- Electrical Equipment & Services

- Outdoor Warning Siren Market

Outdoor Warning Siren Market Size, Share, and Growth Forecast, 2026 – 2033

Outdoor Warning Siren Market by Coverage Pattern (Directional, Rotating, Omni-directional), Range (Below 2500 Feet, 2500–5000 Feet, Above 5000 Feet), Source (Mechanical, Electromechanical, Electronic), and Regional Analysis for 2026-2033

Outdoor Warning Siren Market Share and Trends Analysis

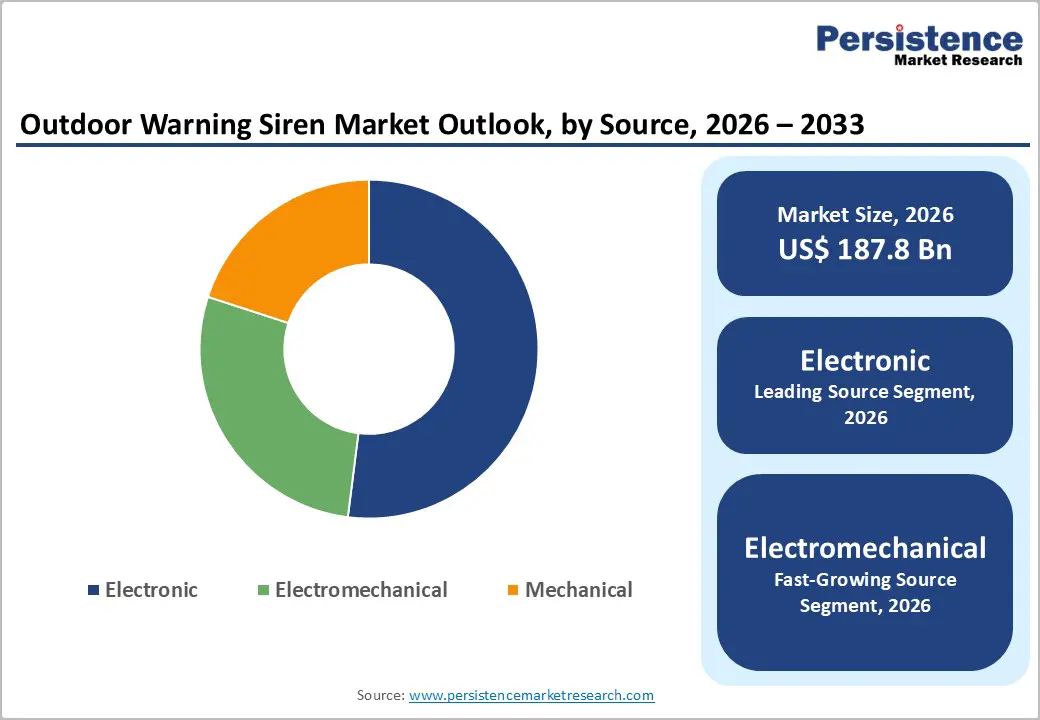

The global outdoor warning siren market size is likely to be valued at US$ 187.8 billion in 2026, and is projected to reach US$ 269.6 billion by 2033, growing at a CAGR of 5.3% during the forecast period 2026−2033. Growth outlook remains positive due to rising disaster-preparedness requirements, infrastructure modernization programs, and expansion of public safety communication networks. Increasing urban density elevates risk exposure to natural hazards, prompting municipal authorities to implement mass notification systems capable of rapid geographic coverage. Integration of digital control technologies enhances reliability, remote activation, and interoperability with emergency platforms, strengthening adoption among civil defense agencies.

Public awareness initiatives led by organizations such as United Nations Office for Disaster Risk Reduction encourage national preparedness frameworks, indirectly supporting deployment of acoustic warning infrastructure. Healthcare system resilience planning also stimulates installation of siren networks around hospitals and industrial zones where emergency evacuation capacity remains critical. Expansion of smart-city programs contributes to technology convergence between sirens, sensors, and communication networks, improving real-time alert dissemination.

