- Medical Devices

- Reprocessed Single-Use Devices Market

Reprocessed Single-Use Devices Market Size, Share, and Growth Forecast, 2025 - 2032

Reprocessed Single-Use Devices Market by Product Type (Cardiovascular Catheters, Electrophysiology Catheters, Laparoscopic Instruments, Gastroenterology Devices, Orthopedic External Fixation Devices, General Surgery Instruments), Class, End-use, Regional Analysis for 2025 - 2032

Reprocessed Single-Use Devices Market Size and Trend Analysis

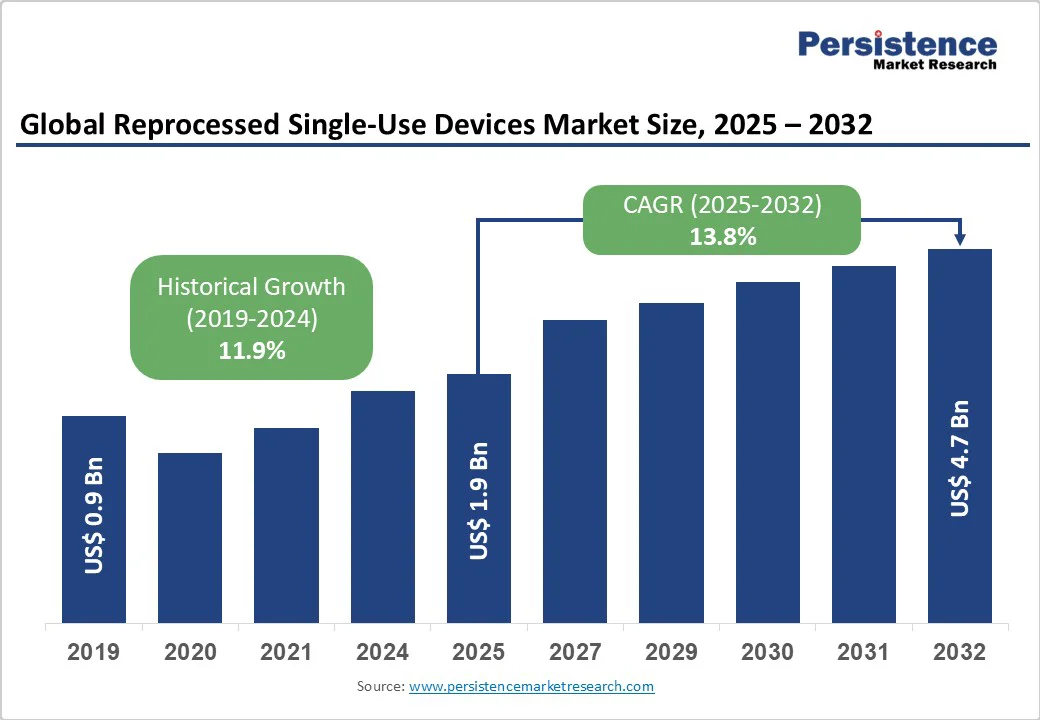

The global reprocessed single-use devices market size is likely to value at US$1.9 Bn in 2025 and reach US$4.7 Bn by 2032, growing at a CAGR of 13.8% during the forecast period from 2025 to 2032.

The reprocessed single-use devices market is witnessing robust growth, driven by escalating healthcare costs, sustainability initiatives, and regulatory support for eco-friendly medical practices.

Key Industry Highlights:

