- Food Ingredients & Additives

- Mycotoxin Testing Market

Mycotoxin Testing Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Mycotoxin Testing Market by Mycotoxin Type (Aflatoxin, Ochratoxins, Deoxynivalenol, Fumonisins, Zearalenone, Trichothecene, Patulin, Others), Technology (Chromatography-Based, Immunoassay-Based, Rapid & Point-of-Care Methods, Spectroscopy & Advanced Methods), Sample Type (Dairy, Meat & Poultry, Processed Food, Fruits & Vegetables, Others), and Regional Analysis from 2026 - 2033

Mycotoxin Testing Market Share and Trends Analysis

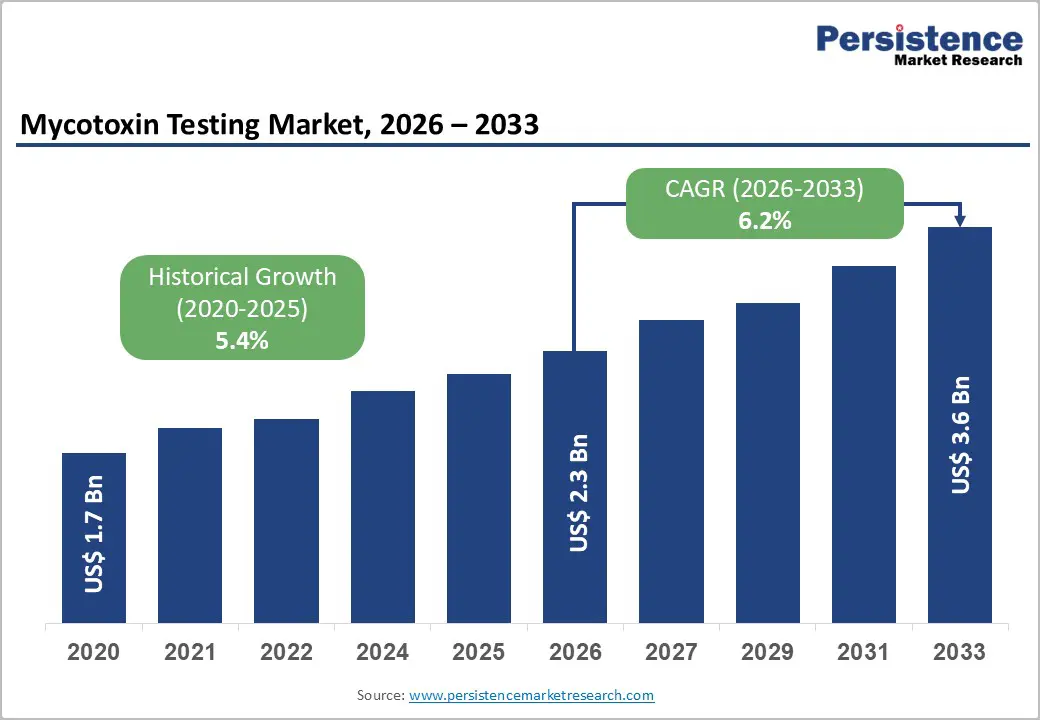

The global mycotoxin testing market is estimated to grow from US$ 2.3 billion in 2026 to US$ 3.6 billion by 2033. The market is projected to record a CAGR of 6.2% during the forecast period from 2026 to 2033.