Key Industry Highlights

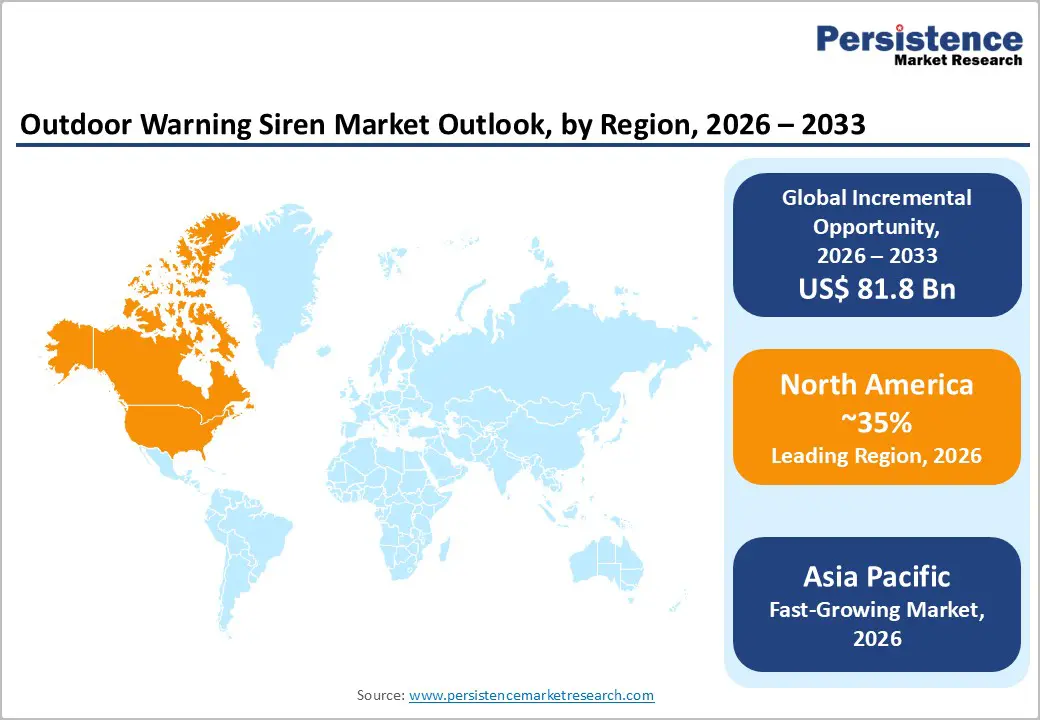

- Dominant Region: North America is projected to lead with about 35% market share in 2026, owing to the concentration of high-risk industrial and coastal zones and mandated layered public-warning frameworks.

- Fastest-growing Market: Asia Pacific is projected to be the fastest-growing market during 2026–2033, driven by rapid infrastructure expansion, rising disaster-preparedness investments, and industrial risk monitoring needs.

- Leading Source: The electronic segment is expected to hold about 52% revenue share in 2026, propelled by strong reliability, programmable functionality, and remote activation capability.

- Fastest-growing Source: The electromechanical segment is projected to be the fastest-growing between 2026 and 2033, fueled by a soaring demand for hybrid systems offering mechanical durability and electronic control flexibility.

| Key Insights | Details |

|---|---|

| Outdoor Warning Siren Market Size (2026E) | US$ 187.8 Bn |

| Market Value Forecast (2033F) | US$ 269.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.8% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Expansion of National Emergency Preparedness Frameworks

Structured national preparedness architectures create sustained procurement cycles, standardized technical specifications, and mandated readiness benchmarks that stimulate demand for large-scale public alert infrastructure. Fiscal Year 2025 data from the Federal Emergency Management Agency confirms that US$ 40 million in funding was allocated under the Next Generation Warning System Grant Program to strengthen alert and warning capabilities through advanced technologies, training, and cross-jurisdiction coordination. Such allocations signal institutional prioritization of integrated public warning capacity, prompting regional authorities, municipalities, and critical-infrastructure operators to modernize legacy acoustic systems and deploy interoperable notification networks. Government frameworks emphasize resilience standards, interoperability protocols, and response-time thresholds, leading procurement agencies to specify high-decibel outdoor signaling equipment capable of functioning across extreme environmental conditions and infrastructure disruptions.

