- Bulk Chemicals

- Australia Nitric Acid Market

Australia Nitric Acid Market Size, Share, and Growth Forecast, 2025 - 2032

Australia Nitric Acid Market By Product Type (Fuming, Non-fuming), Grade (Commercial, Specialty), Application (Explosives, Fertilizers), and State Analysis for 2025 - 2032

Australia Nitric Acid Market Size and Trends Analysis

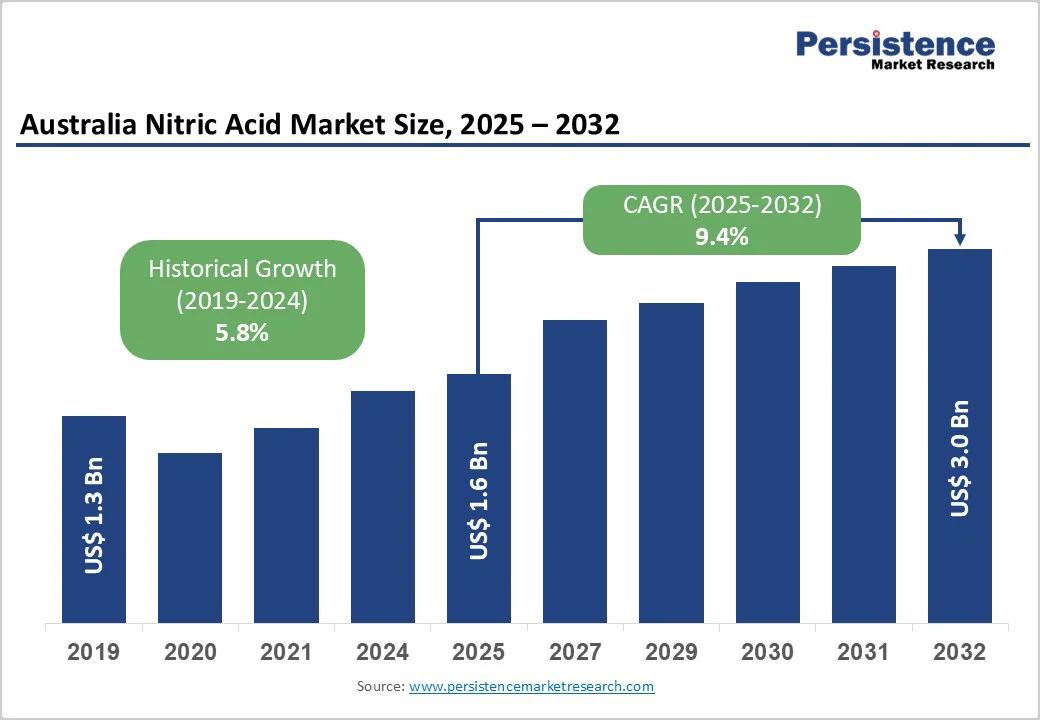

The Australia nitric acid market size is likely to be valued at US$1.6 Billion in 2025 and is estimated to reach US$3.0 Billion in 2032, growing at a CAGR of 9.4% during the forecast period 2025-2032, driven by the country's superior mining base, especially in Western Australia and Queensland. They rely heavily on nitric acid for processing minerals such as gold, copper, and nickel.

Key Industry Highlights

- Government Initiative: The Australian Government introduced new funding incentives under its Industrial Transformation Stream, encouraging chemical manufacturers, including nitric acid producers, to adopt low-emission technologies and expand domestic production capabilities.

