- Specialty & Fine Chemicals

- Polyisobutene Market

Polyisobutene Market Size, Share, and Growth Forecast 2026-2033

Polyisobutene Market by Product Type (C-PIB, HR-PIB), Molecular Weight (Low Molecular Weight, Medium Molecular Weight, High Molecular Weight), Application (Tires, Lube Additives, Fuel Additives, 2-stroke Engines, Industrial Lubes & Others, Adhesives & Sealants), Industry (Transportation, Industrial, Food, Others), and Regional Analysis, 2026–2033

Polyisobutene Market Size and Trend Analysis

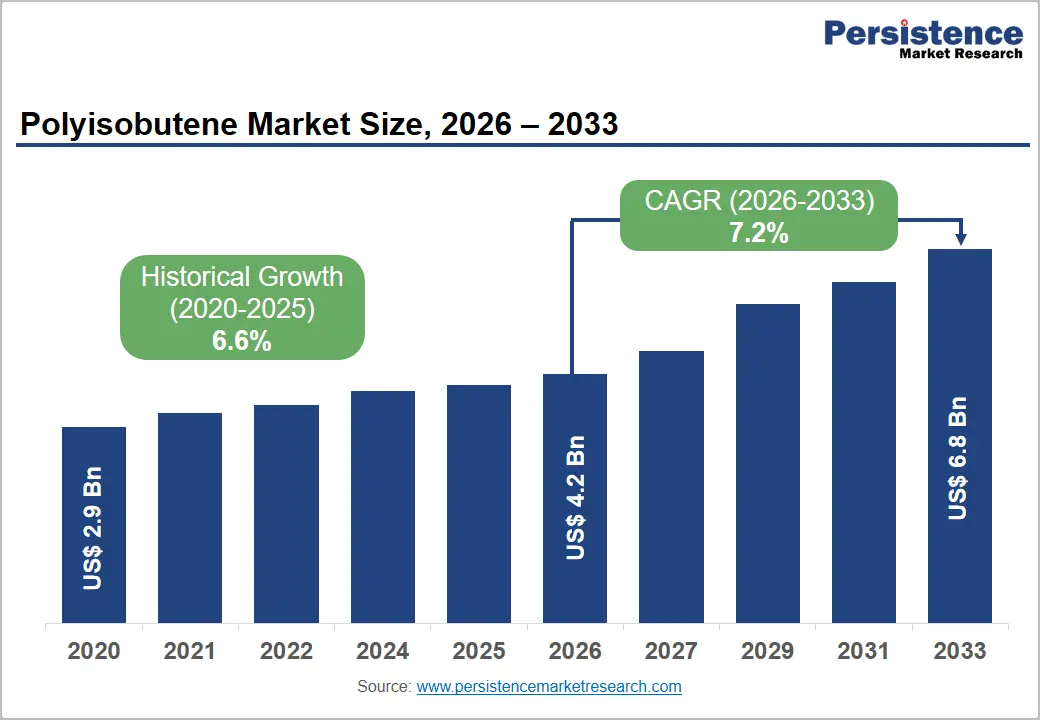

The global polyisobutene market size is expected to be valued at US$ 4.2 billion in 2026 and is projected to reach US$ 6.8 billion by 2033, growing at a CAGR of 7.2% between 2026 and 2033. This robust expansion is driven by rising global demand for high-performance lubricant additives, the accelerating transition toward highly reactive polyisobutene (HR-PIB) in fuel additive applications, and growing adhesive and sealant consumption across construction, automotive, and packaging industries.

The global automotive lubricants market’s ongoing shift toward longer-drain-interval, fuel-economy-enhancing engine oils, requiring PIB-derived dispersant additives, combined with expanding polyisobutylsuccinimide (PIBSI) demand in diesel engine formulations, is creating structural volume and revenue growth for polyisobutene producers through 2033.

