- Semiconductor Materials & Components

- Silver Nanowire Transparent Conductors Market

Silver Nanowire Transparent Conductors Market Size, Share, and Growth Forecast, 2025 - 2032

Silver Nanowire Transparent Conductors Market by Function Type (Transfer Printing onto Poly Substrates, Drop Casting, Air-Spraying from Nanowire Suspension, Vacuum Filtration), Application (Conductive Applications, Optical Applications, Anti-Microbial Applications), and Regional Analysis for 2025 - 2032

Silver Nanowire Transparent Conductors Market Size and Trends Analysis

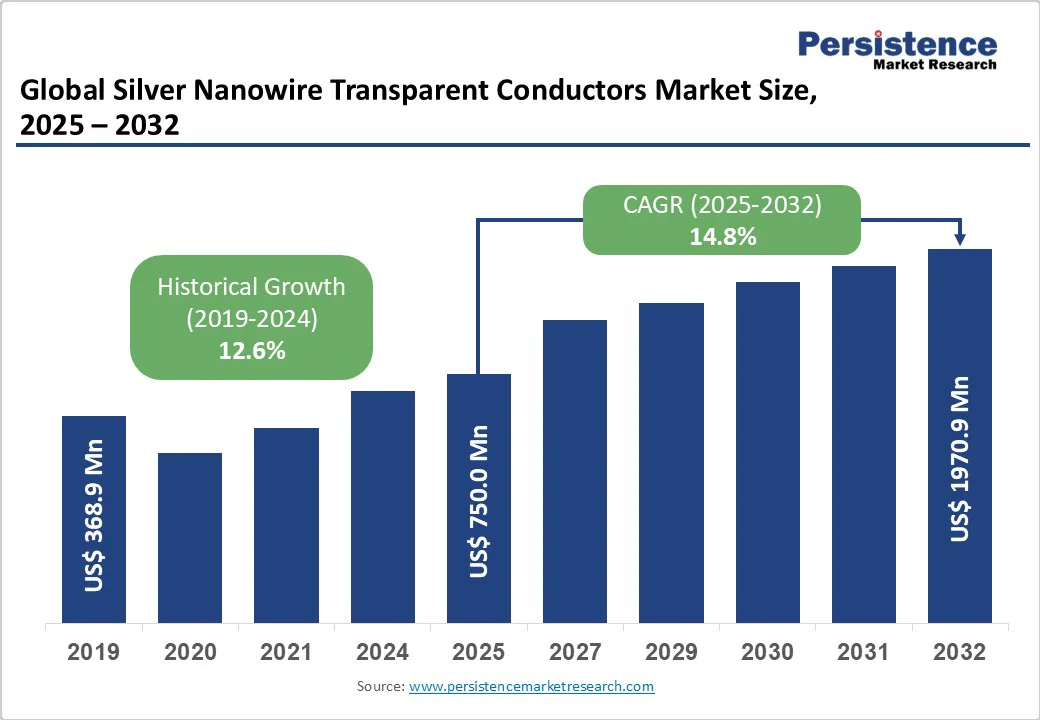

The global silver nanowire transparent conductors market size is likely to be valued at US$750.0 Million in 2025 and expected to reach US$1970.9 Million by 2032, registering a robust CAGR of 14.8% during the forecast period from 2025 to 2032, fueled by the increasing demand for flexible and transparent electronics, advancements in nanomaterial processing, and a global push toward enhancing optoelectronic infrastructure and device performance.

Key Industry Highlights:

