- Medical Devices

- Female Pelvic Implants Market

Female Pelvic Implants Market Size, Share, and Growth Forecast, 2026 - 2033

Female Pelvic Implants Market by Product Type (Vaginal Mesh Implants, Vaginal Sling Implants, Vaginal Graft Implants), Indication (Pelvic Organ Prolapse (POP), Stress Urinary Incontinence (SUI)), End-User (Hospitals, Ambulatory Surgical Centers (ASCs), Specialty Clinics), and Regional Analysis for 2026 - 2033

Female Pelvic Implants Market Share and Trends Analysis

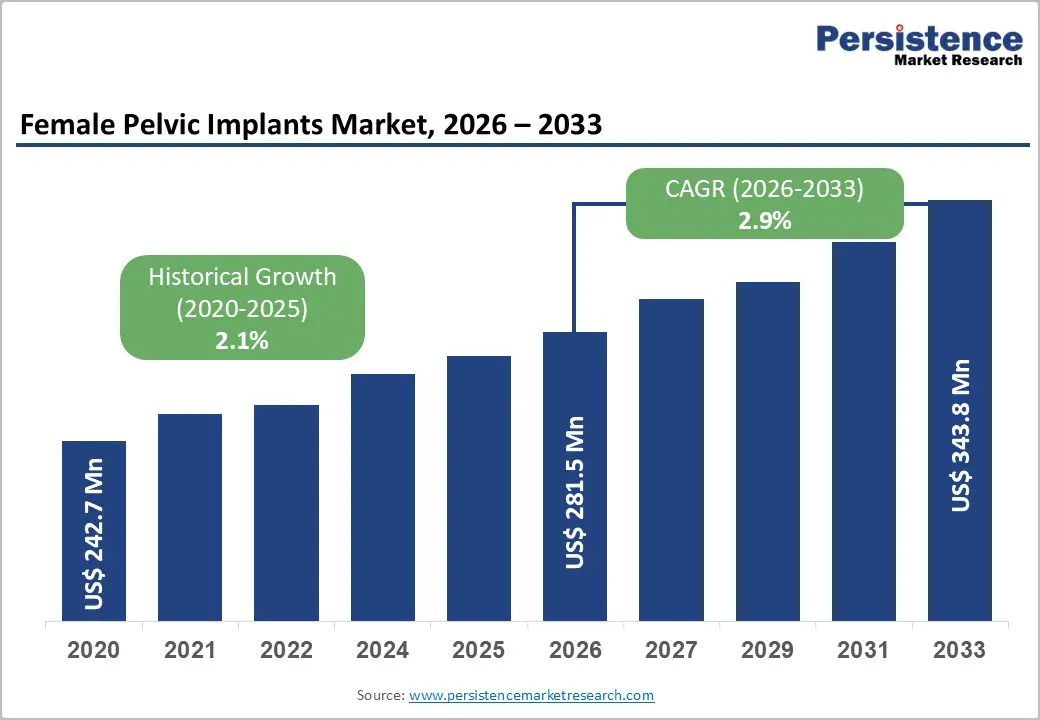

The global female pelvic implants market size is likely to be valued at US$ 281.5 million in 2026, and is projected to reach US$ 343.8 million by 2033, growing at a CAGR of 2.9% during the forecast period 2026−2033. Sustained procedural demand, expanding cohorts of aging females, and structured clinical pathway integration collectively underpin stable, long-term expansion. Rising life expectancy reported by the World Health Organization increases the prevalence pool for pelvic floor disorders, particularly pelvic organ prolapse and stress urinary incontinence. Clinical guidelines issued by bodies such as the American College of Obstetricians and Gynecologists (ACOG) reinforce surgical intervention in moderate to severe cases where conservative therapy fails, driving procedural conversion.

Growing awareness of pelvic health through public health initiatives improves diagnosis rates and referral flows. Integration of minimally invasive surgical techniques reduces hospital stay duration and improves patient-reported outcomes, supporting physician confidence and institutional adoption. Healthcare infrastructure investments across advanced and emerging economies enhance access to urogynecology specialists and operating facilities, translating demographic need into commercial demand.

