- Medical Devices

- Nitric Oxide Asthma Testing Market

Nitric Oxide Asthma Testing Market Size, Share, and Growth Forecast, 2026 – 2033

Nitric Oxide Asthma Testing Market by Product Type (Handheld Monitors, Standalone Monitors, Others), End-User (Hospitals & Clinics, Diagnostic Centers, Home Care Settings, Others), and Regional Analysis for 2026-2033

Nitric Oxide Asthma Testing Market Share and Trends Analysis

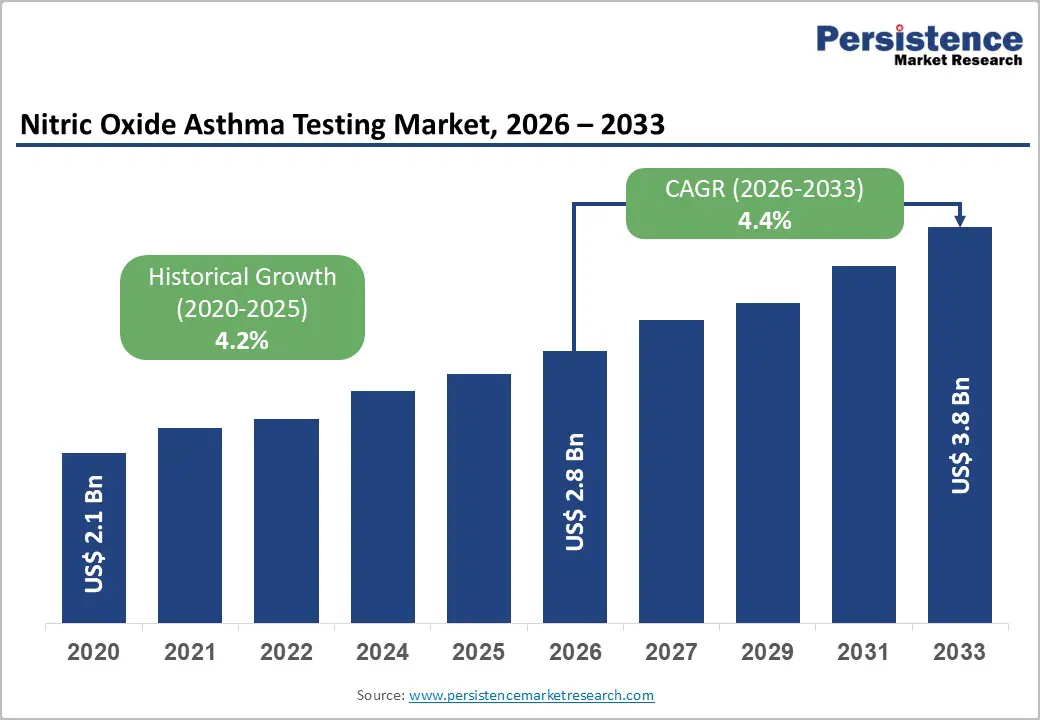

The global nitric oxide asthma testing market size is likely to be valued at US$ 2.8 billion in 2026, and is projected to reach US$ 3.8 billion by 2033, growing at a CAGR of 4.4% during the forecast period 2026−2033. Market growth is driven by rising clinical awareness of asthma management protocols.

Increasing recognition of fractional exhaled nitric oxide (FeNO) testing as a reliable biomarker enables precise diagnosis and monitoring, encouraging adoption in hospitals and specialty clinics. Expansion of treatment adoption further supports market development. Clinicians increasingly integrate FeNO testing into personalized asthma care plans to optimize anti-inflammatory therapy, improving patient outcomes. Demographic shifts contribute to demand acceleration.

Aging populations and rising prevalence of chronic respiratory disorders expand the addressable patient base, creating scalable testing volumes. Technological integration enhances accessibility and accuracy. Development of portable and handheld devices allows point-of-care testing and home monitoring, improving adherence and clinical decision-making. Healthcare infrastructure growth reinforces market expansion. Investments in diagnostic centers, primary care networks, and telehealth platforms enable widespread implementation, particularly in urban and semi-urban regions.

