- Food Packaging

- Transparent Barrier Packaging Films Market

Transparent Barrier Packaging Films Market Size, Share, and Growth Forecast 2026 - 2033

Transparent Barrier Packaging Films Market by Product Type (Polyethylene (PE), Ethylene Vinyl Alcohol (EVOH), Polypropylene (PP), Polyethylene Terephthalate (PET), and Others), Application (Food and Beverages, Pharmaceutical Packaging, Personal Care Product Packaging, and Others), and Regional Analysis for 2026 - 2033

Transparent Barrier Packaging Films Market Size and Share Analysis

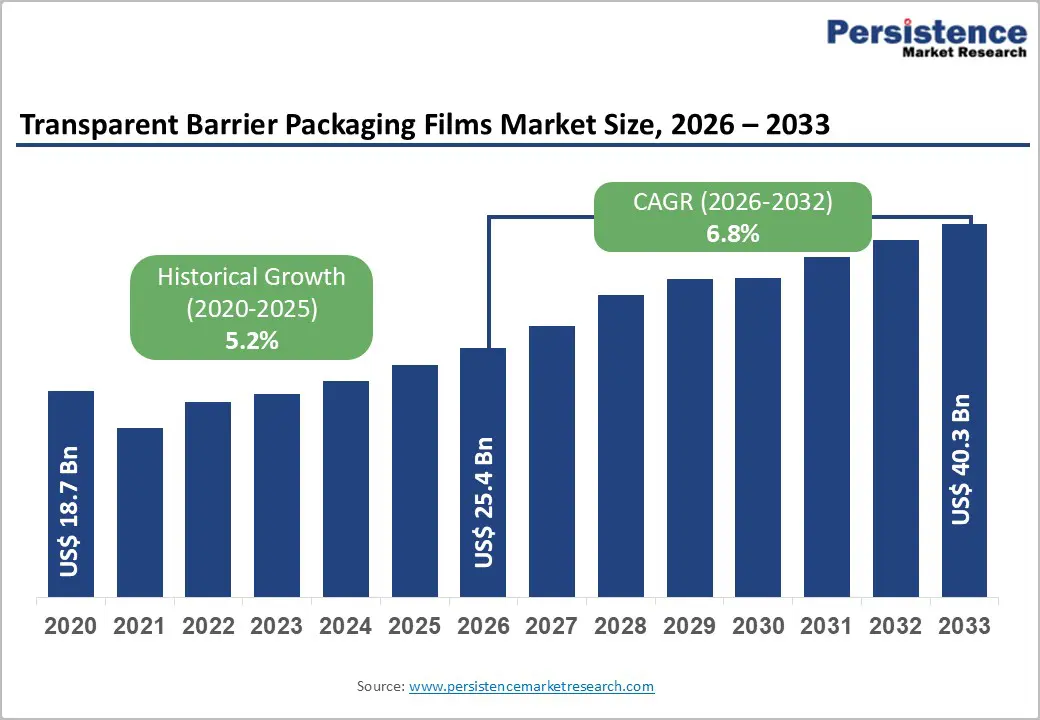

The global transparent barrier packaging films market size is likely to be valued at US$ 25.4 billion in 2026 and is projected to reach US$ 40.3 billion by 2033, growing at a CAGR of 6.8% between 2026 and 2032.

Market expansion is driven by accelerating consumer demand for convenience foods and processed meals, which require extended-shelf-life packaging solutions with superior barrier properties against oxygen, moisture, and aroma permeation, thereby preserving product freshness and enhancing retail visibility. Growth in the pharmaceutical and personal-care industries, which require protective barriers against external contaminants, will further drive demand for advanced barrier film solutions.

Key Industry Highlights:

- Leading Region: North America maintains a significant market position, anchored by the United States' healthcare packaging specialization, a stringent FDA and EPA regulatory framework, premium demand in the pharmaceutical and medical-device sectors, and established manufacturing capabilities that support advanced barrier-film production.

