- Executive Summary

- Global Primary Care POC Diagnostics Market Snapshot 2026 and 2033

- Market Opportunity Assessment, 2026 - 2033, US$ Bn

- Key Market Trends

- Industry Developments and Key Market Events

- Demand Side and Supply Side Analysis

- PMR Analysis and Recommendations

- Market Overview

- Market Scope and Definitions

- Market Dynamics

- Driver

- Restraint

- Opportunities

- Trends

- Macro-Economic Factors

- Global GDP Outlook

- Global Healthcare Expenditure

- Forecast Factors - Relevance and Impact

- COVID-19 Impact Assessment

- Value Added Insights

- Value Chain analysis

- Key Market Players

- Product Adoption Analysis

- Key Promotional Strategies by key players

- PESTLE Analysis

- Porter's Five Forces Analysis

- Regulatory and Technology Landscape

- Global Primary Care POC Diagnostics Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

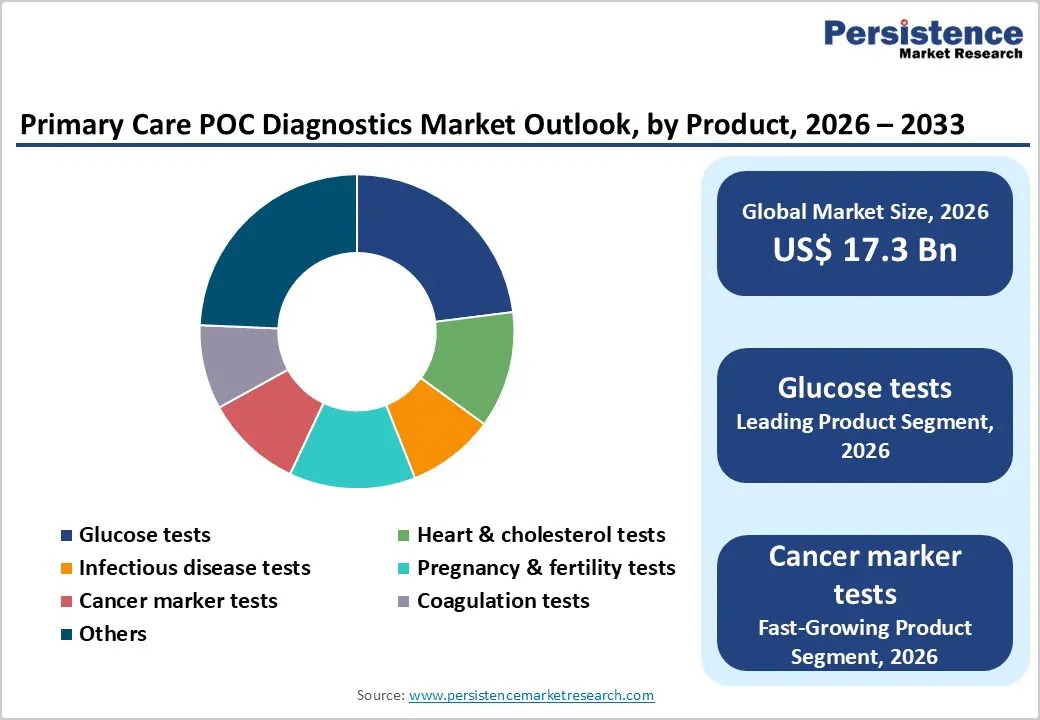

- Global Primary Care POC Diagnostics Market Outlook: Product

- Introduction/Key Findings

- Historical Market Size (US$ Bn) Analysis by Product, 2020-2025

- Current Market Size (US$ Bn) Forecast, by Product, 2026-2033

- Glucose tests

- Heart & cholesterol tests

- Infectious disease tests

- Pregnancy & fertility tests

- Cancer marker tests

- Coagulation tests

- Others

- Market Attractiveness Analysis: Product

- Global Primary Care POC Diagnostics Market Outlook: End User

- Introduction/Key Findings

