- Semiconductor Materials & Components

- Oscilloscope Market

Oscilloscope Market Size, Share, and Growth Forecast, 2026- 2033

Oscilloscope Market by Component (Hardware, Software), Type (Analogue, Digital), End-use Industry (Medical and Life Sciences, Engineering, Automotive, IT and Telecommunications, Consumer Electronics, Aerospace and Defense, Others) and Regional Analysis for 2026 - 2033

Oscilloscope Market Size and Trends Analysis

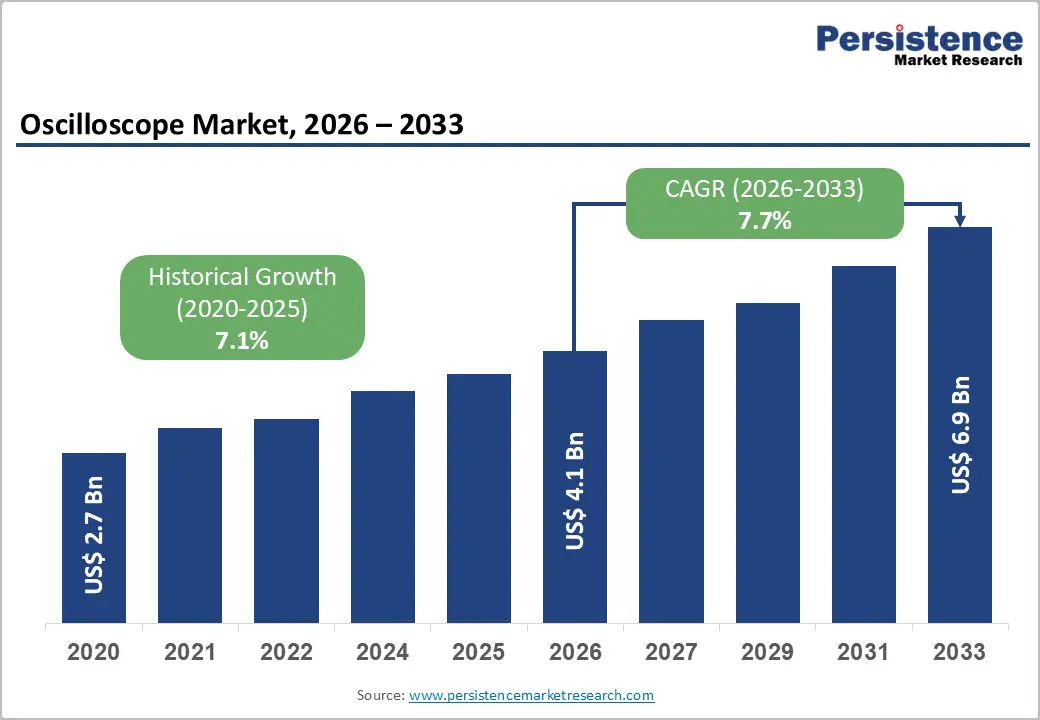

The global oscilloscope market size is supposed to be valued at US$ 4.1 Bn in 2026 and is projected to reach US$ 6.9 Bn by 2033, growing at a CAGR of 7.7% between 2026 and 2033. Drawing on the historical value of US$ 2.7 Bn in 2020, this trajectory reflects a healthy expansion underpinned by sustained R&D in electronics, rapid 5G and high-speed serial interface penetration, and the electrification of transportation and industrial systems. Rising complexity in mixed-signal designs, coupled with stringent compliance demands in sectors such as automotive, aerospace and defense, and medical devices, is driving the adoption of multi-channel, high-bandwidth digital oscilloscopes across both OEM R&D labs and production test environments.