National preparedness strategies also formalize operational drills, compliance audits, and infrastructure assessments, creating recurring replacement cycles for acoustic alert assets. A nationwide civil defence exercise conducted across 244 districts in India during 2025 incorporated air-raid siren testing, evacuation simulations, and public readiness training, demonstrating institutional reliance on physical alert technologies during crisis scenarios. Such exercises expose equipment gaps, stimulate modernization budgets, and reinforce regulatory expectations for audible mass-notification coverage. Policy frameworks further integrate multi-channel alert ecosystems combining broadcast, wireless, and acoustic signaling, reinforcing the strategic role of fixed siren infrastructure within layered communication architectures.

Advancement of Smart Infrastructure and Digital Control Systems

Integration of intelligent infrastructure platforms and digitally managed control environments elevates demand for advanced public alert systems through centralized command capability, predictive analytics, and synchronized response protocols. Urban administrations increasingly deploy integrated monitoring architecture that links sensors, surveillance networks, weather feeds, and safety dashboards into unified control rooms. A 2025 government-documented initiative highlights scale: the Federal Communications Commission technical report on next-generation networks describes ongoing national deployment frameworks designed to support real-time data exchange across critical infrastructure layers, establishing a backbone for automated emergency communications. Such digital ecosystems enable authorities to trigger coordinated alerts instantly across multiple channels, strengthening readiness for climate hazards, industrial incidents, and security threats.

Digital control ecosystems reshape operational efficiency through remote diagnostics, automated testing cycles, and fault detection algorithms embedded within urban management platforms. Smart-city implementations demonstrate practical impact: integrated surveillance and mapping systems in recent municipal projects support real-time monitoring across thousands of sensor points, enabling faster hazard identification and response coordination. Centralized dashboards allow administrators to activate warning networks, adjust broadcast zones, and verify coverage without manual field intervention, reducing latency during crisis scenarios.

Acoustic Coverage Limitations in Complex Urban Environments

Complex metropolitan environments impose structural and acoustic barriers that restrict effective signal reach of emergency siren systems. Dense infrastructure clusters generate reflection, diffraction, and absorption effects that distort wave propagation patterns, reducing intelligibility across streets, transit corridors, and high-rise clusters. Continuous traffic movement, rail activity, aviation corridors, and commercial operations create persistent background noise layers that weaken signal-to-noise ratios required for rapid public recognition. Reinforced concrete, steel frameworks, and glass façades intensify reverberation, producing echo overlap that blurs tonal clarity and diminishes directional perception. Acoustic shadow zones emerge behind large buildings and elevated roadways, limiting uniform sound distribution even when output capacity aligns with regulatory parameters.

Operational deployment in vertically expanding urban centers introduces further constraints. Rooftop installations struggle to penetrate lower street canyons, while ground-level devices face difficulty reaching upper residential floors, resulting in fragmented coverage footprints. Mixed-use zoning increases variability in ambient conditions across short distances, complicating calibration and placement strategies. Regulatory noise limits restrict permissible output intensity, narrowing the operational margin required to overcome environmental masking. Public sensitivity to noise exposure increases scrutiny of high-decibel warning signals, influencing municipal approval processes and installation timelines.

Supply-Chain Dependency on Specialized Components

Reliance on precision acoustic drivers, control circuitry, power amplifiers, and weather-resistant enclosures creates structural procurement risk across emergency alert infrastructure manufacturing. Production of such inputs depends on niche suppliers specializing in defense-grade electronics, corrosion-resistant alloys, and high-decibel transducers. Limited supplier diversity concentrates bargaining power upstream, raising input pricing volatility and extending contract negotiation cycles. Certification requirements tied to civil-defense standards further restrict vendor substitution, since components must comply with strict acoustic output, durability, and signal-clarity specifications before integration into warning assemblies.