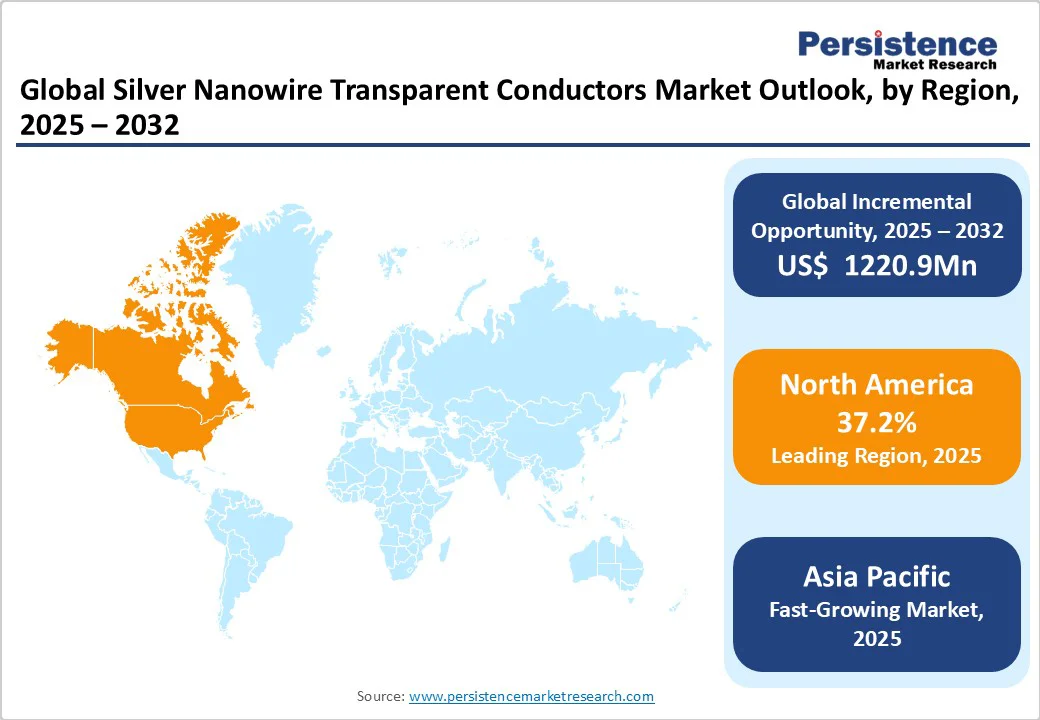

- Leading Region: North America holds a 37.2% market share in 2025, driven by advanced electronics infrastructure, widespread adoption of innovative nanowire solutions, and significant investments in nanomaterials research.

- Fastest-growing Region: Asia Pacific, propelled by increasing prevalence of consumer electronics manufacturing, urbanization, and expanding display access in countries such as China and India.

- Dominant Function Type: Transfer Printing onto Poly Substrates accounts for approximately 26% of the silver nanowire transparent conductors market share in 2025, owing to its critical role in scalable fabrication and advancements in high-throughput designs.