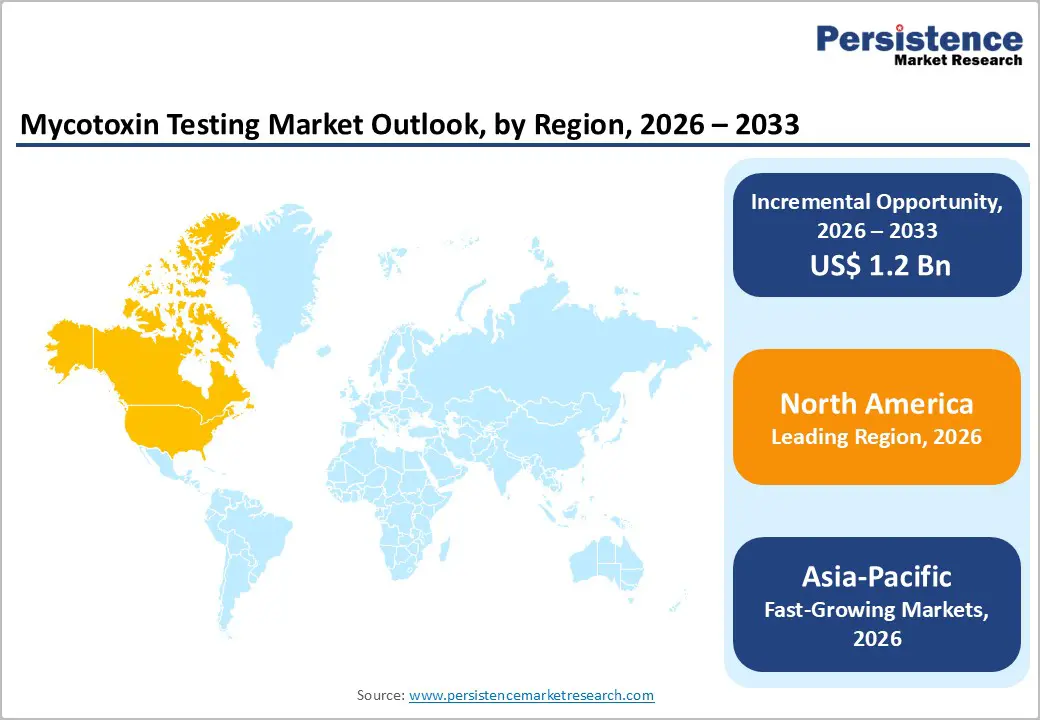

The global market is witnessing steady growth, driven by rising food safety concerns, stringent regulatory standards, and increasing contamination in cereals and feed. North America leads due to strong regulatory frameworks and advanced testing infrastructure. Asia-Pacific is the fastest-growing region, supported by expanding food exports, rising awareness, and improving laboratory capabilities.

Key Industry Highlights:

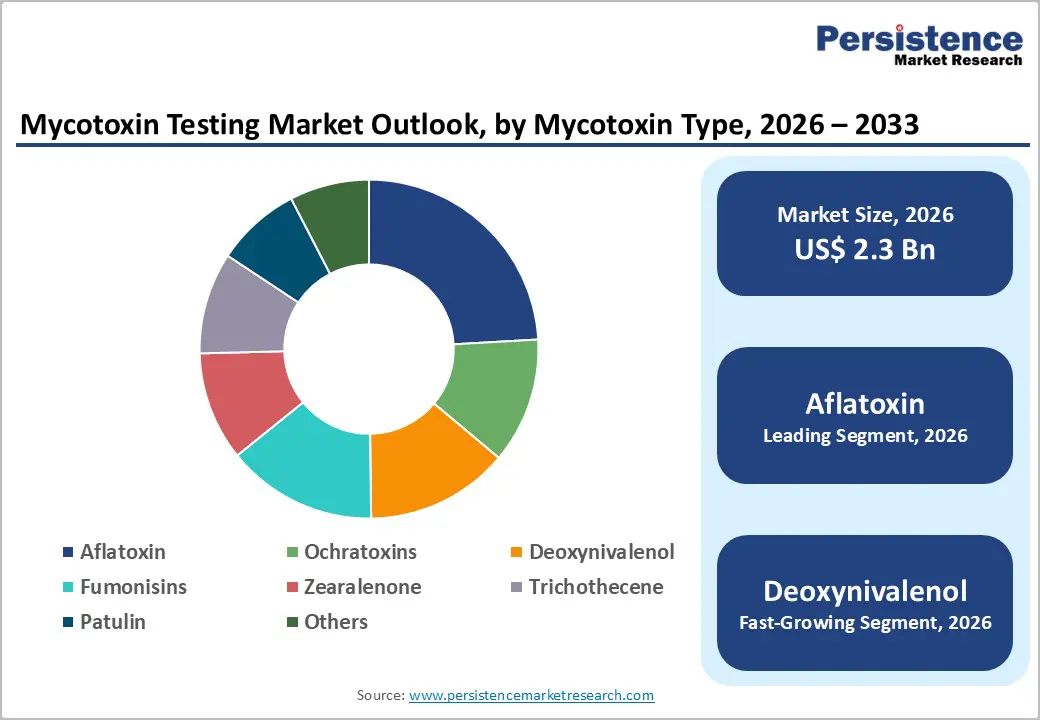

- Dominant Mycotoxin Type Segment: Aflatoxin testing held the largest share 24.1% in 2025, driven by its high toxicity, widespread occurrence in cereals and nuts, and stringent global regulatory limits requiring routine monitoring.

- Regional Leadership: North America led the mycotoxin testing market in 2025, with a 33.0% share, supported by strict food safety regulations, advanced laboratory infrastructure, a strong presence of testing companies, and high awareness of food contamination risks.

