- Home Care & Utilities

- Outdoor Furniture Market

Outdoor Furniture Market Size, Share, and Growth Forecast, 2026 - 2033

Outdoor Furniture Market by Material (Polyester, Wood, Plastic, Other), Product Type (Table, Chair, Dinning Set, Others), Sales Channel (Wholesaler, Direct Sales, Online Retail), Application (Commercial, Residential), and Regional Analysis 2026 – 2033

Outdoor Furniture Market Size and Trends Analysis

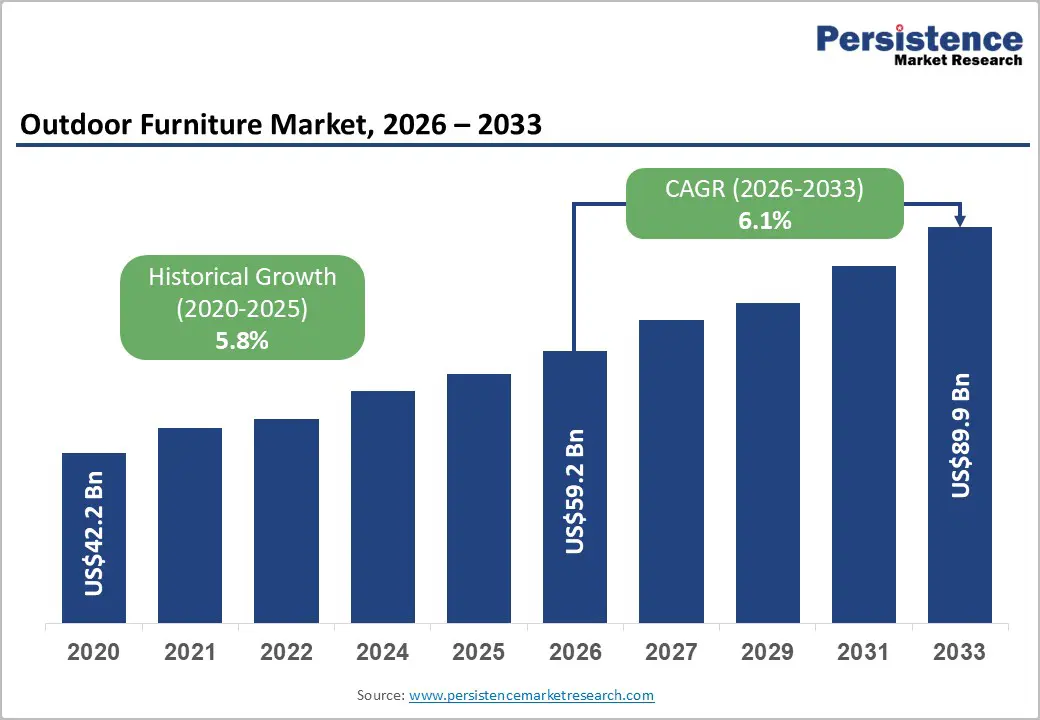

The global outdoor furniture market size is likely to be valued at US$59.2 billion in 2026 and is projected to reach US$89.9 billion by 2033, growing at a CAGR of 6.1% during the forecast period between 2026 and 2033, driven by rising consumer expenditure on outdoor living spaces, consistent increases in home improvement, and leisure spending. Rising awareness regarding the longevity of furniture assets in volatile climates ranging from intense UV exposure to heavy precipitation is a primary catalyst for cover adoption. Stringent durability and weather-resistance requirements are pushing material innovation, while the expansion of e-commerce platforms is significantly enhancing product accessibility. Growth is further reinforced by the expansion of online retail and direct sales channels, alongside increasing adoption of outdoor furniture in urban residential and hospitality projects.