Key Industry Highlights

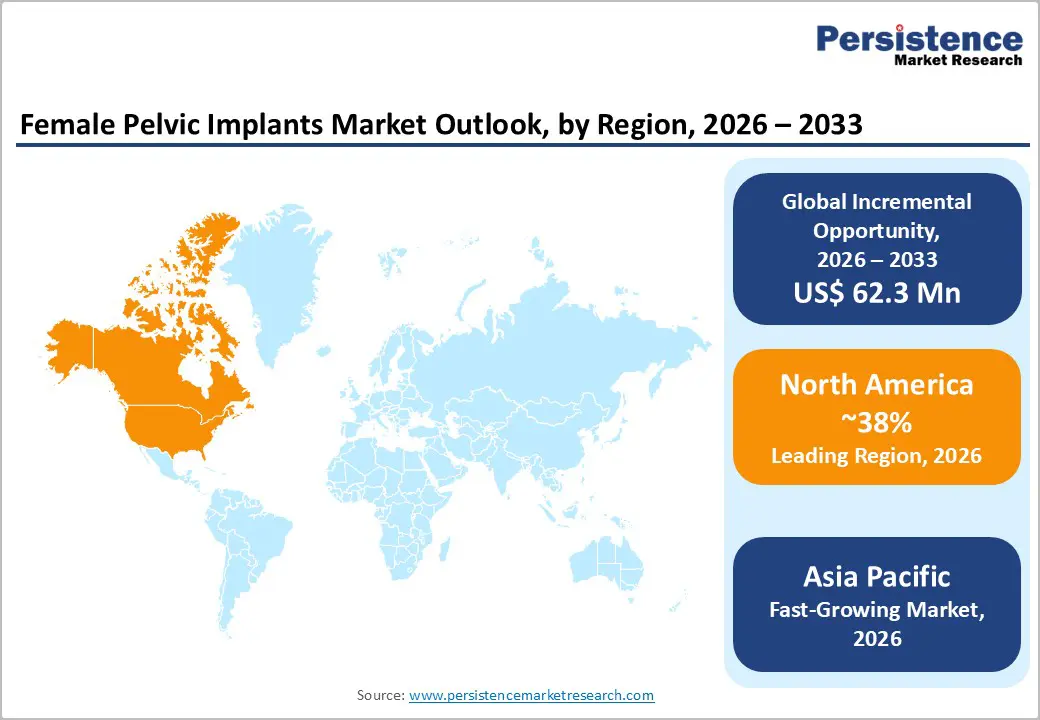

- Dominant Region: North America is projected to hold around 38% share in 2026, driven by advanced surgical infrastructure and strong reimbursement frameworks.

- Fastest-growing Market: Asia Pacific is projected to be the fastest-growing market between 2026 and 2033, supported by surgical expansion in China and India and advanced medical technologies in Japan and South Korea.

- Leading Product Type: Vaginal sling implants are projected to secure around 45% share in 2026, reflecting strong clinical acceptance and minimal invasiveness in stress urinary incontinence treatment.

- Fastest-growing Product Type: Vaginal graft implants are expected to be the fastest-growing segment during 2026–2033, propelled by growing demand for biologic materials in prolapse repair.

| Key Insights | Details |

|---|---|

|

Female Pelvic Implants Market Size (2026E) |

US$ 281.5 Mn |

|

Market Value Forecast (2033F) |

US$ 343.8 Mn |

|

Projected Growth (CAGR 2026 to 2033) |

2.9% |

|

Historical Market Growth (CAGR 2020 to 2025) |

2.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Prevalence of Pelvic Floor Disorders in Aging Female Population

The expanding incidence of pelvic floor disorders within the aging female population functions as a primary growth catalyst for device-based therapeutic interventions. Progressive weakening of pelvic musculature, connective tissue laxity, and post-menopausal estrogen decline contribute to structural instability in the pelvic compartment. This biological transition increases presentation rates of urinary incontinence, stress incontinence, and pelvic organ prolapse in women over 60 years of age. Clinical burden intensifies with cumulative obstetric history, elevated body mass index, chronic respiratory strain, and metabolic comorbidities that elevate intra-abdominal pressure and accelerate tissue deterioration. As life expectancy advances, the duration of symptom exposure extends, leading to higher healthcare utilization, repeat consultations, and demand for durable corrective solutions that restore anatomical support and functional continence.

