- Display Technologies

- Transparent Display Market

Transparent Display Market Size, Trends, Share, and Growth Forecast, 2026 - 2033

Transparent Display Market by Solution (Transparent Display Software and Services), by Deployment Mode (Cloud-based and On-premises, by Organization Size (Large Enterprises and SMEs), by End- use (Healthcare, IT & Telecommunication, BFSI, Manufacturing, Retail, Aerospace & Defense and Others) and Regional Analysis for 2026 - 2033

Transparent Display Market Size and Trends Analysis

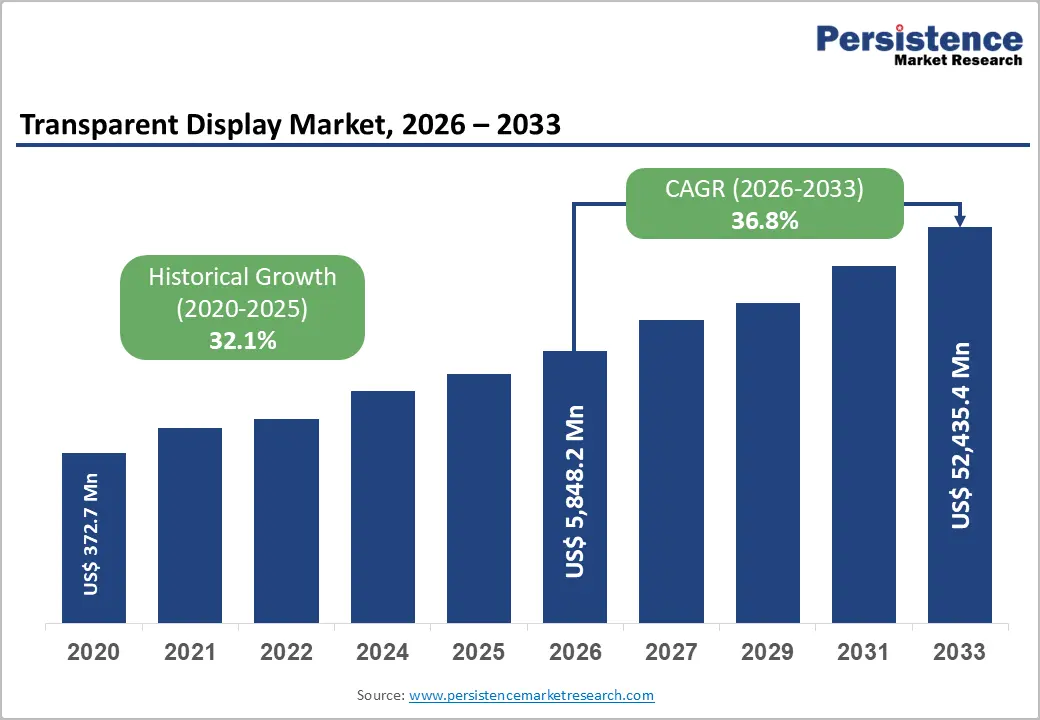

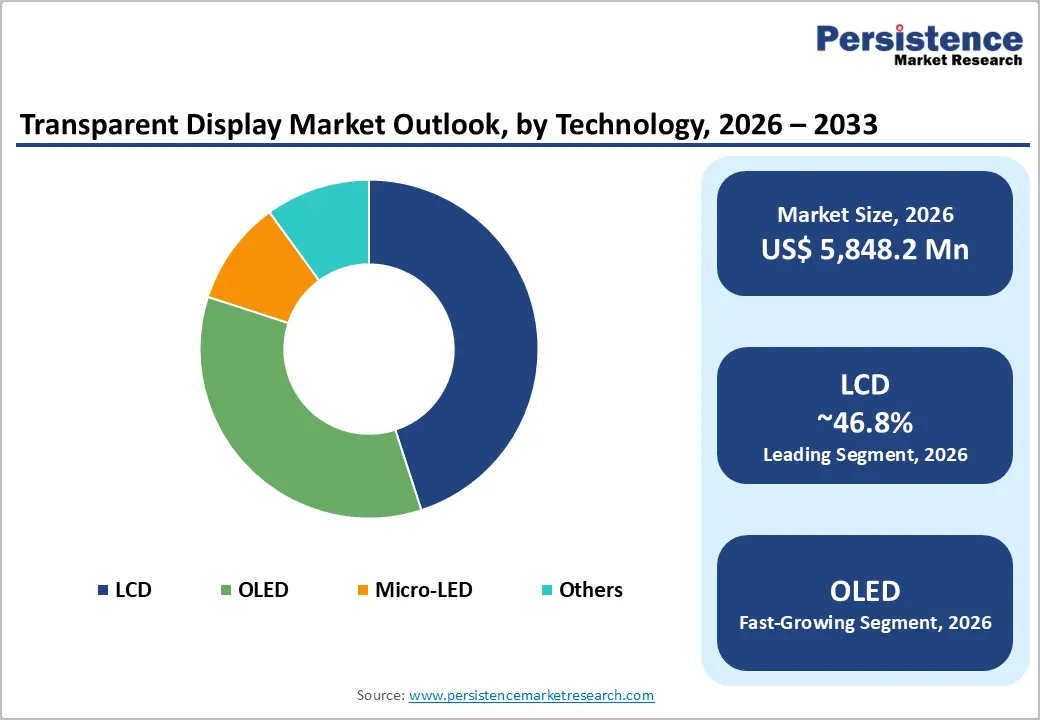

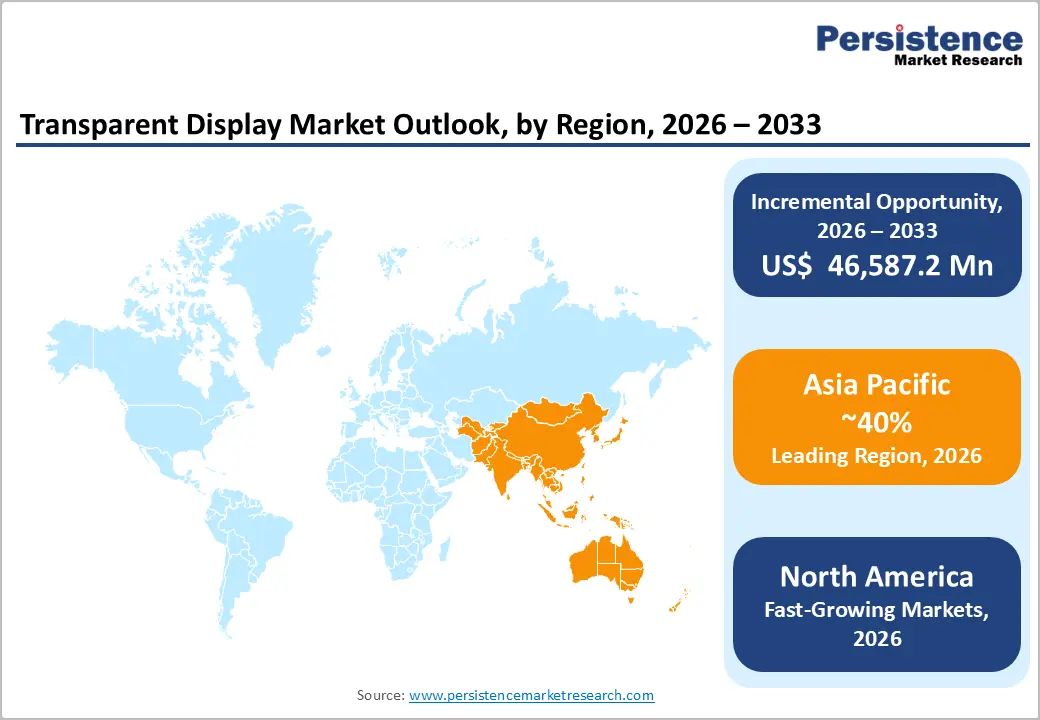

The global transparent display market size is likely to be valued at US$ 5,848.2 million in 2026 and is projected to reach US$ 52,435.4 million by 2033, growing at a CAGR of 36.8% between 2026 and 2033.

The market’s expansion reflects a fundamental shift from traditional opaque panels to transparent display technologies that seamlessly overlay digital content onto real-world environments. Rising demand is closely linked to automotive safety regulations, enhanced in-store and public retail experiences, and the accelerating adoption of augmented reality (AR) devices, all of which favor delivering information directly within the user’s field of vision.