Is growth further reinforced by surging investments in wireless infrastructure and data-center interconnects, where designers use oscilloscopes to validate signal integrity at tens of gigabits per second. The GSMA projects around 1.8 billion 5G connections by 2025, representing roughly 20-25% of total mobile connections, with penetration above 50% in developed Asia and North America. Such high-speed radio and backhaul systems require advanced time and frequency domain debug, directly stimulating demand for high-performance mixed-signal and sampling oscilloscopes. At the same time, Asia’s electronics production exceeded US$ 1.5 trillion in 2022, led by China’s output of about US$ 874 Bn, creating a large installed base of test and measurement users that will continue to refresh and upgrade their oscilloscope fleets.

Key Industry Highlights:

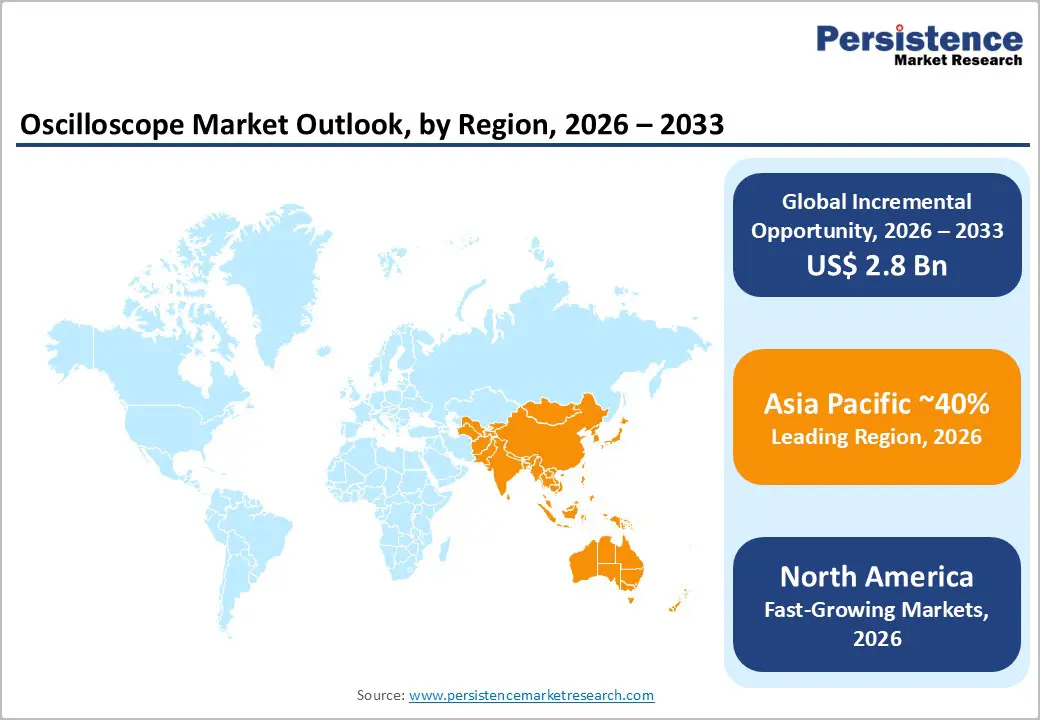

- Leading region: The Asia Pacific oscilloscope market benefits from electronics output above US$ 1.5 trillion, anchored by China’s dominance and expanding EMS capacity in India and ASEAN, making it the largest regional demand pool for test instrumentation.

- Fastest-growing region: North America is the fastest-growing region, driven by 6-7% annual growth in consumer electronics, aggressive 5G rollouts, and rapid EV adoption, which together are boosting oscilloscope deployment across R&D, production, and field-service environments.

- Dominant segment: Digital oscilloscopes form the dominant product segment, widely adopted for their deep memory, protocol decoding, and multi-domain analysis, while analogue scopes are now largely reserved for niche or educational use cases.

- Fastest-growing segment: High-resolution, multi-channel mixed-signal and sampling oscilloscopes serving 5G/6G, AI data-center, and power-electronics applications are the fastest-growing segment, supported by innovations such as 12-bit ADCs, 8-channel architectures, and ultra-fast waveform update rates.