Key Industry Highlights:

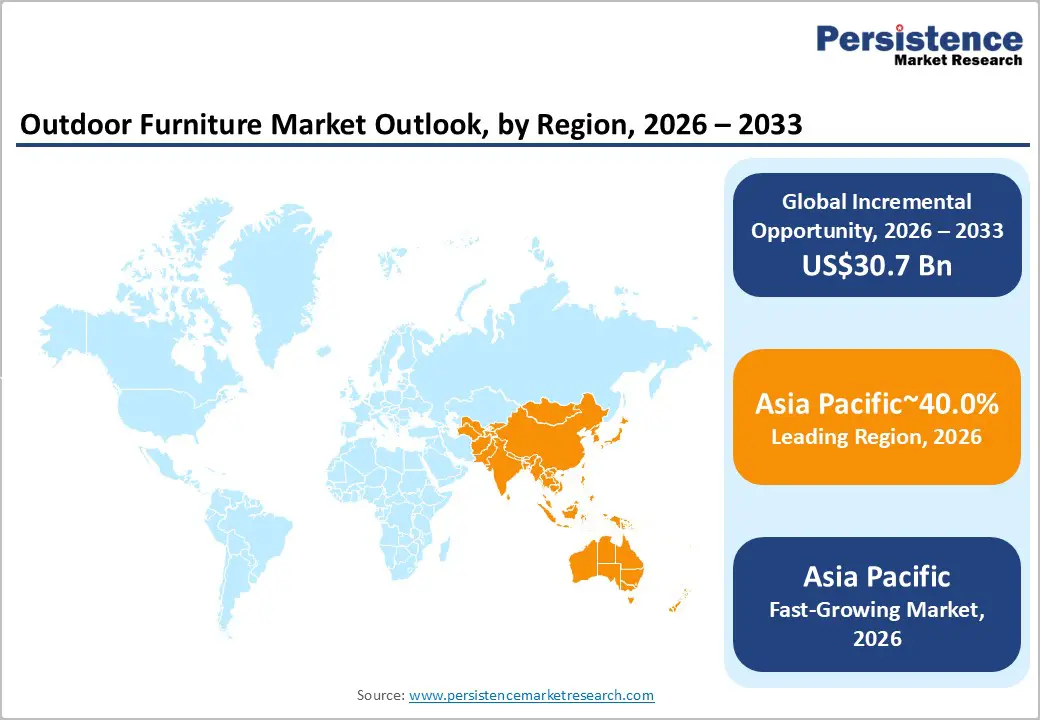

- Leading Region: Asia Pacific is expected to be the leading region in the outdoor furniture market, accounting for over 40% of the global demand. Leadership is driven by large-scale manufacturing capacity, rising residential consumption, rapid urbanization, and sustained expansion of hospitality and tourism infrastructure across China, India, and Southeast Asia.

