- Agrochemicals

- Mycotoxin Binding Agents Market

Mycotoxin Binding Agents Market Size, Share, and Growth Forecast 2026 - 2033

Mycotoxin Binding Agents Market by Product Type (Inorganic Binders, Organic Binders, Biological Binders, Composite/Hybrid Binders), by Mycotoxin Type (Aflatoxins, Ochratoxins, Fumonisins, Zearalenone, Deoxynivalenol, T-2 & HT-2 Toxins, Others), by Form (Powder, Granules, Liquid, Pellets), by Application (Animal Feed, Food & Beverages, Pet Food, Aquaculture, Others), by Regional Analysis, 2026 - 2033

Mycotoxin Binding Agents Market Size and Trend Analysis

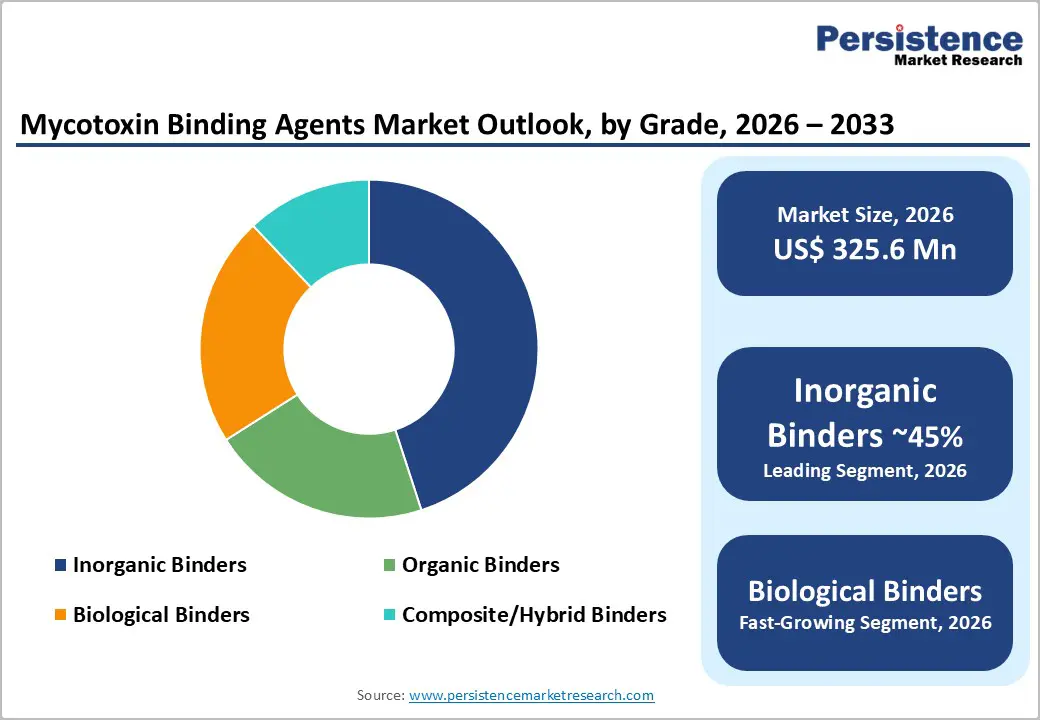

The global mycotoxin binding agents market size is likely to be valued at US$ 325.6 million in 2026 and is expected to reach US$ 446.1 million by 2033, growing at a CAGR of 4.6% during the forecast period from 2026 to 2033. Market growth is fundamentally driven by the escalating prevalence of mycotoxin contamination in agricultural commodities and animal feed worldwide, coupled with increasingly stringent regulatory frameworks enforced by governing bodies across North America, Europe, and the Asia Pacific.

