- Healthcare Services

- Pelvic Organ Prolapse Repair Market

Pelvic Organ Prolapse Repair Market Size, Share, and Growth Forecast, 2026 - 2033

Pelvic Organ Prolapse Repair Market by Product Type (Vaginal Pessary, Vaginal Mesh, Synthetic Mesh Implants, Others), Treatment Type (Surgical, Non-surgical), Application (Cystocele, Rectocele, Enterocele, Uterine Prolapse, Vaginal Vault Prolapse, Others), and Regional Analysis for 2026 - 2033

Pelvic Organ Prolapse Repair Market Share and Trends Analysis

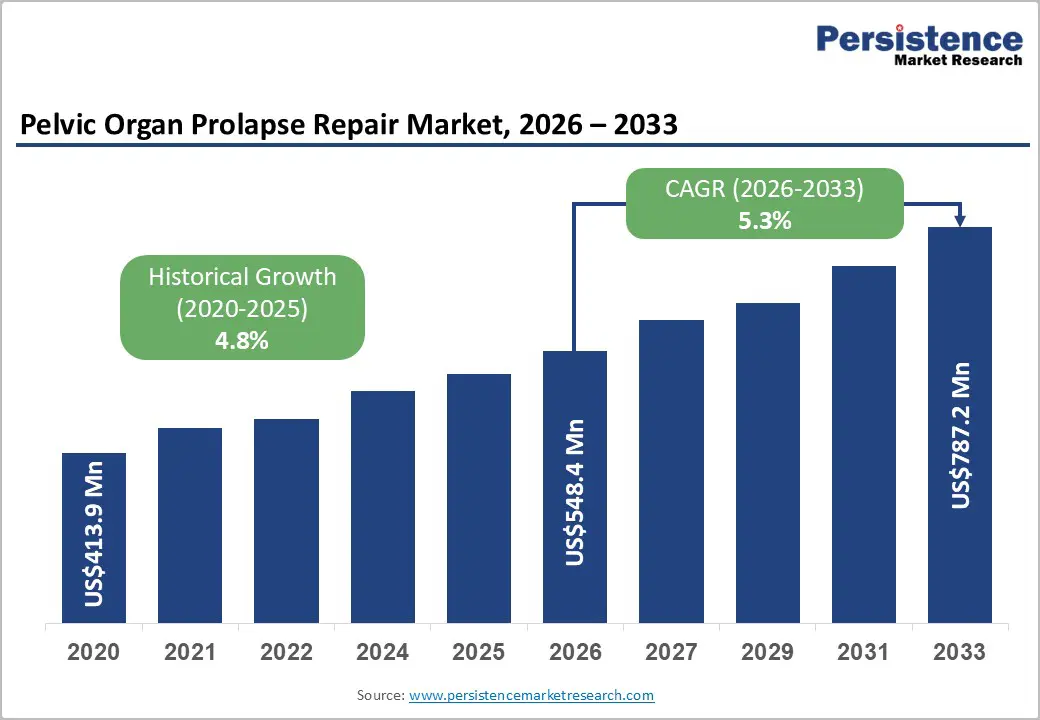

The global pelvic organ prolapse repair market size is likely to be valued at US$548.4 million in 2026 and is estimated to reach US$787.2 million by 2033, growing at a CAGR of 5.3% during the forecast period from 2026 to 2033, driven by changing population dynamics and enhanced clinical strategies.

The expanding geriatric female demographic creates a structural shift in clinical volume, as structural weakness in pelvic architecture correlates directly with advanced age. Strict regulatory assessment pathways established by international governance entities alter product deployment frameworks, shifting preference toward biological materials and specialized fixation instrumentation.

Key Industry Highlights:

- Leading Product Type: Vaginal pessary is set to hold around 31% revenue share in 2026, driven by large-scale adoption as a first-line conservative management tool across outpatient settings.

- Fastest-growing Product Type: Biological grafts are projected as the fastest-growing segment, supported by growing surgeon preference for biocompatible implants following regulatory reduction in synthetic mesh use.