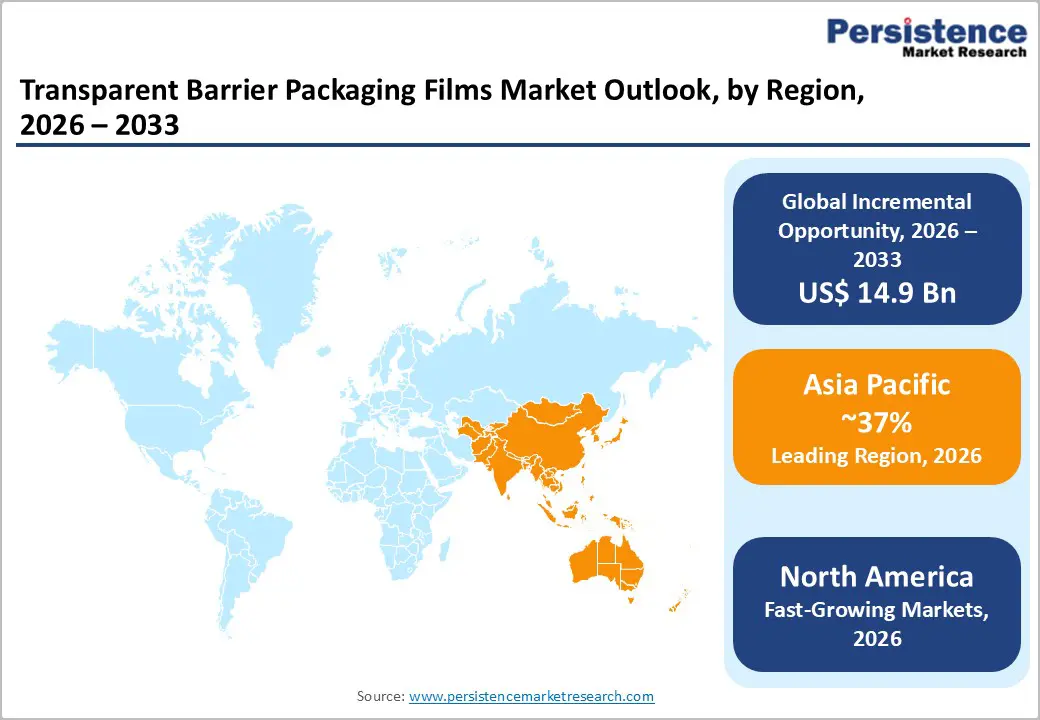

- Fastest Growing Region: Asia-Pacific to hold nearly 37% share of the global market, driven by China's 35 percent regional market share and manufacturing dominance, India's cold-chain expansion and plastic-ban enforcement creating protected packaging demand, e-commerce infrastructure development, and government digital-transformation initiatives.

- Dominant Product Type: Polyethylene (PE) holds a leading position in the global transparent barrier packaging films market, representing an estimated 30% share in 2026, fueled by its outstanding versatility, affordability, and well-rounded performance attributes.