Healthcare systems are observing a structural shift in patient demographics, with a larger proportion of women entering advanced age groups that are more likely to be eligible for procedures. Conservative management approaches such as pelvic floor therapy and pessary use remain relevant, yet persistent or severe cases frequently require implant-based reinforcement to stabilize weakened compartments. Hospital networks and ambulatory surgical centers report expanding urogynecology service lines aligned with demographic aging trends. Reimbursement frameworks in developed economies increasingly recognize pelvic reconstructive procedures as quality-of-life interventions rather than elective care, improving access to device-supported treatment pathways. Strategic investment in minimally invasive surgical techniques and biocompatible implant materials aligns with clinician preference for reduced complication risk and shorter recovery duration.

Technological Refinement and Minimally Invasive Surgical Adoption

The integration of advanced surgical technologies and minimally invasive techniques is reshaping clinical practice in women’s health procedures, delivering tangible improvements in precision, patient safety, and system efficiency. Robotic-assisted and laparoscopic approaches offer surgeons enhanced visualization, articulation, and control within confined pelvic anatomy, reducing operative trauma and enabling complex repairs that were once limited to open surgical access. These refinements shorten hospital stays and lower the risk profile for patients treated for pelvic floor disorders or related conditions, driving preference among healthcare providers and patients alike. Such momentum aligns with broader procedural trends in the United States, where minimally invasive surgery accounts for a significant and growing segment of surgical practice, supported by public and private healthcare emphasis on reducing recovery times and improving outcomes.

Governmental and regulatory frameworks also influence clinical adoption, with public health agencies and professional societies advocating evidence-based practices that demonstrate clear value in quality of care and system cost efficiency. Minimally invasive gynecological surgery techniques have been endorsed for their ability to lower complication rates and improve patient experience compared to traditional open surgery, reinforcing the need to invest in training and infrastructure that support these approaches. Adoption rates are further bolstered by ongoing innovation in imaging, instrumentation, and procedural protocols that expand the range of conditions amenable to less invasive repair, creating a positive feedback loop where clinical confidence and utilization grow in tandem with the sophistication of available technology.

Regulatory Scrutiny and Litigation Risk

Government oversight of surgical mesh devices used in female pelvic floor procedures stems from patient safety considerations and documented adverse outcomes, driving more demanding premarket review standards and ongoing post-market surveillance by the U.S. Food and Drug Administration (FDA). The agency’s risk classifications have shifted surgical mesh for certain uses into high-risk categories, requiring manufacturers to provide extensive safety and effectiveness data that earlier iterations of these products did not meet. This stricter regulatory environment reflects the need to assess long-term outcomes such as mesh erosion, chronic pain, infection and other complications reported through adverse event monitoring systems, prompting reevaluation of benefit-risk profiles for specific indications.

Legal exposure has played a significant role in shaping manufacturer behavior and market dynamics, with litigation outcomes highlighting the financial and reputational consequences of device-related injuries. As of early 2026, more than 103,000 product liability claims linked to transvaginal mesh products have been filed in U.S. courts and roughly 95% resolved through settlements or verdicts, illustrating extensive civil litigation activity over implant performance. Such litigation arises from allegations of inadequate risk disclosure and design flaws, and drives cautious commercial strategies, increased compliance costs and insurer scrutiny across the sector.

Patient Safety Concerns and Reputation Sensitivity

Stringent safety expectations from regulators and heightened reputational sensitivity pose major business constraints, as adverse events associated with surgical mesh implants require rigorous oversight and undermine stakeholder confidence. The U.S. FDA closely monitors adverse event reports and post-market data for urogynecologic mesh, and certain devices have been reclassified as high-risk or removed from sale when long-term safety could not be assured, signaling persistent risk concerns within regulatory frameworks. For example, surveillance and systematic evaluations have identified complication patterns, such as mesh erosion, infection, and tissue injury, that require ongoing analysis and clinician reporting through the FDA’s MedWatch program.

