- Semiconductor Materials & Components

- Programmable Logic Controller Market

Programmable Logic Controller Market Size, Share, and Growth Forecast, 2026 - 2033

Programmable Logic Controller Market by PLC Type (Modular PLC, Compact PLC, Rack-Mounted PLC), Product Size (Nano PLC, Micro PLC, Large PLC), Component Type (Hardware, Software, Services) Industry (Automotive, Oil & Gas, Energy & Utilities, Food & Beverages, Chemicals & Petrochemicals, Pharmaceuticals, Semiconductor & Electronics, Water & Wastewater Treatment, Misc.) and Regional Analysis for 2026 - 2033

Programmable Logic Controller Market Size and Trends Analysis

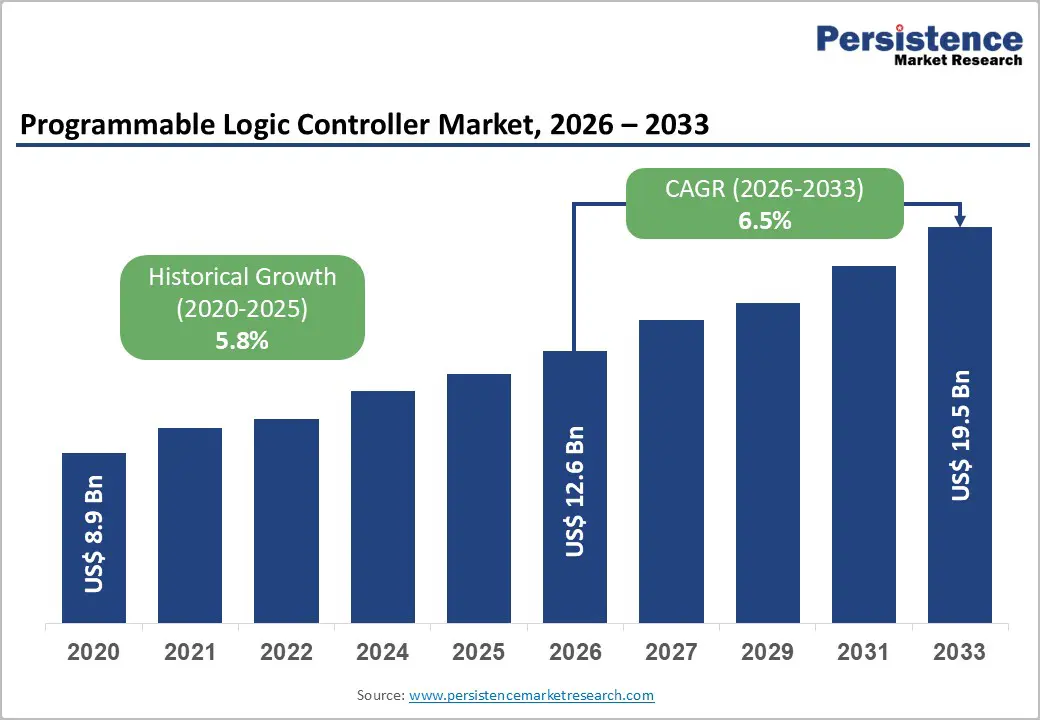

The global programmable logic controller (PLC) market size is likely to be valued at US$12.6 billion in 2026 and is projected to reach US$19.5 billion by 2033, growing at a CAGR of 6.5% during this forecast period. This growth trajectory reflects the accelerating adoption of automated control systems across industrial sectors, driven by Industry 4.0 transformation initiatives, increasing labour costs, and the critical need for operational efficiency. The market's expansion is supported by over 70 million PLCs currently deployed globally, with more than 62% of manufacturing facilities worldwide relying on PLC systems for real-time monitoring and automation tasks.

The shift toward integrated IoT and AI-enabled control systems has elevated the strategic importance of PLCs beyond traditional machine control to become foundational elements of intelligent, interconnected production ecosystems. Historical data indicate the market grew from US$8.9 billion in 2020 to US$12.6 billion in 2026, demonstrating a historical CAGR of 5.8%, with acceleration anticipated through 2033 as digital transformation initiatives mature across emerging and developed economies.

