- Advanced Materials

- Radar Absorbing Materials Market

Radar Absorbing Materials Market Size, Share, and Growth Forecast, 2025 - 2032

Radar Absorbing Materials Market by Material Type (Magnetic absorbers, Dielectric absorbers, Hybrid absorbers, Impedance matching materials, Metamaterial absorbers, Frequency Selective Surfaces, Others), Form, Application, and Regional Analysis for 2025 - 2032

Radar Absorbing Materials Market Size and Trends Analysis

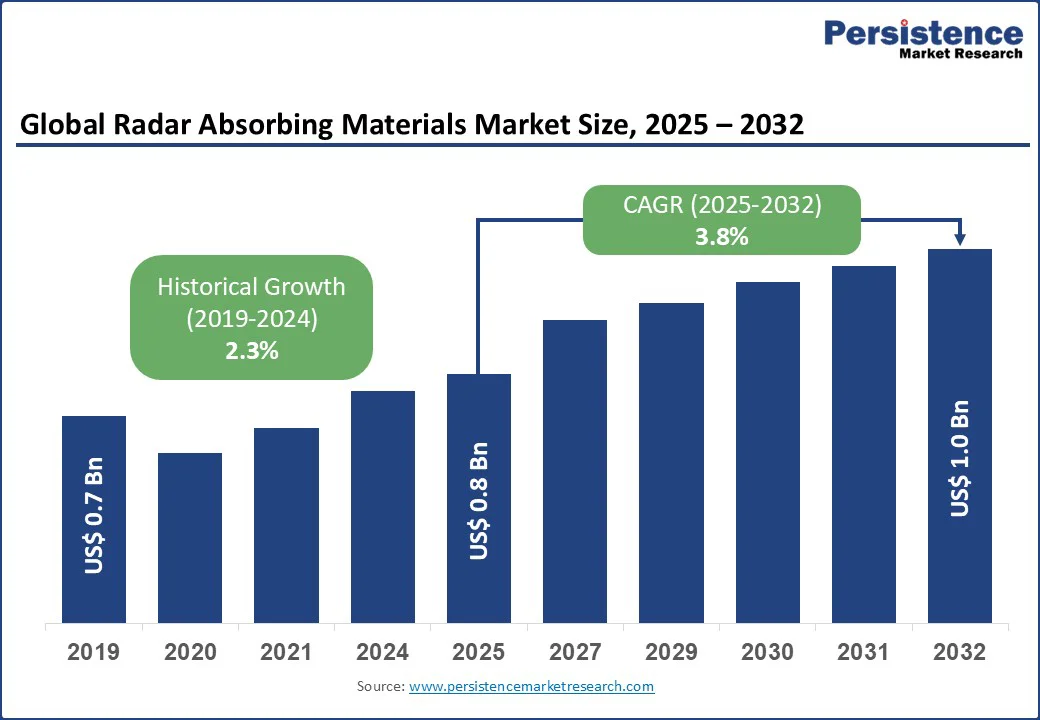

The global radar absorbing materials market size is likely to be valued at US$0.8 Bn in 2025 and expected to reach US$1.0 Bn by 2032, registering a robust CAGR of 3.8% during the forecast period from 2025 to 2032. The industry has experienced significant growth, fueled by the increasing demand for stealth technologies in defense applications, advancements in material science for electromagnetic wave absorption, and a global push toward modernizing military capabilities.

Key Industry Highlights:

