- Metals & Minerals

- Nickel Cobalt Manganese (NCM) Market

Nickel Cobalt Manganese (NCM) Market Size, Share, and Growth Forecast, 2026 - 2033

Nickel Cobalt Manganese (NCM) Market by Product Type (NCM 523, NCM 811, NCM 532, NCM 111), Application (Battery, Energy Storage System, Automotive, Consumer Electronics), End-User (Automotive, Electric, Energy), and Regional Analysis for 2026-2033

Nickel Cobalt Manganese (NCM) Market Share and Trends Analysis

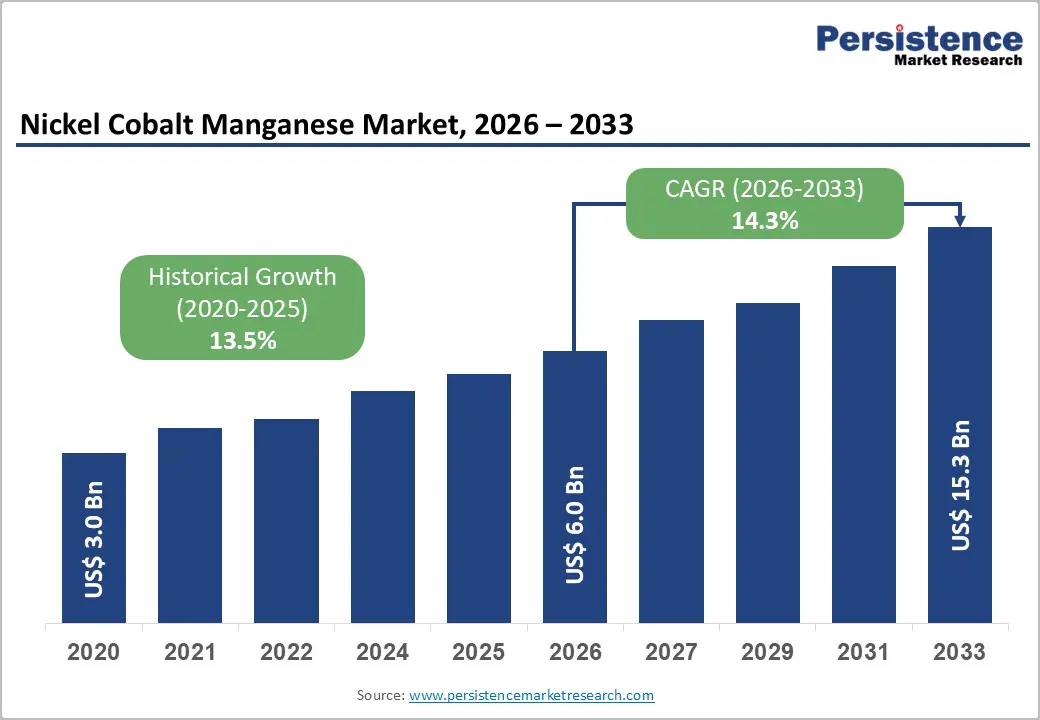

The global nickel cobalt manganese (NCM) market size is likely to be valued at US$ 6.0 billion in 2026, and is projected to reach US$ 15.3 billion by 2033, growing at a CAGR of 14.3% during the forecast period 2026−2033.

This accelerated growth is driven by the increasing deployment of energy storage systems that support grid stabilization and large-scale renewable energy integration. As power systems increasingly incorporate variable-generation sources, demand is increasing for high-performance battery chemistries that deliver energy density, safety, and cycle stability at scale. Market expansion is further supported by government mandates targeting carbon emission reduction across major economies, which are reinforcing long-term investment in electric mobility and stationary storage infrastructure.

Supply chain localization initiatives are gaining momentum as manufacturers seek to reduce geopolitical risk and enhance material security, while ongoing technological advancements are improving cathode efficiency and material utilization. These developments are enhancing performance-to-cost ratios and supporting wider commercial adoption, enabling market growth through policy alignment, infrastructure investment, and continued innovation across battery manufacturing value chains.

Key Industry Highlights

- Product Type Leadership: NCM 523 is slated to lead with about 42% revenue share in 2026, and NCM 811 is likely to be the fastest-growing segment during the 2026-2033 forecast period.