- Growth Indicators: Growth is driven by rising food safety concerns, stringent regulatory standards, increasing global trade of food and feed, and a higher incidence of mycotoxin contamination due to climate variability.

- Market Opportunity: Opportunities exist in rapid testing technologies, expansion of third-party testing services, increasing demand in emerging markets, and advancements in multi-mycotoxin detection solutions.

| Key Insights | Details |

|---|---|

|

Mycotoxin Testing Market Size (2026E) |

US$ 2.3 Bn |

|

Market Value Forecast (2033F) |

US$ 3.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.2% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.4% |

Market Dynamics

Driver: Rising Incidence of Mycotoxin Contamination in Food and Feed

Mycotoxin contamination is a major global food safety issue, significantly driving demand for testing. According to the World Health Organization, mycotoxins commonly contaminate staples such as maize, wheat, rice, and nuts, often penetrating deep into food products and remaining undetectable without testing. Regulatory bodies like Codex Alimentarius have set extremely low permissible limits (e.g., 0.5–15 µg/kg for aflatoxins), highlighting the severity of contamination risks. This strict regulation necessitates continuous monitoring across food supply chains, especially in export-driven economies where compliance is mandatory.

The scale of contamination further reinforces the demand for testing. The Food and Agriculture Organization estimates that around 25% of global crops are affected by mycotoxins, making contamination a widespread agricultural issue. In some regions, contamination levels have exceeded safety thresholds by large margins, with aflatoxin levels in staple foods reported far above regulatory limits. This high prevalence, combined with risks such as carcinogenicity and livestock toxicity, is pushing governments and industries to adopt routine and advanced mycotoxin testing solutions across food and feed sectors.

Restraint: High Cost of Advanced Testing Technologies (LC-MS/MS)

Advanced analytical techniques such as LC-MS/MS and HPLC are considered gold standards for mycotoxin detection due to their high sensitivity and ability to detect multiple toxins simultaneously. However, these technologies involve significant capital investment, skilled personnel, and complex sample preparation processes. Regulatory frameworks require detection at very low concentrations (µg/kg levels), which further necessitates expensive instrumentation and validation procedures. The World Health Organization emphasizes that maintaining compliance with such low tolerance limits requires sophisticated laboratory infrastructure and continuous monitoring systems.

Additionally, operational costs, including maintenance, calibration, and reagent expenses, make these technologies less accessible in developing regions. Many small-scale producers and regional laboratories lack the financial capacity to adopt such systems, creating a gap in testing coverage. This leads to reliance on external laboratories, increasing turnaround time and costs. While rapid kits exist, confirmatory testing still depends on chromatography-based systems, reinforcing cost barriers. As a result, despite growing contamination risks, the high cost of advanced testing technologies continues to limit widespread adoption, particularly in low- and middle-income countries.

Opportunity: Growing Demand for Rapid and On-Site Testing Solutions

The increasing complexity of global food supply chains is driving demand for rapid, on-site mycotoxin testing solutions. Traditional laboratory-based methods are time-consuming and unsuitable for real-time decision-making in agriculture, storage, and logistics. According to the World Health Organization, proper monitoring and control of mycotoxins require frequent inspection across multiple stages, including harvesting, storage, and distribution. This creates a strong need for portable, easy-to-use diagnostic tools that can provide immediate results and reduce contamination risks early in the supply chain.

Furthermore, with 25% of global crops affected by mycotoxins as reported by the Food and Agriculture Organization, large-scale screening becomes essential. Rapid testing kits, such as lateral flow assays and ELISA-based methods, enable high-throughput screening at lower cost, making them ideal for field use and in developing regions. These technologies support faster compliance checks, reduce product recalls, and enhance export quality assurance. As regulatory scrutiny increases globally, the shift toward decentralized, point-of-care testing solutions presents a significant growth opportunity for market players.

Category-wise Analysis

By Mycotoxin Type

Aflatoxins dominate the mycotoxin testing market due to their extreme toxicity and strict global regulation. The WHO classifies aflatoxin B1 as a potent human carcinogen, strongly linked to liver cancer, driving mandatory monitoring in food systems. Governments enforce very low permissible limits (often below 10 µg/kg), requiring frequent and sensitive testing. In addition, aflatoxins are widely prevalent in staple crops like maize, peanuts, and nuts, especially in tropical regions. The FAO estimates that around 25% of global crops are contaminated by mycotoxins, with aflatoxins being the most critical concern. This combination of high health risk, widespread occurrence, and strict compliance requirements ensures aflatoxin testing remains the largest segment globally.