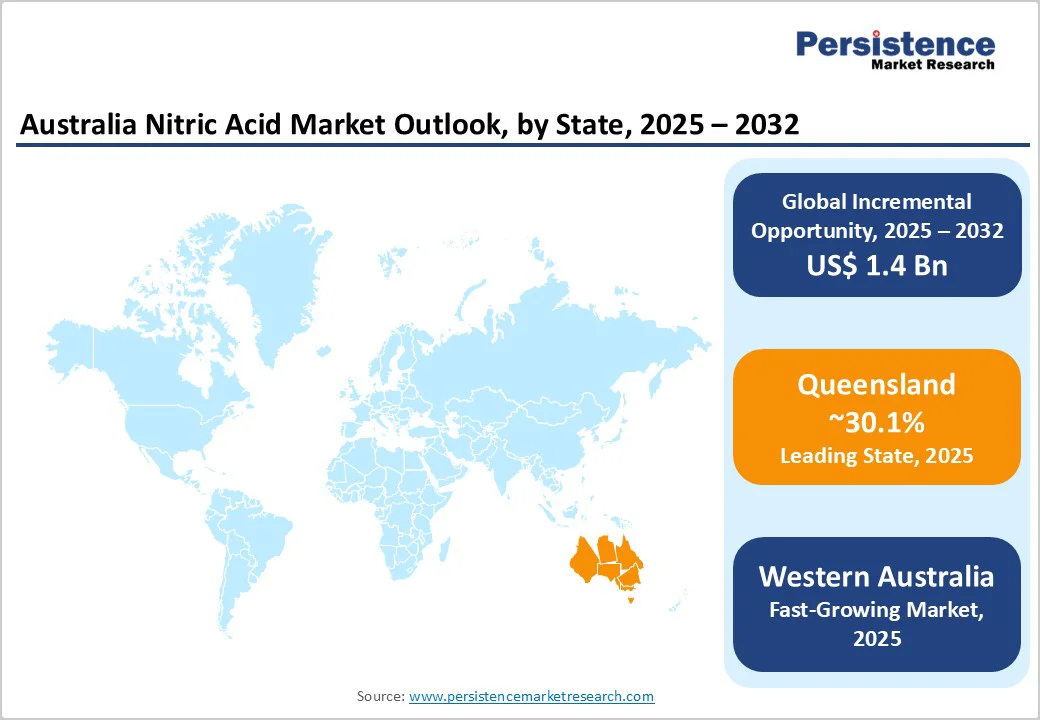

- Leading State: Queensland, approximately 30.1% of the share in 2025, owing to the presence of major mining operations and chemical manufacturing hubs.

- Fastest-growing State: Western Australia, due to expanding gold, nickel, and lithium mining activities.

- Leading Product Type: Non-fuming nitric acid holds nearly 65.4% share in 2025, as it is easier and safer to handle compared to the fuming variant, making it suitable for bulk industrial use.

- Dominant Grade: Commercial grade, approximately 71.9% of the Australia nitric acid market share in 2025, since it provides the right balance of purity and cost-efficiency for large-scale applications.

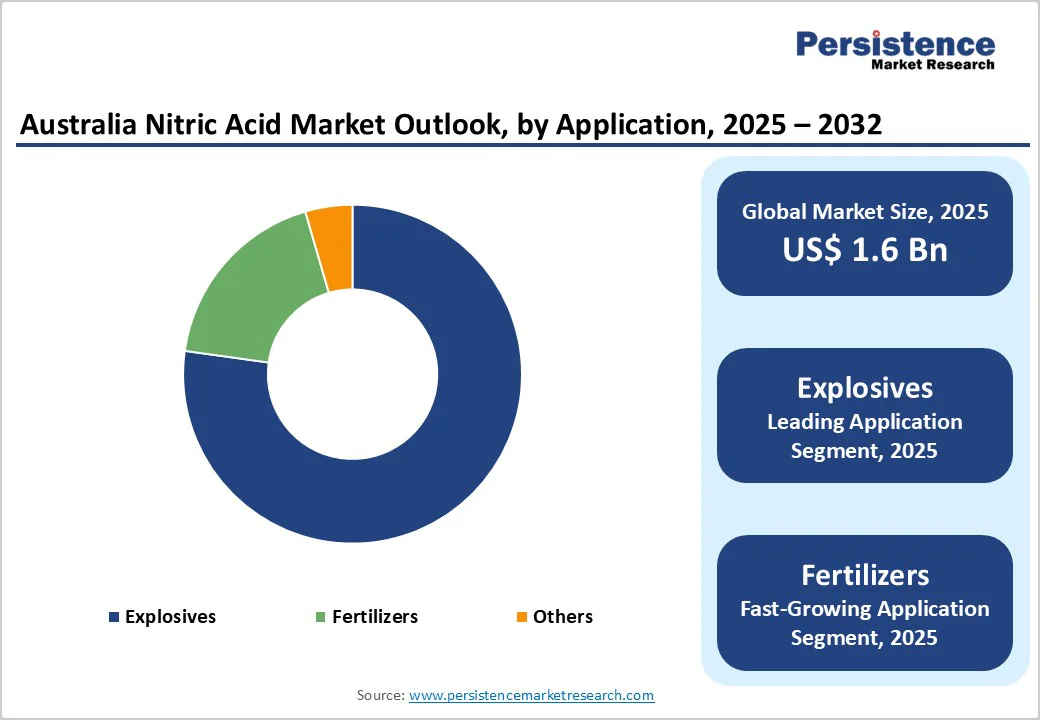

- Key Application: Explosives recorded about 77.2% share in 2025, as nitric acid is a key ingredient in the production of ammonium nitrate, the base for industrial explosives used in mining and quarrying.

| Key Insights | Details |

|---|---|

|

Australia Nitric Acid Market Size (2025E) |

US$1.6 Bn |

|

Market Value Forecast (2032F) |

US$3.0 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

9.4% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Rising Dependence on Nitrogen-enriched Fertilizers in Agriculture

Australia’s agricultural sector continues to rely heavily on nitrogen-based fertilizers such as ammonium nitrate and calcium ammonium nitrate to maintain soil productivity and crop yields, especially in regions with nutrient-depleted soils. With climate variability and rising export demand for wheat, barley, and canola, farmers are increasingly turning to nitrogen-rich inputs to sustain consistent output.