- Key market opportunity: The combination of Asia’s expanding manufacturing footprint, EV and ADAS proliferation, and AI-driven data-center build-outs creates significant upside for vendors that offer application-specific oscilloscope solutions with localized support, flexible pricing, and strong software ecosystems

| Key Insights | Details |

|---|---|

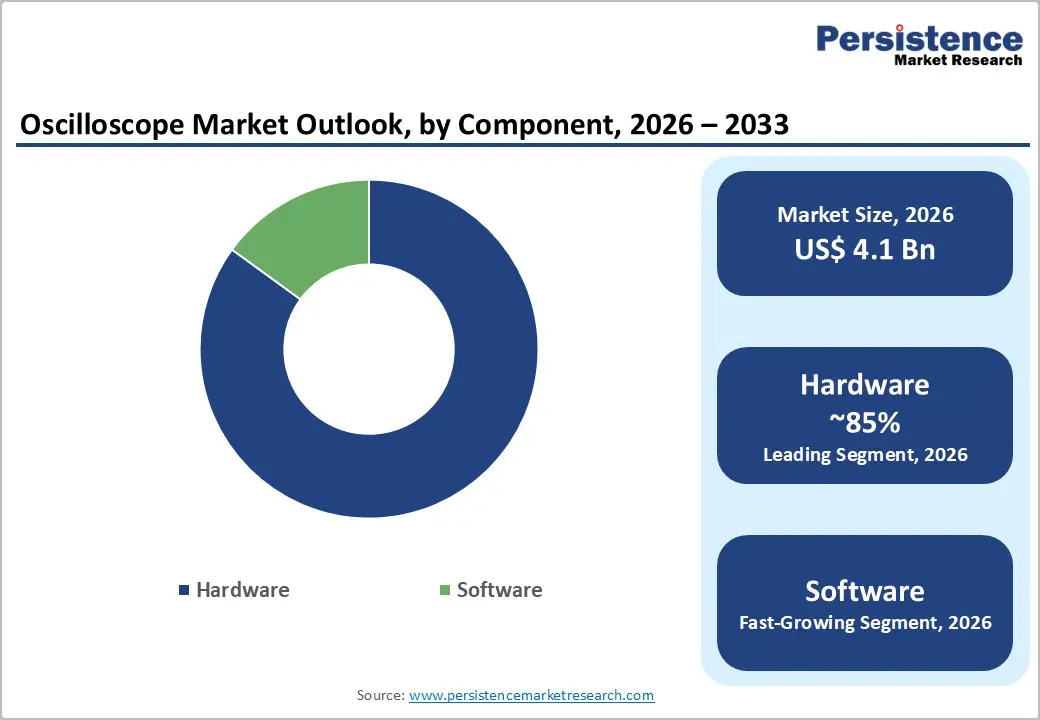

| Oscilloscope Market Size (2026E) | US$ 4.1 Bn |

| Market Value Forecast (2033F) | US$ 6.9 Bn |

| Projected Growth CAGR (2026 - 2033) | 7.7% |

| Historical Market Growth (2020 - 2025) | 7.1% |

Market Dynamics

Key Growth Drivers - Electrification, EV Adoption, and ADAS Proliferation

One of the most powerful growth engines for the global oscilloscope market is the rapid electrification of transportation and the proliferation of advanced driver assistance systems (ADAS) and in vehicle networks. The International Energy Agency (IEA) reports that global electric vehicle sales rose about 25% in 2024, reaching roughly 17.1 million units, with China accounting for close to 80% of incremental growth. These platforms integrate high-voltage battery packs, inverters, SiC/GaN power electronics, multi-gigabit automotive Ethernet, and dense sensor arrays, all of which must be validated using oscilloscopes for switching behavior, EMI, and protocol integrity. Tektronix highlights that oscilloscopes are now central to automotive diagnostics, especially for inverters, motors, and in-vehicle networks, because they provide engineers with waveform-level visibility that multimeters and scan tools cannot. As OEMs and Tier-1 suppliers scale EV and ADAS programs over the coming decade, demand for high-bandwidth, isolated, and automotive-specific oscilloscope solutions is expected to expand in lockstep.