Key Market Highlights

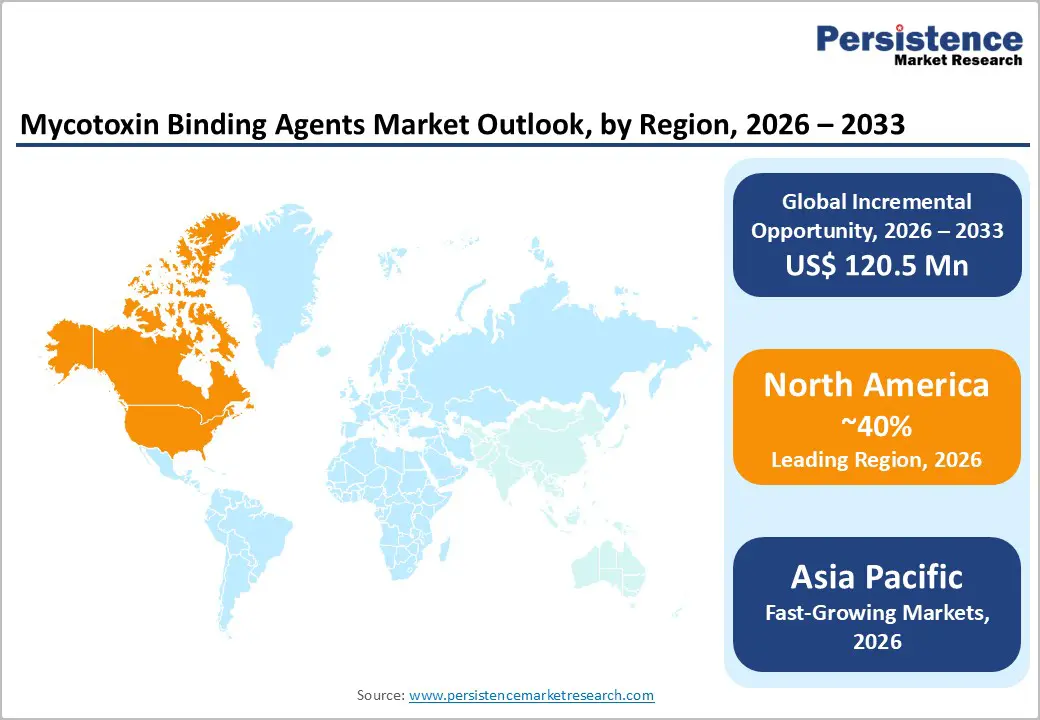

- Leading Region: North America dominates the mycotoxin binding agents market with approximately 40% global revenue share, driven by highly developed livestock infrastructure, stringent FDA regulatory frameworks, substantial poultry and dairy operations, and widespread producer awareness regarding economic losses from mycotoxicosis requiring proactive toxin mitigation.

- Fastest-Growing Region: Asia Pacific demonstrates the highest expansion trajectory at a 7.2% CAGR, with China commanding 63.5% of the East Asian market share, supported by massive growth in the livestock industry, government renewable energy initiatives, and regulatory tightening, which create persistent demand for advanced binding solutions.

- Dominant Segment: Inorganic Binders command approximately 45% market share, with Bentonite specifically representing 48% of the inorganic segment share, leveraging exceptional aflatoxin adsorption capacity (83% mean efficiency), natural abundance, cost-effectiveness, and established supply chain infrastructure supporting market leadership.

- Fastest-Growing Segment: Biological Binders and Biotransformers experience accelerated 15% CAGR growth following FDA's August 2022 fumonisin esterase approval, establishing regulatory precedent for enzyme-based mycotoxin degradation solutions offering superior performance, addressing multi-mycotoxin co-contamination challenges.

- Key Market Opportunity: Aquaculture feed safety expansion in the Asia-Pacific region, where 93.8% of fish feed samples contain regulated mycotoxins and India's aquaculture sector is growing at a 13.3% CAGR, creates substantial demand for cost-effective, region-optimized binder formulations that mitigate risks of plant-based feed-ingredient contamination.

| Key Insights | Details |

|---|---|

|

Mycotoxin Binding Agents Market Size (2026E) |

US$ 325.6 Million |

|

Market Value Forecast (2033F) |

US$ 446.1 Million |

|

Projected Growth CAGR (2026-2033) |

4.6% |

|

Historical Market Growth (2020-2025) |

3.2% |

Market Dynamics

Drivers - Rising global livestock production and stricter feed safety regulations are driving sustained demand for effective mycotoxin-binding solutions worldwide

Global livestock production has expanded rapidly to meet the growing demand for animal protein driven by population growth and rising disposable incomes, particularly across emerging economies. The Asia-Pacific region is experiencing robust growth in poultry, swine, and aquaculture production, with countries such as China, India, and Indonesia significantly increasing production capacity. This industrial expansion increases exposure to mycotoxin contamination, as large-scale farms rely on feed ingredients sourced from global commodity markets, where fungal contamination is common.