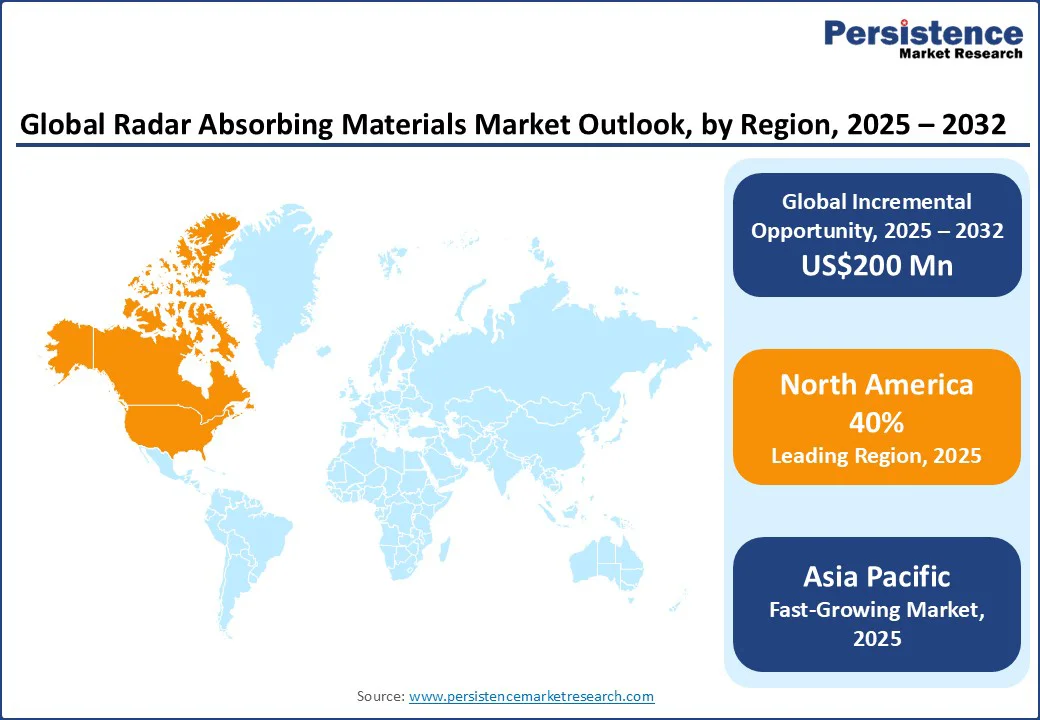

- Leading Region: North America holds a 40% market share in 2025, driven by advanced defense infrastructure, widespread adoption of stealth programs, and significant investments in military technologies.

- Fastest-growing Region: Asia Pacific, propelled by increasing defense investments, a pressing need for modernization, and expanding military capabilities in countries such as China and India.

- Dominant Material Type: Magnetic absorbers account for approximately 45% of the global radar absorbing materials market share in 2025, owing to their effective electromagnetic wave attenuation and ease of integration in defense settings.

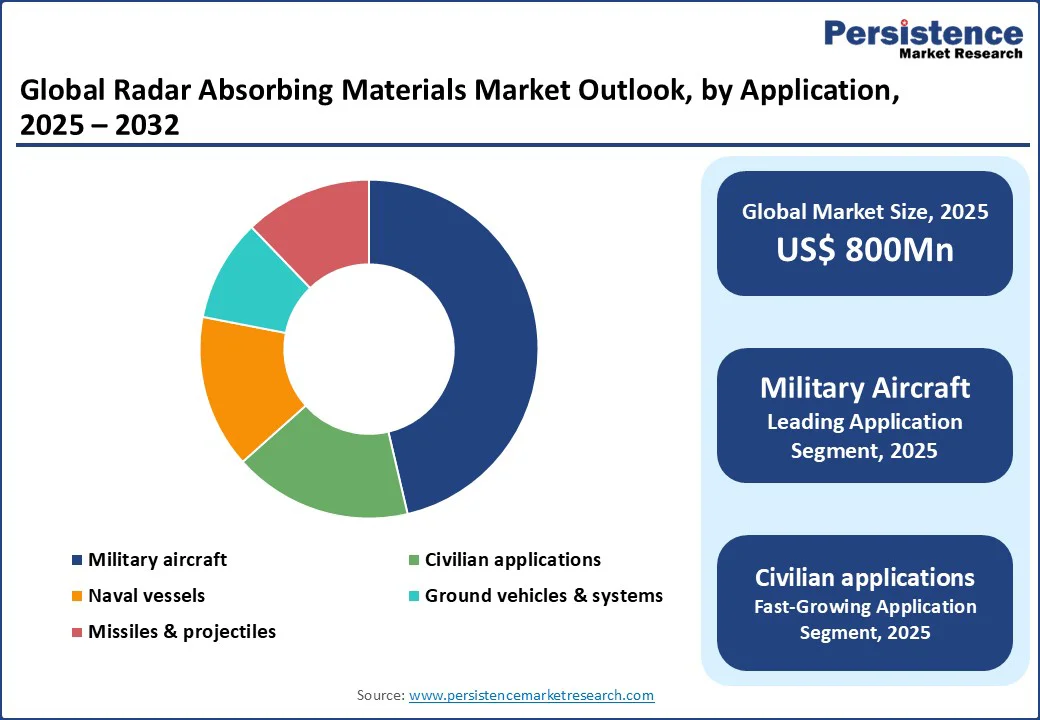

- Leading Application: Military aircraft leads with a 38% share, reflecting its critical role in enhancing stealth and survivability in aerial combat.