5G/6G, High-Speed, Connectivity, and Data-Center Interconnects

The second major demand driver is the migration to 5G and emerging 6G systems, along with the shift to 1.6T and beyond optical interconnects in AI-class data centers. GSMA projections indicate that 5G will account for around 21-25% of global mobile connections by 2025, with penetration surpassing 50% in North America and advanced Asia-Pacific markets. This translates into dense deployments of massive-MIMO radios, small cells, and fronthaul/backhaul links operating at tens of GHz, which must all be characterized in both time and spectrum domains. Vendors such as Keysight Technologies have introduced sampling oscilloscopes and solutions specifically targeting 1.6T optical-transceiver testing at up to 224 Gb/s per lane, underscoring how escalating data rates are reshaping oscilloscope performance requirements. Similarly, Tektronix has embedded 5G NR analysis software into its 6 Series B MSO oscilloscopes, enabling engineers to perform 3GPP-compliant RF measurements directly on the scope, which reinforces the role of oscilloscopes as multi-domain analyzers in next-generation communication systems

Restraint - High Acquisition Cost of Advanced Multi-Channel Systems

Despite strong technology pull, the high upfront cost of advanced oscilloscopes remains a significant barrier, especially for small labs, universities, and cost-sensitive service centers. Industry commentary indicates that historically, 8-channel oscilloscopes in Europe have started at around €25,000- €28,000, positioning them as capital investments rather than routine tools. Even though new architectures such as the R&S MXO 3 and MXO 5 series have lowered entry prices and improved price-performance, the total cost of ownership still includes high-voltage probes, protocol-decode licenses, and maintenance contracts. In emerging markets and smaller organizations, this cost profile can delay refresh cycles, push users toward lower-bandwidth or second-hand equipment, and limit adoption of the most capable mixed-signal and high-resolution platforms, thereby moderating overall market penetration.

Skills Gap and Complexity in Advanced Measurements

A second constraint is the shortage of engineers with deep hands-on expertise in high-speed measurement, signal integrity, and protocol debug. Studies on the engineering workforce highlight a persistent shortfall of qualified electrical and electronics engineers, with some surveys indicating that over 70% of employers struggle to fill such roles within 6 months and that countries like the US, UK, Germany, and Japan face structural engineering skills gaps. At the same time, modern oscilloscopes integrate complex features such as multi-domain analysis, advanced FFTs, jitter decomposition, and embedded-protocol decoding. Without sufficient training and application support, many users under-utilize these capabilities or misconfigure instruments, leading to longer debug cycles and lower perceived ROI. Vendors are responding with application-specific software and education programs, but until the skills gap narrows, oscilloscope utilization, especially at the cutting edge of bandwidth and resolution, will be constrained in many organizations.

Opportunity - AI, Data-Center, and High-Resolution Multi-Domain Oscilloscopes

Another high-potential opportunity lies at the intersection of AI, cloud data centers, and ultra-high-resolution waveform analysis. AI clusters are moving rapidly toward 1.6T and future 3.2T optical links with symbol rates above 100 GBaud, which require sampling oscilloscopes with extremely low noise floors, deep memory, and integrated clock recovery. Rohde & Schwarz’s MXO 5 series, for example, offers up to 2 GHz bandwidth, 4 or 8 analog channels, 12-bit ADCs backed by an 18-bit vertical architecture, and real-time update rates above 4.5 million waveforms per second capabilities designed to capture rare events and complex interactions in power integrity and RF designs.

Similar advances from Teledyne LeCroy, Keysight, and others in high-definition and multi-domain oscilloscopes (combining digital, RF, and protocol analysis) create opportunities to displace legacy instruments in critical design centers. As AI systems, high-speed memory interfaces, and advanced packaging (such as chiplets) proliferate, the need for precise time-aligned visibility across voltage, current, and high-speed data lines will drive incremental demand for premium oscilloscopes.

