- Processed Food

- Processed Meat Market

Processed Meat Market Size, Share, and Growth Forecast, 2025 - 2032

Processed Meat Market by Product Type (Hamburgers, Fried Sausages, Kebabs, Chicken Nuggets, Others), Packaging (Chilled, Frozen, Canned), Meat Type (Beef, Pork, Chicken, Mutton, Others), and Regional Analysis for 2025 - 2032

Processed Meat Market Size and Trend Analysis

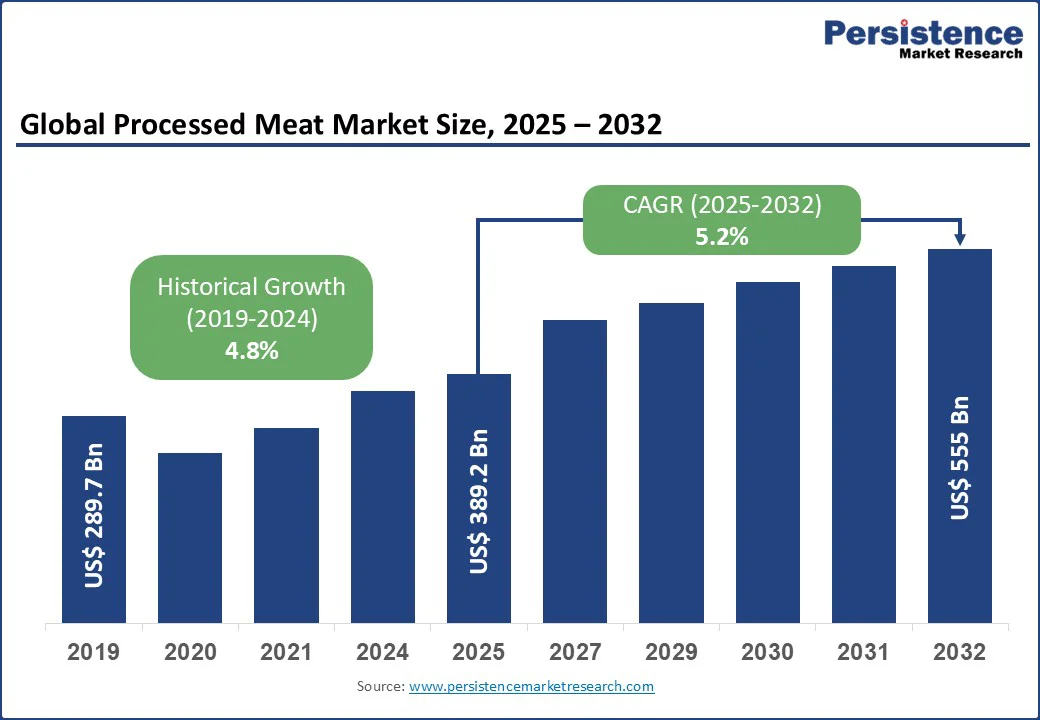

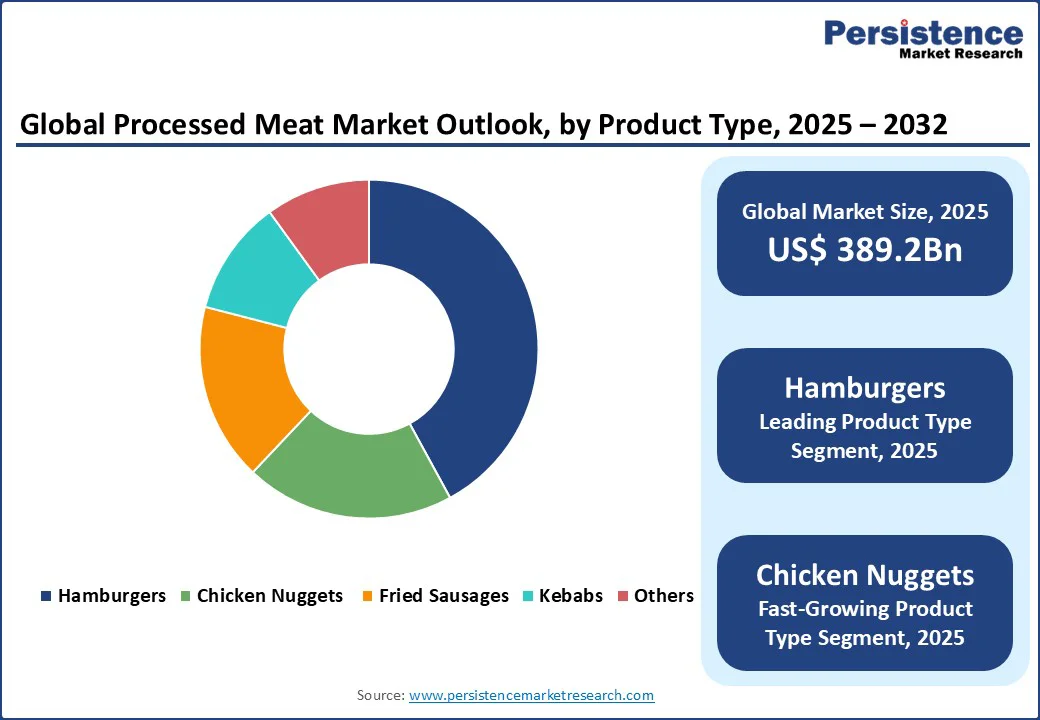

The global processed meat market size is likely to be value at US$389.2 Bn in 2025 reach US$555 Bn by 2032, growing at a CAGR of 5.2% during the forecast period from 2025 to 2032. It is experiencing robust growth, fueled by rising consumer demand for convenient, ready-to-eat food products and increasing urbanization.

Key Industry Highlights

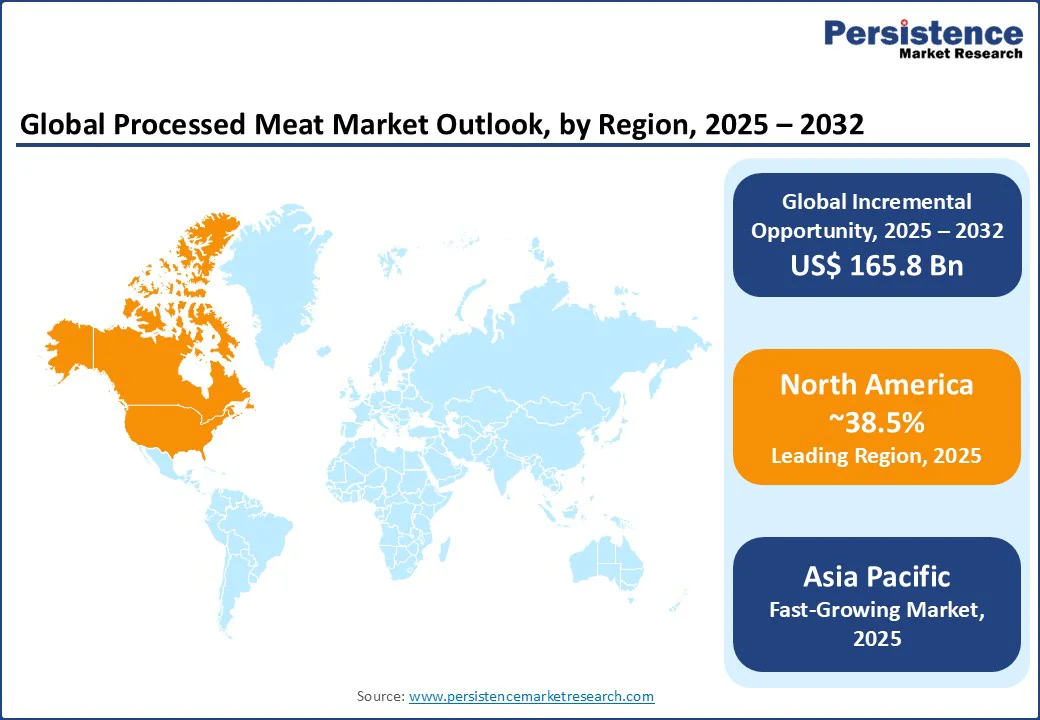

- Leading Region: North America holds 38.5% share in 2025, driven by high consumption of processed meats in the U.S. and Canada, supported by a strong fast-food culture and advanced retail infrastructure.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region, propelled by rapid urbanization, rising disposable incomes, and increasing adoption of Western dietary habits in countries such as China and India.

- Investment Plans: The U.S. Department of Agriculture reported a $1 billion investment in 2024 to expand meat processing capacity, boosting supply chain efficiency and processed meat production.

- Dominant Product Type: Hamburgers account for 42.1% share, driven by their popularity in quick-service restaurants and widespread consumer preference.

- Leading Packaging Type: Chilled packaging dominates with a 55.3% market share, favored for maintaining product freshness and quality in retail settings.

| Key Insights | Details |

|---|---|

| Processed Meat Market Size (2025E) | US$ 389.2Bn |

| Market Value Forecast (2032F) | US$ 555Bn |

| Projected Growth (CAGR 2025 to 2032) | 5.2% |

| Historical Market Growth (CAGR 2019 to 2024) | 4.8% |

Market Dynamics

Driver: Rising Demand for Convenient and Ready-to-Eat Food Products

The global processed meat market is experiencing significant growth due to the increasing demand for convenient, ready-to-eat food products. Urbanization, busy lifestyles, and the growing prevalence of dual-income households have heightened the need for quick meal solutions.