Key Industry Highlights:

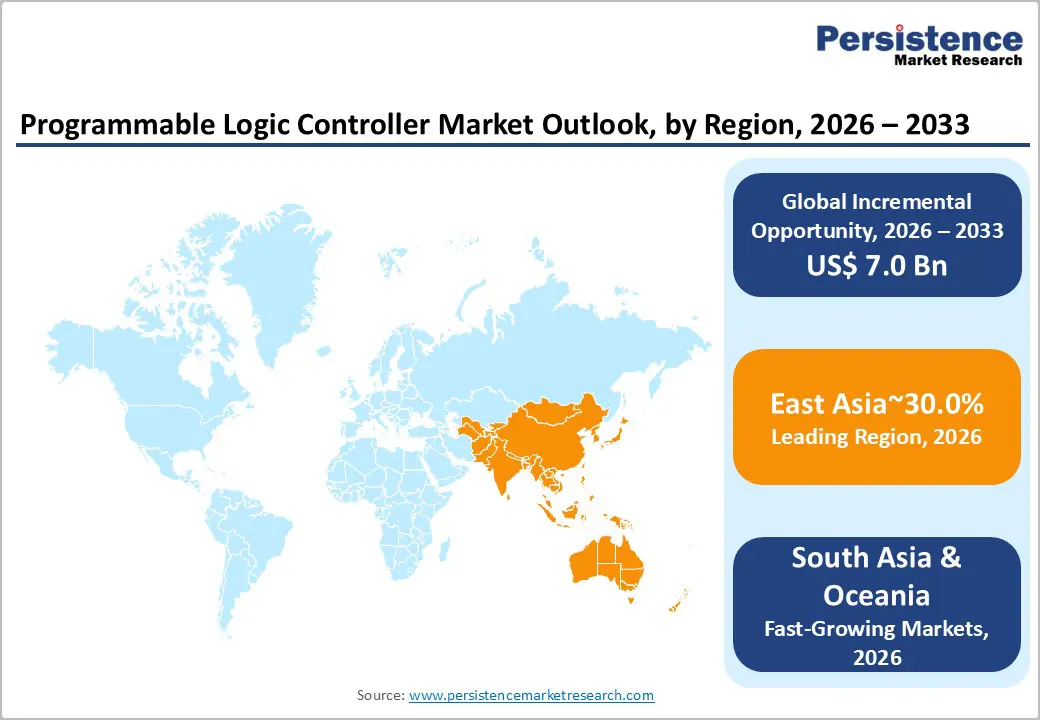

- Regional Leadership: East Asia leads the global market with ~30% share, driven by China’s state-backed investments in robotics, AI, and smart manufacturing, alongside rapid automation adoption in automotive, electronics, and machinery sectors.