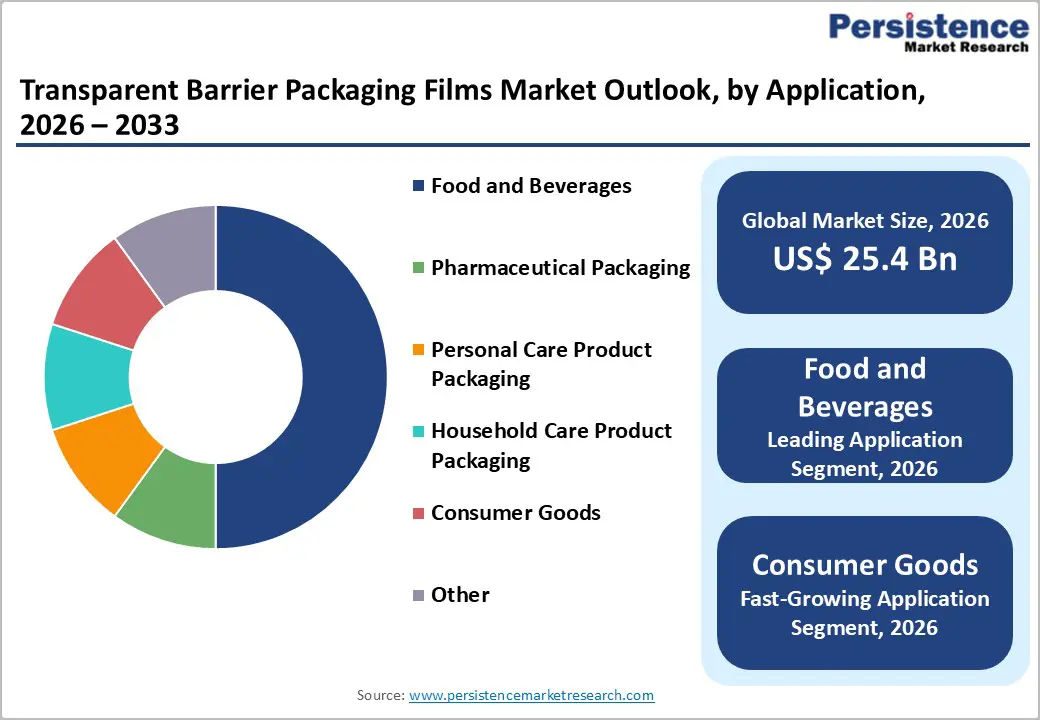

- Dominant Application: Food and beverages command market dominance, with a projected 2026 share of 40%, driven by convenience and ready-to-eat food demand, perishable-product protection requirements, product-visibility preference over metallized alternatives, and e-commerce food-delivery expansion.

- Key Opportunity: Asia-Pacific manufacturing scale expansion and e-commerce-driven demand acceleration, with China reducing import dependence through domestic capacity investment, India expanding cold-chain capacity for pharmaceutical and perishable goods logistics, and cost-competitive positioning enabling aggressive pricing strategies for emerging-market penetration.

| Key Insights | Details |

|---|---|

| Transparent Barrier Packaging Films Market Size (2026E) | US$ 25.4 Bn |

| Market Value Forecast (2033F) | US$ 40.3 Bn |

| Projected Growth CAGR (2026 - 2033) | 6.8% |

| Historical Market Growth (2020 - 2025) | 5.2% |

Market Dynamics

Drivers - Rising Demand for Extended Shelf Life and Product Protection in Food & Beverage Packaging

The accelerating demand for extended shelf life and superior product protection, particularly in the food and beverage industry, is a primary driver of the global transparent barrier packaging films market. Changing consumer lifestyles, characterized by urbanization, busy work schedules, and increased preference for ready-to-eat, frozen, and packaged foods, have significantly elevated the need for high-performance packaging solutions. Transparent barrier films provide effective protection against oxygen, moisture, light, and contaminants while maintaining product visibility, a key factor influencing consumer purchasing decisions. By effectively limiting the transmission of oxygen and water vapor, these films help preserve freshness, flavor, texture, and nutritional value, thereby reducing food spoilage and waste across the supply chain.

The global food distribution networks have become longer and more complex, with products frequently transported across regions and countries. This creates a strong requirement for packaging materials that can withstand extended storage and transportation periods without compromising product integrity. Transparent barrier films meet these needs while supporting modified-atmosphere and vacuum packaging technologies, which are increasingly adopted by food processors to enhance shelf stability. Rising food safety regulations and quality standards across both developed and emerging economies are compelling manufacturers to adopt advanced barrier materials to ensure compliance and minimize product recalls. As consumers continue to demand fresher, safer, and visually appealing packaged food products, the reliance on transparent barrier packaging films is expected to grow steadily, reinforcing their role as a critical material in modern food packaging systems.