Asia-Pacific Manufacturing Expansion and “China-Plus-One” Strategies

The Asia-Pacific region presents a major opportunity as it remains the world’s manufacturing hub for electronics, while OEMs diversify production footprints beyond a single country. Industry yearbooks show that Asia accounted for about US$ 1,518 Bn in electronics equipment and component production in 2022, with China alone contributing approximately US$ 874 Bn.

As multinational brands adopt “China-plus-one” strategies and expand assembly and semiconductor capacity in countries such as India, Vietnam, and other ASEAN economies, they are building new R&D centers, reliability labs, and end-of-line test lines, all of which require oscilloscopes for board bring-up, power-integrity analysis, and compliance verification. This shift also supports demand for more portable, PC-based, and modular oscilloscopes that can be deployed flexibly across distributed manufacturing footprints. Vendors that localize applications, provide regional support, and tailor pricing and leasing models to fast-growing Asian EMS and ODM customers are well positioned to capture outsized growth.

Oscilloscope Market Insights and Trends

Component Insights

Within the oscilloscope market, hardware remains the dominant component, accounting for the clear majority of total revenue because the acquisition front-end, ADCs, memory, and mechanical packaging together constitute the largest share of system cost. Industry portfolios from leading players such as Tektronix, Keysight Technologies, Rohde & Schwarz, and Teledyne LeCroy showcase broad ranges of bench, portable, and modular oscilloscopes with bandwidths from 100 MHz up to 65 GHz, underscoring the centrality of hardware innovation in competitive positioning. Software, while strategically important for protocol decoding, automation, and analytics, is typically licensed as an add-on, limiting its direct revenue contribution even though it significantly enhances lifetime value. As multi-channel high-definition scopes like the R&S MXO 5 integrate deep memory of 500 Mpoints per channel and support up to 45,000 FFT/s, hardware capability drives differentiation and justifies premium pricing, reinforcing hardware’s leadership in component-wise market share.

Product Type Insights

By type, digital oscilloscopes overwhelmingly lead the market and are expected to retain this position through 2033. Technical literature and vendor guidance consistently note that digital storage and mixed-signal oscilloscopes have largely displaced analog models in most professional applications because they offer deep memory, sophisticated triggering, protocol decoding, and PC connectivity. Articles such as “Does Anyone Still Use an Analog Oscilloscope” from Electronic Design highlight that digital scopes now deliver robust analysis features, while analog units are largely confined to niche use in audio, video, and educational settings.

At the same time, digital scopes from entry-level PC-based instruments under US$ 500 to high-end lab systems exceeding US$ 10,000 cover an enormous application space, including embedded design, RF validation, and automotive debug. As vendors continue to add higher-resolution 12-bit ADCs, mixed-domain functionality, and integrated compliance test suites, digital oscilloscopes will continue to command the dominant share of shipments and installed base, while analogue oscilloscopes maintain a small but stable footprint in cost-sensitive or legacy environments.

Industry Insights

Across end-use industries, engineering (including general electronics, industrial, and research laboratories) represents the single largest user base for oscilloscopes. Leading manufacturers position their portfolios explicitly around R&D and design validation workloads in sectors such as embedded systems, power electronics, communications, and semiconductor testing, reflecting a strong concentration of oscilloscope demand in multi-disciplinary engineering environments. In these labs, oscilloscopes are used daily for board bring-up, firmware debug, power-rail analysis, and verification of high-speed buses, making them core bench instruments alongside power supplies and spectrum analyzers.

While verticals such as automotive, IT and telecommunications, medical and life sciences, and aerospace and defense are critical and often pay for higher-end capabilities, they typically do so through specialized engineering teams and contract design houses that fall under the broader “engineering and R&D” umbrella. As product lifecycles shorten and regulatory demands tighten, these engineering-focused oscilloscope users will continue to drive a substantial share of global demand.