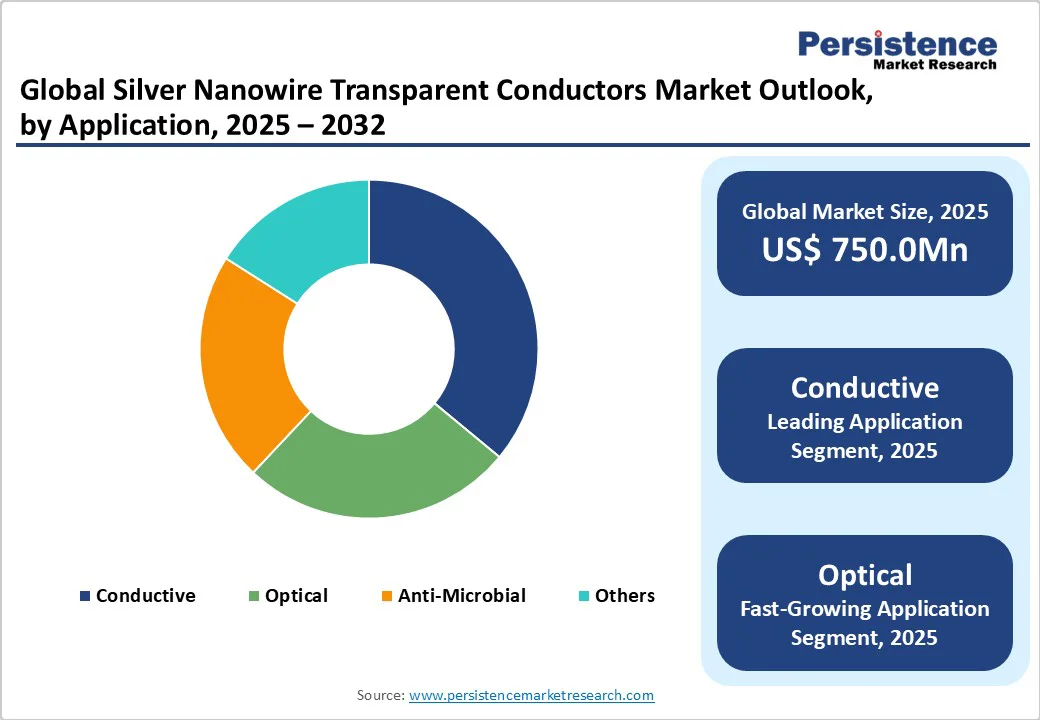

- Leading Application: Conductive Applications with a 36% share, reflecting its critical role in flexible circuits and electrode procedures.

| Key Insights | Details |

|---|---|

| Silver Nanowire Transparent Conductors Market Size (2025E) | US$750.0 Mn |

| Market Value Forecast (2032F) | US$1970.9 Mn |

| Projected Growth (CAGR 2025 to 2032) | 14.8% |

| Historical Market Growth (CAGR 2019 to 2024) | 12.6% |

Market Dynamics

Driver - Rising Demand for Flexible Electronics Amid Increasing Adoption of Wearables and Displays

The flexible electronics market is poised for strong expansion, driven by the adoption of silver nanowires that deliver ultra-high transmittance and low resistance, making them essential for foldable screens and wearable ecosystems. The surge in consumer electronics adoption, alongside rising lifestyle-related technology dependencies, is increasing reliance on transparent conductors, which are emerging as a global optoelectronic challenge.

Governments and manufacturers are investing heavily in nanowire infrastructure, with the United States advancing transfer printing techniques to enhance display densification and bridge urban coverage gaps. In Europe, OLED adoption continues to expand, supported by initiatives such as the EU’s Horizon Europe program, which emphasizes nanomaterial-efficient conductive treatments.

The conductive applications sector, representing a major portion of electronics expenditure, is turning to silver nanowire transparent conductors to overcome rigidity challenges, particularly in regions facing ITO scarcity. Data-intensive display applications are expected to place greater emphasis on flexibility and performance quality.

Emerging economies are projected to lead adoption through public-private partnerships and technology transfers. The rapid growth of wearable devices and the transition toward hybrid flexible-rigid designs highlight the central role of silver nanowires in ensuring seamless connectivity and performance across diverse substrates, establishing them as a cornerstone of next-generation bendable electronics.

Restraint - High Costs of Production and Stringent Regulatory Compliance

High costs associated with producing high-purity silver nanowires act as a key restraint to market growth. Manufacturers, especially small and medium-sized ones, face budget limitations in scaling synthesis methods that demand specialized equipment for polyol reduction and purification.

The challenge of ensuring uniform nanowire lengths and diameters across applications further raises expenses. Compliance with stringent regulations, including frameworks in Europe and the United States, adds additional cost layers, as non-compliance risks fines and supply chain disruptions.

The absence of standardized specifications across industries complicates adoption, creating variability issues and delaying implementations. Continuous R&D is required to address oxidation and agglomeration risks, adding to the financial burden and deterring smaller players from scaling.

Disruptions in silver precursor supply chains also contribute to volatile pricing, making adoption more difficult in cost-sensitive regions. Integration challenges with legacy materials, such as established ITO infrastructure in automotive and electronics, often demand extensive testing services that lengthen timelines and inflate budgets.

These hurdles collectively encourage organizations to pursue partial or alternative solutions rather than widespread nanowire deployments, slowing the silver nanowire transparent conductors market’s full potential realization.

Environmental concerns, particularly regarding silver ion leaching in antimicrobial applications, heighten regulatory scrutiny and procurement caution in tightly regulated sectors. As a result, cost pressures, compliance obligations, and environmental risks remain significant barriers to broader nanowire adoption globally.