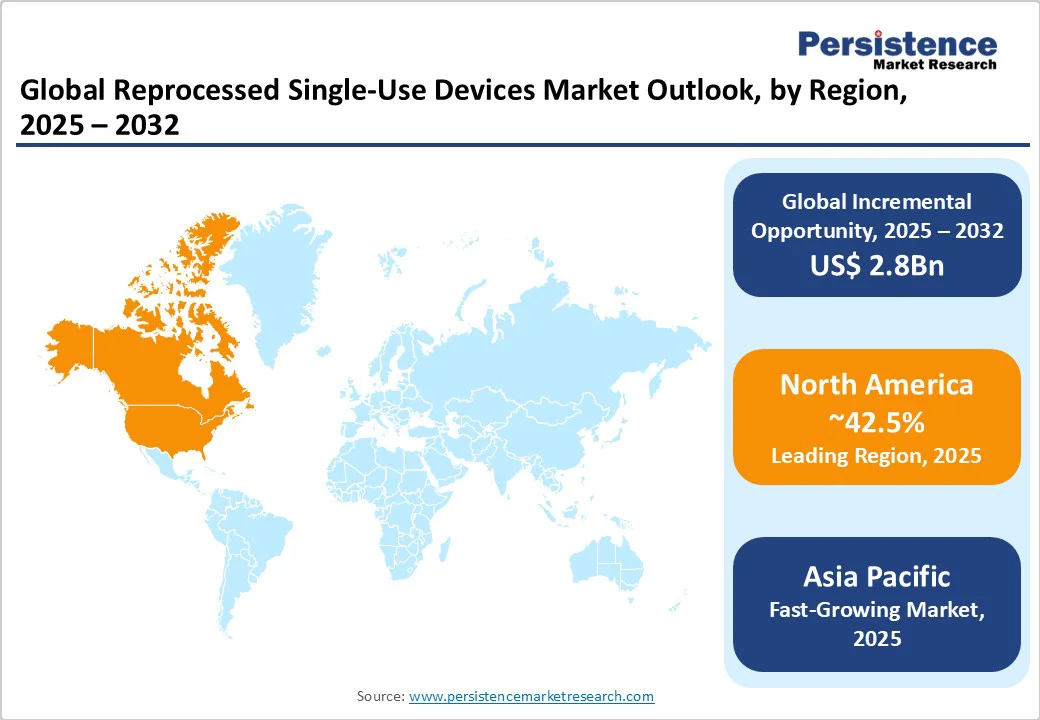

- Leading Region: North America is likely to account for a 42.5% share in 2025, propelled by stringent FDA regulations, high adoption in cost-conscious hospitals, and strong reprocessing infrastructure in the U.S.

- Fastest-growing Region: Asia Pacific is the fastest-growing region, driven by rapid healthcare expansion, government sustainability mandates, and increasing surgical volumes in countries such as China and India.

- Investment Plans: Cardinal Health's Sustainable Technologies™ division collected 18.3 million single-use devices in fiscal 2022, diverting over 5.6 million pounds of waste from landfills. This initiative supports hospitals in achieving sustainability goals while maintaining high standards of patient care.