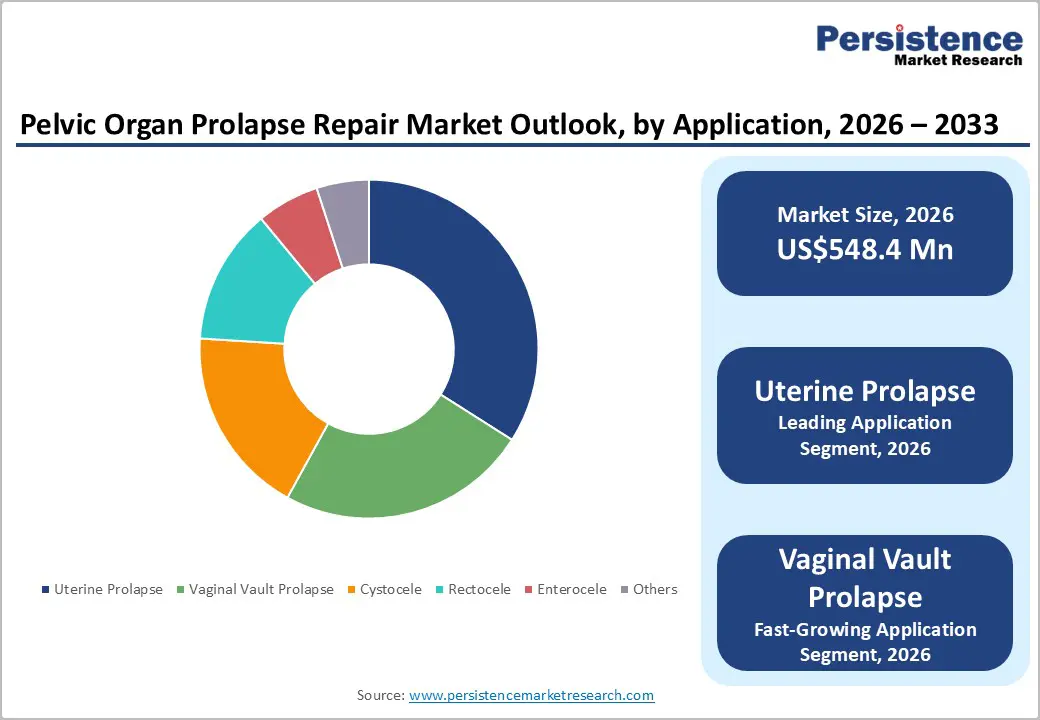

- Leading Application: Uterine prolapse is estimated to hold roughly 34% revenue share in 2026, driven by high clinical prevalence among parous women and availability of multiple validated surgical treatment options.

- Fastest-growing Application: Vaginal vault prolapse is forecast to record the fastest growth, driven by rising post-hysterectomy patient volumes and expanding robotic sacrocolpopexy adoption.