Reputation sensitivity influences adoption behavior among clinicians and patients, shaped by the historical context of litigation and public scrutiny of surgical mesh outcomes. Widespread adverse event narratives in both clinical and public forums have shaped provider preferences, making surgeons cautious about recommending implants perceived as controversial. Concurrent legal actions citing device-related injuries reinforce reputational risk for manufacturers, intensifying scrutiny from payers and clinical guidelines committees. At the same time, satisfied patients may be reluctant to pursue or endorse surgical options with perceived safety trade-offs, which can diminish volume growth and dampen investment appeal for novel designs.

Innovation in Biologic and Hybrid Implant Materials

The elevated demand for advanced pelvic reconstructive solutions is grounded in a substantial clinical burden. According to U.S. National Health Institute (NIH) data, an estimated 23.7% of women report at least one pelvic floor disorder, such as pelvic organ prolapse or stress urinary incontinence, across their lifetime, indicating a large and growing patient population requiring surgical intervention. Traditional synthetic materials, most notably polypropylene mesh, have been associated with chronic inflammatory reactions, erosion, and mechanical mismatch with native tissue, prompting regulatory withdrawals and heightened safety scrutiny by the U.S. FDA.

Better-performing materials offer differentiated clinical value by facilitating host-tissue integration and reducing complication rates that have historically driven reoperations and costly follow-up. Emerging biologic and hybrid scaffolds combine structural support with favorable cell-interactive environments that promote vascularization and remodeling, a capability conventional synthetics typically lack. Research on alternative polymers, such as polyurethane, polyvinylidene fluoride, and polylactic acid, demonstrates improved elasticity and mechanical compatibility with pelvic tissues, addressing fundamental failure modes linked to stiffness and inflammation.

Emerging Market Healthcare Infrastructure Expansion

Expansion of healthcare infrastructure across emerging economies represents a structural growth catalyst for advanced women’s health interventions, driven by rising public investment in hospital construction, surgical capacity, and specialist training programs. National health reforms are prioritizing broader access to secondary and tertiary care, integrating gynecology and urogynecology services into regional medical centers. Modern operating theaters, sterilization systems, imaging platforms, and post-operative care units are being deployed across tier-2 and tier-3 cities, strengthening readiness for complex reconstructive procedures. Policy frameworks aligned with universal health coverage objectives are channeling capital toward equipment procurement and clinical skill development, creating an enabling environment for higher procedural adoption rates.

Infrastructure upgrades are reshaping patient flow dynamics by decentralizing specialized care beyond metropolitan hubs. Public–private partnerships are expanding multispecialty hospitals and ambulatory surgical centers, improving affordability and reducing waiting periods for elective reconstructive procedures. Workforce expansion initiatives are increasing the number of trained surgeons and pelvic health specialists, supporting safe deployment of implant-based treatment options. Digital health integration, electronic medical records, and standardized treatment protocols are improving case identification and clinical outcomes, reinforcing physician confidence in procedural adoption. Rising female health awareness, urbanization, and improving insurance penetration are aligning with infrastructure growth to create sustainable momentum in demand.

Category-wise Analysis

Product Type Insights

Vaginal sling implants is anticipated to secure around 45% of the female pelvic implants market revenue share in 2026, reflecting strong clinical acceptance in stress urinary incontinence treatment. Sling procedures demonstrate predictable efficacy with minimally invasive techniques, supporting broad surgeon familiarity. Standardized procedural protocols enhance reproducibility and reduce complication variability. Favorable recovery timelines increase patient acceptance and physician preference. Institutional reimbursement pathways recognize sling implantation as a validated surgical standard for moderate to severe incontinence. Training programs integrate sling techniques into urogynecology curricula, reinforcing sustained utilization. Continuous product refinement improves tension adjustment mechanisms and anchoring reliability, strengthening outcome consistency.

Vaginal graft implants are expected to be the fastest-growing segment during the 2026-2033 forecast period, propelled by increasing demand for biologic and hybrid materials addressing safety perceptions. Enhanced tissue integration and lower erosion risk profiles align with regulatory expectations. Surgeons managing complex prolapse cases increasingly evaluate graft alternatives in revision scenarios. Innovation pipelines focusing on absorbable scaffolds and regenerative matrices support adoption expansion. Provider preference shifts toward individualized anatomical reconstruction strategies, supporting graft utilization growth.