Key Industry Highlights:

- Technology Leadership: LCD technology leads the transparent display market with a projected 46.8% share in 2026, driven by widespread adoption across kiosks, digital signage, and retail display applications. LCD panels offer cost efficiency, proven reliability, and ease of integration, making them the preferred choice for large-scale commercial deployments. OLED and micro-LED technologies are gaining traction as next-generation alternatives, supported by innovation in consumer electronics and automotive display solutions.

- Resolution Dynamics: Ultra HD resolution is expected to record the highest growth, accounting for 42.1% of the market in 2026, driven by strong demand from the retail and advertising sectors. High pixel density, superior image clarity, and enhanced visual engagement make Ultra HD transparent displays ideal for premium branding, interactive advertising, and immersive customer experiences.

- Regional Market Patterns: Asia Pacific dominates with a 40.2% market share in 2026, supported by the presence of leading transparent display manufacturers in China, Japan, and South Korea. Strong R&D investments, advanced manufacturing capabilities, and rapid adoption across automotive, consumer electronics, and retail industries underpin sustained regional growth.

- Industry Adoption Trends: Market participants are capitalizing on rising demand for automotive HUDs, advanced consumer electronics displays, and interactive retail and advertising solutions, positioning transparent displays as a core driver of innovation through 2026–2033.

| Key Insights | Details |

|---|---|

|

Transparent Display Market Size (2026E) |

US$ 5,848.2 Mn |

|

Market Value Forecast (2033F) |

US$ 52,435.4 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

36.8% |

|

Historical Market Growth (CAGR 2020 to 2024) |

32.1% |

Market Dynamics

Drivers - Companies Focus on Collaboration Initiatives to Boost Production Capability

Industry players are focusing on partnerships and collaborations to enhance their production capabilities and develop interactive display solutions to cater to consumer demand. For instance, in December 2024, German polymer materials manufacturer Covestro, Scottish Ceres Holographics, a leading provider of holographic optical elements, and U.S.-based specialty materials company Eastman signed a Memorandum of Understanding (MoU) to explore the commercial production of the cutting-edge Holographic In-Plan Transparent Display (HIPTD) technology.

It is a laminated hologram solution that allows multiple head-up displays in a single windshield. HIPTD will likely overcome the size, performance, and geometric limitations of traditional HUD systems while ensuring scalable and practical implementation of multiple displays. The Proofs-of-Concept (PoCs) were showcased alongside other OEMs at the Consumer Electronics Show (CES) 2025 in Las Vegas in January 2025.

Smart Retail and Experiential Advertising Transformation

Smart retail sector transformation, driven by consumer preference for interactive brand experiences and omnichannel engagement, has established transparent displays as a premium investment in retail infrastructure. Retail transparency requirements, enabling product visibility while displaying dynamic promotional content, address conflicting retail design objectives previously impossible with traditional opaque signage. Digital signage market expansion, with out-of-home advertising expenditure reaching US$ 300+ billion annually and 15-20% shifting to dynamic digital formats, establishes a proportionate transparent display opportunity.

Customer engagement metrics, with transparent displays that increase retail dwell time by 25% and conversion rates by 15% compared to traditional signage, justify a premium infrastructure investment. Airport and transportation hub deployments, featuring transparent displays that enable real-time information distribution while maintaining environmental visibility, drive adoption in the commercial segment across 1,500+ installations globally.

Restraints - High Manufacturing Cost and Technological Limitations May Negatively Impact Product Development

Factors such as high manufacturing costs and technological limitations are projected to hinder the growth of the transparent display market. The production of transparent interactive display requires precision manufacturing processes and incur high price tag. Therefore, these factors can deter investment and innovation, thereby restricting market growth through 2032.

- In February 2024, Apple announced the end of its micro-LED research and development efforts for future smartwatches and specialty applications, letting go of hundreds of employees at its secret California facility.

Manufacturing Complexity and Supply Chain Capital Requirements

Transparent display production concentration, with leading manufacturers (Samsung Display, BOE Technology, LG Display) controlling 70-80% of production capacity, establishes supply chain dependency and limited competitive entry. Capital intensity barriers, with fabrication facility construction requiring US$ 2-5 billion investment and multi-year production ramp cycles, constrain supplier expansion and competitive entry. Yield-rate challenges, with initial manufacturing yields of 30-40% versus conventional displays exceeding 80%, compress gross margins and limit profitability until scale achieves maturity.