By Technology

Chromatography-based technologies dominate due to their role as the gold standard for confirmatory mycotoxin testing. Methods such as HPLC and LC-MS/MS offer high sensitivity, detecting toxins at µg/kg or even lower levels, which is essential to meet strict regulatory limits set by Codex and food safety authorities. Scientific studies confirm chromatography as the most widely used analytical method for accurate quantification of mycotoxins. These systems also enable simultaneous detection of multiple toxins, improving efficiency in complex food matrices. While rapid tests are used for screening, final validation relies on chromatography due to its precision and reliability. Its regulatory acceptance, accuracy, and multi-toxin capability make it the dominant technology despite higher costs.

Regional Insights

North America Mycotoxin Testing Market Trends

North America dominates the mycotoxin testing market due to strict regulatory frameworks and advanced testing infrastructure. In the United States, the U.S. Food and Drug Administration enforces action levels for aflatoxins as low as 20 µg/kg in food, mandating routine monitoring across supply chains. The United States Department of Agriculture also conducts extensive grain inspection programs to ensure compliance. Additionally, the region has a well-established network of accredited laboratories and high adoption of advanced analytical technologies. High consumption of processed foods and large-scale grain production further increase testing needs. Combined with strong awareness and enforcement, these factors ensure North America remains the leading regional market.

Europe Mycotoxin Testing Market Trends

Europe is a key region due to its highly stringent and harmonized food safety regulations. The European Food Safety Authority and the European Commission set some of the strictest mycotoxin limits globally, such as aflatoxin B1 limits as low as 2 µg/kg in certain foods. These tight thresholds require frequent and highly sensitive testing. Europe also has strong import controls, with mandatory screening of food and feed entering the region. According to EFSA, mycotoxins are among the top food safety concerns monitored annually, reinforcing the need for consistent testing. The region’s focus on consumer safety, traceability, and regulatory compliance makes it a critical and mature market.

Asia-Pacific Mycotoxin Testing Market Trends

Asia Pacific is the fastest-growing region due to high contamination risk, expanding food trade, and improving regulatory systems. The Food and Agriculture Organization reports that around 25% of global crops are affected by mycotoxins, with higher prevalence in warm, humid climates common across Asia. Countries like India and China are major producers and exporters of cereals, increasing the need for compliance testing. Governments are strengthening food safety frameworks, such as India’s Food Safety and Standards Authority of India, which enforces mycotoxin limits in food products. Rising awareness, export requirements, and expanding laboratory infrastructure are accelerating adoption, making the Asia Pacific the fastest-growing regional market.

Competitive Landscape

The mycotoxin testing market is highly competitive, led by companies such as SGS SA, Eurofins Scientific SE, Intertek Group plc, ALS Limited, and Mérieux NutriSciences. These players focus on advanced testing technologies, regulatory compliance, global lab expansion, and service portfolio strengthening.

Key Industry Developments:

- In March 2026, Qalitex Laboratories expanded its mycotoxin testing capabilities by enhancing its analytical infrastructure and service offerings. The company upgraded its laboratory with advanced technologies such as LC-MS/MS to improve detection accuracy and enable multi-mycotoxin analysis across food and feed samples. This expansion aimed to support stricter regulatory compliance and increasing demand for food safety testing.

- In February 2025, CellMade® advanced mycotoxin testing by introducing comprehensive solutions and launching new products designed to improve detection efficiency and accuracy. The company focused on integrating advanced analytical technologies and user-friendly testing kits to support rapid and reliable identification of multiple mycotoxins across food and feed samples.

Companies Covered in Mycotoxin Testing Market

- SGS SA

- Eurofins Scientific SE

- Romer Labs Division Holding GmbH

- Charm Sciences, Inc.

- Intertek Group plc.

- Trilogy Analytical Laboratories

- ELISA Technologies, Inc.

- EMSL Analytical, Inc

- Belcosta Labs, Inc.

- ALS Limited

- Mérieux NutriSciences

- Premier Analytical Services

- Others

Frequently Asked Questions

The global mycotoxin testing market size is projected to be valued at US$ 2.3 Bn in 2026.

Stringent food safety regulations, rising contamination incidence, global trade growth, and increasing consumer awareness.

The global mycotoxin testing market is poised to witness a CAGR of 6.2% between 2026 and 2033.

Rapid testing adoption, emerging market expansion, third-party services growth, and advancements in multi-mycotoxin detection technologies.

SGS SA, Eurofins Scientific SE, Romer Labs Division Holding GmbH, Charm Sciences, Inc., Intertek Group plc., Trilogy Analytical Laboratories.