Indication Insights

Pelvic organ prolapse (POP) extracts are poised to dominate with a forecasted market share of over 55% in 2026, powered by high disease burden among post-menopausal women and recurrent prolapse risk after conservative therapy. Structured diagnostic protocols improve detection accuracy. Culturally normalizing pelvic health discussions increases consultation rates. Surgical correction remains clinically indicated in advanced-stage prolapse. Institutional expertise in reconstructive gynecology sustains procedural volume concentration within this indication category. Growing life expectancy across major economies increases the at-risk female population, strengthening long-term procedural demand visibility. Clinical guidelines emphasize timely surgical referral for symptomatic stage III and IV prolapse, reinforcing standardization of treatment.

Stress urinary incontinence (SUI) is estimated to be the fastest-growing segment from 2026 to 2033, driven by expanding outpatient surgical models and the adoption of minimally invasive slings. Increasing workforce participation among women drives treatment-seeking behavior due to quality-of-life considerations. Preventive healthcare awareness campaigns and digital health information access increase early-stage diagnosis. Broader insurance coverage in developing markets improves affordability, supporting incremental growth momentum. Technological refinements in mid-urethral sling systems enhance procedural efficiency and shorten recovery timelines, aligning with ambulatory care delivery models. Day-care surgical centers and specialty urology clinics are integrating standardized continence pathways, improving patient throughput and cost optimization.

Regional Insights

North America Female Pelvic Implants Market Trends

North America is expected to lead with an estimated 38% of the female pelvic implants market share in 2026, supported by advanced surgical infrastructure and structured regulatory frameworks across the United States and Canada. A dense concentration of tertiary hospitals and accredited ambulatory surgical centers enables consistent procedural throughput across pelvic reconstructive specialties. In the United States, defined reimbursement coding systems and broad commercial insurance penetration sustain elective surgical volumes. Canada benefits from centralized clinical pathways within publicly funded hospital networks, strengthening standardized referral systems for advanced-stage pelvic floor disorders. Clear clinical guidelines issued by professional societies reinforce uniform treatment algorithms, improving surgical planning and implant selection discipline.

Leadership is further reinforced by a coordinated innovation ecosystem spanning academic institutions, specialty training centers, and device manufacturers located primarily in the United States, with collaborative research networks extending into Canada. Fellowship-driven sub-specialization in female pelvic medicine expands procedural competency and accelerates adoption of minimally invasive implant techniques. Regulatory agencies in both countries maintain stringent evaluation frameworks that elevate product quality thresholds, strengthening clinician trust in next-generation biomaterials and fixation systems. Investment in robotic-assisted platforms and advanced imaging technologies enhances operative precision in complex reconstruction cases.

Europe Female Pelvic Implants Market Trends

Europe represents a structurally mature yet innovation-driven landscape within the female pelvic implants market, characterized by disciplined regulatory oversight and standardized clinical governance across Germany, France, Italy, Spain, and the United Kingdom. Implementation of the European Union (EU) Medical Device Regulation (MDR) framework has elevated evidence thresholds for implant approval, compelling manufacturers to strengthen clinical validation and post-market surveillance systems. This regulatory rigor enhances product credibility and supports physician confidence in advanced biomaterials and refined mesh architectures. Concentrated academic centers in Germany and the United Kingdom continue to generate peer-reviewed outcome data in urogynecology, reinforcing protocol-based surgical selection.

Market stability is reinforced by demographic aging trends and strong subspecialization in female pelvic medicine. Multidisciplinary pelvic floor units integrate gynecology, urology, and colorectal expertise, improving comprehensive case management and reducing revision rates. Day-surgery optimization initiatives within the United Kingdom and Germany are increasing efficiency in minimally invasive sling and prolapse repair procedures, supporting cost containment objectives within publicly funded systems. Procurement models emphasize value-based evaluation, encouraging adoption of implants demonstrating durable functional outcomes and low complication profiles. Cross-border clinical collaboration and registry-based outcome monitoring strengthen transparency and quality benchmarking across hospital networks.