- Historical Growth: Industry recorded a CAGR of 2.3% from 2019 to 2024, driven by initial adoption in stealth aircraft and naval projects.

| Key Insights | Details |

|---|---|

|

Radar Absorbing Materials Market Size (2025E) |

US$0.8 Bn |

|

Market Value Forecast (2032F) |

US$1.0 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

3.8% |

|

Historical Market Growth (CAGR 2019 to 2024) |

2.3% |

Market Dynamics

Driver - Rising Demand for Stealth Technologies and Defense Modernization

The global surge in demand for stealth technologies is a primary driver of the radar absorbing materials market. According to the Stockholm International Peace Research Institute (SIPRI), world military expenditure reached $2,718 billion in 2024, marking a 9.4% increase from 2023 and the steepest y-o-y rise since 2009-10. Heightened geopolitical tensions in regions such as Eastern Europe and the Indo-Pacific are driving nations to prioritize stealth technologies that enhance survivability and reduce radar detection.

The United States Department of Defense continues to channel substantial resources into advanced programs such as the F-35 Lightning II and B-21 Raider, which rely on radar-absorbing materials to minimize radar cross-sections. These materials, including magnetic and dielectric absorbers, are vital in reducing electromagnetic reflections, allowing aircraft to operate with greater stealth in hostile environments.

Restraint - High Initial Costs and Need for Skilled Personnel

The radar absorbing materials market faces notable challenges stemming from high development costs and the need for specialized expertise. Manufacturing these advanced materials requires precise formulation of composites and coatings, often involving nanotechnology-based processes that demand substantial research and development investments. These costs are further elevated by the rigorous testing needed to validate performance under extreme conditions such as high temperatures, pressure, and mechanical stress, ensuring durability in demanding military environments.

Another barrier is the absence of standardized production techniques, which leads to performance inconsistencies, higher rework expenses, and delays in deployment. The shortage of skilled professionals trained in electromagnetic materials science compounds the issue, as expertise remains concentrated in regions such as North America and Europe, limiting accessibility for emerging markets. In addition, strict regulatory frameworks and export controls surrounding sensitive defense technologies add to the complexity, escalating timelines and expenses. Collectively, these challenges hinder broader adoption, discourage smaller defense contractors, and constrain applications beyond the military sector.

Opportunity - Innovation in Sustainable Systems and Multi-Application Use

Technological advancements in sustainable radar absorbing materials are creating strong growth opportunities across defense and civilian sectors. The shift toward eco-friendly solutions, including recyclable composites and bio-based polymers, supports global sustainability goals while reducing dependence on hazardous substances. Breakthroughs involving graphene and carbon nanotubes enable the development of ultra-thin, lightweight materials with superior absorption, making them ideal for next-generation unmanned aerial vehicles and satellite systems where agility and efficiency are critical.

The potential extends beyond defense, as these materials are increasingly applied in civilian technologies such as electromagnetic interference shielding for 5G infrastructure and automotive radar systems, broadening their commercial scope. In Europe, projects such as the Eurofighter Typhoon upgrades highlight the adoption of hybrid absorbers to enhance stealth capabilities, while emerging economies are investing in retrofitting older fleets with advanced coatings. Partnerships between defense companies, research institutions, and universities are accelerating innovation, paving the way for diverse revenue opportunities and wider adoption of sustainable radar absorbing technologies.

Category-wise Analysis

Material Type Insights

By material, the market is segmented into magnetic absorbers, dielectric absorbers, hybrid absorbers, impedance matching materials, metamaterial absorbers, frequency selective surfaces, and others. Magnetic absorbers dominate, holding approximately 45% share in 2025, due to their superior electromagnetic wave attenuation, effectiveness across wide frequency ranges, and integration into defense platforms.

Metamaterial absorbers are the fastest-growing segment, driven by increasing demand for advanced, multi-spectral absorption in next-generation defense systems. Metamaterials offer tunable properties for specific frequencies, enabling applications in hypersonic missiles and UAVs, where traditional materials fall short in performance and weight.

Form Insights

By form, the market is segmented into coatings & paints, sheets & films, foams & honeycombs, tiles & panels, molded components, and others. Coatings & paints dominate with a 39% share in 2025, driven by their affordability, ease of application, and versatility in defense and aerospace. Materials such as sprayable coatings are used for retrofitting aircraft and ships, providing effective radar absorption without significant structural changes.

Foams & honeycombs are the fastest-growing form segment, propelled by their use in lightweight, structural applications for UAVs and satellites. These forms offer enhanced durability and integration with composites, supporting advanced programs such as the B-21 Raider.

Application Insights

The global radar absorbing materials market is divided into military aircraft, naval vessels, ground vehicles & systems, missiles & projectiles, fixed installations, civilian applications, and others. Military aircraft leads with a 38% share in 2025, driven by the need for stealth in combat scenarios. Applications include fighters such as the F-35, where absorbers reduce RCS for enhanced survivability.