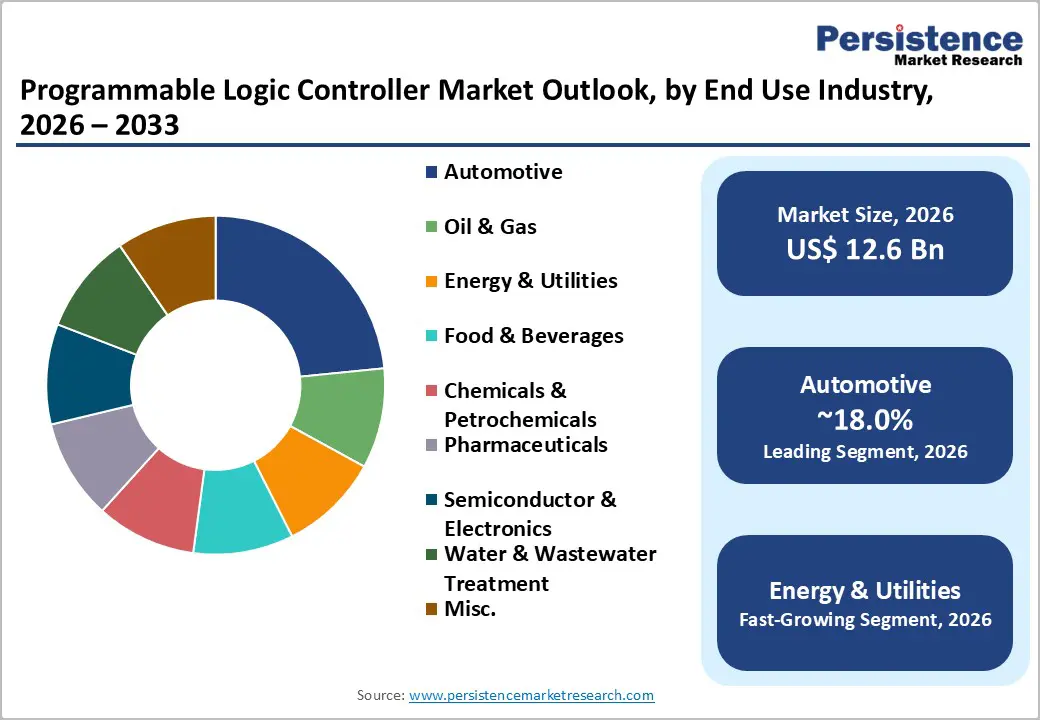

- Leading End-user: Automotive dominates with ~18% market share, reflecting PLC integration for assembly line automation, electrification, autonomous vehicle production, and efficiency optimisation.

- Fastest-Growing End-user: Energy & Utilities is expanding rapidly, fueled by renewable energy deployment, smart grid integration, and the need for real-time, high-reliability PLC systems for distributed power management.

- Dominant Component Type: Hardware leads with ~64% share, driven by large-scale industrial installations, reliability demands, and foundational control requirements, while Services is the fastest-growing component segment due to predictive maintenance and integration needs.

| Key Insights | Details |

|---|---|

|

Programmable Logic Controller Market Size (2026E) |

US$ 12.6 Bn |

|

Market Value Forecast (2033F) |

US$ 19.5 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.8% |

Market Dynamics

Driver - Industry 4.0 and Smart Manufacturing Transformation

Industry 4.0 represents a fundamental shift in how manufacturing organisations approach production control and operational optimisation. Rather than standalone machine controllers, modern PLCs must support integrated ecosystems that combine real-time data processing, cloud connectivity, and advanced analytics capabilities. The transformation toward smart manufacturing necessitates PLCs that can execute complex control logic while simultaneously handling vast data streams for edge analytics and cloud integration. According to the U.S. Department of Energy, the American manufacturing sector alone invested US$182 billion in automation and control systems in 2022, underscoring the substantial capital deployment required for this transition.

The programmable logic controller market has experienced a 21% growth in IoT and AI-based platform integration over the past year, enabling predictive maintenance, reduced downtime, and higher production efficiency. In China alone, the government announced in March 2025 a state-backed venture capital fund of approximately RMB 1 trillion over 20 years specifically targeted at robotics, AI, and smart manufacturing initiatives, representing an unprecedented commitment to scaling domestic automation deployment. This government-level investment directly accelerates PLC adoption as manufacturers upgrade their control infrastructure to support intelligent automation.

The integration of digital twin technology, now embedded in over 16% of global PLC systems, offers enhanced simulation and remote monitoring capabilities, with over 2.3 million new PLCs projected to include digital twin compatibility by 2026. As manufacturers recognize that Industry 4.0 implementation requires foundational improvements to their control architecture, the programmable logic controller market continues to benefit from the structural transformation of global manufacturing.

Rise in Demand for Process Automation and Labor Cost Optimization

Rising labor costs, workforce ageing, and the competitive imperative to enhance productivity drive sustained investment in automation solutions across both developed and emerging economies. Nearly 74% of industrial plants in 2023 reported adopting PLCs specifically to enhance productivity and cut down time through predictive control systems. The automotive sector exemplifies this trend: in India, 42% of production lines are now roboticized, reducing downtime by 30–50% and generating approximately US$300 million in cumulative gains per plant.