- Historical Market Size (US$ Bn) Analysis by End User, 2020-2025

- Current Market Size (US$ Bn) Forecast, by End User, 2026-2033

- Hospitals

- Clinics / Diagnostic centers

- Home care

- Pharmacy / Retail clinics

- Research labs

- Market Attractiveness Analysis: End User

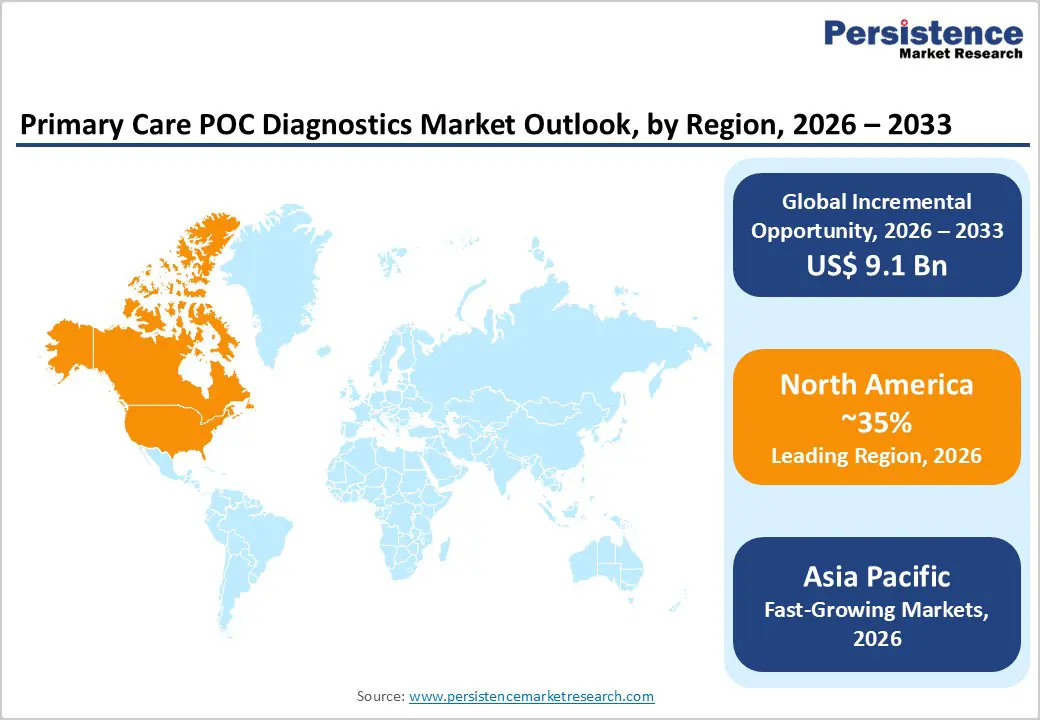

- Global Primary Care POC Diagnostics Market Outlook: Region

- Key Highlights

- Historical Market Size (US$ Bn) Analysis by Region, 2020-2025

- Current Market Size (US$ Bn) Forecast, by Region, 2026-2033

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

- Market Attractiveness Analysis: Region

- North America Primary Care POC Diagnostics Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Pricing Analysis

- North America Market Size (US$ Bn) Forecast, by Country, 2026-2033

- U.S.

- Canada

- North America Market Size (US$ Bn) Forecast, by Product, 2026-2033

- Glucose tests

- Heart & cholesterol tests

- Infectious disease tests

- Pregnancy & fertility tests

- Cancer marker tests

- Coagulation tests

- Others

- North America Market Size (US$ Bn) Forecast, by End User, 2026-2033

- Hospitals

- Clinics / Diagnostic centers

- Home care

- Pharmacy / Retail clinics

- Research labs

- Europe Primary Care POC Diagnostics Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Europe Market Size (US$ Bn) Forecast, by Country, 2026-2033

- Germany

- Italy

- France

- U.K.