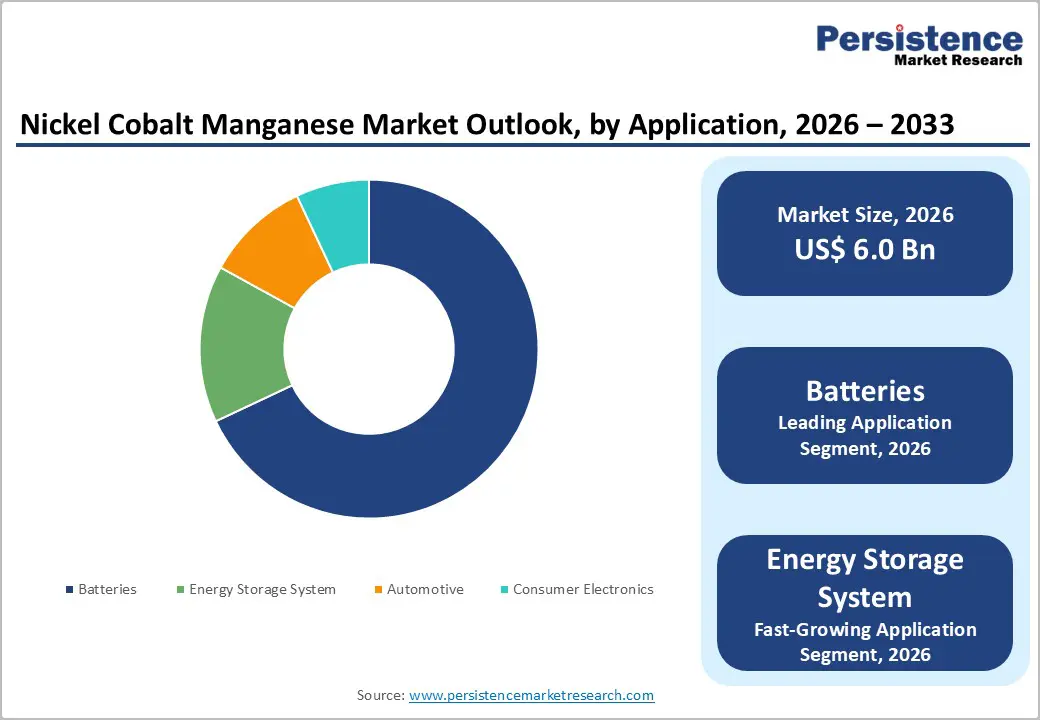

- Application Dominance: Batteries are projected to account for 68% of revenue in 2026, while energy storage systems are expected to be the fastest-growing segment through 2033.