Processed meats, such as hamburgers, fried sausages, and chicken nuggets, cater to this demand due to their ease of preparation and long shelf life. According to the Food and Agriculture Organization (FAO), global meat consumption is projected to increase by 14% by 2030, with processed meats accounting for a significant share.

In the U.S., the National Restaurant Association reported that 60% of consumers prefer quick-service restaurants for convenience, driving demand for processed meat products. In emerging economies such as India and China, the expansion of retail chains and e-commerce platforms, such as Amazon Fresh, further boosts accessibility.

Companies such as Tyson Foods and JBS S.A. have reported increased sales of pre-packaged processed meats in 2024, underscoring the sustained demand for convenience-driven products through 2032.

Restraint: Health Concerns and Regulatory Challenges

The processed meat market faces challenges due to growing health concerns and stringent regulatory standards. Processed meats, often high in sodium, preservatives, and saturated fats, are linked to health risks such as cardiovascular diseases and cancer, as highlighted by the World Health Organization. This has led to declining consumer confidence in some markets, particularly in developed regions such as Europe.

Additionally, regulatory bodies, such as the European Food Safety Authority, impose strict guidelines on additives and labeling, increasing compliance costs for manufacturers. In 2023, raw material price volatility, particularly for pork and beef, further strained profit margins, with beef prices rising by 8% globally, per the FAO.

The rise of plant-based meat alternatives, such as those offered by Beyond Meat, also poses competitive pressure, particularly in health-conscious markets, limiting growth potential for traditional processed meat products.

Opportunity: Growth in Plant-Based and Hybrid Processed Meat Products

The rising consumer interest in sustainable and healthier food options presents significant opportunities. The growing popularity of plant-based and hybrid meat products, which combine traditional meat with plant-based ingredients, aligns with sustainability trends and health-conscious diets. The Plant Based Foods Association reported that plant-based meat sales in the U.S. grew by 45% from 2020 to 2023, indicating strong consumer interest.

Companies such as Tyson Foods and Maple Leaf Foods are investing in hybrid products, blending pork or chicken with plant-based proteins to appeal to flexitarian consumers.

Additionally, advancements in food processing technologies enable the development of low-sodium and preservative-free processed meats, addressing health concerns. Government initiatives, such as the EU’s Farm to Fork Strategy, promote sustainable food systems, encouraging manufacturers to innovate with eco-friendly packaging and cleaner labels, creating growth opportunities through 2032.

Category-wise Analysis

By Product Type

- Hamburgers hold the largest market share, approximately 42.1% in 2025, due to their widespread popularity in quick-service restaurants and retail settings. Their versatility, affordability, and appeal across age groups drive demand, particularly in North America and Europe. Companies such as Tyson Foods and JBS S.A. lead with extensive hamburger portfolios, catering to fast-food chains such as McDonald’s and Burger King, which reported a 5% sales increase in hamburger-based meals in 2024.

- Chicken nuggets are the fastest-growing product type, driven by rising consumer preference for poultry-based processed meats due to their lower cost and perceived health benefits compared to red meat. The expansion of retail frozen food sections and kid-friendly meal options in the Asia Pacific and North America fuels growth, with brands such as Pilgrim’s Pride innovating with flavored and organic nugget offerings.

By Packaging

- Chilled packaging accounts for 55.3% share in 2025, favored for maintaining the freshness, texture, and flavor of processed meats. Its dominance is driven by widespread use in retail supermarkets and hypermarkets, particularly in North America and Europe, where consumers prioritize quality. Companies such as Hormel Foods and WH Group leverage advanced cold chain logistics to ensure product availability in chilled formats.

- Frozen packaging is the fastest-growing segment, propelled by increasing demand for long-shelf-life products and the expansion of e-commerce grocery platforms. The convenience of frozen processed meats, such as chicken nuggets and sausages, appeals to busy consumers in urban areas of the Asia Pacific. Innovations in freezing technologies by players such as Cargill enhance product quality, driving adoption through 2032.

By Meat Type

- Beef accounts for the largest share, approximately 40.2% in 2025, due to its widespread use in hamburgers and kebabs, particularly in North America and the Middle East. Its rich flavor and high protein content drive consumer preference, with companies such as JBS S.A. and Cargill dominating through extensive supply chains and premium beef offerings for fast-food and retail markets.