China's industrial robotics market is heavily dependent on advanced PLC controls, largely driven by increasing labor costs and workforce shortages in manufacturing hubs. Over 90% of tier-1 automotive manufacturers in North America and Europe have upgraded their Programmable Logic Controller systems to support robotic arms and conveyor systems, reflecting a fundamental shift toward labour-independent production models.

The pharmaceutical sector demonstrates similar patterns, with machine-vision technologies integrated into PLC-based systems achieving 20% faster batch releases. As global competition intensifies and manufacturers seek to maintain cost competitiveness despite labor constraints, the economic justification for advanced PLC systems continues to strengthen across all major manufacturing regions.

Cybersecurity Mandates and Regulatory Compliance Requirements

Industrial cybersecurity has evolved from a secondary consideration to a critical strategic imperative, particularly following escalating cyberattacks on critical infrastructure and manufacturing facilities. The IEC 62443 cybersecurity standard series, which establishes comprehensive frameworks for industrial automation and control systems security, has become increasingly mandatory across developed economies and large industrial enterprises. This standard encompasses security requirements across multiple dimensions: identification and authentication control, system integrity, data confidentiality, restricted data flow, and timely response to security events, all of which require PLCs with embedded security capabilities.

The integration of advanced cybersecurity features directly into Programmable Logic Controller hardware and firmware has become a standard market expectation, driving technology upgrades across existing installations. Patent activity related to AI inference at the edge and secure PLC communication protocols rose 23% in 2024, indicating sustained innovation in security-enhanced controllers.

Regulatory pressure varies by region. Europe's stringent operational technology (OT) cybersecurity requirements and North America's growing emphasis on critical infrastructure protection are compelling manufacturers to invest in PLCs that meet or exceed IEC 62443 compliance levels. The July 2024 announcement of Arc Embedded, the first OT/IoT security sensor embedded directly in Mitsubishi Electric PLCs, exemplifies how vendors are responding to this regulatory imperative by integrating real-time anomaly detection and enhanced cybersecurity directly at the process control level.[User Development] Organizations operating in regulated sectors such as energy, chemicals, and water treatment increasingly perceive PLC security compliance as non-negotiable, creating a sustained upgrade cycle that supports the market growth.

Restraint - High Integration Costs and Implementation Complexity

Custom integration costs remain a significant barrier to adoption, particularly for small and medium-sized enterprises (SMEs). Deployment and programming investments typically range from US$12,000 to US$38,000 per PLC unit, depending on industry complexity and system configuration requirements.

Beyond hardware acquisition, total implementation costs encompass systems engineering, control logic programming using IEC 61131-3 standards, integration with existing SCADA and HMI systems, and comprehensive staff training. These cumulative expenses create substantial upfront capital requirements that small manufacturers struggle to justify, particularly in price-sensitive markets such as India and Southeast Asia, where labor costs traditionally provided an economic offset to automation investment.

The technical sophistication required to design and implement redundant PLC systems for mission-critical applications further elevates implementation barriers, as specialized expertise commands premium consulting fees. Legacy system integration remains particularly challenging, as older equipment often requires custom adapter development and extensive engineering work to achieve seamless communication with modern PLC architectures. These structural cost and complexity barriers effectively limit market penetration in SME segments, constraining overall market growth and creating a bifurcated market where large enterprises drive advanced PLC adoption while SMEs remain reliant on older, lower-cost solutions.

Opportunity - Edge Computing Integration and Distributed Intelligence Architecture

Edge computing, the processing of data at or near the source of collection rather than in centralized cloud infrastructure, represents a fundamental architectural shift in industrial automation that fundamentally enhances PLC value propositions. The integration of edge computing capabilities in conjunction with advanced PLCs allows latency reduction by 12% and energy savings of 9%, particularly beneficial in high-volume production facilities where millisecond-level responsiveness is critical. This capability addresses a fundamental limitation of cloud-only approaches: cloud-dependent systems introduce unacceptable latency for real-time manufacturing processes such as precision welding, semiconductor fabrication, and high-speed packaging.