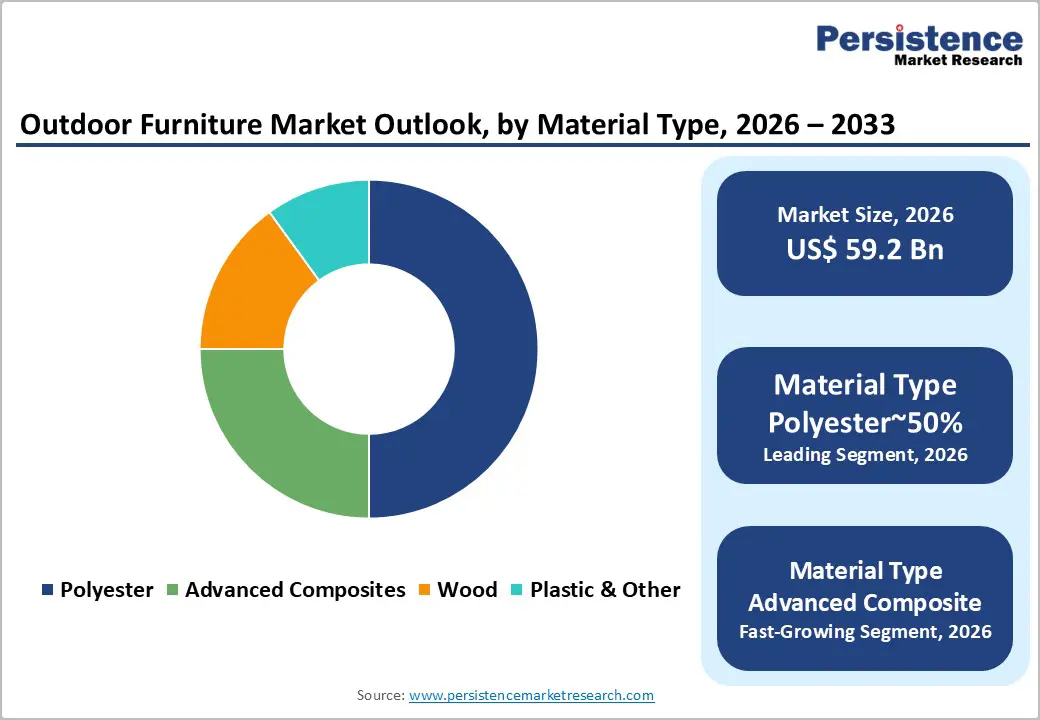

- Leading Material: Polyester is expected to remain the leading material in the outdoor furniture market, accounting for approximately 50% of fabric and upholstery usage. Its dominance is reinforced by durability, UV resistance, moisture tolerance, and design flexibility, enabling mass-market scalability across residential and commercial outdoor environments.

- Leading Application: Residential use is expected to remain the leading application segment, representing nearly 60% of total demand. Growth is anchored in the structural shift toward outdoor spaces as permanent extensions of indoor living, supported by home renovation activity and hybrid work lifestyles.

- Strategic developments: Industry participants focus on innovation, omnichannel expansion, and sustainable materials, with increased collaboration between furniture brands and cover manufacturers to offer bundled, higher-value solutions.

| Key Insights | Details |

|---|---|

| Outdoor Furniture Market Size (2026E) | US$ 59.2 Bn |

| Market Value Forecast (2033F) | US$ 89.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.8% |

Market Factors – Growth, Barrier, and Opportunity Analysis

Rising Investments in Premium Outdoor Living Spaces

Rising spending on premium outdoor living areas is pushing steady demand for reliable protective covers. As more households treat patios and decks as usable living zones, the value of outdoor sofas, dining sets, and modular pieces has increased. Higher-ticket purchases make buyers more cautious about damage from sunlight, moisture, or dust, turning protective covers from a nice-to-have into a necessary safeguard.

Consumer behavior data show a clear pattern: buyers typically allocate about 10 to 15% of their furniture spend to covers. This spending helps prevent early wear, staining, and weather-related deterioration, reinforcing stable aftermarket demand. As climate exposure becomes more unpredictable, households prefer covers that offer stronger UV protection, multi-layer fabrics, and longer service life. These shifts support steady revenue growth for the protective cover segment and strengthen its role within the broader outdoor living market.

Intense Competition from Low-Cost Generic Products

Intense competition from low-cost, generic covers continues to pressure the market, especially as online marketplaces make entry easier for unbranded suppliers. The technical barriers are relatively low; many products enter the market without verified material standards, UV ratings, or durability testing. These offerings compete almost entirely on price, which pulls a large share of cost-sensitive buyers toward short-lifecycle products. The increase in market fragmentation & reduction in visibility of performance make it harder for premium brands to demonstrate the value of higher-grade fabrics or verified protection levels.

Branded manufacturers face added challenges in consumer education, as many buyers prioritize immediate affordability over long-term durability or sustainability benefits. This reduces the pace at which higher-quality, certified, or eco-engineered covers gain adoption. The resulting price compression affects margins and weakens incentives for material innovation, even as weather-related risks and durability expectations rise. In this environment, differentiation relies more on clear performance claims, trusted testing standards, and stronger communication of lifetime value rather than short-term cost.

Customization and Made-to-Measure Solutions

Customization and made-to-measure solutions are emerging as a structurally advantaged opportunity as standard-size covers increasingly fail to accommodate modular sectionals, asymmetrical loungers, mixed-material hybrids, and expanding multi-piece configurations. The growing shift toward premium outdoor layouts exposes clear fit limitations in universal Stock Keeping Units (SKUs), where loose tolerances reduce moisture control and accelerate abrasion, reinforcing the need for precision coverage. Digital dimension-capture, mobile scanning workflows, and streamlined on-demand manufacturing now allow producers to deliver tailored covers with materially shorter lead times, strengthening alignment between furniture complexity and protection performance. The segment remains under-penetrated relative to the installed base of non-standard formats, creating room for targeted scaling.