Market Introduction and Definition

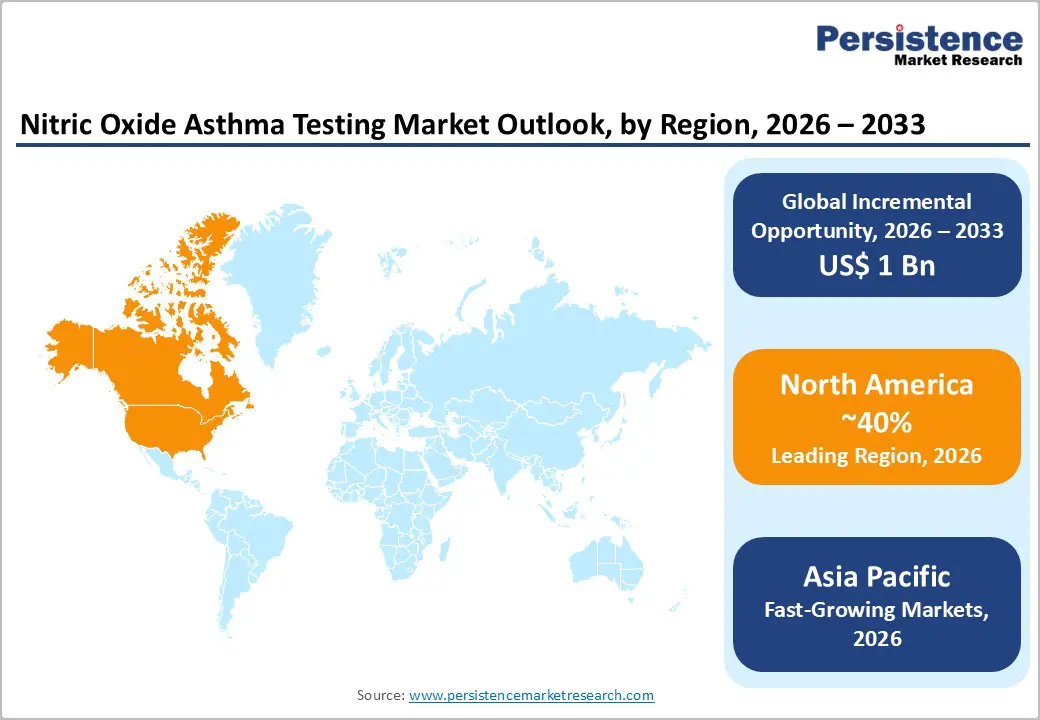

- Dominant Region: North America is projected to capture nearly 40% market share in 2026, driven by advanced hospital networks and clinician adoption.

- Fastest-growing Regional Market: Asia Pacific is forecasted to be the fastest-growing market between 2026 and 2033, fueled by diagnostic expansion and initiatives.