Component sourcing complexity, with specialized transparent substrate materials and precision optical components sourced from limited suppliers, creates supply chain vulnerability. Geopolitical supply chain risks, with Taiwan semiconductor production concentration and US-China tensions creating political and trade uncertainties.

Opportunity - Increasing Adoption of Augmented and Virtual Reality to Spur Demand for Transparent Displays

Interactive displays play a crucial role in augmented reality (AR) and virtual reality (AR) applications, especially in healthcare, education, engineering, and the gaming industry. They aid in creating immersive experiences and provide enhanced 3D visuals to engage viewers. The demand for innovative display technology is likely to propel manufacturers to develop practical and comfortable wearable solutions. In addition, the recent introduction of Apple’s Vision Pro and the Quest series from Meta underscores the importance of AR in interpreting digital information in the real world. Companies operating in the market are conducting research activities and focusing on launching novel products, which is anticipated to boost market growth. For instance, in January 2024, researchers at the University of Melbourne, the Melbourne Centre for Nanofabrication (MCN), and KDH Design Corporation successfully introduced the world’s first-ever flexible, transparent AR display screen, perceived as a significant breakthrough in this field. Such innovations showcase how interactive displays are paving the way for new possibilities in the AR/VR applications, where digital overlay capabilities are essential.

Smart Building and Infrastructure Integration

Smart building transformation, with 60%+ of new construction projects incorporating IoT and intelligent building management systems, establishes a transparent display infrastructure opportunity. Building façade applications that enable energy-efficiency monitoring and visualization while maintaining architectural transparency create novel installation categories. The deployment of transportation infrastructure, with metros, airports, and rail systems implementing transparent displays for passenger information and crowd management, drives large-scale procurement.

Industrial facility applications that enable production monitoring through transparent overlays on the manufacturing floor drive operational efficiency gains. Healthcare infrastructure, with transparent displays enabling patient monitoring room visibility while displaying critical health metrics, establishes specialized medical applications.

Category-wise Analysis

Technology Insights

LCD segment is estimated to hold a share of 46.8% in 2026. Compared to traditional LCD panels with backlight units, LCD technology leverages light-modulating characteristics of liquid crystals, while offering high transparency rate and 90% less consumption of electricity. Due to its extensive adoption in various applications such as kiosks, digital signage, and interactive displays globally, the segment is experiencing considerable growth.

Micro-LED segment, on the other hand, is projected to hold a share of 41.6% in 2026. Micro-LED’s superior brightness capabilities along with minimal impact from ambient light are factors that are propelling growth of this segment.

Resolution Insights

Ultra HD resolution accounts for 42.1% of the transparent display market, driven by its strong adoption in premium and professional applications. Automotive head-up displays benefit from 4K resolution, which enables precise navigation visuals and multi-layer data projection with high legibility. In retail, Ultra HD transparent displays enhance product presentation and advertising impact by delivering superior image clarity and color detail. Large-format transparent panels above 30 inches rely heavily on higher resolutions to maintain visual sharpness at wider viewing distances.

In contrast, Full HD is the fastest-growing resolution segment, projected to grow at a 35% CAGR. Lower manufacturing complexity, 20% cost savings, and higher production yields support broader deployment across HMDs, mobile devices, and cost-sensitive installations.

- At CES 2025, established brands like TCL, Hisense, and Samsung showcased RGB backlighting technology that ensures a brighter and power-efficient display experience for the viewer.

End-user Insights

Retail accounts for 28.4% of the transparent display market, driven by large-scale commercial deployment and experiential marketing strategies. Luxury storefronts increasingly use transparent display windows to create immersive product showcases without blocking visibility. Retail chains are standardizing transparent digital signage to deliver promotional content while preserving open, modern store designs. These displays improve customer engagement, increase dwell time by 25%, and boost brand recall by 20%, which supports premium investment decisions.

Automotive is the fastest-growing end-use segment, projected to expand at ~40% CAGR through 2033. Rapid OEM adoption of transparent HUDs, tightening safety regulations, EV growth, and autonomous vehicle development are accelerating integration across passenger, fleet, and premium vehicle platforms.

Regional Insights

North America Transparent Display Market Insights

The transparent display market overview in North America forecasts a steady growth through 2032. The U.S. is projected to hold the largest market share in the region, followed by Canada, which is projected to experience rapid growth. Players in this region are aggressively developing cutting-edge display technologies, including OLED, LED, and 8K displays.