The U.S. livestock sector processes nearly 600 million poultry units annually, while China reports comparable production volumes, underscoring the need for feed safety systems to ensure uninterrupted operations. Regulatory authorities, including the FDA, the European Food Safety Authority, and India’s FSSAI, have implemented strict compliance frameworks that define maximum allowable mycotoxin limits. These regulations require feed manufacturers and integrators to adopt effective mycotoxin-binding agents as standard safety practices to ensure legal compliance, protect animal health, and maintain consistent production efficiency.

Climate change and widespread multi-mycotoxin contamination are increasing awareness and accelerating the adoption of broad-spectrum toxin control solutions

Climate change has significantly altered agricultural environments through temperature fluctuations, irregular rainfall, and extended growing seasons, creating favorable conditions for mycotoxin-producing fungi. Scientific studies indicate that nearly 88% of animal feed samples contain at least one major mycotoxin, while 80% of global feed and crop samples exceed permitted contamination levels. Multi-mycotoxin contamination has become increasingly common rather than exceptional. For example, research shows that 96% of livestock feed samples in Kenya contained multiple toxins, including aflatoxins, fumonisins, and zearalenone.

This co-contamination intensifies economic losses, as combined toxin exposure produces stronger adverse effects than exposure to individual toxins. As awareness of these synergistic impacts grows through research publications and industry events, producers are actively seeking broader protection solutions. This trend is driving demand for advanced mycotoxin binders capable of addressing multiple toxins at once, outperforming traditional single-mechanism products.

Restraints - High costs of advanced binders and concerns over nutrient loss continue to limit adoption in price-sensitive and regulation-driven markets

Advanced mycotoxin-binding formulations, especially those incorporating biological components and engineered polymers, are priced at a premium due to complex manufacturing processes and stringent quality validation requirements. In cost-sensitive regions such as Latin America, Sub-Saharan Africa, and parts of the Asia Pacific, adoption of these premium solutions remains limited. Many producers continue to use low-cost clay-based binders despite their lower performance.

Another major concern is nutrient binding, as some formulations inadvertently bind essential minerals and vitamins with toxins, reducing feed nutritional value and adversely affecting animal performance. Regulatory bodies closely monitor this issue. The European Union, for instance, restricts the inclusion of clay to a maximum of 2% in feed formulations to prevent nutrient loss. These limitations reduce manufacturers' formulation flexibility and create compliance challenges, particularly for companies supplying standardized products across multiple regions with varying regulatory expectations.

Fragmented global regulatory frameworks increase compliance complexity, delaying commercialization and raising development costs for manufacturers

The global mycotoxin binder market faces significant challenges due to inconsistent regulatory systems across major regions. In the United States, the FDA has not formally approved any mycotoxin binder under GRAS status, limiting product classifications mainly to feed additives. In contrast, the European Union enforces rigorous feed additive registration procedures requiring extensive scientific documentation and risk assessments. China’s updated GB 13078-2023 regulation sharply reduced the allowable aflatoxin level in poultry feed from 50 ppb to 10 ppb, creating pressure to reformulate existing products.

India’s FSSAI mandates the registration of foreign facilities, thereby increasing compliance complexity for international suppliers. Meanwhile, Canada, Australia, and other regions maintain separate approval structures. This regulatory fragmentation forces manufacturers to develop region-specific formulations, extend commercialization timelines, and increase regulatory expenses, ultimately slowing global product launches and limiting economies of scale.

Opportunity - Growing regulatory acceptance of enzyme-based biotransformation technologies is unlocking premium growth opportunities in advanced mycotoxin mitigation solutions

The FDA’s approval of fumonisin esterase in August 2022 marked a major milestone for enzyme-based mycotoxin mitigation technologies. This approval validated biotransformation approaches that degrade mycotoxins into non-toxic compounds rather than simply adsorbing them. The decision has opened regulatory pathways for similar innovations targeting toxins such as zearalenone and deoxynivalenol.

In 2022, DSM-Firmenich launched Mycofix Plus 5. Z in the Asia Pacific, highlighting strong market acceptance for enzyme-enhanced solutions. Currently, biotransformers account for nearly 15% of the total market and are expected to grow at a CAGR of over 12% through 2033. These solutions are particularly attractive in aquaculture, pet food, and premium livestock segments where performance reliability is critical. Manufacturers investing in enzyme technology and microbial platforms are well-positioned to capture high-margin opportunities as regulatory approvals continue to expand globally.