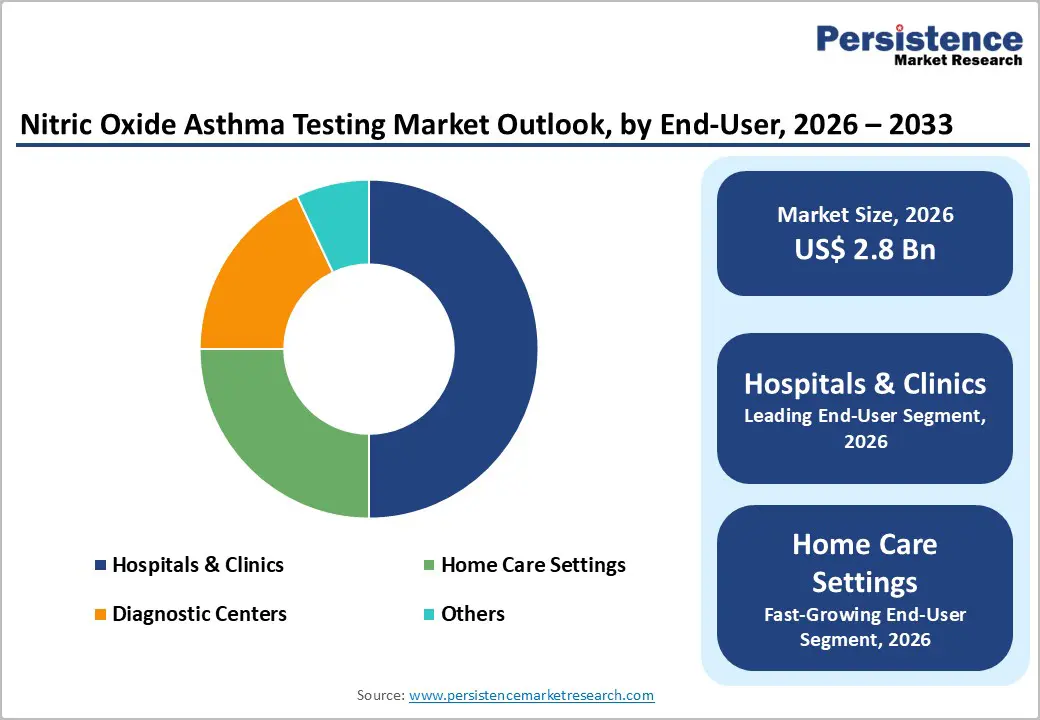

- Leading End-User: Hospitals and clinics are anticipated to command around 50% of the market in 2026, supported by clinical credibility and trained staff.

- Fastest-growing End-User: Home care is expected to be the fastest-growing segment from 2026 to 2033, fueled by portable devices and patient convenience.

| Key Insights | Details |

|---|---|

|

Nitric Oxide Asthma Testing Market Size (2026E) |

US$ 2.8 Bn |

|

Market Value Forecast (2033F) |

US$ 3.8 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.2% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Increasing Clinical Adoption of FeNO Testing

Healthcare systems increasingly adopt fractional exhaled nitric oxide measurement due to its ability to provide quantitative, non invasive assessment of airway inflammation that correlates with eosinophilic activity typical of many asthma phenotypes. Traditional diagnostic tools often rely on spirometry and clinical history, which identify airflow obstruction or symptoms but do not directly measure underlying inflammatory processes that drive disease progression and exacerbations. FeNO levels above clinical thresholds indicate elevated nitric oxide in exhaled breath, reflective of inflammatory signaling in the bronchial mucosa, aiding clinicians in distinguishing eosinophilic asthma from other respiratory disorders.

Public health agencies in the United States emphasize regular monitoring and proactive management of asthma, noting that over 25 million Americans live with the condition, with significant morbidity and healthcare utilization documented in 2025 analysis from the U.S. Centers for Disease Control and Prevention (CDC). The CDC highlights inflammatory biomarkers such as FeNO in research and surveillance contexts, reflecting governmental acknowledgement of its clinical relevance in assessing airway inflammation and potential to improve disease control and reduce exacerbation risks.

Demographic Shifts and Rising Chronic Respiratory Burden

Population aging alongside a sustained burden of chronic respiratory disease is a principal factor driving demand for advanced diagnostic approaches. A larger proportion of adults in many countries now falls into age brackets where chronic airways conditions such as asthma remain persistent or increase in prevalence, creating a steadily expanding user base for objective inflammatory assessments. Age associated vulnerability to airway inflammation combined with the direct and indirect costs of unmanaged chronic symptoms places emphasis on measurable biomarkers that can guide personalized patient management rather than reliance on episodic clinical judgment alone.

Environmental exposures, lifestyle trends and urbanization contribute to chronic airway irritation across demographic segments, reinforcing the need for tools that can help clinicians differentiate between inflammatory phenotypes and monitor treatment outcomes over time. Shifts in population structure mean that more individuals occupy age cohorts where respiratory conditions are likely to persist and interact with comorbidities, elevating clinical complexity. Persistent exposure to triggers such as air pollutants and allergens amplifies symptom frequency and severity across all ages, increasing clinical encounters and highlighting gaps in early detection methods.

Lack of Awareness to Inhibit Market Growth

Awareness regarding nitric oxide asthma testing remains limited among healthcare providers and patients, impacting adoption rates across key markets. Many clinicians continue relying on traditional diagnostic methods such as spirometry and symptom-based assessments, resulting in reduced familiarity with FeNO testing protocols and interpretation. Training programs for FeNO device usage are limited in scope, particularly in emerging regions, restricting knowledge dissemination. Patients exhibit minimal understanding of the test’s clinical significance, leading to lower demand and infrequent requests during routine asthma management. Marketing and educational efforts by device manufacturers often target specialized respiratory centers, leaving general practitioners and primary care facilities underinformed.