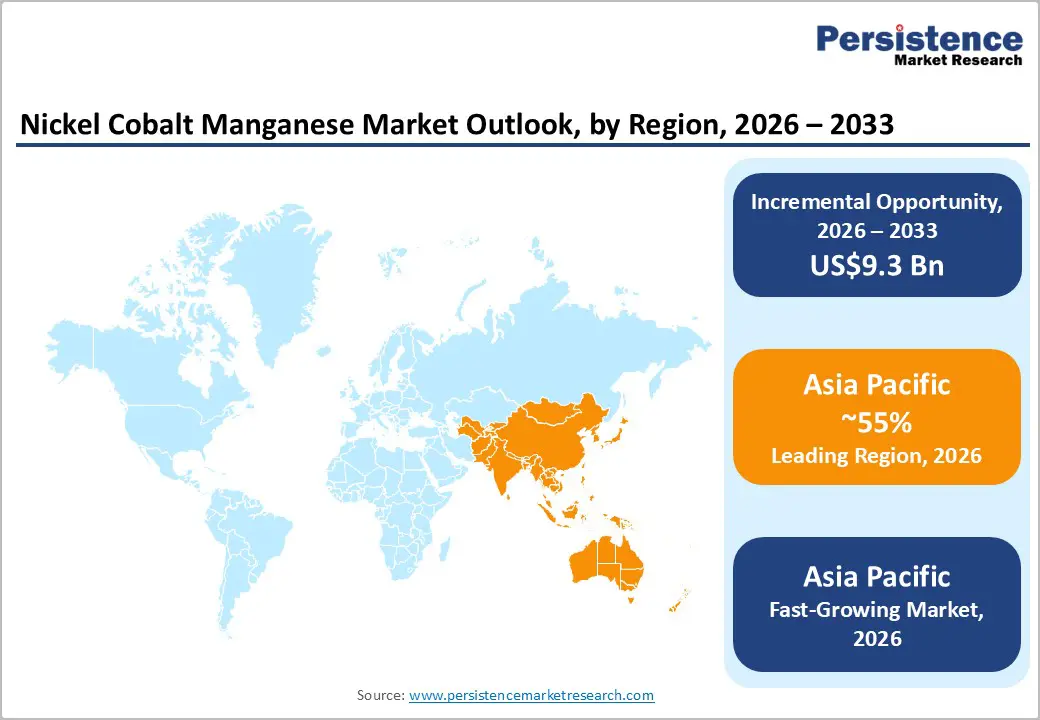

- Regional Dynamics: Asia Pacific is forecast to be the leading and fastest-growing market for nickel, cobalt, and manganese in 2026, driven by China’s dominance in battery manufacturing.

- Key Driver: Rapid advances in electric vehicle (EV) battery technologies are the primary driver of demand for NCM cathode materials.

- Key Opportunity: Governments worldwide are setting ambitious EV deployment targets to reduce carbon emissions, creating significant opportunities for market players.

| Key Insights | Details |

|---|---|

| Nickel Cobalt Manganese (NCM) Market Size (2026E) | US$ 6.0 Bn |

| Market Value Forecast (2033F) | US$ 15.3 Bn |

| Projected Growth (CAGR 2026 to 2033) | 14.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 13.5% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Expansion of Global Manufacturing Infrastructure and Industrial Automation

The global EV market is the primary driver of demand for NCM cathode materials, as battery-powered mobility continues to scale across major economies. Leading automotive manufacturers such as Tesla, Volkswagen Group, and General Motors are expanding EV production while investing directly in battery manufacturing capacity. Policy frameworks reinforce this trajectory, as governments link regulatory compliance to electrification outcomes. In the United States, the Inflation Reduction Act (IRA) provides tax incentives for qualifying electric vehicles, while the European Union enforces Corporate Average Fuel Economy (CAFE) standards to reduce carbon dioxide emissions.

China is advancing its New Energy Vehicle (NEV) mandate to strengthen domestic electric-vehicle output and upstream cathode-material supply. Together, these measures are creating predictable and sustained demand for NCM-based batteries in automotive applications. Declining battery costs are further accelerating EV adoption by improving affordability and expanding addressable consumer segments. Manufacturers are responding by scaling production volumes, thereby increasing the preference for NCM chemistries due to their balanced profile of energy density, thermal stability, and cost efficiency.

From a strategic standpoint, industry leaders should prioritize long-term supply agreements with reliable cathode material producers to mitigate supply risk. Investment in localized manufacturing is also becoming essential to navigate region-specific regulatory requirements and incentive structures. Companies that are integrating battery recycling capabilities early are positioning themselves to benefit from future compliance mandates, secondary material recovery, and lower input costs.

Competition from Alternative Battery Chemistries

Lithium iron phosphate (LFP) chemistry is intensifying competitive pressure on nickel-cobalt-manganese cathode materials, particularly in entry-level and mid-range electric vehicle segments. Automakers are increasingly favoring LFP batteries due to lower material costs and stronger intrinsic safety characteristics, which align well with cost-sensitive markets, especially in China. Manufacturers are actively optimizing LFP formulations to enhance energy density while preserving thermal stability and safety advantages.

This shift is exerting margin pressure on NCM producers, as automotive original equipment manufacturers are reallocating procurement toward more cost-competitive chemistries. Despite these performance gains, nickel-rich NCM chemistries are presenting thermal stability challenges that require more sophisticated safety and battery management systems. Additional monitoring, cooling, and protection measures are increasing battery pack integration costs, which is narrowing cost competitiveness outside premium segments.

At the same time, sodium-ion battery technology is emerging as a longer-term competitive threat, particularly for stationary energy storage applications, where energy-density constraints are less critical. Government-funded research programs and rising corporate investment are accelerating the commercialization timelines for sodium-ion technologies. Strategic partnerships with LFP suppliers can enhance supply chain resilience, while continued investment in thermal management innovation can help sustain market leadership in premium EV applications.