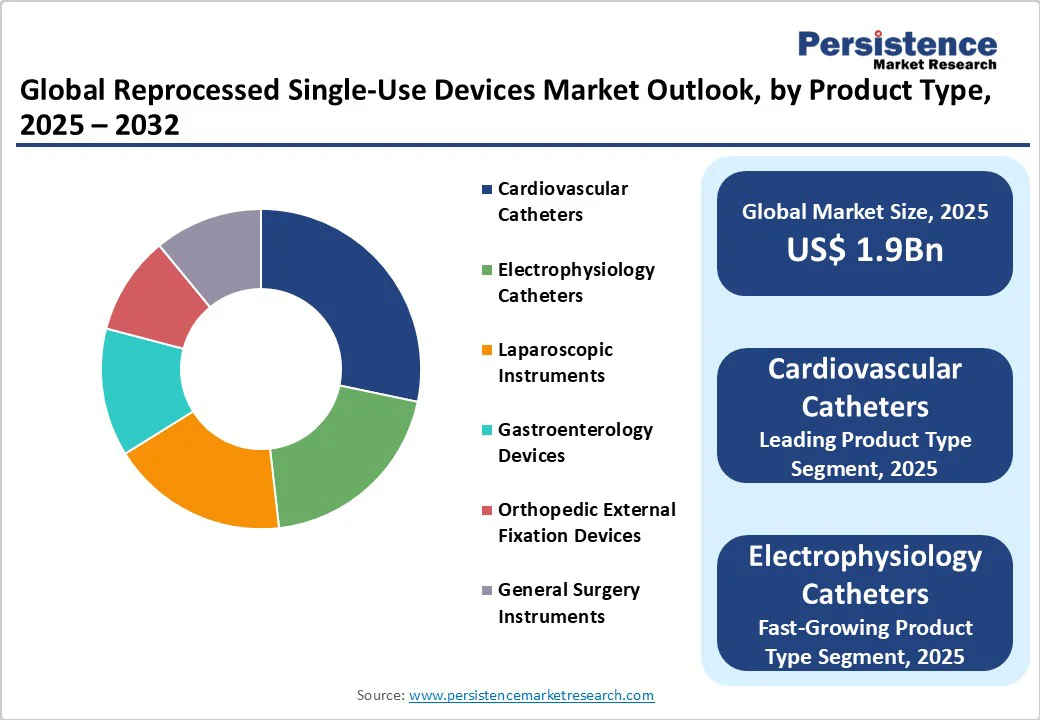

- Dominant Product Type: Cardiovascular Catheters, accounting for nearly 28.4% of the reprocessed single-use devices market share, due to their high usage in interventional procedures and significant cost savings through reprocessing.

- Leading End-use: Hospitals, contributing over 52.7% of market revenue, driven by large-scale procurement and integration of reprocessed devices in routine surgeries.

| Key Insights | Details |

|---|---|

| Reprocessed Single-Use Devices Market Size (2025E) | US$ 1.9Bn |

| Market Value Forecast (2032F) | US$ 4.7Bn |

| Projected Growth (CAGR 2025 to 2032) | 13.8% |

| Historical Market Growth (CAGR 2019 to 2024) | 11.9% |

Market Dynamics

Driver: Mounting Healthcare Costs and Cost-Saving Imperatives Fuel Market Expansion

The global reprocessed single-use devices market is experiencing substantial growth due to skyrocketing healthcare expenditures and the imperative for cost optimization in medical facilities worldwide. Reprocessed devices provide a viable alternative to virgin single-use items, reducing expenses by 40-60% without compromising patient safety, as validated by FDA guidelines.

The World Health Organization (WHO) reported that global health spending reached US$9.8 trillion in 2021, accounting for 10.3% of global GDP, with total spending at hospitals accounted for 65% to 84% of total health spending.

According to the Centers for Medicare & Medicaid Services (CMS), U.S. health care spending reached $4.9 trillion in 2023, equating to $14,570 per person., reprocessing programs in facilities such as Mayo Clinic have saved million since 2020.

As healthcare systems worldwide grapple with inflation and resource scarcity, reprocessed single-use devices position themselves as a cornerstone for financial resilience, driving market penetration through 2032 and enabling providers to allocate savings toward advanced treatments and patient care enhancements.

Restraint: Regulatory Compliance Challenges and Safety Perceptions Limit Adoption

The reprocessed single-use devices market faces significant challenges driven by stringent regulatory requirements and ongoing concerns about safety and efficacy. Regulatory agencies such as the FDA and EU Notified Bodies enforce rigorous validation processes, including microbial contamination testing, material durability assessments, and sterilization efficacy verification. These demanding standards elevate operational costs and complexity, creating substantial barriers for smaller reprocessing firms lacking extensive resources.

Conservative healthcare sectors remain hesitant, further slowing adoption rates. Although technological advancements in traceability and quality assurance have improved safety monitoring and risk mitigation, inconsistent regulatory frameworks across regions hinder seamless growth. The absence of globally harmonized guidelines exacerbates uncertainties, complicating approval pathways and fostering mistrust among providers and patients.

Addressing these regulatory and perception challenges through standardized international protocols is crucial to unlocking the reprocessed single-use devices market’s sustainability potential, reducing medical waste, and enabling broader acceptance of reprocessed single-use medical devices worldwide.