Complexity in interpreting test results further contributes to hesitancy among providers. FeNO values require context-specific evaluation, including patient history, medication use, and environmental factors. Limited access to standardized guidelines and reference ranges adds uncertainty to clinical decision-making. In regions with constrained healthcare resources, investments in staff training and infrastructure for advanced testing are deprioritized, reinforcing the knowledge gap. Research and development focus on device innovation has overshadowed educational outreach, delaying integration into standard care pathways.

Limited Reimbursement Coverage to Create Hurdles

Insurance providers often restrict coverage for nitric oxide asthma testing due to high device costs and variability in clinical adoption. Reimbursement policies typically favor well-established diagnostic procedures with long-term outcome data. Nitric oxide testing, despite clinical validation, remains relatively new compared to traditional spirometry or peak flow assessments. Payers assess cost-effectiveness and long-term economic impact before expanding coverage. Variations in regional healthcare policies and budget constraints in public health systems further influence reimbursement decisions. As a result, healthcare facilities may face financial barriers to integrating these testing solutions into routine care pathways, limiting accessibility for patients across diverse demographics.

Clinical guidelines and real-world adoption trends also shape reimbursement patterns. Evidence supporting nitric oxide testing demonstrates utility in monitoring airway inflammation and guiding asthma therapy, yet standardized protocols differ across regions and institutions. Discrepancies in test frequency, interpretation, and clinical outcome correlation create uncertainty for insurers. Coverage decisions often require rigorous documentation and justification, leading to administrative burdens for providers. Payer hesitation reduces incentives for clinics to invest in specialized analyzers or train personnel.

Home Monitoring and Telehealth Integration

The rising trend in remote clinical engagement among asthma patients signals a shift in care delivery, with 47.7% of adults with asthma reporting telemedicine use in 2021–2022 according to U.S. government health data. Virtual care channels enable continuous oversight of respiratory symptoms and relevant biomarkers, supporting proactive intervention outside traditional clinical settings. Monitoring tools that record physiological data from patient homes extend the reach of clinicians into patients’ daily environments, improving visibility into condition variability and enabling early adjustments in treatment plans, reducing reliance on episodic, in person visits.

Integration of digital platforms with remote monitoring addresses structural inefficiencies in chronic respiratory care by capturing objective health information and facilitating clinician patient communication without geographic constraints. Government health agencies emphasize the importance of educational and self management support, which is amplified when paired with telecommunication technologies, empowering patients to adhere to care protocols and report trends in real time. Telehealth’s capacity to aggregate longitudinal data supports personalized treatment strategies and may reduce emergency healthcare utilization by enabling timely clinical decisions informed by continuous monitoring, aligning with public health goals of improved chronic disease control.

Innovation in Portable and Affordable Devices

Wider adoption of point of care, compact nitric oxide breath measurement platforms is emerging as a strategic growth vector aligned with broader shifts in respiratory care delivery. A significant portion of the asthma burden remains in community and outpatient settings where traditional laboratory based diagnostics are less accessible, and routine monitoring is constrained by clinic capacity. In the United States in 2024, an estimated 8.6% of adults and 6.5% of children report current asthma, a sizeable population requiring frequent clinical assessment and management adjustments. Portable analyzers that deliver rapid inflammatory biomarker data at the initial point of contact empower clinicians to make timely, evidence based decisions on treatment initiation and modification.

Cost pressures within healthcare systems underscore the importance of more efficient diagnostic pathways. Traditional spirometry and advanced pulmonary tests often necessitate referrals, scheduling delays, and specialized technicians, which can defer therapeutic adjustments and contribute to suboptimal disease control. In contrast, inexpensive, handheld nitric oxide measurement solutions shorten the diagnostic loop, supporting longitudinal monitoring in both clinic and home environments. Enhanced device affordability can drive broader reimbursement support from payers and public health programs, particularly where non invasive testing aligns with preventive care initiatives and quality metrics tied to reduced exacerbations and hospital utilization.

Category-wise Analysis

Product Type Insights

Nitric oxide testing standalone monitor is anticipated to secure around 45% of the nitric oxide asthma testing market revenue share in 2026, reflecting its established clinical credibility and widespread adoption in hospitals and diagnostic centers. Standalone monitors provide precise measurement of FeNO, enabling clinicians to monitor airway inflammation accurately and guide anti-inflammatory therapy. Providers prefer standalone devices for their reliability, reproducibility, and compliance with international clinical guidelines.