This capability supports premium pricing, with custom-fitted solutions consistently achieving higher margins than universal categories due to tighter patterning, enhanced material utilization, and reduced fit-related claims. The model also compresses inventory exposure, shifting value generation toward engineered accuracy rather than broad SKU proliferation. As households invest more in modular furniture ecosystems with multi-unit configurations, demand rises for exact-fit covers to preserve these high-value setups. These dynamic positions made-to-measure offerings as a commercially attractive pathway for differentiation in a market pressured by generic, low-cost incumbents.

Category–wise Analysis

Material Type Insights

Polyester is expected to remain the leading material in the outdoor furniture market, accounting for approximately 50% of the fabric and upholstery segment. Its dominance is driven by its unmatched adaptability, allowing manufacturers to replicate the visual and tactile qualities of premium natural fibers such as linen, wool, and silk while preserving durability under outdoor exposure. Polyester is widely adopted across both mass-market and mid-premium collections due to its balance of aesthetic flexibility, color retention, and moisture resistance. The material supports indoor-outdoor continuity in furniture design, aligns with evolving sustainability expectations through recycled feedstocks, and enables high-volume production without compromising performance. These attributes make polyester the most widely specified material across residential patios, hospitality seating, and high-traffic commercial environments.

Advanced composites, including wood-plastic composites and fiber-reinforced polymers, are anticipated to be the fastest-expanding material category within the outdoor furniture market. Growth is supported by rising demand for materials that outperform wood and metal in variable climates while meeting durability, maintenance, and sustainability expectations. Composites offer high structural strength, design precision, and resistance to moisture, UV exposure, and biological degradation, making them increasingly attractive for urban residential settings and large-scale hospitality projects. Ongoing innovation in bio-based resins, modular manufacturing, and integrated functional features is likely to accelerate adoption, positioning composites as a preferred alternative for long-life, design-driven outdoor furniture applications.

Application Insights

The residential segment is expected to remain the leading end-use category in the outdoor furniture market, accounting for approximately 60% of total demand. This dominance reflects a sustained structural shift in household behavior, where outdoor spaces are increasingly treated as permanent extensions of indoor living environments rather than seasonal amenities. Post-pandemic lifestyle normalization around remote and hybrid work is anticipated to continue driving investment in multifunctional residential furniture, including dining-led work surfaces, modular seating, and compact balcony solutions. Rising renovation activity, generational home transfers, and growing emphasis on wellness-oriented outdoor living are likely to reinforce residential demand. Brands such as IKEA, Wayfair, Polywood, and Ashley Furniture Industries are positioned to benefit from volume-driven purchases, customization tools, and sustainability-aligned materials such as FSC-certified wood and recycled composites.

The hospitality segment is projected to be the fastest-growing application area, supported by global tourism recovery and the monetization of outdoor commercial spaces. Hotels, resorts, restaurants, and bars are increasingly treating outdoor areas as year-round revenue assets, accelerating demand for contract-grade, high-durability furniture with rapid replacement cycles. Growth is expected to be strongest in rooftop venues, resort developments, and urban mixed-use projects, where modularity, branding customization, and weather resilience are critical. Regulatory alignment around fire safety, durability standards, and sustainability compliance is likely to favor established suppliers such as Kettal, Vondom, Kimball Hospitality, and Akula Living, reinforcing hospitality’s above-market growth trajectory.

Regional Insights

Asia Pacific Outdoor Furniture Market Trends

Asia Pacific is expected be a leading as well as the fastest-growing region, holding a leading share of over 40% and benefiting from rapid urbanization, rising disposable incomes, and continued tourism and hospitality expansion. Regulatory conditions vary, but major economies increasingly adopt durability, weather-resilience, and material-safety standards that influence procurement across residential and commercial segments. China retains a dual position as both a structural manufacturing hub and a growing consumption base, with demand supported by real estate upgrades and domestic travel. India and ASEAN markets add further scale, each shaped by climate-specific exposure such as monsoons, humidity, and high UV intensity, which sustains the need for reinforced protective materials.

Regional infrastructure strength is defined by its manufacturing concentration, with China and Vietnam producing most of the global supply and enabling competitive export capability. Demand diversification across urban households, hospitality operators, and emerging e-commerce channels contributes to steady adoption. Competitive activity remains broad, balancing global brands with OEM-led supply chains that prioritize cost efficiency and customization. These dynamics position Asia Pacific as the core production ecosystem and a rising

North America Outdoor Furniture Market Trends

North America is expected to maintain a stable position at an estimated 35%, supported by a sophisticated consumer base that evaluates technical specifications and drives consistent premium uptake in 2026. The region’s regulatory oversight is shaped by strict flammability controls and disclosure. The compliance layers position North America as an innovation-driven environment where product differentiation relies on technical credibility, durability enhancements, and measurable performance attributes that align with evolving safety expectations.