Global Shift towards Sustainable Energy Solutions

Governments worldwide are implementing ambitious EV adoption targets to reduce carbon emissions and accelerate the transition away from internal combustion engines. National policy frameworks are mandating structural shifts toward battery-powered mobility, while incentives such as purchase subsidies, tax exemptions, and preferential financing are accelerating consumer uptake. Infrastructure expansion is reinforcing this momentum, as charging networks are scaling rapidly across urban centers and highway corridors.

At the same time, technological progress is improving battery performance, driving range, and charging speed, which is addressing earlier adoption barriers. Consumer awareness initiatives are also strengthening market confidence by highlighting the total cost of ownership benefits, environmental advantages, and technology maturity. Renewable energy integration is presenting an equally strong growth pathway for NCM deployment beyond transportation applications. Solar photovoltaic and onshore wind installations are achieving record capacity additions each year, increasing variability within national power systems.

Grid operators are therefore increasingly relying on energy storage systems to maintain reliability and provide frequency regulation services. NCM-based batteries offer a balanced combination of cycle life, discharge capability, and thermal performance that is well suited to multi-hour storage requirements. Utility-scale projects are prioritizing proven chemistries capable of sustaining thousands of charge and discharge cycles while preserving capacity over time. As renewable penetration deepens, NCM batteries are set to play a critical role in supporting grid stability and long-term energy system resilience.

Category-wise Analysis

Product Insights

NCM 523 is poised to be the leading segment, accounting for approximately 42% of nickel cobalt manganese market revenue in 2026. This formulation, containing equal proportions of nickel, cobalt, and manganese (5:2:3 ratio), delivers optimal trade-offs between energy density (180-200 Wh/kg), thermal stability, and production cost efficiency, making it the preferred choice for mainstream electric vehicle applications and residential energy storage systems.

Major battery manufacturers, including CATL, LG Energy Solution, and Samsung SDI, maintain extensive NCM 523 production capacity, supported by established supply chains and qualified automotive customer relationships, which together sustain their continued market leadership.

NCM 811 is likely to be the fastest-growing segment over the 2026-2033 forecast period, driven by automotive manufacturers' increasing focus on extended vehicle range and lower battery pack costs. NCM811 cathode materials deliver superior energy density due to elevated nickel content. Electric vehicle manufacturers favor this chemistry for extended driving ranges and premium performance applications.

Reducing cobalt content addresses ethical sourcing concerns and supply chain concentration risks associated with mining operations. Material cost structures improve as manufacturers substitute expensive cobalt with more abundant nickel resources.

Application Insights

Batteries are projected to dominate, accounting for approximately 68% of NCM market revenue in 2026. EV manufacturers and energy storage developers are prioritizing NCM cathode materials due to their consistent performance across a wide range of power and endurance requirements. High energy density supports longer driving ranges while enabling compact battery pack designs, which is critical for automotive efficiency and space optimization.

Stable charge and discharge cycling also ensures long-term reliability in demanding industrial environments. NCM chemistry is therefore performing effectively across multiple end-use applications, including consumer electronics that require compact formats and fast charging, electric vehicles that demand high-capacity and safety-compliant solutions, and industrial equipment used for material handling and backup power systems.

Energy storage systems are forecast to be the fastest-growing application area from 2026 to 2033, driven by accelerating investments in solar and wind power generation. As renewable penetration increases, utilities and grid operators are facing greater intermittency challenges, making efficient and durable storage solutions essential for maintaining supply stability. Nickel-cobalt-manganese batteries offer a veritable combination of high energy density and long operational life, which is enabling reliable multi-hour storage performance.

This capability is supporting consistent power delivery and grid balancing services for utilities and independent power producers. Expanding grid-scale storage projects across global markets are expected to further strengthen demand for NCM-based systems, reinforcing their role as a core technology within the evolving energy storage landscape.

End-User Insights

The automotive segment is expected to account for approximately 65% of the nickel, cobalt, and manganese market share in 2026. The sector is consuming the highest volumes of NCM batteries, as electric vehicle manufacturers are prioritizing this chemistry to meet competitive range, power, and performance requirements. Electrification targets are driving sustained procurement across passenger vehicles, commercial fleets, and public transportation systems, reinforced by environmental regulations that are accelerating the phase-out of internal combustion engines.

