Premium boxed assortments and limited-edition flavors inspired by global cuisines are gaining popularity, especially during festive and gifting occasions. Retail dynamics are also evolving, with specialty stores and online platforms offering curated vegan chocolate selections.

Europe Vegan Belgian Chocolate Market Trends

Europe is projected to dominate, accounting for 48% of the share in 2026, supported by its deep-rooted chocolate heritage and strong consumer preference for premium confectionery. Countries such as Belgium, Germany, the U.K., and France play a central role, where demand is driven by a combination of tradition and evolving dietary choices.

Europe places a strong emphasis on authenticity and craftsmanship, with consumers valuing chocolates that reflect traditional Belgian techniques while incorporating plant-based ingredients. Many manufacturers are reformulating classic recipes using alternatives like oat, almond, and hazelnut milk to maintain taste and texture without dairy. European consumers are highly conscious of fair-trade cocoa, environmentally friendly packaging, and transparent supply chains, which significantly influence purchasing decisions. The region is also witnessing growth in premium and artisanal product segments, including organic, single-origin, and limited-edition vegan chocolates.

Asia Pacific Vegan Belgian Chocolate Market Trends

Asia Pacific is the fastest-growing region, driven by shifting urban lifestyles and evolving taste preferences. A distinctive trend is the fusion of Western premium chocolate with local flavors, where products incorporate ingredients such as matcha, yuzu, coconut, mango, and spices to appeal to regional palates. This localization strategy is helping brands bridge the gap between traditional Belgian chocolate and Asian consumer expectations.

Unique development is the rise of “light indulgence” consumption, where consumers prefer smaller portion sizes with reduced sugar and cleaner ingredient profiles. Instead of bulk purchases, there is a growing demand for mini packs and individually wrapped pieces suited for controlled consumption and gifting. The region is also seeing increased traction in travel retail and premium gifting channels, particularly in countries, including Japan, South Korea, and Singapore, where aesthetically appealing packaging and brand storytelling play a crucial role in purchase decisions. Seasonal gifting culture further supports demand for premium boxed vegan chocolates. Digital influence is especially strong, with social media and e-commerce platforms driving the discovery of niche and imported brands.

Competitive Landscape

The global vegan Belgian chocolate market includes a mix of traditional Belgian chocolatiers and large multinational companies, each leveraging distinct strengths to expand their presence. Key players such as Belgian Chocolate Brand, Belvas, Nestlé, Bruyerre Chocolates SA, Galler, and Ferrero Group play a significant role in shaping market dynamics. Traditional brands like Belvas, Bruyerre, and Galler focus on authentic Belgian craftsmanship, emphasizing organic ingredients, fair-trade cocoa, and artisanal production methods. Their offerings are often positioned in the premium segment, appealing to consumers who value quality, transparency, and ethical sourcing.

Global players such as Nestlé and Ferrero Rocher capitalize on strong brand recognition, extensive distribution networks, and continuous product innovation. These companies are expanding their vegan product lines while maintaining premium appeal through attractive packaging and diverse flavor options. Competition within the market is driven by a combination of heritage, innovation, and sustainability, with companies striving to balance traditional taste with modern consumer preferences.

Key Industry Developments:

- In May 2023, Barry Callebaut launched Callebaut NXT (plant-based chocolate) and SICAO Zero (sugar-free chocolate) in Mexico, expanding its better-for-you portfolio and targeting rising demand for vegan and low-sugar options.

Companies Covered in Vegan Belgian Chocolate Market

- The Belgian

- Belvas

- Nestlé

- Bruyerre Chocolates SA

- Galler

- Ferrero Group

- Barry Callebaut

- Leonidas

- Neuhaus

Frequently Asked Questions

The global vegan Belgian chocolate market is projected to reach US$1.2 billion in 2026.

Consumer eating habits are shifting toward plant-based diets driven by health benefits, environmental concerns, and ethical considerations, with many opting for alternatives perceived as healthier and more sustainable.

The vegan Belgian chocolate market is poised to witness a CAGR of 8.3% from 2026 to 2033.

The global vegan population is rising as consumers increasingly adopt plant-based lifestyles driven by health, environmental awareness, and animal welfare concerns.

Key players in the vegan Belgian chocolate market include Belvas, Bruyerre Chocolates SA, Galler, Barry Callebaut, and Nestlé.