Asia Pacific Female Pelvic Implants Market Trends

Asia Pacific is forecast to be the fastest-growing market for female pelvic implants between 2026 and 2033, driven by rapid expansion of surgical infrastructure and specialist capacity across major healthcare systems. China and India are accelerating tertiary hospital development and integrating urogynecology units within multispecialty public institutions, increasing procedural access in high-density urban and semi-urban clusters. Japan and South Korea are advancing minimally invasive gynecological surgery through technology-enabled operating environments and structured clinical training pathways. Public health modernization programs are elevating institutional readiness for complex pelvic floor reconstruction, while growing private hospital networks are increasing competitive service delivery standards.

Growth momentum is reinforced by evolving reimbursement frameworks and rising female workforce participation across these economies. Insurance penetration is expanding within urban middle-income populations, reducing out-of-pocket burden for elective corrective procedures. Digital health platforms are improving early symptom recognition and referral efficiency, supporting stronger conversion from diagnosis to surgical intervention. Domestic medical device manufacturing initiatives in China and India are improving pricing flexibility and supply chain responsiveness, while Japan and South Korea continue to emphasize precision-engineered implant technologies supported by stringent regulatory oversight. Academic–industry collaboration programs are generating localized clinical evidence, enhancing physician confidence and accelerating adoption cycles.

Competitive Landscape

The global female pelvic implants market structure reflects moderate concentration, with multinational corporations shaping competitive structure through scale advantages, diversified portfolios, and established clinical networks. Boston Scientific Corporation, Coloplast Corp, and Johnson & Johnson Services, Inc. command meaningful revenue share through integrated commercialization strategies and broad distribution access across hospital and ambulatory surgical channels. These organizations leverage global regulatory expertise, structured post-market surveillance systems, and multicenter clinical trials to reinforce product credibility. Competitive strength is derived from disciplined quality systems, portfolio bundling capabilities, and long-standing relationships with urogynecology specialists.

Focused product development strategies emphasize niche graft configurations and tailored anatomical designs aligned with specific surgical techniques. These firms compete by offering customization flexibility and responsive technical support to specialist surgeons operating in concentrated pelvic health centers. Competitive differentiation across the broader landscape centers on demonstrable safety outcomes, transparent risk communication, and adherence to evolving regulatory frameworks that demand robust clinical documentation. Market participants increasingly prioritize real-world evidence generation and registry participation to sustain trust among providers and payers.

Key Industry Developments

- In September 2025, Medtronic received U.S. FDA approval for its Altaviva device, a minimally invasive implantable tibial neuromodulation system designed to treat urge urinary incontinence. The small device is implanted near the ankle and delivers electrical stimulation to regulate bladder control.

- In August 2025, Boston Scientific Corporation announced that results from clinical studies featuring its women’s health products, including pelvic floor reconstruction and mid-urethral sling systems, were set to be presented at the joint International Continence Society (ICS) and International Urogynecological Association (IUGA) annual meeting, highlighting research on synthetic meshes and sling performance in pelvic surgery.

- In February 2025, researchers at the Hudson Institute reported development of next-generation degradable 3D-printed meshes for pelvic organ prolapse repair that aim to support tissue regeneration and reduce foreign body response compared with traditional non-degradable options.

Companies Covered in Female Pelvic Implants Market

- Boston Scientific Corporation

- Coloplast Corp

- Johnson & Johnson Services, Inc.

- Dipromed Srl

- Betatech Medical

- Promedon Group

- Caldera Medical

- Cook Medical

Frequently Asked Questions

The global female pelvic implants market is projected to reach US$ 281.5 million in 2026.

Rising prevalence of pelvic organ prolapse and stress urinary incontinence, expanding access to reconstructive surgery, and growing adoption of minimally invasive implant technologies are driving the market.

The market is poised to witness a CAGR of 2.9% from 2026 to 2033.

Expansion of surgical infrastructure in emerging economies, development of next-generation biocompatible and degradable implant materials, and rising adoption of minimally invasive outpatient procedures represent the key market opportunities.

Some of the key market players include Boston Scientific Corporation, Coloplast Corp, and Johnson & Johnson Services, Inc.