Smart PLCs are increasingly becoming integral components of distributed intelligence systems that combine local autonomous decision-making with periodic cloud-based analytics and optimization. The Programmable Logic Controller Market stands to benefit significantly as manufacturers recognize that hybrid edge-cloud architecture provides an optimal balance between real-time responsiveness and advanced analytics capabilities.

Over 60% of engineers now deploy advanced PLCs that support remote access, modular expansion, and seamless communication with SCADA and IoT platforms, indicating strong market validation of this hybrid approach. The opportunity for PLC vendors lies in developing controllers that seamlessly bridge edge and cloud computing, providing manufacturers with flexible deployment options and future-proof system architectures. This convergence creates substantial revenue opportunities not only in hardware sales but also in integration services, edge analytics software, and cloud connectivity platforms, where specialized consulting and services revenue is expanding at around 8%-9% CAGR.

The rise of cloud-based PLC systems represents an emerging business model opportunity within the broader market. Over 1.2 million PLC units are already connected to industrial cloud platforms, enabling centralised monitoring and management across global production networks while reducing response latency by up to 15%. This shift toward cloud-connected PLCs opens opportunities for subscription-based software licensing, managed services, and analytics-as-a-service business models. Equipment manufacturers in industries like automotive, semiconductor, and pharmaceuticals increasingly value the ability to manage hundreds of production facilities through centralized dashboards, driving demand for cloud-enabled Programmable Logic Controller systems with enhanced connectivity features.

Renewable Energy and Green Manufacturing Applications

The global energy transition toward renewable sources, such as solar, wind, hydro, and emerging technologies, is driving significant demand for advanced PLC systems capable of managing intermittent power, coordinating inverters, and integrating with smart grids. Green energy applications, including solar farms and wind turbines, have seen a 24% increase in PLC adoption, reflecting manufacturers’ response to environmental regulations and energy optimization initiatives. IoT-enabled PLCs enable energy savings of 18–25%, directly supporting sustainability goals and operational cost reduction. In India, government programs such as Make in India 2.0 and net-zero manufacturing targets are accelerating industrial automation, creating strong incentives for deploying advanced PLCs in energy-efficient production systems.

Beyond renewable energy, PLC vendors benefit from the manufacturing sector’s focus on sustainable production through digital twin integration and energy simulation. Virtual factory models allow companies to optimize equipment operation, model energy consumption, and validate sustainability improvements before implementation. This attracts ESG-focused manufacturers and aligns with global carbon reduction initiatives. Regulatory frameworks like the EU’s Carbon Border Adjustment Mechanism (CBAM) further enhance the business case for energy-optimising PLC systems. Companies that demonstrate measurable carbon reductions via PLC-enabled efficiency gain a competitive advantage in low-emission markets.

Category-wise Analysis

Component Type Insights

The Hardware segment dominates the Programmable Logic Controller Market with 64% market share in 2026, representing the foundational value layer where manufacturing, supply chain, and technical support converge. Hardware encompasses controllers of varying scales, from compact PLCs with limited I/O capacity to modular systems supporting hundreds of input and output modules, each addressing distinct application requirements and industry verticals. The predominance of hardware reflects the capital-intensive nature of manufacturing operations, where reliable, proven control devices command substantial procurement budgets. However, the Services segment represents the fastest-growing component category, expanding at 8.2% CAGR as industrial organisations transition from purely capital-expenditure (CapEx) purchasing models toward operational-expenditure (OpEx) approaches.

This shift toward services reflects evolving customer preferences and business model innovation within the Programmable Logic Controller Market. System integration complexity, particularly as PLCs incorporate IoT connectivity, cybersecurity features, and advanced analytics capabilities have elevated demand for vendor-provided consulting, implementation services, and ongoing technical support. Predictive maintenance services, remote diagnostics, and optimization services command premium pricing and create recurring revenue streams that benefit both PLC manufacturers and authorized system integrators.