Growth of Pharmaceutical, Personal Care, and Healthcare Packaging Applications

The robust growth of pharmaceutical, personal care, and healthcare packaging applications is another significant driver for the global transparent barrier packaging films market is the robust growth of pharmaceutical, personal care, and healthcare packaging applications. These industries require packaging materials that provide high-barrier performance to protect sensitive products from environmental factors such as moisture, oxygen, UV radiation, and microbial contamination. Transparent barrier films are increasingly preferred in these sectors because they combine functional protection with product visibility, enabling easy inspection, authentication, and consumer confidence. In pharmaceutical packaging, transparent barrier films are widely used for blister packs, sachets, and strip packaging to safeguard drug efficacy and stability throughout their shelf life.

Rising global healthcare expenditure, expanding access to medicines in emerging markets, and the growing prevalence of chronic diseases are directly increasing demand for reliable and compliant packaging solutions. The personal care and cosmetics industry is experiencing strong growth, driven by rising disposable incomes, premiumization, and heightened consumer awareness of product quality. Transparent barrier films support attractive packaging designs while preventing oxidation, fragrance loss, and moisture ingress, which are critical to maintaining product performance. Increasing regulatory scrutiny regarding packaging safety, traceability, and tamper evidence is encouraging manufacturers to adopt advanced barrier films that meet stringent compliance requirements. As innovation continues in high-barrier, lightweight, and cost-effective transparent film technologies, their adoption across healthcare and personal care applications is expected to expand, positioning these technologies as key contributors to sustained market growth.

Restraint - Technical Complexity and Performance Trade-Offs in Transparent Barrier Films

The technical complexity of achieving high-barrier performance while maintaining transparency, flexibility, and processability is restraining the growth of the global transparent barrier packaging films market. Enhancing oxygen, moisture, and aroma barriers often requires multilayer structures, coatings, or metallization, which can compromise optical clarity, seal integrity, or mechanical strength if not precisely engineered. Manufacturers frequently face trade-offs among barrier efficiency and other critical properties, such as heat resistance, puncture strength, machinability, performance on high-speed packaging lines, and compatibility with different product types. These challenges lengthen development timelines and increase the risk of performance variability across batches.

Integrating transparent barrier films into existing packaging lines may require equipment modifications, recalibration, or changes in sealing parameters, increasing operational complexity for end users. Food, pharmaceutical, and personal care companies that prioritize production efficiency may hesitate to adopt materials that demand process adjustments or introduce downtime. Achieving uniform barrier coatings at an industrial scale requires advanced technology and strict quality control, which may not be readily available to all manufacturers, particularly in developing regions. These technical hurdles can slow adoption, limit supplier diversification, and constrain market growth despite strong end-user demand.

Competition from Alternative Packaging Materials and Technologies

Strong competition from alternative packaging materials and barrier technologies is another restraint on the transparent barrier packaging films market. Rigid packaging formats such as glass, metal cans, and aluminum foil continue to offer superior barrier properties and are widely trusted for long-shelf-life applications, particularly in beverages, pharmaceuticals, and sensitive food products. Paper-based and fiber-based packaging solutions are gaining traction as sustainable alternatives, supported by regulatory incentives and consumer preference for plastic-free packaging. Advances in coatings, laminates, and biodegradable materials are enabling these alternatives to deliver improved barrier performance while aligning with environmental goals.

Emerging technologies such as active packaging, edible coatings, and smart packaging solutions may reduce reliance on high-barrier plastic films by extending shelf life through non-material-based methods. Brand owners seeking differentiation or sustainability leadership may prioritize these alternatives over transparent barrier films, particularly when transparency is not a critical requirement. As innovation continues across competing packaging formats, transparent barrier films face ongoing pressure to justify their value proposition in terms of cost, performance, and sustainability, which can restrain market expansion in certain end-use segments.