Lead-time rigidity intensifies operational exposure within manufacturers and municipal procurement agencies. Fabrication of high-output siren motors and signal controllers involves custom tooling, low-volume production runs, and calibration procedures requiring skilled technical labor. Disruptions affecting semiconductor fabrication plants, magnet processing facilities, or specialty resin suppliers cascade through procurement schedules, delaying installation projects tied to public-safety modernization programs. Inventory buffering offers limited mitigation since many components degrade during long storage or require firmware compatibility with current communication protocols. Contracting authorities therefore face scheduling uncertainty, budget variance, and deployment delays when upstream suppliers experience logistics interruptions, export licensing reviews, or production backlogs.

Expansion across Climate-Vulnerable Emerging Economies

Investment prioritization in hazard-exposed developing regions reflects escalating disaster frequency, infrastructure fragility, and population density patterns that elevate demand for mass-notification capability. Government-linked international data indicates 40 % of global land area faces increasingly frequent and severe drought conditions as of 2025, intensifying wildfire risk, agricultural disruption, and emergency response requirements. Public safety frameworks in such environments emphasize rapid alert dissemination across rural and peri-urban zones where telecommunications penetration remains uneven. Budget allocations therefore favor wide-coverage acoustic systems that operate independent of cellular networks, strengthening resilience planning for cyclones, floods, landslides, and heatwaves.

Operational realities in emerging economies reinforce procurement rationale. Disaster mortality spikes correlate strongly with gaps in preparedness capacity and early-warning penetration, especially where reporting systems remain fragmented and hazard monitoring networks limited. Fiscal risk models indicate extreme events trigger long-term public-debt increases, encouraging authorities to prioritize preventive alert infrastructure rather than post-disaster recovery expenditure. Government planners therefore integrate community-level warning coverage into national resilience strategies, aligning capital deployment with climate-adaptation funding streams and international development finance eligibility.

Integration with Multi-Channel Public Alert Ecosystems

Coordinated public-alert frameworks linking sirens with broadcast, cellular, and digital notification channels create strong commercial potential through infrastructure modernization programs and civil-defense digitization initiatives. Emergency management authorities prioritize unified command communication environments that transmit synchronized warnings across multiple platforms, ensuring message consistency during natural disasters, industrial incidents, or security threats. Guidance issued by National Disaster Management Authority outlines integrated alert dissemination as a core preparedness requirement, emphasizing interoperability between acoustic signaling equipment and telecom-based notification systems through national disaster management protocols available on official government portals.

Public-safety modernization strategies supported by agencies such as Federal Emergency Management Agency highlight layered notification architecture as a resilience priority within national preparedness frameworks. Multi-channel alignment enables authorities to address diverse population segments, including individuals without smartphone access or network connectivity, through parallel delivery pathways that reinforce message reach and credibility. Cross-platform synchronization strengthens operational efficiency during high-risk scenarios by enabling unified activation protocols, centralized monitoring, and automated escalation sequences across communication assets.

Category-wise Analysis

Coverage Pattern Insights

Omni-directional is poised to lead with a forecasted 46% of the outdoor warning siren market revenue share in 2026, owing to widespread institutional preference for uniform sound distribution across populated zones. Emergency planners prioritize equipment capable of delivering consistent audio coverage without directional calibration. Omni-directional designs simplify installation planning because a single unit can cover multiple approach paths, which improves accessibility for public safety authorities. Acceptance among disaster-management agencies stems from proven effectiveness during large-scale drills conducted by organizations such as the National Disaster Management Authority (NDMA). Providers value these systems because maintenance requirements remain predictable and spare-part inventories remain standardized. Innovation in digital amplifiers improves clarity while maintaining compliance with environmental noise thresholds.

Rotating is anticipated to be the fastest-growing segment between 2026 and 2033, fueled by demand for adaptable sound projection in complex terrain. Rotational mechanisms allow sound waves to sweep across irregular landscapes, improving reach in mountainous or coastal environments. Emergency response planners consider this feature valuable for regions where obstacles disrupt fixed-direction sound propagation. Technological innovation incorporating variable-speed rotation enhances signal penetration while reducing mechanical wear. Accessibility improves since rotating units require fewer installations to cover large areas, which supports cost efficiency, and adoption accelerates among industrial complexes seeking dynamic coverage across wide facilities. Provider preference grows as programmable rotation patterns allow targeted alerts for specific zones. Integration with digital monitoring platforms enables remote calibration, increasing operational efficiency.