Industry Insights

The automotive sector holds the leading position with approximately 18% market share in 2026, reflecting the structural importance of manufacturing automation in vehicle production and the regulatory pressures driving electrification and safety innovation. PLCs are indispensable in automotive environments, facilitating precision manufacturing processes, quality control, and automation of assembly lines. As the automotive sector embraces automation and advances in electric and autonomous vehicle technologies, the demand for PLCs continues to expand. PLCs ensure efficient production, reduce downtime, and enhance vehicle safety by integrating sophisticated control systems.

The increasing adoption of electric vehicles necessitates PLCs for battery management systems, charging infrastructure control, and advanced vehicle control systems, creating incremental demand beyond traditional powertrain automation. Global car registrations increased 5% in the first half of 2025, led by China, while the electric vehicle segment experienced particularly strong expansion

The Energy & Utilities sector represents the fastest-growing end-use segment, driven by the energy transition toward renewable sources and the increasing complexity of grid management as distributed generation becomes prevalent. The Programmable Logic Controller Market benefits from renewable energy deployment, where sophisticated control systems manage power generation, battery storage, grid synchronization, and demand response capabilities. Smart grid initiatives across developed economies require advanced PLCs capable of processing vast amounts of real-time data while maintaining deterministic, fail-safe operational characteristics.

The energy sector's emphasis on operational reliability and cybersecurity compliance creates sustained demand for premium-tier PLC systems with built-in redundancy, safety certification, and security hardening. Industrial utilities increasingly invest in monitoring and control infrastructure to optimise operations, reduce emissions, and integrate renewable sources, all applications requiring advanced PLC systems.

Regional Insights and Trends

North America Programmable Logic Controller Market Trends

North America holds 28% of the global Programmable Logic Controller Market share, with the United States positioned as the global leader in advanced automation technology development and deployment. High capital intensity across manufacturing and industrial sectors, combined with elevated labor costs and strong emphasis on operational efficiency, creates sustained demand for sophisticated PLC systems. The U.S. leads the North American market, driven by the existence of major PLC vendors and top companies, coupled with substantial research and development resources tailoring solutions for diverse customer bases.

Smart infrastructure initiatives and Industry 4.0 adoption drive regional growth, with high spending on incorporating artificial intelligence and IoT into PLC systems for automation and predictive maintenance across numerous sectors. North America's manufacturing sector has demonstrated strength in adopting advanced automation, with over 90% of tier-1 automotive manufacturers upgrading PLC systems to support robotic integration.

The regulatory environment emphasises safety, cybersecurity, and environmental compliance factors, driving demand for premium-grade PLC systems with enhanced security features, redundancy capabilities, and comprehensive monitoring. The October 2025 launch of Rockwell Automation's ControlLogix 5590 PLC, featuring 80 MB user memory, dual 1-Gigabit Ethernet ports with CIP Security, and expanded motion/robotics capabilities, exemplifies vendor innovation responding to North American customer requirements for integrated, scalable control platforms

East Asia Programmable Logic Controller Market Trends

East Asia commands a 30% share of the global Programmable Logic Controller market, positioned as the fastest-growing region, with particularly strong momentum in China, South Korea, and Japan.[User Data] China's manufacturing sector has emerged as the primary growth engine for PLC adoption, with the country accounting for 54% of global industrial robot deployments in 2024, a proxy metric indicating substantial concurrent PLC system deployment. The government's March 2025 announcement of a RMB 1 trillion state-backed venture capital fund targeted at robotics, AI, and smart manufacturing directly accelerates PLC adoption across automotive, electronics, and machinery manufacturing sectors.

The rapid automation demand across electronics and automotive manufacturing, fueled by rising labour costs, workforce ageing, and productivity imperatives, drives substantial PLC market expansion. Chinese manufacturers have achieved particular sophistication in production automation, with companies like ABB investing heavily in local manufacturing and R&D capacity. In July 2025, ABB launched three new robot families produced at its Shanghai Mega Factory, integrating AI and cloud technologies to provide flexible, scalable solutions for mid-market and SME customers with a strategic move reflecting recognition that PLC-enabled automation increasingly addresses SME segments in addition to large enterprises.