The ongoing development of controlled-release and environmentally safe fertilizer variants has further boosted nitric acid consumption as a key precursor. This is reinforcing its position in the country’s agrochemical supply chain.

Expanding Use in Advanced Industrial Materials

Nitric acid plays a key role in the production of specialty chemicals used to manufacture high-performance materials, including polyurethane foams, protective coatings, and synthetic fibers. The rising construction and automotive activities across Australia are pushing demand for durable foams and coatings that rely on nitric-acid-derived intermediates.

The continued focus on lightweight synthetic fibers for industrial textiles and insulation materials is strengthening industrial use. This links nitric acid to the country’s broader manufacturing and infrastructure growth.

Barrier Analysis - Environmental Impact and Regulatory Pressures

Nitric acid’s contribution to nitrogen oxide emissions makes it a key environmental concern in Australia, where strict sustainability standards are being enforced under national climate targets. The release of nitrogen oxides during production can lead to acid deposition, affecting ecosystems such as the Murray-Darling Basin, one of Australia’s most sensitive agricultural regions.

To comply with environmental policies, producers such as Orica and CSBP have had to invest heavily in nitrous oxide abatement systems. It further increases operational costs and limits small-scale firms' entry into the market.

High Reactivity and Handling Risks

Nitric acid’s highly corrosive and reactive nature poses serious safety challenges during storage, transport, and industrial use. It can react violently with metals and organic substances, creating fire and explosion hazards.

Recent safety regulations have tightened handling standards, especially for plants and distributors near populated or mining areas. These restrictions raise compliance costs and complicate logistics, discouraging new investments in large-scale nitric acid facilities across Australia.

Opportunity Analysis - Surging Use of Nitric Acid in Metal Extraction and Processing

Australia’s expanding mining sector continues to create new opportunities for nitric acid, especially in gold, copper, and rare earth processing. The chemical is extensively used in hydrometallurgical refining and leaching operations due to its efficiency in dissolving base and precious metals.

In Western Australia and Queensland, ongoing projects such as BHP’s nickel expansion and Northern Star’s gold operations have boosted demand for high-purity nitric acid. As the country accelerates exploration for essential minerals required in electric vehicles and renewable energy technologies, the use of nitric acid in metal recovery is anticipated to rise steadily.

Capacity Expansion and Green Production Initiatives

Australia’s leading nitric acid producers are actively expanding production capacity while integrating clean technologies to reduce emissions and energy consumption. CSBP’s low-emission nitric acid and ammonium nitrate projects in Kwinana illustrate the industry’s move toward sustainable operations. These projects not only improve environmental performance but also refine production efficiency and supply reliability for domestic users.

The push to develop green ammonia and hydrogen-based feedstocks provides long-term potential for producing low-carbon nitric acid, creating export opportunities to the Asia Pacific’s markets seeking sustainable industrial chemicals. This combination of expansion and decarbonization investments positions Australia as a future-ready producer in the global nitric acid value chain.

Category-wise Analysis

Product Type Insights

Non-fuming nitric acid is anticipated to hold approximately 65.4% of the share in 2025, as it provides a stable and safer handling profile compared to its fuming variant. Its low volatility minimizes the risk of toxic gas emissions, making it suitable for continuous industrial operations in fertilizers, dyes, and chemical manufacturing. In Australia, where stringent workplace safety laws are enforced under Safe Work Australia guidelines, industries rely more on non-fuming nitric acid to reduce occupational hazards and storage risks during large-scale processing.

Fuming nitric acid is gaining momentum due to its critical use in aerospace propellants, defense-grade explosives, and semiconductor etching. Its superior oxidizing ability makes it valuable for advanced manufacturing where high-purity reactions are essential. Increasing investments in Australia’s defense modernization programs, such as missile and propulsion research under the AUKUS alliance, have indirectly boosted local demand for fuming nitric acid in specialized chemical applications.

Grade Insights

Commercial grade is poised to capture about 71.9% of the share in 2025, as it meets the quality requirements of bulk consumers such as fertilizer and explosives manufacturers without the high costs associated with premium grades. It strikes a balance between purity and cost-effectiveness, supporting mass-scale operations at sites such as Orica’s Kooragang Island and CSBP’s Kwinana complex. Its wide compatibility with existing production systems further strengthens its dominance in the domestic market.

Specialty-grade nitric acid is in high demand from industries such as electronics, pharmaceuticals, and advanced materials, which require high-purity levels for precision reactions. The rise of semiconductor assembly and lab chemical usage across Australia’s technology and research sectors supports this niche growth. Although produced in small volumes, the segment benefits from increasing research and development activities in nanomaterials and clean energy storage technologies that depend on ultra-pure chemical inputs.