Consumer preferences are also shifting toward zero-emission mobility, strengthening long-term demand. NCM chemistry is delivering a balanced combination of energy density, thermal stability, and scalable manufacturing, which is supporting mass-market adoption. Original equipment manufacturers (OEMs) are also standardizing NCM formulations across multiple vehicle platforms to optimize supply chains and control cost structures.

The electronics segment is projected to be the fastest-growing through 2033, driven by soaring demand for portable and connected devices. Manufacturers of smartphones, laptops, and wearable electronics are relying on NCM batteries to deliver high energy density within compact form factors, which is essential for extended runtime in space-constrained designs.

NCM chemistry also maintains strong capacity retention across thousands of charging cycles while preserving thermal stability, meeting both performance and safety expectations. Electronics original equipment manufacturers are therefore prioritizing standardized NCM battery specifications across product portfolios to streamline global supply chains, reduce development complexity, and accelerate product rollout.

Regional Insights

Asia Pacific Nickel Cobalt Manganese (NCM) Market Trends

Asia-Pacific is emerging as the largest and fastest-growing regional market for nickel, cobalt, and manganese cathode materials in 2026, accounting for an estimated 55% of the NCM market. The region controls a significant share of global battery manufacturing capacity and upstream raw material supply chains, reinforcing structural advantages in scale and cost efficiency. China is establishing clear leadership through highly integrated production ecosystems that combine mining, precursor processing, and cathode material manufacturing.

Government policies are accelerating electric vehicle adoption through consumer subsidies and manufacturing incentives, while domestic battery producers are expanding vertically integrated operations from materials through vehicle assembly. Battery manufacturers are standardizing NCM formulations across passenger vehicles, commercial fleets, and stationary storage applications, and automotive original equipment manufacturers are increasingly prioritizing regional suppliers to enhance proximity, reliability, and supply chain resilience.

The rapid expansion of renewable energy infrastructure across the region is another key driver of growth. Utility-scale solar PV and onshore wind installations are increasing the need for dispatchable storage capacity to manage intermittency and maintain grid stability. Japan is contributing advanced battery innovation through proprietary cathode coating and material doping techniques that improve performance and longevity. South Korean producers specialize in high-nickel formulations, such as NCM 811, which support premium automotive platforms with higher energy-density requirements. Regional governments are coordinating industrial development through technology transfer initiatives and joint research programs, further strengthening competitiveness.

Europe Nickel Cobalt Manganese (NCM) Market Trends

Europe is establishing itself as a strategically important region for NCM cathode materials, driven by an increasingly stringent regulatory and policy environment. The European Union (EU) is enforcing ambitious carbon-reduction targets, while the Battery Regulation framework mandates recycled-content thresholds and responsible-sourcing standards across the battery value chain. Electric vehicle adoption is accelerating as corporate average fuel economy requirements and zero-emission vehicle mandates are tightening across member states.

National governments are also designing industrial policy, keeping in mind clean technology funding programs and regional development initiatives. Germany is maintaining regional leadership through its premium automotive manufacturing base, supported by the rapid development of battery gigafactories aligned with domestic demand from original equipment manufacturers. At the country level, targeted investments are strengthening Europe’s upstream and midstream capabilities. France is investing heavily in cathode material processing through state-backed industrial partnerships, while the U.K. is coordinating battery ecosystem development through funding mechanisms of the Advanced Propulsion Centre.

Across the region, governments are prioritizing supply chain localization to improve strategic autonomy in critical materials. Circular economy principles are shaping innovation, as battery producers are integrating hydrometallurgical recycling processes that recover more than 95% of the cathode material value. Cobalt reduction strategies are accelerating adoption of high-nickel formulations such as NCM 811, balancing energy density with ethical sourcing requirements. Precursor manufacturers are also advancing sustainable synthesis routes, supported by waste heat recovery systems and closed-loop water circuits that are improving processing efficiency and reducing environmental impact.