Source Insights

The electronic segment is slated to hold a dominant position, with an anticipated 52% revenue share in 2026, driven by high clinical credibility equivalent within safety engineering contexts, advanced reliability, and programmable functionality. Electronic sirens enable remote activation through secure networks, which enhances accessibility for emergency coordinators. Provider referrals from safety consultants often recommend digital systems due to diagnostic capabilities that allow real-time performance monitoring. Technology-enabled service delivery improves maintenance efficiency through automated alerts indicating component wear. Integration with geographic information systems (GIS) supports targeted warning strategies for different zones. Cost efficiency improves over lifecycle because software updates extend functionality without hardware replacement. Institutional buyers value compatibility with centralized control platforms.

The electromechanical segment is forecasted to be the fastest-growing source segment between 2026 and 2033, boosted by demand for hybrid solutions combining mechanical durability with electronic control flexibility. These systems deliver robust sound output while retaining programmable features that support modern emergency protocols. Provider referrals from engineering consultants often favor electromechanical models for installations requiring high acoustic intensity and resistance to extreme weather. Accessibility advantages arise from compatibility with existing infrastructure, enabling upgrades without full system replacement. Technology integration allows connection to digital command centers while maintaining mechanical reliability.

Regional Insights

North America Outdoor Warning Siren Market Trends

North America is expected to dominate with an estimated 35% of the outdoor warning siren market share in 2026, supported by high concentration of nuclear facilities, chemical manufacturing clusters, and coastal hazard zones that require permanent acoustic alert infrastructure. Federal civil-defense frameworks mandate layered public-warning coverage for industrial corridors and metropolitan belts, creating sustained procurement cycles. Large municipal budgets enable replacement of legacy mechanical sirens with network-connected electronic systems integrated into digital command platforms. Procurement patterns show preference for interoperable equipment compatible with national alert protocols, which elevates average contract value and lengthens vendor engagement periods. Strong presence of established manufacturers and defense-technology integrators reinforces supply reliability, accelerating deployment timelines for public-safety agencies.

Dominance reflects structural demand intensity rather than population scale. Extensive coastline exposure to hurricanes, tornado-prone central plains, and wildfire-affected western zones generate continuous risk-mitigation spending across multiple hazard categories. Insurance industry risk-modeling standards encourage municipalities and industrial operators to deploy certified warning infrastructure to qualify for liability reductions, indirectly stimulating equipment adoption. Advanced telecommunications backbone supports centralized activation and remote diagnostics, enabling large-scale synchronized alerts across thousands of units.

Europe Outdoor Warning Siren Market Trends

Europe demonstrates advanced deployment maturity for outdoor warning siren infrastructure due to regulatory standardization, cross-border civil protection coordination, and dense distribution of high-risk industrial facilities. Policy frameworks issued by the European Union require member states to maintain interoperable public alert mechanisms capable of operating during telecom disruption scenarios. This requirement drives procurement of standalone acoustic systems integrated with satellite and radio activation layers. Extensive rail tunnels, chemical corridors, nuclear energy sites, and flood-control dams across Germany, France, and Italy necessitate localized high-decibel warning coverage. Municipal authorities prioritize multi-hazard readiness linked to climate adaptation programs, resulting in replacement cycles for legacy siren towers with digitally addressable units capable of zone-specific signaling. Funding support from cohesion instruments sustains modernization initiatives. Public safety digitization remains strategic priority continually.

Market progression reflects institutional emphasis on population protection standards and disaster communication reliability benchmarks. Continental civil defense exercises coordinated through the European Civil Protection Mechanism test acoustic alert audibility, redundancy, and synchronization performance, influencing procurement specifications for municipalities. Coastal storm surges along North Sea belts, alpine avalanche zones, and river floodplains along the Danube basin sustain investment justification for high-power siren arrays. Urban density patterns encourage installation of networked systems capable of segmented activation to prevent unnecessary alarm spread. Manufacturers benefit from technical certification pathways aligned with harmonized safety directives, reducing market entry barriers across multiple countries.