Opportunity - Innovation in Formulations and E-commerce Expansion

The silver nanowire transparent conductors market is witnessing strong growth potential, supported by advances in hybrid nanomaterial formulations and the rapid expansion of e-commerce display technologies. Integrating silver nanowires with graphene or carbon nanotubes enhances stability, reduces junction resistance, and improves durability, paving the way for ultra-flexible sensors and wearable devices.

With rising e-commerce activity worldwide, demand for cost-effective, high-transmittance films capable of enduring dynamic bending in interactive packaging is accelerating. Core-shell encapsulation techniques also hold transformative potential, enabling humidity-resistant conductors that reduce degradation risks and extend product lifespans.

Electric vehicle adoption is further creating demand for scalable optical applications such as heads-up displays, encouraging vendors to invest in roll-to-roll compatible processes such as air-spraying that integrate seamlessly with PET substrates.

Sustainability adds another growth avenue, with recycled silver sourcing and eco-friendly nanomaterials aligning with regulatory and consumer preferences in green-focused regions. Emerging technologies, including the metaverse and augmented reality, are expanding nanowire applications into immersive optics and advanced interactive interfaces.

Digitization initiatives led by the public sectors in emerging economies present additional opportunities for affordable conductive solutions tailored to smart city infrastructure. Strategic collaborations between nanowire suppliers and display manufacturers could accelerate foldable-optimized films, enhancing performance and reducing flexibility failures, thereby solidifying silver nanowire’s role in next-generation optoelectronics.

Category-wise Analysis

Function Type Insights

The silver nanowire transparent conductors market is segmented into transfer printing onto poly substrates, drop casting, air-spraying from nanowire suspension, and vacuum filtration. Transfer Printing onto Poly Substrates dominates, holding approximately 26% share in 2025, due to its proven efficacy in large-area deposition, high yield, and integration into standard fabrication protocols. Transfer printing is widely used in display manufacturing, offering precise alignment that reduces defects.

Air-Spraying from Nanowire Suspension is the fastest-growing segment, driven by increasing demand for aerosol-based scalability in flexible substrates. Air-spraying provides versatile deployment as non-contact options, with advancements in nozzle precision and solvent optimization making them suitable for long-term use in high-volume populations.

Application Insights

The silver nanowire transparent conductors market is segmented into conductive applications, optical applications, and anti-microbial applications. Conductive Applications account for approximately 36% share in 2025, due to their proven efficacy in circuit electrodes, current support, and integration into electronic protocols. Conductive applications are widely used in touch sensors, offering low-resistance paths that reduce power loss.

Optical applications are the fastest-growing, driven by increasing demand for transparent films in AR/VR devices. These applications provide reliable transmittance as core elements, with advancements in haze reduction and UV stability making them suitable for long-term use in immersive populations.

Regional Insights

North America Silver Nanowire Transparent Conductors Market Trends

North America dominates the global silver nanowire transparent conductors market, expected to account for a 37.2% share in 2025, driven by a robust electronics ecosystem, high infrastructure investments, and a cultural emphasis on innovation and nanomaterials. The United States, as the silver nanowire transparent conductors market leader within the region, benefits from stringent regulations such as EPA nanomaterial guidelines that mandate advanced conductor adoption across sectors.

Key drivers include the rapid proliferation of flexible display R&D, with a growing number of patents filed annually, necessitating sophisticated transfer printing integration. Enterprises in tech hubs such as Silicon Valley are at the forefront, investing heavily in conductive films to counter ITO shortages, with substantial spending on nanomaterials.

The region's mature startup ecosystem fosters innovation in anti-microbial coatings, while government initiatives such as NSF nanotechnology grants accelerate manufacturing uptake. However, challenges such as supply chain dependencies persist, prompting increased reliance on domestic synthesis. Overall, North America's device-heavy landscape and regulatory maturity position it as the epicenter of nanowire evolution, with trends increasingly leaning toward AI-optimized deposition controls.

Europe Silver Nanowire Transparent Conductors Market Trends

Europe presents a mature yet dynamic landscape in the silver nanowire transparent conductors market, with countries such as Germany, the UK, and France leading growth through rigorous standards and strategic initiatives. Germany’s Industry 4.0 programs drive demand in automotive optics, emphasizing secure integrations for HUDs, while the UK focuses on sovereign material solutions to strengthen economic resilience. France advances optical digitization through its national photonics network, serving millions of display units annually and highlighting interoperability priorities.