Opportunity: Sustainability Mandates and Green Healthcare Initiatives Unlock New Avenues

The growing emphasis on sustainability mandates and green healthcare initiatives is creating substantial opportunities for the reprocessed single-use devices market. Governments worldwide are increasingly integrating environmental criteria into healthcare policies, linking reimbursements and funding to providers’ adherence to low-carbon and waste-reduction practices. This regulatory momentum encourages hospitals and clinics to adopt reprocessed devices, which significantly reduce medical waste and carbon emissions.

In addition, insurers are beginning to incentivize sustainable procurement, making eco-friendly devices more financially attractive. Manufacturers are responding by innovating with biodegradable materials and enhanced reprocessing technologies that maintain safety while minimizing environmental impact.

This convergence of policy, economic incentives, and technological advances is expected to drive strong market growth through 2032. Ultimately, the trend supports a circular economy within healthcare, enabling stakeholders to reduce ecological footprints while improving cost efficiency, thereby transforming the industry’s approach to sustainability and patient care.

Category-wise Analysis

By Product Type

- Cardiovascular catheters are likely to account for the largest share, approximately 28.4% in 2025, due to their extensive use in minimally invasive procedures, such as angioplasty and stent placements, where reprocessing offers substantial cost reductions of up to 50% while adhering to biocompatibility standards. These devices, often discarded after single use despite remaining functional lifespan, benefit from advanced cleaning technologies that restore functionality without degradation. Leading players, such as Stryker and Cardinal Health, dominate with FDA-approved reprocessing lines, supplying major U.S. and European cath labs.

- Electrophysiology catheters represent the fastest-growing product type, driven by surging demand for electrophysiology studies and growing arrhythmia. Reprocessing these complex, wire-guided devices cuts costs and aligns with sustainability goals, with companies such as Innovative Health expanding automated validation systems for precision restoration.

By Class

- Class I devices command a leading share, around 55.2% in 2025, owing to their lower risk profile and straightforward reprocessing requirements, encompassing items such as laparoscopic graspers and tourniquet cuffs that undergo basic sterilization without complex electronics. The segment thrives on volume, with global surgical procedures surpassing 300 million annually per WHO data, emphasizing cost efficiency in resource-limited settings and driving widespread integration.

- Class II devices are the fastest-growing segment in reprocessing, fueled by advances in refurbishing moderate-risk products such as pulse oximeter sensors and sequential compression sleeves. These devices require stringent testing protocols to ensure electrical safety, material durability, and consistent performance after multiple reprocessing cycles.

By End-use

- Hospitals are projected to hold over 52.7% of the reprocessed single-use devices market revenue in 2025, primarily because they perform the majority of high-volume, complex medical procedures. These facilities often operate in-house reprocessing units, enabling them to reduce costs, manage waste more efficiently, and comply with sustainability mandates without compromising patient care.

- Ambulatory Surgical Centers (ASCs) are emerging as the fastest-growing end-use segment, driven by the rise in minimally invasive, same-day procedures. Their focus on operational efficiency and cost-effectiveness aligns with reprocessing benefits. Providers such as Hygia Health Services support ASCs with tailored, on-site reprocessing solutions that ensure quick turnaround and regulatory compliance.

Regional Insights

North America Reprocessed Single-Use Devices Market Trends

North America is a leading market and is likely to capture a 42.5% share in 2025. This dominance stems from a combination of mature regulatory oversight, high healthcare expenditure, and early adoption trends, particularly in the U.S. and Canada. The U.S. healthcare sector alone reached $4.9 trillion in 2023, according to CMS, underscoring the scale of spending and the urgent need for cost-efficient, sustainable solutions such as device reprocessing.

The Food and Drug Administration (FDA) plays a critical role in ensuring safety, mandating that reprocessed devices meet the same standards as new ones. This regulatory clarity has built trust among providers, encouraging adoption across major hospital systems.

Additionally, supportive policies from insurers and sustainability mandates have further accelerated integration. Canada, following similar environmental and cost-containment priorities, is also expanding its reprocessing infrastructure. Overall, North America's structured approach and innovation-friendly environment continue to drive the region's leadership in this sector.