Opportunity - Bio-Based and Sustainable Barrier Film Development and Environmental Compliance Leadership

Growing consumer environmental consciousness, combined with regulatory mandates for recyclability, creates opportunities for bio-based barrier film developers, including polylactic acid (PLA) and cellulose-based alternatives. Advanced co-extrusion technology enabling multilayer structures (3-layer current, 7-layer+ future configurations) with blended bio-based and conventional polymers, creating performance optimization with sustainability positioning.

Mono-material barrier solutions are gaining market traction as regulatory restrictions discourage the use of complex, non-recyclable multilayer films. Water-based and bio-based coating technologies are replacing solvent-based solutions, expanding sustainability credentials while addressing chemical-restriction regulations. Companies investing in advanced materials science, including BASF, Mitsubishi Chemical, and DuPont, are developing next-generation sustainable barrier solutions, thereby establishing competitive differentiation and creating multi-segment growth opportunities over the forecast period.

Expanding Applications in E-Commerce and Home-Delivery Packaging

The rapid expansion of e-commerce and home-delivery channels across food, pharmaceuticals, and personal care products presents a significant opportunity for the global transparent barrier packaging films market. The shift toward online purchasing has fundamentally changed packaging requirements, with greater emphasis on product protection during extended transit, handling, and last-mile delivery. Transparent barrier packaging films offer strong resistance to moisture, oxygen, and contamination while maintaining product visibility, which is increasingly important for consumer trust in online purchases where physical inspection is not possible. In food and grocery e-commerce, barrier films help preserve freshness and prevent leakage or spoilage during transportation, particularly for ready-to-eat meals, frozen foods, and perishable items.

The pharmaceutical and healthcare e-commerce platforms require high-barrier, tamper-resistant packaging to ensure product safety, compliance, and integrity throughout distribution. The growing adoption of direct-to-consumer business models by brands further amplifies the need for lightweight, flexible, and protective packaging materials that minimize shipping costs while maximizing performance. Transparent barrier films meet these requirements more effectively than rigid packaging alternatives. As global e-commerce penetration continues to rise, especially in emerging markets, packaging solutions that combine durability, barrier protection, and visual appeal are expected to see increased demand. This structural shift in retail and distribution channels creates a long-term growth opportunity for transparent barrier film manufacturers willing to tailor products for e-commerce-specific packaging needs.

Category-wise Insights

Product Type Analysis

Polyethylene (PE) materials command a dominant position in the global transparent barrier packaging films market, accounting for an estimated 30% market share in 2026, driven by their exceptional versatility, cost-effectiveness, and balanced performance characteristics. PE films are widely used across food, pharmaceutical, and personal care packaging due to their excellent moisture barrier properties, flexibility, and sealability, making them suitable for pouches, wraps, and multilayer laminates. Their compatibility with high-speed packaging lines and ability to be easily processed through extrusion and lamination further enhances adoption among manufacturers. Increasing demand for lightweight and flexible packaging, particularly in packaged foods and e-commerce applications, continues to support PE consumption.

The growing focus on sustainability has strengthened PE’s position, as mono-material polyethylene structures are increasingly favored to enhance recyclability and compliance with circular-economy regulations. Compared to specialty barrier polymers such as EVOH or PVDC, PE offers a favorable cost-to-performance ratio, enabling large-scale use in both developed and emerging markets. Continuous innovations in downgauging, metallocene-based PE grades, and recyclable, barrier-enhanced PE structures are further expanding its application scope, reinforcing polyethylene’s leadership within the product-type segmentation of transparent barrier packaging films.