Key Industry Highlights:

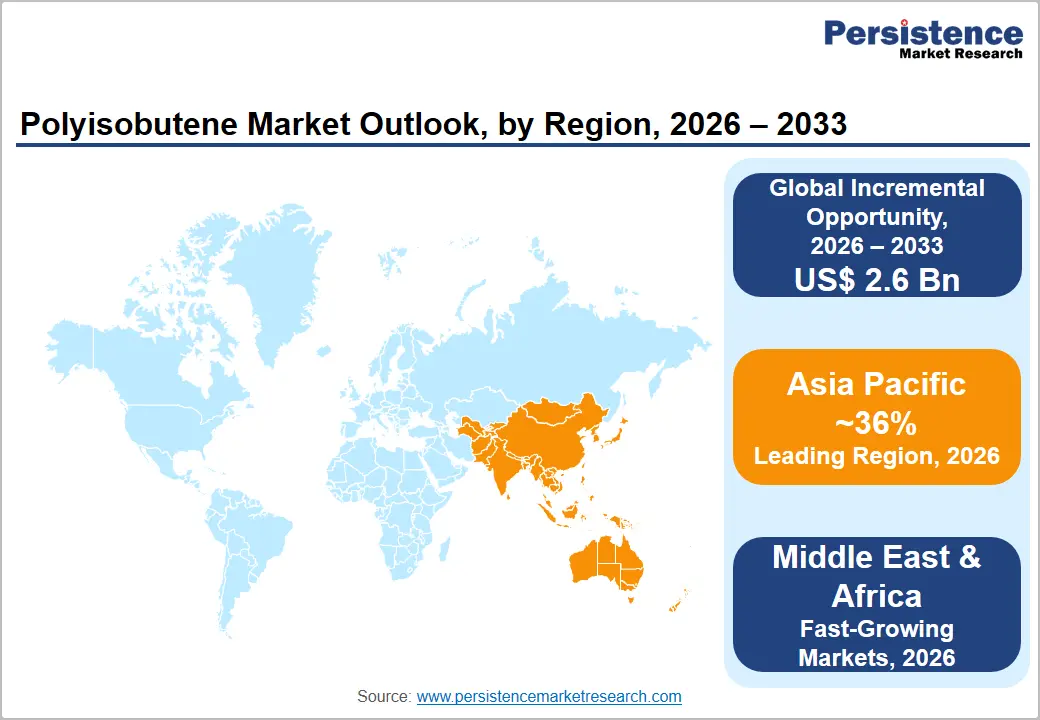

- Leading Region: Asia Pacific dominates the global polyisobutene market with 36% market share in 2026, anchored by China’s massive petrochemical PIB production capacity, rapidly growing automotive fleet lubricant demand, and strong HR-PIB adoption accelerated by China 6b emission standards across fuel and lubricant additive formulations.

- Fastest Growing Region: Middle East & Africa is projected to register the highest CAGR during 2026–2033, driven by Saudi Arabia’s Vision 2030 trillion-dollar infrastructure investment, rapidly expanding transportation fleets, and growing lubricant additive and construction sealant consumption across GCC states, Egypt, and Nigeria.