Asia Pacific Reprocessed Single-Use Devices Market Trends

Asia Pacific is emerging as the fastest-growing region in the reprocessed single-use devices (SUDs) market, driven by rapid healthcare infrastructure development, rising surgical volumes, and increasing environmental awareness. Countries such as China and India are at the forefront of this growth, propelled by large populations and expanding access to surgical care.

In China, the medical equipment market reached 1.27 trillion Yuan (~US$179 billion) in 2023, according to the China Association of Medical Equipment. This growth aligns with national strategies promoting healthcare sustainability, including policies targeting medical waste reduction.

Reprocessing is gaining traction in hospitals, particularly for high-use devices in laparoscopic and minimally invasive procedures. Similarly, India’s focus on reducing healthcare costs while managing waste is fostering a favorable environment for reprocessed SUDs. Both countries are also investing in local reprocessing capabilities and regulatory frameworks. As demand for cost-effective, eco-conscious solutions intensifies, the Asia Pacific is poised to become a central hub for market expansion.

Europe Reprocessed Single-Use Devices Market Trends

Europe stands as the second fastest-growing region in the reprocessed single-use devices (SUDs) market, propelled by a strong regulatory foundation and a growing emphasis on environmental, social, and governance (ESG) principles. The implementation of the EU Medical Device Regulation (MDR) has established strict standards for safety, performance, and traceability, which reprocessed devices must meet, fostering increased trust among healthcare providers.

In parallel, the European Green Deal and the Circular Economy Action Plan are encouraging hospitals and manufacturers to adopt sustainable practices, including medical device reprocessing, to reduce healthcare waste and lower carbon footprints.

Countries such as Germany, the Netherlands, and the Nordic nations are leading the way, integrating reprocessed SUDs into national procurement strategies and hospital sustainability frameworks. With increasing public and institutional support for environmentally responsible healthcare, the region is seeing rapid adoption across high-volume specialties such as cardiology, gastroenterology, and orthopedics. Europe's policy-driven, sustainability-first approach continues to accelerate market growth and innovation.

Competitive Landscape

The global reprocessed single-use devices market is moderately consolidated, with key players leveraging regulatory expertise, technological innovations, and strategic partnerships to capture share. Dominated by established firms with FDA approvals and global footprints, the landscape features a mix of full-service reprocessors and specialized providers.

Competition centers on quality assurance, cost competitiveness, and sustainability certifications, with leaders expanding via acquisitions and R&D in automated systems. Regional dynamics influence strategies, from U.S.-centric compliance to Asia’s volume scaling.

Key Industry Developments:

- June 2025: In a landmark ruling, a U.S. District Court ordered Johnson & Johnson MedTech’s Biosense Webster unit to pay $442 million in damages for violating antitrust laws. The case involved allegations that the company withheld clinical and technical support from hospitals using reprocessed electrophysiology catheters, effectively blocking competition. The damages were initially awarded at $147 million but were tripled under antitrust law provisions.

- January 2025: Healthcare institutions in the Netherlands were permitted to reprocess single-use medical devices, including those bearing the CE mark. This policy change was part of the Dutch government’s Green Deal for Sustainable Healthcare, aimed at promoting more sustainable and cost-effective medical practices. The policy required adherence to strict quality management systems, limited reprocessing cycles, and annual audits to ensure compliance.

Companies Covered in Reprocessed Single-Use Devices Market

- Stryker

- SterilMed (Johnson & Johnson)

- Medline ReNewal

- Innovative Health

- Northeast Scientific

- Vanguard AG

- Cardinal Health

- ReNu Medical

- Hygia Health Services

- Midwest Reprocessing Center

- Centurion Medical Products

- Arjo

- Sterimed Inc.

- Others

Frequently Asked Questions

The Reprocessed Single-Use Devices market is projected to reach US$1.9 Bn in 2025.

Escalating healthcare costs and sustainability mandates in medical waste reduction are the key market drivers.

The Reprocessed Single-Use Devices market is poised to witness a CAGR of 13.8% from 2025 to 2032.

Green healthcare initiatives and rising outpatient procedures present key market opportunities.

Stryker, Cardinal Health, Medline ReNewal, and Innovative Health are key market players.