Companies are focusing on developing innovative display products by adopting growth strategies such as partnerships and mergers. For instance, Smartkem, a leading U.K.-based company, has partnered with North American companies to develop innovative display solutions. With Chip Foundation, they co-developed a new generation of micro-LED-based backlight technology for Liquid Crystals Displays, and further have announced a joint agreement to develop new generation display solutions.

Transparent display companies in the US are also increasing investments in research and development to meet rising consumer demand across the electronics, automotive, and retail industries. In December 2025, Smartkem raised US$ 7.65 Mn and secured a US$ 1.1 Mn grant to develop the world’s first rollable, transparent micro-LED display in collaboration with Chip Foundation.

Europe Transparent Display Market Insights

Europe represents approximately 22% of the global transparent display market share, valued at approximately US$ 1,400 million in 2026. Germany, the United Kingdom, France, and Spain collectively represent 78% of the European market value, reflecting established automotive manufacturing presence and luxury retail concentration.

Automotive manufacturing excellence, with Germany's automotive ecosystem (Audi, Mercedes-Benz, BMW, Volkswagen, Bosch, Continental) driving transparent-display innovation for premium and electric-vehicle applications. Regulatory environment, with European Union environmental directives and sustainability mandates encouraging energy-efficient, transparent display adoption. Luxury retail adoption, with Paris, London, and Milan establishing global fashion hub status and transparent display storefront installations.

Asia Pacific Transparent Display Market Insights

Asia Pacific is likely to dominate the global transparent display industry, accounting for about 40.2% of the market in 2025. Transparent displays are experiencing high demand from retail sector to create interactive and immersive experiences. These types of displays are ideal for digital signage applications, especially at retail outlets, kiosks, airports, and public transportation.

Asia Pacific region, with its dense urban environments and bustling retail markets, provides a significant opportunity for advertising companies and retail outlets to enhance their overall customer experience. For instance,

According to an industry report, by 2026, over 70% of retail outlets in APAC are likely to use digital signage for in-store advertising, while offering an enhanced shopping experience through technologies such as transparent displays and augmented reality (AR).

Competitive Landscape

Market concentration demonstrates oligopolistic characteristics with six major vendors (Workday, Microsoft, SAP, Oracle, UKG, ADP) controlling 50% of the global market value. Workday maintains market leadership with an estimated 9.8% global market share through sophisticated cloud platform, agentic AI integration, and a strategic acquisition strategy consolidating talent acquisition, contingent workforce management, and analytics capabilities. Microsoft follows with a substantial cloud presence and Power BI analytics adoption among Office 365 organizations. SAP SuccessFactors and Oracle Fusion Analytics command enterprise market segments through comprehensive HCM suite integration.

Key Industry Developments

- In November 2024, Smartkem announced its collaboration with AUO, the largest display manufacturer in Taiwan, to develop the world’s first advanced rollable, transparent microLED display. This partnership is likely to aid in the development of a novel display using Smartkem’s technology, making mass production of transparent display products viable.

- In January 2024, Continental, a renowned automotive supplier, unveiled the world’s first automotive display screen made with transparent Swarovski crystal. Product innovations have taken center stage among companies that look to leverage the rising demand for displays globally.

Companies Covered in Transparent Display Market

- LG Electronics

- Samsung Electronics

- Japan Display Inc. (JDI)

- Sony Corporation

- Tianma Microelectronics

- BOE Technology Group

- Panasonic Holdings Corporation

- Osram

- Universal Display Corporation

- Crystals Display Systems Ltd.

- Others Key Players

Frequently Asked Questions

The Transparent Display market is estimated to be valued at US$ 5,848.2 Mn in 2026.

The primary demand driver for the transparent display market is the rapid integration of see-through display technologies in automotive safety systems and next-generation retail environments.

In 2026, the Asia Pacific region will dominate the market with an exceeding 40% revenue share in the global Transparent Display market.

Among the resolutions, Ultra HD holds the highest preference, capturing beyond 32.3% of the market revenue share in 2026, surpassing other Resolution.

The key players in Transparent Display are LG Electronics, Samsung Electronics, Japan Display Inc. (JDI), and Sony Corporation.