Asia Pacific Outdoor Warning Siren Market Trends

Asia Pacific is forecasted to be the fastest-growing market for outdoor warning sirens between 2026 and 2033, stimulated by rapid urban infrastructure expansion, rising disaster-preparedness investments, increasing industrial risk-monitoring requirements, and government-led deployment of integrated public alert networks across densely populated and hazard-exposed economies. Large metropolitan development corridors across China, India, Vietnam, and Indonesia require wide-coverage acoustic alert infrastructure linked with centralized command platforms. National resilience programs prioritize early-warning capability within coastal belts, seismic zones, and flood-prone plains, creating sustained procurement pipelines for interoperable siren technologies compatible with digital emergency communication architecture.

Acceleration reflects structural investment intensity and regulatory modernization rather than short-term demand spikes. Industrial expansion across petrochemical hubs, export manufacturing clusters, and transport logistics corridors increases compliance requirements for certified mass-notification systems, generating parallel demand from enterprise operators and public authorities. Telecommunications network expansion enables remote activation and synchronized signaling across large territories, strengthening operational readiness during high-risk events. Participation of regional electronics manufacturers improves supply continuity, reduces acquisition cost thresholds, and supports customization aligned with local regulatory frameworks.

Competitive Landscape

The global outdoor warning siren market demonstrates moderate fragmentation characterized by coexistence of multinational engineering corporations and specialized acoustic-technology manufacturers operating across public safety and industrial risk-management domains. Competitive structure reflects capability stratification rather than volume concentration, where system reliability, interoperability, and regulatory certification determine vendor selection. Major participants such as Honeywell International Inc., Siemens, and Federal Signal Corporation control a significant portion of global revenue due to diversified technology portfolios, established government procurement channels, and extensive service infrastructure. Competitive strength derives from integration capacity linking siren platforms with satellite, cellular, and radio alert networks, enabling synchronized activation across large territories.

Competitive dynamics remain influenced by specialized firms delivering customization and regional compliance expertise suited for varied terrain, climate exposure, and communication protocols. Companies such as Eaton, Telegrafia, and Whelen Engineering differentiate through modular system design, multilingual voice broadcasting capability, and precision acoustic coverage modeling tailored for industrial zones or coastal evacuation belts. Local partnerships with emergency authorities strengthen contract acquisition potential while reducing deployment timelines.

Key Industry Developments

- In February 2026, Okmulgee County Emergency Management received FEMA funding to launch a US$ 248,000 outdoor warning siren project installing six new units and system upgrades to strengthen severe-weather alert coverage before storm season.

- In November 2025, the Texarkana Texas Fire Department began replacing ten outdoor warning sirens with a new system from Federal Signal, following City Council approval, to enhance severe-weather alert coverage and reliability across the community.

- In September 2025, Boulder County installed twenty new outdoor warning sirens and conducted a systemwide test across multiple communities to verify functionality and readiness for emergency alerts.

Companies Covered in Outdoor Warning Siren Market

- Honeywell International Inc.

- Eaton.

- Siemens

- Telegrafia a.s.

- Whelen Engineering

- Acoustic Technology, Inc.

- American Signal Corporation

- Hörmann

Frequently Asked Questions

The global outdoor warning siren market is projected to reach US$ 187.8 billion in 2026.

The market is driven by rising investments in disaster preparedness, expansion of public safety infrastructure, and adoption of digitally integrated emergency alert systems.

The market is poised to witness a CAGR of 5.3% from 2026 to 2033.

Key market opportunities include expansion of disaster-preparedness infrastructure in emerging economies, integration with multi-channel digital alert ecosystems, and deployment across industrial and smart-city safety networks.

Some of the key market players include Honeywell International Inc., Eaton, Siemens, Telegrafia a.s., and Whelen Engineering.