Regional Insights and Trends

North America Leads Premium Oscilloscope Demand Through Innovation

North America is a key demand center for high-performance oscilloscopes, underpinned by its concentration of semiconductor design houses, networking OEMs, cloud data centers, and aerospace and defense contractors. GSMA expects 5G technology to account for around 63% of mobile subscribers in North America by 2025, well above global averages, which implies intensive deployment and upgrade cycles of radio and transport equipment that rely on oscilloscopes for validation and maintenance. Additionally, North American electronics production exceeded US$ 350 Bn in 2022, with the United States accounting for nearly 79% of regional output, and the region is investing heavily in on-shore semiconductor fabrication under initiatives like the CHIPS and Science Act. These dynamics support sustained investment in advanced test and measurement equipment, including high-bandwidth mixed-signal and sampling oscilloscopes.

The region also hosts many of the world’s leading oscilloscope vendors and innovation centers, notably Keysight Technologies and Tektronix, along with a dense ecosystem of start-ups developing high-speed interfaces, automotive electronics, and quantum-computing hardware. In aerospace and defense, US primes and laboratories rely on oscilloscopes for radar, EW, and satellite link analysis, which often demands cutting-edge bandwidth, low noise, and secure, long-term support. While macro-economic cycles can influence capital spending, North America’s deep engineering skill base, advanced regulatory framework, and high adoption of subscription and service-based test models should keep the region at the forefront of premium oscilloscope demand.

Europe Drives Oscilloscope Demand Through Engineering and Innovation

Europe’s oscilloscope market benefits from strong positions in automotive engineering, industrial automation, and aerospace, particularly in countries such as Germany, France, and the United Kingdom. European governments and the European Union are investing in semiconductor resilience and 5G/fiber infrastructure, while automotive hubs in Germany and surrounding countries continue to push forward in EVs and ADAS, all of which require advanced test and measurement. At the same time, Europe is a manufacturing and R&D base for several leading oscilloscope brands, notably Rohde & Schwarz, which has launched innovative multi-channel platforms like the MXO 3 and MXO 5 to capture mid-range and high-end demand across power integrity, RF, and EMC pre-compliance applications. These developments reinforce local supply, service, and application engineering ecosystems that support widespread oscilloscope adoption across both SMEs and large enterprises.

Regulatory harmonization on EMC, safety, and telecom standards in the EU further increases mandatory testing requirements, expanding oscilloscope use in certification labs and contract testing facilities. However, growth is influenced by moderate macro-economic expansion and tight capital-expenditure controls in some industrial segments. Vendors are responding with more cost-efficient 8-channel platforms and scalable software licensing to align with European budget structures and sustainability goals. Over the forecast period, Europe is expected to maintain a substantial share of oscilloscope demand, with Germany and the UK anchoring engineering and test-equipment clusters, while countries such as Spain and Italy contribute through renewed investments in telecom and renewable-energy infrastructure.

Asia Pacific Leads Oscilloscope Demand Through Electronics Manufacturing

Asia Pacific is both the largest electronics manufacturing hub and the fastest-growing oscilloscope market, driven by high volumes of consumer electronics, expanding automotive production, and deepening telecom infrastructure. Regional data show that Asia’s electronics equipment and component output reached about US$ 1,518 Bn in 2022, with China alone contributing approximately US$ 874 Bn of that total, underscoring the region’s central role in global supply chains. At the same time, the Asia-Pacific consumer electronics market spanning countries such as China, Japan, South Korea, India, and ASEAN states is projected to grow at a CAGR of around 6-7% toward 2033, creating sustained demand for test equipment in smartphones, TVs, and smart devices.device production. EMS providers and ODMs across China, Vietnam, Malaysia, and India deploy oscilloscopes extensively for functional test, board repair, and failure analysis, generally favoring cost-effective but capable digital scopes.