Infrastructure maturity supports advanced retail and DTC models, while demand stability is reinforced by high discretionary spending and structured replacement cycles. Private equity activity continues to increase, with investors consolidating smaller players into integrated outdoor living platforms that link protection products with furniture, heating, and broader home-lifestyle categories. This consolidation trend strengthens procurement scale, accelerates R&D coordination, and elevates competitive intensity, positioning North America as a benchmark region for innovation governance and capability depth relative to global peers.

Europe Outdoor Furniture Market Trends

Europe is expected to maintain a stable, mature marketing position at roughly 28%, supported by a regulatory environment that prioritizes chemical safety, waste reduction, and circular-economy alignment under frameworks such as Registration, Evaluation, Authorization and Restriction of Chemicals (REACH) and evolving eco-design mandates. These policies influence material selection, accelerate shifts toward recyclable and low-toxicity inputs, and reinforce Europe’s role as a regulatory benchmark for compliance-driven product development. Demand remains concentrated in Germany, the U.K., and France, while Southern Europe experiences stronger momentum due to climate-related wear and sustained hospitality sector requirements.

Infrastructure strength, characterized by dense urban housing and established DIY retail networks, supports a structured mix of private-label penetration and specialized manufacturers. Market maturity encourages differentiation through compliance readiness, lifecycle-oriented design, and suitability for constrained living spaces such as balconies and compact patios. Growth potential is shaped by the region’s ability to align product attributes with environmental mandates, positioning Europe as a reference point for sustainability governance and harmonized regulatory progression across global markets.

Competitive Landscape

The global outdoor furniture market is moderately fragmented, with a combination of global manufacturers, regional specialists, and private-label brands competing across price tiers. Leading players collectively account for a meaningful but not dominant share of global revenue, with long-tail competition from smaller producers in key regions. Competitive positioning often hinges on material technology, product range breadth, brand reputation, and distribution capabilities across wholesale, direct sale, and online channels.

Key Industry Developments:

- In July 2025, BIFMA published the OF-2025 Outdoor Furniture Whitepaper on durability and environmental performance standards. The whitepaper provided guidelines for withstanding harsh conditions, helping manufacturers achieve compliance, improve products, and build consumer trust in long-lasting furniture.

- In April 2025, IKEA launched the STOCKHOLM-25 collection, featuring updated iconic designs available globally. This affordable, high-quality refresh broadened access to stylish outdoor options, supported mass-market growth, and encouraged wider consumer investment in outdoor spaces.

- In February 2025, Luxus Home & Garden introduced sustainable outdoor living trends for Spring 2025, highlighting eco-friendly furniture. This initiative reinforced the brand’s commitment to green materials, attracted environmentally conscious buyers, and accelerated the industry’s shift toward low-impact products.

Companies Covered in Outdoor Furniture Market

- Trex Company

- Barlow Tyrie

- The Home Depot

- The Furniture Cove

- Lowe’s Companies

- IKEA

- Lowe Alpine Group

- Keter Group

- JYSK

- Amazon

- Wayfair and House Brands

- Formosa Covers

- Plastotech

Frequently Asked Questions

The global outdoor furniture market is valued at US$59.2 billion in 2026 and is projected to reach US$89.9 billion by 2033.

The outdoor furniture market is driven by rising spending on outdoor living spaces, material innovation for weather-resilient designs, and strong expansion across e-commerce and direct-to-consumer channels.

The outdoor furniture market is expected to grow at a CAGR of 6.1% between 2026 and 2033, supported by sustained residential upgrades and hospitality sector investments.

Key opportunities include premiumization of materials, sustainability-aligned engineered fabrics, and expansion of customized, made-to-measure protective solutions.

Prominent players include Trex Company, The Home Depot, Lowe’s, IKEA, Keter Group, JYSK, Amazon private-label brands, and specialized cover manufacturers worldwide.