North America Nickel Cobalt Manganese (NCM) Market Trends

The North America NCM market is demonstrating strong growth potential, led by accelerating electric vehicle production in the United States. Policy support under the Inflation Reduction Act (IRA) is channeling substantial investment into clean energy, including tax credits for battery manufacturing and incentives for electric vehicle purchases. Major automotive manufacturers are expanding domestic capacity, with Tesla operating large-scale production facilities in Nevada and Texas, General Motors scaling Ultium battery plants, and Ford developing Blue Origin manufacturing complexes.

These players are forming long-term partnerships with cathode material suppliers to secure dependable NCM supply chains and reduce exposure to global sourcing risks. Public-sector research and regional integration are further strengthening the market outlook. Federal programs led by the United States Department of Energy (DOE) support next-generation cathode chemistry development, while the Advanced Research Projects Agency–Energy (ARPA-E) funds innovation in battery recycling technologies.

Canada is leveraging domestic nickel mining resources and expanding processing infrastructure to support regional material security, reinforced by government-backed agreements with automotive manufacturers. Mexico is broadening its automotive footprint to include electric vehicle assembly, complementing upstream and midstream capacity across the region. These initiatives are accelerating supply chain integration, as near-shoring strategies reduce reliance on overseas imports and position North America as a more self-sufficient and resilient NCM production hub.

Competitive Landscape

The global nickel cobalt manganese market structure is a moderately concentrated one, spearheaded by CATL, LG Energy, Samsung SDI, Panasonic Energy, and Umicore, which rule around three-fifths of the market. This concentration is reflecting the high capital intensity, technical complexity, and scale advantages required to compete effectively in advanced battery materials. Leading companies are accelerating research and development investments focused on next-generation NCM formulations, with engineering teams optimizing energy density through high-nickel compositions such as nickel cobalt manganese 811 (NCM 811) and nickel cobalt manganese 955 (NCM 955).

Material scientists are simultaneously reducing cobalt content to address cost volatility and sourcing concerns, while maintaining thermal stability and cycle life. Process engineering efforts are improving synthesis efficiency by combining precise wet-chemistry methods with manufacturing processes that support large-scale, cost-competitive production. Strategic collaboration is playing a central role in reinforcing competitive positioning across the NCM value chain.

Cathode material producers are forming technology partnerships with battery manufacturers to co-develop application-specific material specifications that align with automotive, energy storage, and industrial performance requirements. Automotive OEMs are establishing joint ventures with precursor suppliers to secure long-term material availability and stabilize procurement costs. Research institutions are contributing through licensing of proprietary coating techniques and doping strategies, which are enhancing performance differentiation at the material level. These collaborative models are shortening development cycles, reducing commercialization risk, and enabling coordinated innovation, allowing participants to strengthen market position.

Key Industry Developments:

- In January 2026, Honda and Princeton NuEnergy signed an MOU to collaborate on plasma-based direct cathode-to-cathode recycling for lithium-ion batteries that rejuvenates NCM cathode material to match primary raw performance.The partnership advances Honda's electrification and resource circularity goals through joint validation and potential commercial-scale closed-loop production of battery-grade materials.

- In January 2026, researchers at Monash University developed a novel recycling process using mild deep eutectic solvents to recover over 95% of nickel, cobalt, manganese, and lithium from spent lithium-ion battery black mass, eliminating high temperatures and hazardous chemicals.

- In February 2025, BMW announced plans to mass produce its sixth-generation cylindrical NCM batteries in China by 2026, promising 30% more range, 20% higher energy density, 30% faster charging, and up to 50% lower production costs compared to current packs.

Companies Covered in Nickel Cobalt Manganese (NCM) Market

- CATL

- LG Energy Solution

- Samsung SDI

- Panasonic Energy

- SK On

- Umicore

- Xiamen Tungsten

- Hunan Shanshan Energy Technology

- BASF

- Sumitomo Metal Mining

- Toda Kogyo

- Posco Chemical

Frequently Asked Questions

The global nickel cobalt manganese (NCM) market is projected to reach US$ 6.0 billion in 2026.

Explosive electric vehicle adoption and renewable energy storage demand require high-energy-density NCM cathode materials, driving market growth.

The market is poised to witness a CAGR of 14.3% from 2026 to 2033.

Electrification drives across India and China, solid-state battery integration, and battery recycling infrastructure development are opening new opportunities.

CATL, LG Energy Solution, Samsung SDI, Panasonic Energy, and Umicore are some of the key players in the market.