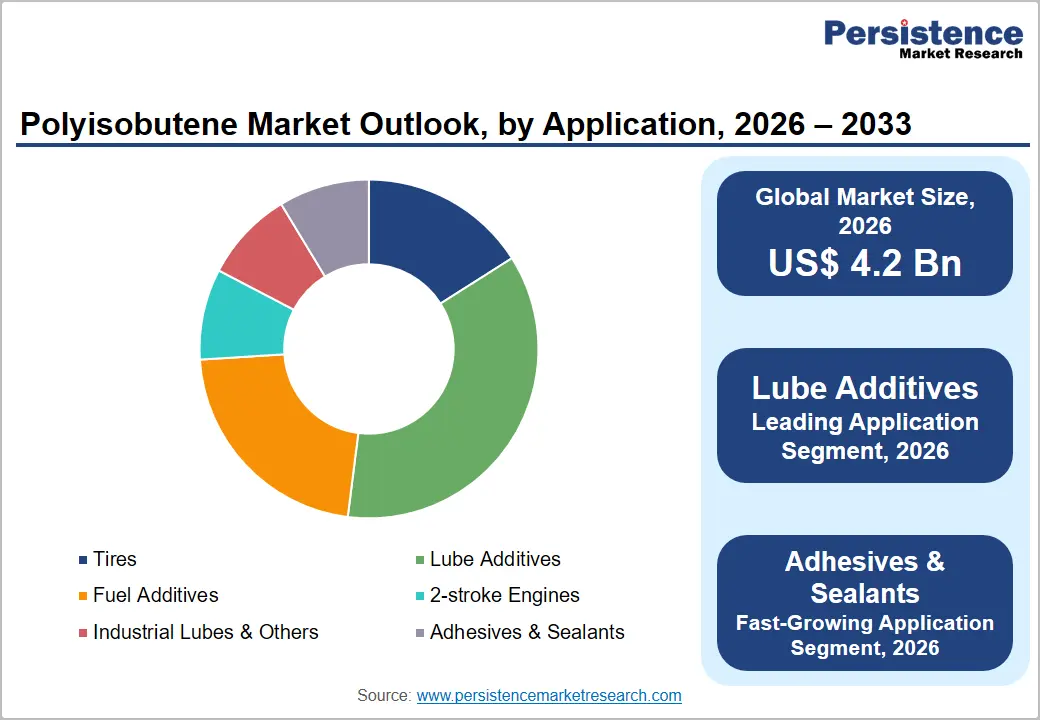

- Dominant Segment: Lube Additives lead the application category with 39% market share in 2026, underpinned by PIB-derived PIBSI ashless dispersants’ non-discretionary role in API SN Plus, ILSAC GF-6, and ACEA-compliant engine oil formulations for a global vehicle fleet of approximately 1.4 billion vehicles.

- Fast-Growing Segment: Adhesives & Sealants represent the fastest growing application at 8% CAGR, driven by construction hot-melt adhesive demand, automotive assembly PSA consumption, and expanding food-contact packaging applications where PIB’s low permeability and chemical inertness deliver unique performance advantages.

- Key Opportunity: HR-PIB’s accelerating adoption in Euro 7 and China 6b-compliant fuel additive formulations, combined with Middle East infrastructure-driven lubricant and sealant demand growth, represents a US$ 2.6 billion incremental dollar opportunity between 2026 and 2033 for PIB producers with established HR-PIB capabilities.

DRO Analysis

Drivers - Strong Demand from Lubricant Additives Sector Driven by Automotive Fleet Growth

Polyisobutene, primarily in medium and high molecular weight forms, is the core feedstock for polyisobutylsuccinimide (PIBSI) and polyisobutylsuccinic anhydride (PIBSA) ashless dispersants, the highest-volume lubricant additive category globally. According to the American Chemistry Council (ACC), lubricant additives represent a multi-billion-dollar global market, with dispersants accounting for the single largest additive volume category.

The International Energy Agency (IEA) projects the global vehicle fleet will grow from approximately 1.4 billion vehicles in 2023 to over 2 billion by 2050, sustaining long-term growth in engine oil consumption. Premium engine oil formulations for GDI (Gasoline Direct Injection) and Euro VI/EPA Tier 4 diesel engines require higher-performance dispersant additive packages, elevating per-liter PIB consumption and supporting above-average revenue growth.

Accelerating Adoption of HR-PIB in Fuel Additives and Ashless Dispersant Applications

Highly Reactive Polyisobutene (HR-PIB), characterized by a high terminal vinylidene content (typically >85%), is experiencing accelerated adoption in fuel additive applications due to its superior reactivity in maleic anhydride functionalization, enabling production of more effective fuel detergent-dispersant additives.

BASF SE and INEOS are among the leading global HR-PIB producers, with established customer relationships with major fuel additive manufacturers, including Afton Chemical, Chevron Oronite, and Infineum. EU Euro 6d and upcoming Euro 7 vehicle emissions regulations mandate superior fuel injection cleanliness, amplifying demand for PIB-based fuel detergent additives. This regulatory tailwind is expected to sustain above-average HR-PIB demand growth through 2033.

Restraints - Feedstock Price Volatility Linked to Isobutylene and Refinery Output Fluctuations

Polyisobutene is produced from isobutylene, a C4 refinery byproduct whose availability and price are directly tied to crude oil refining activity, steam cracker operations, and petrochemical complex utilization rates. The American Chemistry Council (ACC) has documented multiple cycles of significant C4 feedstock price volatility between 2020 and 2023, impacting PIB producer operating margins and requiring frequent product price adjustments that destabilize downstream formulator procurement planning. Energy transition trends reducing long-term refinery throughput also pose structural feedstock supply risks for conventional PIB producers.

Competition from Synthetic Alternatives in High-Performance Lubricant Applications

In premium synthetic lubricant applications, polyisobutene faces increasing competition from poly-alpha-olefins (PAO), polyalkylene glycols (PAG), and ester-based synthetic base fluids that offer superior viscosity index, oxidation resistance, and low-temperature performance.