Application Insights

Food and beverages hold a dominant market position, with a projected 2026 share of 40%, driven by a shift toward convenience and ready-to-eat packaged foods that require extended shelf-life maintenance. Perishable-product protection requirements for meat, dairy, snacks, and fresh produce packaging establish high-volume demand for superior oxygen and moisture barriers. Transparency preference enables product visibility and consumer trust, whereas opaque metallized alternatives support transparent barrier film adoption across retail channels.

E-commerce food delivery expansion necessitates robust protective packaging that withstands logistics stress while maintaining product freshness and shelf-appeal. Premium packaging segment growth, particularly for organic, fresh, and specialty foods, is commanding higher barrier-film pricing, supporting margin expansion opportunities. The pharmaceutical and personal-care segments account for a combined 30% share, driven by specialized barrier requirements that protect active ingredients against oxidation and moisture exposure, thereby ensuring multi-segment demand diversification throughout the forecast period.

Regional Insights

North America Transparent Barrier Packaging Films Market Trends

North America represents a mature and highly regulated market for transparent barrier packaging films, characterized by stringent food safety, healthcare, and environmental compliance requirements. A strong regulatory framework enforced by the U.S. Food and Drug Administration and the Environmental Protection Agency compels packaging manufacturers to meet rigorous standards related to material safety, traceability, and sustainability. This environment supports the adoption of high-performance and premium barrier films, particularly in healthcare packaging. The region’s well-established pharmaceutical and medical-device industries drive consistent demand for transparent barrier films that ensure sterility, prevent contamination, and maintain product integrity over extended shelf lives and complex distribution networks.

Regulatory focus on PFAS restrictions, recyclability mandates, and reduced environmental impact is reshaping material innovation. Manufacturers are increasingly investing in bio-based polymers, recyclable mono-material structures, and advanced recycling technologies to align with sustainability goals without compromising barrier performance. In healthcare procurement, buyers remain cost-conscious despite demanding premium quality and regulatory compliance, intensifying competition among established players. This balance between regulatory rigor, innovation-led sustainability, and pricing pressure defines current market dynamics and continues to shape product development and competitive strategies across North America.

Europe Transparent Barrier Packaging Films Market Trends

Europe is and highly developed market for transparent barrier packaging films, supported by strong industrial capabilities and innovation-driven demand. Germany plays a key role through its specialized industrial manufacturing base, particularly in high-precision polymer processing and advanced coating technologies, while the UK maintains an innovation-focused positioning driven by R&D-intensive packaging, material science, and sustainability-oriented start-ups. The introduction of EU regulations in 2024 - 2025 establishing stringent restrictions on PFAS has created a structural compliance requirement for packaging manufacturers, accelerating investment in alternative barrier chemistries, water-based and solvent-free coatings, and next-generation functional layers that deliver high performance without regulated substances.

European consumer preferences strongly favor sustainable and environmentally responsible packaging, supporting premium positioning for bio-based transparent barrier films and recyclable multilayer or mono-material solutions. Brand owners increasingly leverage transparent, sustainable packaging as a differentiator, particularly in the food, beverage, and personal care sectors. At the regulatory level, harmonization initiatives across EU member states are promoting consistent safety, recyclability, and performance standards, reducing market fragmentation.

Asia Pacific Transparent Barrier Packaging Films Trends

Asia-Pacific, with 37% share, commands a dominant position in the global transparent barrier packaging films market, underpinned by large-scale manufacturing capacity, rapid consumption growth, and strong policy support. China accounts for approximately 35% of the regional market share, driven by its massive food-processing industry, expanding pharmaceutical production, and a vertically integrated packaging supply chain. High volumes of packaged food, ready-to-eat meals, and pharmaceutical products generate sustained demand for transparent barrier films that offer moisture and oxygen protection while enabling product visibility.