The segment benefits from high clinical acceptance, particularly in tertiary care settings where diagnostic accuracy is critical. Its accessibility for repeated measurements and integration into established workflows makes it the default choice in structured care environments.

Nitric oxide testing handheld monitor is expected to be the fastest-growing segment during the 2026–2033 forecast period, propelled by increasing demand for portable, point-of-care, and home-based testing solutions. Handheld monitors allow real-time measurement of FeNO outside traditional clinical settings, enhancing convenience for patients and clinicians. The growth is supported by technological innovation in miniaturized sensors, wireless connectivity, and user-friendly interfaces that facilitate adoption in home care, remote clinics, and emergency settings. Providers increasingly integrate handheld devices into asthma management plans for continuous monitoring and rapid assessment of treatment response.

End-User Insights

Hospitals and clinics are likely to be the leading segment with a projected 50% of the nitric oxide asthma testing market share in 2026 due to the segment’s high clinical credibility, provider trust, and capacity to integrate diagnostic workflows. Hospitals and specialty clinics possess trained personnel, standardized infrastructure, and regulatory compliance frameworks, facilitating adoption of FeNO testing devices. Provider referrals from primary care to hospital-based diagnostic units reinforce centralized testing practices, ensuring consistent usage. Established reimbursement mechanisms and capital investment capacity further support procurement of standalone and advanced devices.

Home care settings are anticipated to be the fastest-growing segment from 2026 to 2033, fueled by rising patient preference for convenient, technology-enabled monitoring and increasing adoption of portable handheld devices. Integration with telehealth services allows remote clinician oversight, supporting personalized asthma management while reducing hospital visits. Digital tracking, automated reporting, and patient adherence monitoring increase clinical value, encouraging providers to recommend home-based FeNO testing. Cost-efficiency, accessibility, and patient-centric care models further drive segment expansion.

Regional Insights

North America Nitric Oxide Asthma Testing Market Trends

North America is forecast to lead with an estimated 40% of the nitric oxide asthma testing market value in 2026, supported by deep clinical integration of non invasive airway inflammation assessment in routine respiratory care across the United States and Canada. A high concentration of specialty care facilities and advanced hospital networks prioritizes implementation of diagnostic platforms that accelerate decision making and optimize treatment pathways.

Public and private payers in these countries have established structured reimbursement categories for biomarker based testing, making investments in these systems financially viable for large healthcare networks and outpatient clinics. Extensive clinician familiarity with nitric oxide quantification tools and established practice protocols reinforce preference for these diagnostic modalities over conventional assessments that necessitate additional interpretive effort or specialist intervention.

A robust regulatory and innovation ecosystem drives continual product enhancements that resonate with care delivery needs. Regulatory agencies in the United States and Canada maintain clear pathways for market entry of next generation analyzers, facilitating an environment where iterative improvements in accuracy, connectivity, and workflow integration are rapidly adopted. Concentrated headquarters and R&D centers for multiple key manufacturers in these countries enable rapid iteration and alignment of device features with provider requirements, reducing friction in procurement decisions.

Europe Nitric Oxide Asthma Testing Market Trends

Europe is experiencing steady growth in nitric oxide asthma testing driven by a combination of advanced healthcare infrastructure and widespread integration of guideline-based respiratory management. High adoption rates among tertiary hospitals and specialized pulmonary clinics are supported by established reimbursement frameworks that recognize biomarker-based diagnostics as part of standard asthma care. In Germany and France, large-scale chronic disease programs promote routine inflammatory assessment, enabling earlier intervention and more precise therapy adjustments. In the United Kingdom, healthcare authorities emphasize preventive care metrics, leading to incorporation of breath-based inflammation monitoring in both hospital and primary care settings.

Innovation and policy alignment further underpin market performance. Investment in connected diagnostic systems facilitates integration with electronic health records, allowing longitudinal tracking of airway inflammation and supporting data-driven therapeutic decisions. Manufacturers are introducing devices with reduced operational complexity, targeting broad clinical adoption across diverse hospital networks and specialist centers. Public and private payers increasingly support evidence-based protocols that link testing outcomes to optimized treatment plans, reinforcing adoption among providers focused on outcome-based care.