API Group IV and V synthetic base oils are gaining share in automotive and industrial lubricant formulations requiring extended drain intervals and energy efficiency certifications, potentially limiting PIB’s share of the highest-value lubricant additive sub-segments over the medium term.

Opportunities - Rapid Growth of Adhesives & Sealants Applications Driven by Construction and Packaging Sectors

The adhesives and sealants application represents the fast-growing segment for polyisobutene at 8% CAGR, driven by rising demand in hot-melt adhesives, pressure-sensitive adhesives (PSA), and sealant formulations for construction, automotive assembly, and flexible packaging. High molecular weight polyisobutene delivers exceptional tackiness, water vapor barrier performance, and chemical inertness required in food-contact and medical device packaging applications.

According to the Adhesive and Sealant Council (ASC), global adhesive and sealant consumption has expanded consistently above 4% annually over the past decade, driven by construction activity in Asia Pacific and e-commerce packaging growth globally. PIB’s unique combination of low permeability, tackiness, and compatibility with polyolefin systems positions it as a preferred base polymer in this high-growth application segment.

Middle East & Africa Infrastructure Boom Generating Growing Lubricant and Sealant Demand

The Middle East & Africa (MEA) region is emerging as the fastest growing polyisobutene market, driven by massive infrastructure investment, expanding petrochemical and industrial capacity, and rapidly growing automotive fleet size. Saudi Arabia’s Vision 2030 program has allocated over US$ 1 trillion in infrastructure, giga-project, and industrial development, generating large-scale demand for PIB-based sealants in construction applications and lubricant additives for industrial machinery and transport fleets.

The UAE, Egypt, and Nigeria are simultaneously expanding transportation and industrial infrastructure, amplifying lubricant consumption. Companies capable of establishing regional distribution partnerships and technical service networks aligned with local formulator requirements in MEA will be positioned to capture this fastest-growing demand base through 2033.

Category-wise Analysis

Product Type Insights

HR-PIB (Highly Reactive Polyisobutene) is the fastest growing product type and an increasingly significant revenue contributor, while C-PIB (Conventional PIB) retains the dominant share of total market volume in 2026. C-PIB’s volume leadership reflects its entrenched use across the established lube additive, fuel additive, and adhesive sectors, where long-qualified supply chains and mature formulation databases support continued procurement.

HR-PIB’s superior reactivity, driven by >85% terminal vinylidene content, enables more efficient and cleaner functionalization chemistry for next-generation fuel and lubricant additive synthesis, and its adoption is being accelerated by evolving emissions regulations across Europe (Euro 7), the U.S. (EPA Tier 4), and China (China 6b) standards. Leading producers, including BASF SE, INEOS, and Daelim Co., Ltd, invest heavily in HR-PIB production capacity expansion.

Application Insights

Lube Additives dominate the polyisobutene market by application, accounting for approximately 39% of market share in 2026. This dominance is attributable to the fundamental role of PIB-derived PIBSI/PIBSA ashless dispersants as the highest-volume additive category in engine oil formulations globally. Modern passenger car motor oils (PCMO) and heavy-duty diesel engine oils (HDEO) require dispersant additive packages that prevent sludge formation, deposit buildup, and viscosity degradation, functions exclusively delivered by PIB-derived chemistry at commercial scale.

API SN Plus, ILSAC GF-6, and ACEA A3/B4 engine oil performance specifications mandate dispersant additive use, creating non-discretionary volume demand. The world’s approximately 1.4 billion motor vehicles all require periodic oil changes, generating massive, recurring PIB-derivative lubricant additive consumption globally.

Molecular Weight Insights

Medium Molecular Weight polyisobutene represents the leading molecular weight segment in 2026, reflecting its optimal performance balance across the broadest range of applications, including lube additives, fuel additives, and adhesives, that collectively account for the majority of global PIB consumption.

Medium MW PIB (typically 1,000–2,300 Mn) offers the ideal viscosity and reactivity profile for PIBSA/PIBSI dispersant synthesis while maintaining adequate processability in adhesive and sealant formulations. BASF SE’s Glissopal® and TPC Group’s Indopol® product lines include a wide range of medium MW PIB grades serving diverse end-user industries. The segment’s broad applicability across multiple end-use markets sustains its leading position despite growing adoption of low MW HR-PIB in fuel additive applications.