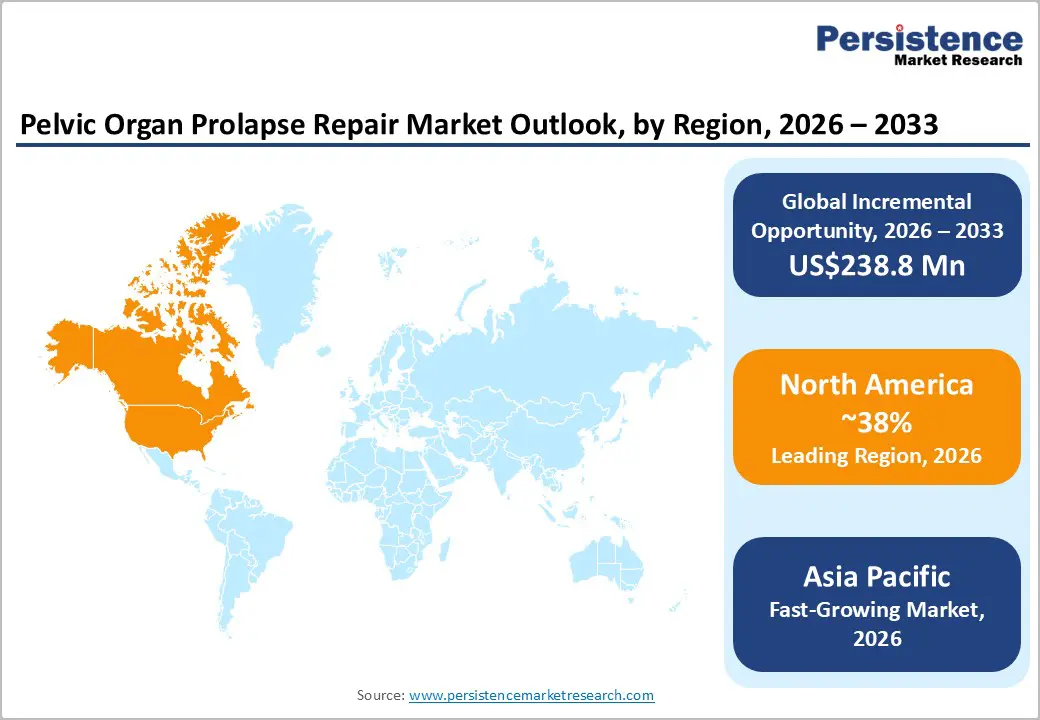

- Regional Leadership: North America is projected to capture roughly 38% of market share in 2026, driven by high procedural volumes and well-established reimbursement infrastructure under CMS and commercial insurance plans.

- Competitive Environment: The market is moderately consolidated, with Boston Scientific, Medtronic, Johnson and Johnson MedTech, Coloplast, and CooperSurgical holding leading positions through diversified portfolios and direct sales infrastructure.

- Key Opportunity: Asia Pacific is forecast to record the fastest regional growth, driven by expanding gynecological surgical infrastructure investment across China and India under government healthcare development programs.

DRO Analysis

Driver - Demographic Shifts and Accelerating Prevalence Rates among Geriatric Populations

The expanding global pool of elderly female patients acts as a primary catalyst for clinical intervention volume. Pathological deterioration of pelvic floor structural integrity demonstrates a direct correlation with biological aging and parity status. Statistical tracking by the United States National Institutes of Health in 2025 indicated that approximately 20% of women undergo surgical intervention for pelvic floor disorders during a normal lifespan. This substantial clinical prevalence generates consistent institutional utilization of supportive fixation matrices, specialized surgical kits, and non-invasive containment apparatuses across international healthcare infrastructure networks.

The resulting demand pressure shifts procurement prioritization toward durable, biocompatible therapeutic options within hospital purchase order frameworks. Institutional purchasing entities experience direct volume increases for reconstructive devices, balancing long-term healthcare expenditure via permanent structural stabilization. The elimination of repetitive outpatient symptomatic therapeutic interventions provides long-term financial justification for immediate device utilization. Surgical centers allocate substantial baseline capital to ensure continuous availability of diverse sizing configurations, driving sustained procurement volume through established manufacturing supply lines.

Restraint - Limited Specialist Availability and Procedure Cost Burden

Pelvic reconstructive procedures require highly trained urogynecologists and minimally invasive surgical expertise, creating workforce limitations across healthcare systems. Insufficient specialist availability restricts treatment accessibility, particularly in secondary care facilities. High capital investment requirements for robotic surgical systems and advanced imaging platforms increase financial pressure on hospitals operating under constrained reimbursement environments.

Long procedural training cycles and certification requirements slow workforce expansion within pelvic floor reconstruction services. Patients in lower-income healthcare systems often delay surgical treatment due to out-of-pocket expenditure concerns. Reduced affordability impacts procedural adoption rates, limiting revenue scalability for premium surgical technologies and biologic implant manufacturers operating within cost-sensitive healthcare environments.

Opportunity - Targeted Penetration of Decentralized Ambulatory Surgical Centers via Specialized Kit Optimization

The systematic migration of elective reconstructive interventions from centralized tertiary hospitals to decentralized ambulatory surgical centers offers a structural expansion opportunity. Single-use, complete procedural instrumentation configurations eliminate the necessity for extensive institutional sterilization infrastructure within smaller clinical footprints. Streamlined kit architecture reduces operational preparation time, maximizing daily case throughput for specialized outpatient surgical teams. This logistical efficiency matches the financial goals of ambulatory networks, facilitating rapid clinical integration outside traditional hospital systems.