- Spain

- Russia

- Rest of Europe

- Europe Market Size (US$ Bn) Forecast, by Product, 2026-2033

- Glucose tests

- Heart & cholesterol tests

- Infectious disease tests

- Pregnancy & fertility tests

- Cancer marker tests

- Coagulation tests

- Others

- Europe Market Size (US$ Bn) Forecast, by End User, 2026-2033

- Hospitals

- Clinics / Diagnostic centers

- Home care

- Pharmacy / Retail clinics

- Research labs

- East Asia Primary Care POC Diagnostics Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- East Asia Market Size (US$ Bn) Forecast, by Country, 2026-2033

- China

- Japan

- South Korea

- East Asia Market Size (US$ Bn) Forecast, by Product, 2026-2033

- Glucose tests

- Heart & cholesterol tests

- Infectious disease tests

- Pregnancy & fertility tests

- Cancer marker tests

- Coagulation tests

- Others

- East Asia Market Size (US$ Bn) Forecast, by End User, 2026-2033

- Hospitals

- Clinics / Diagnostic centers

- Home care

- Pharmacy / Retail clinics

- Research labs

- South Asia & Oceania Primary Care POC Diagnostics Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- South Asia & Oceania Market Size (US$ Bn) Forecast, by Country, 2026-2033

- India

- Southeast Asia

- ANZ

- Rest of SAO

- South Asia & Oceania Market Size (US$ Bn) Forecast, by Product, 2026-2033

- Glucose tests

- Heart & cholesterol tests

- Infectious disease tests

- Pregnancy & fertility tests

- Cancer marker tests

- Coagulation tests

- Others

- South Asia & Oceania Market Size (US$ Bn) Forecast, by End User, 2026-2033

- Hospitals

- Clinics / Diagnostic centers

- Home care

- Pharmacy / Retail clinics

- Research labs

- Latin America Primary Care POC Diagnostics Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Latin America Market Size (US$ Bn) Forecast, by Country, 2026-2033

- Brazil

- Mexico

- Rest of LATAM

- Latin America Market Size (US$ Bn) Forecast, by Product, 2026-2033

- Glucose tests

- Heart & cholesterol tests

- Infectious disease tests

- Pregnancy & fertility tests

- Cancer marker tests

- Coagulation tests

- Others

- Latin America Market Size (US$ Bn) Forecast, by End User, 2026-2033

- Hospitals

- Clinics / Diagnostic centers

- Home care

- Pharmacy / Retail clinics

- Research labs

- Middle East & Africa Primary Care POC Diagnostics Market Outlook: Historical (2020 - 2025) and Forecast (2026 - 2033)