Industry Insights

Transportation represents the leading Industry for polyisobutene in 2026, driven by the sector’s massive consumption of PIB-derived lube additives (engine oil dispersants), fuel additives (injector cleanliness detergents), and tire sealant compounds. The IEA projects global vehicle fleet growth from 1.4 billion in 2023 to over 2 billion by 2050, ensuring structural long-term PIB demand growth from the transportation sector.

PIB-based inner liner compounds in tires, providing low air permeability in tubeless tire designs, are used in virtually every passenger car tire manufactured globally, with Michelin, Bridgestone, and Continental as major downstream consumers. This combination of lubricant additive, fuel additive, and tire compound applications makes transportation the anchor demand sector for PIB consumption.

Regional Analysis

North America Polyisobutene Market Trends and Insights

North America is a mature, innovation-driven polyisobutene market, characterized by strong demand from the lubricant additives sector, active HR-PIB adoption for clean fuel additive formulations, and a large installed base of PIB-consuming industries. The U.S. is home to major PIB producers including TPC Group, ExxonMobil Chemical, and INEOS, sustaining domestic supply chain depth for lube and fuel additive formulators.

U.S. Polyisobutene Market Size

The United States accounts for approximately 80–83% of North American PIB revenues, driven by the world’s largest lubricant additives industry and a large vehicle fleet of approximately 290 million registered vehicles per FHWA data, requiring regular oil change PIB-derivative dispersant consumption. TPC Group and ExxonMobil Chemical maintain major PIB production facilities in Texas.

Europe Polyisobutene Market Trends and Insights

Europe is the second-largest PIB market, driven by its position as the global originator of HR-PIB technology and strong demand from premium automotive lubricant and fuel additive industries. EU Euro 7 emissions regulations are compelling fuel and lubricant additive formulators to upgrade performance levels, creating structural HR-PIB demand growth. BASF SE and INEOS dominate European PIB production with integrated supply chain advantages.

Germany Polyisobutene Market Size

Germany accounts for approximately 28% of European market revenues, anchored by BASF SE’s Ludwigshafen operations producing the globally recognized Glissopal® HR-PIB product line. Germany’s large automotive and chemical industries create deep local demand, and BASF’s integrated value chain from PIB to PIBSA additives positions it uniquely in the European market.

U.K. Polyisobutene Market Size

The U.K. contributes approximately 14% of revenue share, driven by INEOS’s Grangemouth PIB production facility, one of Europe’s largest, and strong lubricant additive formulation industry presence through companies including Infineum (a joint venture of ExxonMobil and Shell). The U.K.’s additive chemistry expertise sustains premium HR-PIB consumption.

France Polyisobutene Market Size

France contributes approximately 12% of Europe's polyisobutene market revenues, driven by the automotive lubricant industry, TotalEnergies’ lubricant additive formulation operations, and demand from the food-grade PIB segment used in food contact adhesives and sealants certified under EU Regulation (EC) No 1935/2004 for food contact materials.

Asia Pacific Polyisobutene Market Trends and Insights

Asia Pacific dominates the global polyisobutene market with 36% market share in 2026, anchored by China’s massive petrochemical complex producing both C-PIB and increasing volumes of HR-PIB, and strong demand from Asia’s rapidly growing automotive fleet, lubricant additive industry, and construction adhesive and sealant markets. China’s China 6b emission standards are accelerating HR-PIB adoption in fuel and lubricant additive applications.

India Polyisobutene Market Size

India accounts for approximately 12% of the Asia Pacific revenue share, with demand driven by a rapidly expanding vehicle fleet now exceeding 330 million registered vehicles per MoRTH data, growing lubricant additive consumption, and Reliance Industries Ltd. and Kothari Petrochemicals serving as domestic PIB producers supplying the Indian lube and fuel additive market.

Japan Polyisobutene Market Size

Japan contributes approximately 16% of Asia Pacific revenues, driven by a mature automotive lubricant market with high premium synthetic oil penetration and strong PIB-based hot-melt adhesive and PSA consumption from the electronics and automotive manufacturing sectors. ENEOS Corporation, Idemitsu Kosan, and INEOS supply the Japanese market through domestic production and imports.