Asia Pacific Nitric Oxide Asthma Testing Market Trends

Asia Pacific is anticipated to be the fastest growing market for nitric oxide asthma testing during the 2026-2033 forecast period, stimulated by expanding access to diagnostic infrastructure and increasing prioritization of respiratory disease management within public health agendas. Rapid enhancement of primary care facilities is enabling broader deployment of point of care inflammatory assessment tools outside major metropolitan centers. In 2026, healthcare investment in China is accelerating capacity building in tier 2 and tier 3 cities, driving demand for efficient, non invasive diagnostics that can relieve pressure on overloaded specialist clinics.

In India, government led screening initiatives aimed at early detection of chronic respiratory conditions are generating higher utilization rates for biomarker based assessment platforms, supporting wider penetration in both urban and rural health networks.

Growth dynamics are further strengthened by commercial and policy forces that align diagnostic innovation with broader system goals to improve care efficiency and reduce long term treatment costs. Manufacturers are introducing scalable solutions that fit heterogeneous clinical environments, from high volume hospital programs to community health outreach services, minimizing barriers to adoption related to space, training, and capital investment. Collaborative frameworks between device developers and health care payers in the region are beginning to explore outcome linked reimbursement models that reward objective disease control measures, positioning accelerated uptake of nitric oxide measurement platforms as part of performance oriented care contracts.

Competitive Landscape

The global nitric oxide asthma testing market features a moderately consolidated structure, where a limited number of global manufacturers capture significant market share while regional and specialized firms operate within niche segments. Key players such as NIOX Group plc, ECO MEDICS AG, Bedfont® Scientific Ltd., and Fortis Healthcare collectively drive innovation and establish clinical benchmarks for airway inflammation assessment. Market dominance is reinforced through continuous development of advanced diagnostic platforms, regulatory clearances, and integration of devices into standard respiratory care pathways. These organizations maintain strong relationships with hospitals, outpatient clinics, and specialty care centers, ensuring broad adoption and sustained utilization of testing systems.

Strategic initiatives by leading manufacturers shape overall market dynamics by emphasizing product innovation and service quality. Investment in portable, user-friendly analyzers supports adoption across diverse clinical settings, while compliance with regulatory standards accelerates market entry for new devices. Collaborative engagements with healthcare providers enable validation studies, reinforcing confidence in test reliability and clinical utility. Fragmented regional participants leverage specialized applications to address specific gaps in patient monitoring and diagnostic coverage, complementing the broader market ecosystem.

Key Industry Developments

- In February 2026, MGC Diagnostics launched the Fenom Flo™ FeNO monitoring system in the United States, introducing a portable, handheld nitric oxide breath analyzer that delivers rapid fractional exhaled nitric oxide results with a shorter 6 second breath test to support broader point of care respiratory assessment.

- In November 2025, Bedfont® Scientific Ltd. formed a strategic partnership with Aerosol Medical Systems to register and introduce the NObreath® FeNO testing device in Mexico, expanding access to non invasive airway inflammation diagnostics for improved asthma care.

- In November 2025, Bedfont® Scientific Ltd. partnered with Rbeck Healthtech Private to register and distribute the NObreath® FeNO device in India, significantly expanding access to fractional exhaled nitric oxide testing to support earlier and more precise asthma diagnosis and management.

Companies Covered in Nitric Oxide Asthma Testing Market

- NIOX Group plc.

- ECO MEDICS AG

- Bedfont® Scientific Ltd.

- Fortis Healthcare.

- Bosch Healthcare Solutions GmbH

- Sunvou EU

- CAIRE Inc.

Frequently Asked Questions

The global nitric oxide asthma testing market is projected to reach US$ 2.8 billion in 2026.

Rising asthma prevalence, demand for non‑invasive diagnostics, and adoption of point‑of‑care inflammatory monitoring are driving the market.

The market is poised to witness a CAGR of 4.4% from 2026 to 2033.

Expansion into emerging healthcare markets, home monitoring solutions, and integration with telehealth platforms represent key market opportunities.

Some of the key market players include NIOX Group plc, ECO MEDICS AG, Bedfont® Scientific Ltd., Fortis Healthcare, and Bosch Healthcare Solutions GmbH.