India is experiencing the fastest growth within the Asia-Pacific region, shaped by a unique combination of regulatory enforcement and infrastructure expansion. Plastic-ban regulations are accelerating the transition toward compliant, high-performance, and recyclable barrier film solutions, while rapid expansion of cold-chain infrastructure is driving demand for protective packaging for frozen foods and temperature-sensitive pharmaceuticals. In parallel, government-led digital-transformation programs and continued e-commerce infrastructure development are boosting demand for durable, lightweight, and high-barrier flexible packaging.

Competitive Landscape

The transparent barrier packaging films market is moderately consolidated, with a strong presence of Tier-1 global manufacturers that exert significant influence over pricing, technology adoption, and customer relationships. Leading players such as Amcor, Sealed Air, Berry Global, and Mondi command substantial market share through broad and diversified product portfolios, global manufacturing footprints, and long-standing relationships with multinational food, pharmaceutical, and personal care brands. These companies leverage advanced material science capabilities, multilayer and coating technologies, and strong R&D pipelines to deliver high-performance transparent barrier films that meet stringent regulatory and sustainability requirements.

Their established global supply chains and localized production facilities enable reliable, high-volume supply while optimizing cost efficiency and responsiveness to regional demand. Competitive advantage is further reinforced through continuous innovation in recyclable, mono-material, and bio-based barrier film solutions, aligning with evolving regulatory frameworks and brand-owner sustainability commitments. While Tier 1 players dominate premium and large-volume contracts, Tier 2 and regional manufacturers compete on cost, customization, and niche applications, particularly in emerging markets. Overall, competition is increasingly driven by technological differentiation, sustainability credentials, and the ability to offer scalable, compliant solutions across global markets.

Key Developments:

- In November 2025, TOPPAN Inc. installed a hybrid manufacturing line capable of manufacturing both BOPP and BOPE films on a single platform. The company’s India-based subsidiary, TOPPAN Speciality Films Private Limited (TSF), initiated mass production in mid-November 2025, supplying high-performance BOPP and BOPE films to packaging converters and leading global food and FMCG brand owners.

- In April 2025, Amcor announced the completion of its all-stock combination with Berry Global to enhance its position as a global leader in consumer and healthcare packaging solutions. The acquisition will unlocks further opportunities to refine portfolio and enhanced positions in attractive categories.

Companies Covered in Transparent Barrier Packaging Films Market

- Amcor plc

- Bemis Manufacturing Company

- Sealed Air

- Sonoco Products Company

- DS Smith

- 3M

- Mitsubishi Chemical Advanced Materials

- Innovia Films

- TOPPAN INC.

- Daibochi Berhad

- Klöckner Pentaplast

- OIKE & Co., Ltd.

- Mondi

- DuPont

Frequently Asked Questions

The global Transparent Barrier Packaging Films Market is projected to reach US$ 40.3 billion by 2033, expanding from US$ 25.4 billion in 2026 at a CAGR of 6.8%, driven by convenience-food market explosion requiring shelf-life extension, pharmaceutical and healthcare protection requirements.

Market demand growth is driven by multiple converging factors including accelerating consumer demand for convenience and ready-to-eat foods, superior oxygen barrier performance, e-commerce expansion requiring robust protective packaging, and consumer environmental consciousness driving bio-based alternative adoption.

Food and beverages command market leadership with 40% projected 2026 market share, driven by convenience-food market explosion, perishable-product protection necessity, transparency preference versus metallized alternatives, e-commerce food-delivery expansion, and premium-packaging segment growth.

Asia-Pacific maintains market leadership position driven by China's 35% regional market share with massive food-processing sector and government domestic film-capacity investment, India's fastest-growing pharmaceutical and food-packaging markets, cold-chain infrastructure expansion.

Major market opportunities include bio-based and sustainable barrier-film development addressing EU mandates, e-commerce-driven demand acceleration requiring protective flexible packaging, and cost-competitive barrier-film positioning enabling aggressive pricing strategies for emerging-market penetration.

Players include Amcor, Bemis Manufacturing Company, 3M, Mondi, TOPPAN INC., DuPont, among others are the leading companies.