- Key Highlights

- Middle East & Africa Market Size (US$ Bn) Forecast, by Country, 2026-2033

- GCC Countries

- South Africa

- Northern Africa

- Rest of MEA

- Middle East & Africa Market Size (US$ Bn) Forecast, by Product, 2026-2033

- Glucose tests

- Heart & cholesterol tests

- Infectious disease tests

- Pregnancy & fertility tests

- Cancer marker tests

- Coagulation tests

- Others

- Middle East & Africa Market Size (US$ Bn) Forecast, by End User, 2026-2033

- Hospitals

- Clinics / Diagnostic centers

- Home care

- Pharmacy / Retail clinics

- Research labs

- Competition Landscape

- Market Share Analysis, 2025

- Market Structure

- Competition Intensity Mapping

- Competition Dashboard

- Company Profiles

- Roche Diagnostics

- Company Overview

- Product Portfolio/Offerings

- Key Financials

- SWOT Analysis

- Company Strategy and Key Developments

- BD Biosciences

- Danaher Corporation

- Abbott Laboratories

- Instrumentation Laboratory

- bioMerieux

- Siemens Healthcare

- Quidel Corporation

- Roche Diagnostics

- Appendix

- Research Methodology

- Research Assumptions

- Acronyms and Abbreviations

Primary Care POC Diagnostics Market Share and Trends Analysis

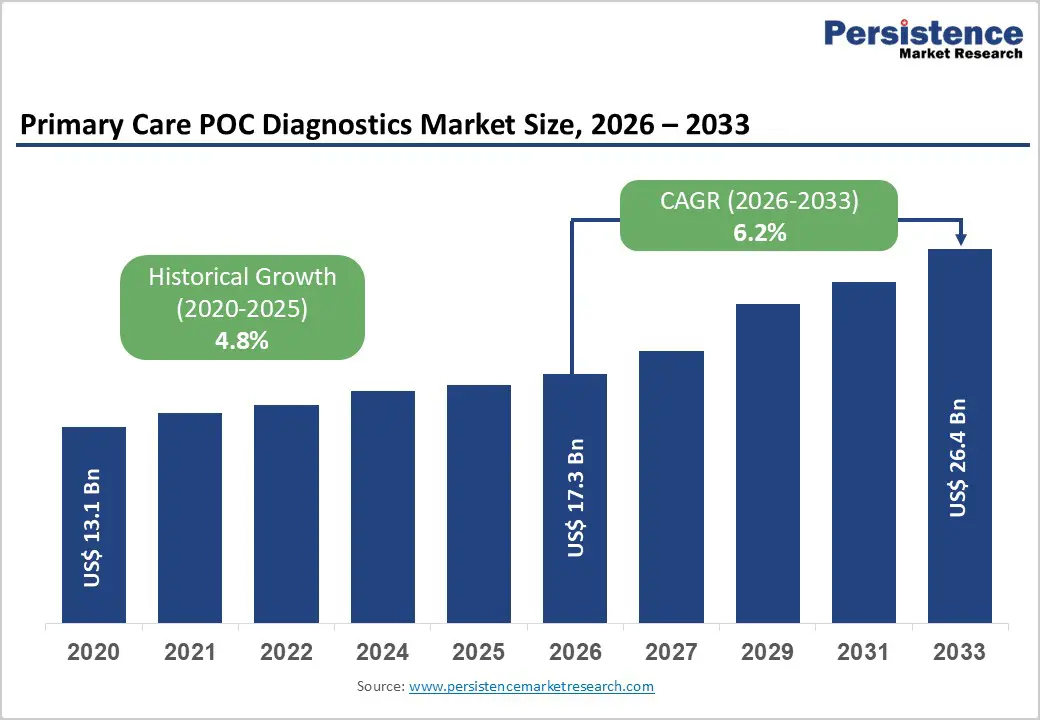

The global primary care POC diagnostics market is expected to be valued at US$ 17.3 billion in 2026 and projected to reach US$ 26.4 billion by 2033, growing at a CAGR of 6.2% between 2026 and 2033.

Market expansion is fundamentally driven by three distinct structural mechanisms rather than incremental demand shifts. First, technological inflection points in high-sensitivity cardiac troponin assays achieving near-perfect correlation with laboratory-based platforms (r = 0.999) enable 1-hour ACS rule-out decision pathways, establishing POC testing as a clinical prerequisite rather than a convenience alternative in emergency medicine. Second, regulatory expansion of CLIA-waived testing, combined with 2025 regulatory updates strengthening Proficiency Testing and personnel qualifications, enables pharmacy and clinic deployment of molecular diagnostics multiplexing (enabling simultaneous influenza/RSV/COVID differentiation and targeted antiviral selection), creating structural demand independent of individual disease prevalence. Third, geographic market asymmetries position Asia Pacific as the fastest-growing region through manufacturing cost convergence, enabling affordable POC deployment across rural primary health centers in China, India, and ASEAN, addressing diagnostic infrastructure gaps affecting over 20 countries facing 20%+ chronic disease premature death risk.