Civilian applications are the fastest-growing segment, as industries leverage absorbers for EMI shielding in telecommunications and automotive radar. This growth reflects the emphasis on 5G infrastructure and autonomous vehicles requiring interference-free operations.

Regional Insights

North America Radar Absorbing Materials Market Trends

North America dominates and is expected to account for 40% share in 2025, primarily driven by the United States. The region’s leadership is fueled by substantial defense spending, as the Department of Defense prioritizes stealth capabilities through flagship programs such as the Next Generation Air Dominance initiative. This focus is accelerating the adoption of advanced metamaterials in unmanned aerial vehicles, fighter jets, and hypersonic platforms, supported by collaborations with major defense contractors such as Lockheed Martin.

Beyond military applications, the region is also witnessing rising demand in civilian sectors. The rapid deployment of 5G networks and the growing use of automotive radar systems are driving the integration of radar absorbing materials for electromagnetic interference reduction. Regulatory initiatives, combined with advanced R&D infrastructure, further strengthen North America’s leadership in this evolving market.

Europe Radar Absorbing Materials Market Trends

Europe commands a substantial share of the global radar absorbing materials market, with leadership driven by the UK, Germany, and France. The UK is advancing its defense capabilities through major investments in the Tempest sixth-generation fighter program, creating strong demand for hybrid absorbers to enhance stealth. Germany is focusing on naval applications, with projects such as the F126 frigate highlighting the integration of advanced radar absorbing coatings to improve survivability at sea.

France continues to strengthen its position through Rafale fighter upgrades, incorporating frequency-selective surfaces that boost low-observability features. In addition, stringent European Union regulations on defense exports and sustainability are fostering innovations in eco-friendly and recyclable absorber materials. Collectively, these initiatives underline Europe’s role as both a technological innovator and a major consumer of radar-absorbing materials, supporting growth across air, naval, and multi-domain defense platforms.

Asia Pacific Radar Absorbing Materials Market Trends

Asia Pacific is emerging as the fastest-growing region, driven by rapid defense modernization and expanding industrial capabilities. China is at the forefront, with advancements such as the J-35A stealth fighter showcasing the integration of metamaterial absorbers for enhanced low observability. India’s Tejas Mk2 program and Japan’s F-X fighter initiative are further fueling demand, supported by rising defense budgets and heightened regional security challenges.

Beyond military applications, the region’s strong aerospace manufacturing base is accelerating adoption in civilian sectors, particularly in telecommunications and automotive radar systems. Growing investments in research, combined with government-backed defense initiatives and international collaborations, are positioning the Asia Pacific as a hub for innovation and large-scale deployment of radar absorbing technologies. This blend of military demand, industrial expansion, and civilian adoption underscores the region’s pivotal role in shaping future market growth.

Competitive Landscape

The global radar absorbing materials market is highly competitive, with global and regional players competing through innovation, competitive pricing, and reliability. The rise of sustainable materials and multi-spectral absorbers intensifies competition, as companies strive to meet the diverse needs of defense and civilian sectors. Strategic partnerships, mergers, and certifications for military standards are key differentiators in this dynamic market.

Key Developments

- July 2025: FibreCoat GmbH, based in Germany, announced the development of a fiber-reinforced composite material aimed at improving stealth performance. The innovation was designed to reduce the radar visibility of aircraft, tanks, and spacecraft by enhancing absorption properties, marking a significant advancement in defense materials technology.

- August 2025: GC Shield (Graphene Composites Ltd.) announced the development of a next-generation ballistic and blast protection system, integrating advanced materials to improve lightweight protection and electromagnetic/radar absorbing performance.

Companies Covered in Radar Absorbing Materials Market

- BAE Systems

- Lockheed Martin

- Northrop Grumman

- Laird / Lairdtech

- Parker Hannifin

- Panashield

- Mast Technologies

- Soliani EMC

- Arc Technologies

- Hitek

Frequently Asked Questions

The radar absorbing materials market is projected to reach US$0.8 Bn in 2025.

Rising demand for stealth technologies, advancements in material science, and government initiatives for defense modernization are key drivers.

The radar absorbing materials market is poised to witness a CAGR of 3.8% from 2025 to 2032.

Innovations in sustainable materials and multi-application solutions, such as EMI shielding, present significant growth opportunities.

BAE Systems, Lockheed Martin, Northrop Grumman, and Laird / Lairdtech are among the leading players, known for their defense-focused solutions.