The region is also rapidly rolling out 5G networks and investing in EV ecosystems, particularly in China, which accounted for nearly 80% of global EV sales growth in 2024. These trends drive requirements for oscilloscopes with automotive-specific trigger and analysis packages, high-voltage probing, and advanced RF capabilities. Asian manufacturers such as Rigol and Siglent are intensifying competitive pressure by “commoditizing” features like higher bandwidth and deep memory that were previously limited to premium Western brands, thereby accelerating adoption among local engineers and pushing incumbents to innovate in channel density, ASICs, and software. Collectively, these forces position Asia Pacific as the fastest-growing region for oscilloscopes over the 2026-2033 forecast horizon.

Competitive Landscape

The oscilloscope market is moderately concentrated, with a core group of global leaders Keysight Technologies, Tektronix, Rohde & Schwarz, and Teledyne LeCroy competing alongside fast-rising Asian vendors such as Rigol and Siglent. Competition increasingly centers on bandwidth, channel density, vertical resolution, and application-specific software, particularly in the mid-range segment where engineers demand both high-precision measurement and system-level debug capabilities.

Technological advances such as custom oscilloscope ASICs, 12-bit and 18-bit architectures, and high-speed FFT engines enable incumbents to differentiate on performance, while aggressive pricing and feature-rich entry-level units from Asian challengers are reshaping value expectations. Business models are evolving toward subscription-based software, remote-access workflows, and “oscilloscope-as-a-service” offerings, supported by cloud connectivity and licensing flexibility that align capital expenditure with project-based demand

Key Industry Developments

- In Feb 2026, Keysight Technologies launched Infiniium XR8 real-time oscilloscopes to accelerate high-speed digital and compliance testing, supporting advanced electronics development amid strong market demand for precision measurement solutions.

- In Oct 2025, Rohde & Schwarz introduced MXO 3 compact oscilloscopes with 4 and 8 channels, delivering advanced performance, precision measurement capability, and affordability through next-generation MXO technology in a space-efficient design.

- In Sep 2025, Tektronix launched its first flagship performance oscilloscope in over a decade, featuring a 25 GHz digital phosphor architecture with improved noise floor and enhanced effective number of bits for high-speed testing.

- In Jul 2024, Rohde & Schwarz introduced the industry’s first ASIC-based zone triggering for MXO oscilloscopes, enabling up to 600,000 waveforms per second and significantly improving signal capture speed and trigger accuracy.

Companies Covered in Oscilloscope Market

- Scientech Technologies Pvt. Ltd.

- Tektronix Inc.

- B&K Precision Corporation

- Keysight Technologies Inc.

- Pico Technology Holdings Ltd.

- Rohde & Schwarz GmbH & Co. KG

- Siglent Technologies Co. Ltd.

- Teledyne LeCroy Inc.

- Fluke Corporation

- Yokogawa Test & Measurement Corporation

- Rigol Technologies Inc.

- National Instruments Corporation

- Other Market Players

Frequently Asked Questions

The Oscilloscope market is estimated to be valued at US$ 4.1 Bn in 2026.

The key demand driver for the Oscilloscope Market is the rapid growth of high-speed electronics and semiconductor technologies, which require precise signal measurement and testing during product development and validation.

In 2026, the Asia Pacific region will dominate the market with an exceeding 45% revenue share in the global Oscilloscope market.

Hardware components dominate the Oscilloscope market, commanding over 85% of total market revenue in 2026, driven by the growing adoption of high-performance testing instruments used for signal measurement, waveform analysis, and circuit diagnostics across electronics R&D, semiconductor testing, telecommunications, and automotive electronics development.

Key players operating in the Oscilloscope market include Scientech Technologies Pvt. Ltd., Tektronix Inc., B&K Precision Corporation, Keysight Technologies Inc., Pico Technology Holdings Ltd., Rohde & Schwarz GmbH & Co. KG, Siglent Technologies Co. Ltd., and Teledyne LeCroy Inc.