Developing targeted commercial agreements with corporate ambulatory network operators facilitates rapid, multi-site product adoption. Designing specialized packaging configurations reduces physical inventory footprint requirements, directly lowering overhead expenses for compact outpatient clinics. Lowering the overall cost per procedure while maintaining optimal clinical outcomes unlocks a large, underserved market vertical. This operational model ensures consistent, high-volume reorders, driving predictable revenue expansion across commercial supply networks.

Category-wise Analysis

Product Type Insights

Vaginal pessary is expected to lead the pelvic organ prolapse repair market, accounting for approximately 31% of revenue in 2026. Pessaries serve as a first-line conservative tool across primary care and outpatient settings. CooperSurgical markets a broad portfolio covering varying prolapse severity grades. Low procedural risk and suitability for surgical-ineligible patients sustain consistent demand across a broad demographic.

Biological grafts are likely to represent the fastest-growing segment, propelled by rising surgeon preference for biocompatible materials following reduced synthetic mesh use. Integra LifeSciences' collagen matrix products exemplify this shift. Clinical evidence supporting long-term tissue integration is reinforcing adoption. This segment benefits directly from the regulatory-driven contraction of synthetic mesh commercial activity.

Treatment Type Insights

Surgical treatment is projected to lead the market, capturing around 68% of the revenue share in 2026. American College of Obstetricians and Gynecologists (ACOG) clinical guidelines recommend that surgical intervention for symptomatic prolapse significantly impairs quality of life. Growing ambulatory surgical center capacity is reducing procedural costs and wait times. This supports continued growth in surgical procedure volumes across both hospital and outpatient settings.

Non-surgical treatment is likely to be the fastest-growing segment, fueled by expanding patient preference for conservative management and increasing telehealth-enabled physiotherapy delivery. Centers for Medicare & Medicaid Services (CMS) reimbursement expansion for pelvic floor physical therapy is reducing access barriers. Demand from older patients with surgical contraindications and younger patients seeking fertility-preserving options is sustaining volume growth in this segment.

Application Insights

Uterine prolapse is likely to be the leading segment with a projected 34% of the pelvic organ prolapse repair market share in 2026 due to its high prevalence among parous women and the availability of multiple validated treatment pathways. National Institutes of Health (NIH) Women's Health Initiative epidemiological data identifies it as the most commonly diagnosed prolapse form.

Vaginal vault prolapse is anticipated to be the fastest-growing segment, fueled by increasing post-hysterectomy incidence and expanding robotic sacrocolpopexy adoption as the preferred surgical correction. Post-hysterectomy vault prolapse creates a structurally growing patient cohort over time. FDA-cleared robotic platforms enabling precise apical support repair are shifting procedural preference toward sacrocolpopexy. This drives sustained demand for sacrocolpopexy kit components and advanced energy devices.

Regional Insights

North America Pelvic Organ Prolapse Repair Market Trends

North America is anticipated to be the leading region, accounting for a market share of 38% in 2026, driven by high procedural volumes, well-established CMS and commercial insurance reimbursement, and the presence of major device manufacturers. ACOG and American Urogynecologic Society guideline dissemination standardizes diagnosis and referral pathways. This creates predictable surgical volume growth across hospital and ambulatory surgical center settings.

U.S. Pelvic Organ Prolapse Repair Market Insights

The U.S. market is projected to expand due to intense capital investment in ambulatory surgical infrastructure and advanced clinical training programs. Major corporate healthcare operators prioritize single-use procedural kits to maximize operating room utilization and compress patient discharge cycles.

Canada Pelvic Organ Prolapse Repair Market Insights

Canada is likely to demonstrate steady growth, supported by provincial healthcare investments in women's health and expanding surgical capacity at academic centers, including Toronto General Hospital. The Canadian Continence Foundation's awareness initiatives are expected to reduce diagnostic delays and expand procedural referral pipelines.