Southeast Asia Polyisobutene Market Size

Southeast Asia accounts for approximately 12% share in Asia Pacific, with Indonesia, Thailand, and Vietnam driving growth through expanding automotive manufacturing, two-stroke engine lubricant demand, and construction adhesive consumption. The region’s growing petrochemical infrastructure is gradually reducing import dependency for polyisobutene and lube additive intermediates.

Competitive Landscape

The global polyisobutene market is moderately consolidated at the top tier, with BASF SE, INEOS, TPC Group, ExxonMobil Chemical, and Daelim Co., Ltd. collectively commanding significant global production capacity and revenue share. Key competitive differentiators include HR-PIB technological capability, molecular weight range breadth, application technical service depth, and geographic production footprint.

Chinese producers including Zhejiang Shunda and Shandong Hongrui are expanding HR-PIB capacity to serve domestic demand. Strategic trends include capacity expansions targeting HR-PIB production growth, co-development programs with lube and fuel additive formulators, and food-grade PIB certification programs targeting the adhesive and sealant segment.

Key Developments

- In April 2025, BASF SE announced expansion of its Glissopal® HR-PIB production capacity at its Ludwigshafen complex, targeting growing European and export demand for HR-PIB driven by Euro 7 fuel additive formulation requirements.

- In November 2024, INEOS completed a capacity optimization project at its Grangemouth PIB facility in Scotland, increasing high-MW PIB output for adhesive and sealant applications and strengthening supply reliability for European customers.

- In February 2024, Reliance Industries Ltd. commissioned an expanded HR-PIB production unit at its Jamnagar complex in India, targeting domestic lube additive manufacturers and enabling HR-PIB export to Southeast Asian markets under India’s Make in India chemical manufacturing initiative.

Global Polyisobutene Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 2.9 Billion |

|

Current Market Value (2026) |

US$ 4.2 Billion |

|

Projected Market Value (2033) |

US$ 6.8 Billion |

|

CAGR (2026–2033) |

7.2% |

|

Leading Region |

Asia Pacific, 36% market share (2026) |

|

Dominant Application (Category-3) |

Lube Additives, 39% market share (2026) |

|

Top-ranking Product Type (Category-1) |

C-PIB, leading volume share (2026) |

|

Incremental Opportunity |

US$ 2.6 Billion (2026–2033) |

Companies Covered in Polyisobutene Market

- BASF SE

- Daelim Co., Ltd.

- TPC Group

- INEOS

- Kothari Petrochemicals

- Braskem

- ENEOS Corporation

- Zhejiang Shunda New Material Co., Ltd.

- Shandong Hongrui New Material Technology Co., Ltd.

- Reliance Industries Ltd.

- Jilin Petrochemical

- SIBUR

- ExxonMobil Chemical

- Lanxess

- Idemitsu Kosan

Frequently Asked Questions

The global polyisobutene market is projected to be valued at US$ 4.2 billion in 2026, driven by robust demand from lube additives, where PIB-derived PIBSI dispersants are non-discretionary components in API SN Plus and ACEA-compliant engine oil formulations, combined with accelerating HR-PIB adoption in fuel additive applications driven by Euro 7 and China 6b emission standard compliance requirements.

Primary drivers include growth of lubricant additive demand linked to IEA-projected vehicle fleet expansion from 1.4 billion vehicles in 2023 to over 2 billion by 2050, and the accelerating regulatory push for high-performance fuel and lube additive formulations.

Asia Pacific leads with approximately 36% share in 2026, driven by China’s position as the world’s largest PIB producer and consumer, supported by the region’s rapidly expanding automotive fleet requiring lubricant additive consumption, and growing adhesive and sealant demand from construction and electronics manufacturing across Japan, South Korea, and India.

The most significant opportunities are the adhesives & sealants application segment growing at 8% CAGR, driven by hot-melt adhesive demand in construction and food-contact packaging, and Middle East & Africa’s infrastructure boom under Saudi Vision 2030 generating large-scale lubricant additive and construction sealant demand.

Key players include BASF SE (Glissopal®), INEOS, TPC Group (Indopol®), ExxonMobil Chemical, Daelim Co. Ltd., Lanxess, Kothari Petrochemicals, Reliance Industries Ltd., Braskem, ENEOS Corporation, Idemitsu Kosan, SIBUR, Jilin Petrochemical, Zhejiang Shunda New Material Co. Ltd., Shandong Hongrui New Material Technology Co. Ltd., and Infineum International Ltd., among others.