Japan and South Korea demonstrate distinct characteristics within East Asia, with Japan maintaining a strong demand for high-precision, deterministic PLCs used in semiconductor manufacturing and automotive production. South Korea's shipyards and semiconductor fabrication facilities specify redundant PLC clusters for mission-critical uptime, anchoring high-margin orders. The region's emphasis on manufacturing excellence and quality drives demand for premium PLC systems capable of achieving tight process control and advanced diagnostics.

Europe Programmable Logic Controller Market Trends

Europe represents 26% of the global programmable logic controller market share. Germany is dominant and leverages its position as the continent's manufacturing powerhouse and innovation leader in industrial automation technology. The European Union's economic growth projection of 1.1% in 2025, supported by resilient household consumption and investment despite trade tensions, provides a measured but stable backdrop for industrial capital equipment, including PLCs.

Automotive manufacturing remains the dominant end-use sector in Europe, particularly given the region's concentration of premium vehicle manufacturers and the structural complexity of electrification-driven retooling. European automotive production has experienced recent headwinds, declining 2.6% in 2024, attributed to CO2 targets, energy costs, and trade tariffs, yet EU-made vehicles maintain competitive strength in export markets to the UK, U.S., and Türkiye.

Competitive Landscape

The global Programmable Logic Controller (PLC) market is characterised as semi-consolidated with moderate fragmentation, where a few major multinational companies dominate a large portion of the market while numerous smaller players cater to niche and regional demands. Leading companies such as Siemens AG, Rockwell Automation (Allen-Bradley), Mitsubishi Electric Corporation, Schneider Electric SE, and Omron Corporation drive the market through extensive product portfolios, global distribution networks, and continuous innovation in areas like AI integration, edge computing, and cybersecurity-enabled PLCs.

Other notable players, including ABB, Emerson Electric (GE Fanuc), and Bosch Rexroth, contribute specialized solutions and regional expertise, enhancing competition. The presence of smaller and emerging companies creates additional fragmentation, especially in cost-sensitive and customized industrial applications. The market’s structure enables dominant players to set technological trends, while smaller vendors provide flexibility, specialized solutions, and localized support, making the overall PLC market semi-consolidated yet dynamic.

Key Industry Developments

- In October 2025 - Rockwell Automation: Launched the ControlLogix 5590 PLC, a high-performance integrated controller featuring advanced safety, built-in cybersecurity, multidiscipline control, up to 80 MB user memory, and dual 1-Gigabit Ethernet ports with CIP Security. This development enhances operational efficiency, system scalability, and secure high-speed automation across complex industrial processes.

- In April 2023 - Siemens: Launched the Simatic S7-1500V, the first virtual PLC, offering hardware-independent, software-based automation with central management via Industrial Edge. This enables flexible IT-OT integration, scalable PLC projects, and enhanced remote diagnostics, marking a significant step in software-driven, adaptable industrial automation.

Companies Covered in Programmable Logic Controller Market

- ABB Ltd.

- Mitsubishi Electric Corporation

- Rockwell Automation, Inc.

- Schneider Electric SE

- Siemens AG

- Honeywell International Inc.

- General Electric Company (GE)

- IDEC Corporation

- Omron Corporation

- Robert Bosch GmbH

- Bosch Rexroth AG

- Emerson Electric Co.

- Hitachi, Ltd.

- Panasonic Industry Co., Ltd.

- Delta Electronics, Inc.

- Fuji Electric Co., Ltd.

Frequently Asked Questions

The global programmable logic controller market is projected to be valued at US$ 12.6 Bn in 2026.

The Modular PLC segment is expected to account for approximately 45.0% of the Global Programmable Logic Controller Market by PLC Type in 2026.

The market is expected to witness a CAGR of 6.5% from 2026 to 2033.

The Programmable Logic Controller market growth is driven by Industry 4.0 adoption, smart manufacturing transformation, rising process automation needs, labor cost optimization, IoT/AI integration, digital twin technology, and stringent cybersecurity and regulatory compliance requirements.

Key market opportunities in the Programmable Logic Controller market lie in edge computing integration, distributed intelligence architectures, cloud-connected PLC systems, and adoption in renewable energy and green manufacturing applications supported by digital twin technology and energy optimization initiatives.