Regulatory frameworks, such as REACH nanomaterial registration, have encouraged substantial compliance investments, promoting proactive conductor upgrades. The EU’s Digital Europe Programme further supports cross-border collaborations and hybrid function models, while Nordic countries such as Sweden excel in sustainable nanowire applications aligned with EU Green Deal goals. Challenges, including harmonized toxicity assessments, are being addressed through initiatives such as the European Nanotechnology Gateway, which fosters standardization.

Overall, Europe’s combination of stringent regulations, sustainability focus, and national innovation programs positions it as a critical hub for silver nanowire adoption, driving precise, reliable, and advanced applications across multiple sectors.

Asia Pacific Silver Nanowire Transparent Conductors Market Trends

Asia Pacific is the fastest-growing region in the silver nanowire transparent conductors market, driven by rapid electronics industrialization and expanding display production in countries such as China, India, and South Korea. China’s industrial initiatives encourage widespread conductor adoption in consumer goods, strengthening urban manufacturing infrastructures and supporting the growth of OLED panels.

India’s Digital India program promotes nanowire films for e-governance touch interfaces, creating strong demand for cost-effective drop casting solutions. South Korea leads in vacuum filtration techniques for its export-focused display sector, integrating anti-microbial layers for wearable health technologies.

Key drivers include booming semiconductor growth, which requires versatile applications, alongside government investments in flexible technology frameworks. Regional initiatives, such as APEC’s nanomaterial standards, facilitate shared research and innovation, mitigating challenges such as varying IP protections.

The young, tech-savvy population accelerates the adoption of advanced substrates, while techniques such as air-spraying expand applications in areas such as rural solar technology. These factors collectively position the Asia Pacific for sustained high growth in silver nanowire adoption across multiple sectors.

Competitive Landscape

The global silver nanowire transparent conductors market is fragmented yet consolidating, with materials giants and specialized firms competing through innovation and strategic partnerships. Leading players leverage proprietary synthesis combining high-aspect-ratio wires with polymers for conductive and optical applications.

Intense R&D focuses on haze-free films, bend-cycle durability, and scalable production. Emerging trends include bio-derived stabilizers and recyclable processes, while consolidation grows as electronics shift toward ITO-free, flexible solutions.

Key Developments

- December 2024: With an emphasis on transparent conductive films, DENSO Corporation has teamed up with Canatu of Finland to implement carbon nanotube technology. By tackling visibility problems brought on by frost and condensation, this partnership seeks to improve autonomous driving systems. These developments rely heavily on carbon nanotubes, which are renowned for their strength and conductivity. Additionally, the project supports DENSO's endeavors to become carbon neutral.

- January 2024: To increase the production of electronic materials, such as Transparent Conductive Films (TCFs), FUJIFILM Corporation announced plans to invest in its Kumamoto facility. The action is intended to satisfy the growing demand for sophisticated electronic components worldwide. This expansion demonstrates the company's commitment to enhancing its manufacturing capabilities. With this calculated investment, FUJIFILM hopes to increase efficiency and market share in the TCF industry.

Companies Covered in Silver Nanowire Transparent Conductors Market

- 3M

- Armor Group

- Atmel

- Cambrios Technologies

- Carestream Advanced Materials

- Heraeus

- Innova Dynamics

- Seashell Technology

Frequently Asked Questions

The silver nanowire transparent conductors market is projected to reach US$750.0 Mn in 2025.

Rising demand for flexible displays, technological advancements in deposition methods, and industry initiatives for ITO alternatives are key drivers.

The silver nanowire transparent conductors market is poised to witness a CAGR of 14.8% from 2025 to 2032.

Innovations in hybrid nanomaterials and scalable printing techniques, such as aerosol deposition, present significant growth opportunities.

3M, Armor Group, Atmel, Cambrios Technologies, Carestream Advanced Materials, Heraeus, Innova Dynamics, and Seashell Technology are among the leading players, known for their innovative nanowire solutions.