Europe Pelvic Organ Prolapse Repair Market Trends

The Europe market is likely to be influenced by the comprehensive enforcement of the Medical Device Regulation framework, which alters product validation structures. Manufacturing entities allocate significant capital to secure conformity assessments, prioritizing high-margin reconstructive portfolios across major Western European healthcare networks.

Germany Pelvic Organ Prolapse Repair Market Insights

Germany is expected to dominate the continental revenue share due to the presence of extensive hospital networks and well-funded social health insurance structures. High-volume urogynecological specialization centers drive rapid adoption of advanced apical suspension kits, integrating novel materials into standardized clinical pathways.

U.K. Pelvic Organ Prolapse Repair Market Insights

The U.K. market is likely to grow through targeted National Health Service initiatives designed to reduce elective surgical backlogs in women's health departments. Procurement guidelines favor cost-effective conservative management tools, driving high-volume distribution of premium non-surgical containment systems across primary care networks.

Asia Pacific Pelvic Organ Prolapse Repair Market Trends

Asia Pacific is forecast to be the fastest-growing market for pelvic organ prolapse repair, stimulated by rapid healthcare infrastructure modernization and expanding middle-class disposable income levels. Governments across developing economies implement broad medical insurance expansion programs, significantly lowering out-of-pocket expenditure thresholds for complex reconstructive interventions.

Japan Pelvic Organ Prolapse Repair Market Insights

Japan is expected to exhibit advanced market dynamics driven by one of the highest geriatric demographic ratios globally. Institutional focus on long-term geriatric quality of life parameters supports high utilization rates of non-invasive containment systems and low-risk surgical interventions.

China Pelvic Organ Prolapse Repair Market Insights

China is projected to contribute massive volume growth due to sweeping healthcare reform initiatives and localized manufacturing expansion. Government procurement strategies emphasize domestic production capabilities, prompting international medical technology firms to establish localized assembly facilities or form joint ventures with regional entities.

Competitive Landscape

The global pelvic organ prolapse repair market is moderately consolidated. A small number of multinational companies hold disproportionate revenue shares through diversified product portfolios spanning surgical mesh, biological grafts, pessaries, and energy-based instruments. Boston Scientific, Medtronic, Johnson and Johnson MedTech, Coloplast, and CooperSurgical represent the leading commercial participants. Their positions reflect capital-intensive compliance infrastructure and direct surgical sales force advantages.

Mid-tier manufacturers remain active in pessary and suturing kit segments, where regulatory barriers are lower. Merger and acquisition activity serves as the primary mechanism for portfolio expansion. Larger players absorb innovative smaller companies with differentiated graft or digital health technologies, reinforcing portfolio depth and competitive separation from smaller regional participants.

Key Industry Development

- In December 2024, ConTIPI Medical and EVERSANA advanced the commercial launch of the ProVate device for pelvic organ prolapse management, reinforcing the expansion of non-surgical treatment accessibility across women's healthcare settings.

Companies Covered in Pelvic Organ Prolapse Repair Market

- Boston Scientific Corporation

- Medtronic plc

- Johnson and Johnson MedTech (Ethicon)

- Coloplast A/S

- CooperSurgical Inc.

- C.R. Bard (Becton, Dickinson and Company)

- Karl Storz SE and Co. KG

- Olympus Corporation

- Neomedic International

- American Medical Systems (Endo International)

- Caldera Medical Inc.

- Pelvalon Inc.

- Terumo Corporation

- Integra LifeSciences Corporation

- Cousin Biotech

Frequently Asked Questions

The global pelvic organ prolapse repair market is projected to reach US$548.4 million in 2026.

Rising aging female populations, increasing pelvic floor disorder prevalence, and expanding adoption of minimally invasive gynecological procedures are driving the pelvic organ prolapse repair market.

The pelvic organ prolapse repair market is poised to witness a CAGR of 5.3% from 2026 to 2033.

Expanding adoption of biologic graft technologies and growing outpatient pelvic reconstruction infrastructure are creating key opportunities in the pelvic organ prolapse repair market.

Some of the key market players include Boston Scientific, Medtronic, Johnson and Johnson MedTech, Coloplast, and CooperSurgical.