- Chicken is the fastest-growing meat type, driven by its affordability, versatility, and growing consumer preference for leaner proteins. The rise in poultry consumption in the Asia Pacific, particularly in China and India, is supported by increasing production capacities. Brands such as BRF S.A. and Nippon Meat Packers innovate with chicken-based processed meats, such as nuggets and sausages, to meet evolving dietary trends.

Regional Insights

North America Processed Meat Market Trends

North America dominates in 2025, capturing 38.5% share, propelled by high consumption levels in both the U.S. and Canada. The strong fast-food culture in the U.S., centered on quick-service restaurants, heavily relies on staples such as hamburgers and chicken nuggets, driving significant demand.

Canada’s increasing appetite for chilled and frozen processed meat products, as highlighted by the Canadian Meat Council, further fuels regional growth. Leading companies such as Tyson Foods and Hormel Foods dominate the processed meat market, leveraging extensive distribution networks that effectively serve both retail outlets and the foodservice industry.

Additionally, consumer preferences are shifting toward convenient, high-protein meal options, reinforcing processed meat’s popularity. These combined factors position North America for continued expansion and a strong market presence through 2032.

Asia Pacific Processed Meat Market Trends

Asia Pacific is the fastest-growing region. This growth is driven by rapid urbanization, increasing disposable incomes, and evolving dietary habits, especially in populous countries such as China and India. China, as the world’s largest pork consumer, significantly fuels demand for processed pork products. Major players such as WH Group have reported substantial sales increases in 2024, reflecting strong market momentum.

Meanwhile, India’s burgeoning fast-food industry, with popular chains such as KFC expanding rapidly, is boosting demand for chicken nuggets, hamburgers, and other processed meat items. The region benefits from expanding retail infrastructure and robust e-commerce platforms such as Alibaba, which enhance product accessibility and convenience for consumers. Additionally, government efforts to improve food safety standards and investments in cold chain logistics further reinforce market expansion.

Europe Processed Meat Market Trends

Europe is the second fastest-growing processed meat market, fueled by robust demand in key countries such as Germany, France, and the UK. The region’s growth is supported by stringent food safety regulations that ensure high product quality, bolstering consumer confidence.

There is an increasing preference for premium processed meats, with chilled sausages and hamburgers dominating retail shelves and foodservice menus asuch as. Germany’s meat processing sector, led by industry giants such as Danish Crown, exemplifies the region’s commitment to quality and tradition.

Furthermore, the European Union’s strong emphasis on sustainable food systems, particularly through initiatives such as the Farm to Fork Strategy, is driving innovation in healthier, low-sodium options and environmentally friendly packaging. These efforts align with growing consumer demand for products that are both nutritious and sustainable.

Competitive Landscape

The global processed meat market is highly competitive and fragmented, with numerous global and regional players vying for market share. Leading companies, such as Tyson Foods Inc., JBS S.A., and WH Group, dominate through extensive product portfolios, advanced processing technologies, and global distribution networks.

Regional players, such as Nippon Meat Packers in Asia Pacific, focus on localized offerings. Companies are investing in sustainable packaging and healthier product formulations to align with consumer trends, enhancing their market position through 2032.

Key Industry Developments

- July 2025: Tyson Foods introduced its new Tyson Simple Ingredient Nuggets. These nuggets are crafted with 100% all-natural white meat chicken, mozzarella and parmesan cheeses, and simple, savory seasonings. They are gluten-free, contain no added sugar, and offer 23 grams of protein with just 1-2 grams of total carbs per serving. The product is available in two varieties: Original and Spicy.

- September 2024: JBS S.A. announced an investment of R$70 million (approximately US$12.5 million) in its metal packaging subsidiary. This investment aims to enhance production capacity, particularly for deli meat packaging, with the goal of increasing output by 180% by November 2024. The funds are being allocated equally between Zempack’s aerosol can facility in Guaiçara and the packaging production at Lins, both located in São Paulo state.

Companies Covered in Processed Meat Market

- Tyson Foods Inc.

- JBS S.A.

- WH Group (Smithfield Foods)

- Cargill Inc.

- Hormel Foods Corporation

- BRF S.A.

- Pilgrim’s Pride Corporation

- Maple Leaf Foods Inc.

- Nippon Meat Packers Inc.

- Danish Crown Group,

- Others

Frequently Asked Questions

The processed meat market is projected to reach US$389.2 Bn in 2025.

Rising demand for convenient, ready-to-eat food products and expanding quick-service restaurant chains are key market drivers.

The processed meat market is poised to witness a CAGR of 5.2% from 2025 to 2032.

The rising demand for plant-based and hybrid processed meat products is the key market opportunity.

Tyson Foods Inc., JBS S.A., WH Group, and Hormel Foods Corporation are key market players.