Application Insights

Explosives are projected to account for nearly 77.2% of the share in 2025, due to Australia’s vast mining sector. Nitric acid is essential for producing ammonium nitrate, the primary component in mining explosives used across the Pilbara, Bowen Basin, and Goldfields regions. Companies such as Dyno Nobel and Orica rely on large-scale nitric acid supply for blasting agents critical to the extraction of iron ore, coal, and gold. The steady expansion of mining and infrastructure projects ensures explosives remain the top nitric acid application.

Fertilizers are a major outlet for nitric acid as it serves as a precursor for ammonium nitrate and calcium ammonium nitrate, both of which are important for improving soil nitrogen content. Australia’s dependence on nutrient-enriched fertilizers to maintain yields in arid and semi-arid regions keeps demand stable. With the agricultural industry focused on sustainable farming and precision nutrient management, the use of nitric-acid-based fertilizers continues to rise, particularly in grain-producing regions such as Western Australia and New South Wales.

State Insights

Queensland Nitric Acid Market Trends

In 2025, Queensland is predicted to account for approximately 30.1% of the share, owing to increased production in Orica’s Yarwun plant near Gladstone and Dyno Nobel’s Moranbah facility. Both plants primarily serve the mining and explosives sectors. The Moranbah site, which integrates ammonia, nitric acid, and ammonium nitrate production, plays a key role in supplying explosives to the Bowen Basin coal mines.

The state’s nitric acid supply landscape has been uncertain due to Incitec Pivot’s recent restructuring and the potential closure or sale of its Phosphate Hill fertilizer plant, which relies on nitric acid derivatives. This development has raised concerns about long-term feedstock stability for agricultural and industrial users in northern Queensland.

Western Australia Nitric Acid Market Trends

In Western Australia, the market is dominated by CSBP’s Kwinana operations, which serve both fertilizer and explosives markets across the Pilbara mining belt. The company has recently implemented nitrous oxide abatement projects, claiming up to 98% reduction in greenhouse gas emissions from its nitric acid and ammonium nitrate plants.

Backed by government funding and decarbonization grants, these upgrades position Kwinana as one of the most sustainable nitric acid production hubs in Asia Pacific. The facility is also exploring green hydrogen integration to produce low-carbon ammonia and nitric acid, signaling a shift toward clean industrial chemistry in Western Australia.

New South Wales Nitric Acid Market Trends

In New South Wales, Orica’s Kooragang Island complex in Newcastle is the central nitric acid production site, operating multiple plants that support both domestic and export requirements. The facility has undergone significant upgrades, including a US$37 million tertiary abatement system that cuts nitrous oxide emissions by up to 95%, making it one of the most environmentally advanced nitric acid operations globally.

The site supplies key mining and construction clients while also supporting Orica’s move toward clean manufacturing. These investments have not only strengthened the reliability of New South Wales’s nitric acid supply but have also set a benchmark for sustainable industrial production in Australia.

Competitive Landscape

The Australia nitric acid market is dominated by a handful of large domestic producers such as Orica, CSBP, and Dyno Nobel (formerly Incitec Pivot Limited). These three companies control most of the country’s nitric acid production, primarily catering to the mining and fertilizer sectors. Beyond the domestic producers, global nitrogen majors, traders, and chemical distributors act as price-makers for non-explosive industrial grades and as contingency suppliers. But they rarely compete head-to-head on spot explosives-grade volumes because of the safety or regulatory limits and transport costs tied to nitric acid.

Key Industry Developments

- In April 2025, Wesfarmers Chemicals, Energy & Fertilizers (WesCEF) announced the successful commissioning of advanced abatement technology at its Kwinana nitric acid facility in Western Australia. Supported by the Australian Government’s Powering the Regions Fund, this installation aims to reduce nitrous oxide emissions by up to 98%.

- In September 2024, Dyno Nobel, a subsidiary of Incitec Pivot Limited, revealed plans to restructure its fertilizer and explosives operations in Queensland. This included evaluating the future of the Phosphate Hill facility, which supplies ammonia for nitric acid production.

Companies Covered in Australia Nitric Acid Market

- Orica Limited

- Dyno Nobel

- CSBP

- Yara International

- BASF

- Nutrien

- Univar Solutions

- CF Industries

Frequently Asked Questions

The Australia nitric acid market is projected to reach US$1.6 Billion in 2025.

Rising mining activities in Australia and the adoption of sustainable fertilizer production methods are the key market drivers.

The Australia nitric acid market is poised to witness a CAGR of 9.4% from 2025 to 2032.

Development of low-emission nitric acid plants supported by governments and strategic capacity expansions by key players are the key market opportunities.

Orica Limited, Dyno Nobel, and CSBP are a few key market players.