Rapid Aquaculture Expansion and Rising Plant-Based Feed Usage in the Asia Pacific are Creating Strong Demand For Specialized Mycotoxin Control Products

Aquaculture is among the fastest-growing markets for mycotoxin-binding agents, driven by the industry’s shift from fishmeal to plant-based feed ingredients. This transition significantly increases exposure to mycotoxin contamination. Studies show that 93.8% of fish feed and 83.6% of shrimp feed samples contain at least one regulated mycotoxin, with several exceeding EU safety limits. Asia-Pacific leads global aquaculture expansion, with India growing at a 13.3% CAGR and Indonesia experiencing similarly strong production growth.

These trends are creating urgent demand for effective feed safety solutions. Regional markets require cost-efficient and locally optimized binders designed for prevalent mycotoxin profiles. Manufacturers that offer aquaculture-specific formulations and establish regional production facilities gain strong competitive advantages. Strategic partnerships with feed mills and aquaculture integrators across China, Southeast Asia, and South Asia further strengthen market penetration and long-term revenue potential.

Category-wise Analysis

Product Type Insights

Inorganic binders dominate the feed mycotoxin binders market, holding nearly 45% market share due to their cost-effectiveness, wide availability, and strong binding performance. These binders primarily comprise clay minerals, zeolites, and aluminosilicate compounds and are widely used in commercial feed operations. Bentonite- and montmorillonite-based formulations lead this segment, accounting for approximately 33% of total market consumption.

These materials exhibit strong adsorption efficiency, binding nearly 0.8 mg of aflatoxin B1 per gram of clay. In 2023, North American feed manufacturers consumed around 198,000 metric tons of raw clay binders, representing nearly 38% of global raw clay usage. Average wholesale prices remained stable at approximately US$ 380 per ton. The continued preference for inorganic binders reflects their proven performance, regulatory acceptance, and suitability for large-scale feed manufacturing operations.

Mycotoxin Type Insights

Aflatoxin B1 remains the primary focus of mycotoxin control strategies, accounting for nearly 35% of total market demand. This dominance is driven by its high toxicity and carcinogenic risk, as well as strict regulatory limits across global feed markets. Bentonite-based binders continue to deliver strong performance, achieving more than 95% reduction in aflatoxin B1 under controlled conditions. These solutions are widely approved in North America, Europe, and Asia, reinforcing their commercial reliability. Zearalenone and fumonisins constitute the second-largest demand segment, together accounting for 25% of the total market focus.

Organic binders exhibit particularly strong performance for zearalenone via β-glucan interactions, achieving removal efficiencies of 85%. In contrast, ochratoxin A and trichothecenes such as deoxynivalenol and T-2/HT-2 toxins remain technically challenging, with conventional binders achieving only 20% reduction. This gap has accelerated innovation toward composite binders and enzymatic biotransformation technologies.

Form Insights

Powder-based mycotoxin binders continue to dominate the market, accounting for approximately 60% of the market share due to their widespread acceptance in industrial feed manufacturing. Their ease of storage, long shelf life, and compatibility with standard premix systems make them the preferred choice for large feed mills. Granule formulations account for 20% of the market and are commonly used in smaller operations, where reduced dust generation and improved handling are important considerations. These products enhance workplace safety and improve mixing consistency.

Liquid binders are emerging as the fastest-growing segment, recording annual growth rates of 15%. Market share has increased from nearly 8% in 2022 to an estimated 15% by 2026. Liquid formulations enable accurate dosing via automated metering systems and provide uniform distribution, even at inclusion rates of 0.3–0.5% in complete feed. Their precision and efficiency are driving growing adoption across modern feed facilities.

Regional Insights

North America Mycotoxin Binding Agents Market Trends

North America leads the global market with approximately 40% revenue share, driven primarily by the United States. The region’s dominance reflects highly structured livestock production systems across poultry, dairy, and swine industries. The U.S. processes nearly 600 million poultry units annually and maintains extensive dairy and feedlot operations, generating consistent demand for feed safety solutions. Strict FDA action limits for aflatoxins, fumonisins, and DON require proactive mitigation strategies, positioning mycotoxin binders as essential components rather than optional additives.

High producer awareness regarding economic losses from mycotoxicosis further supports stable demand. Poultry integrators often mandate binder inclusion across all feed formulations. Market trends favor advanced composite and enzymatic products, with premium segment growth outpacing basic binder demand. Leading companies such as Novus, Kemin, BASF, and Biomin maintain strong positions through technical support, research-backed efficacy, and established distribution networks.

Europe Mycotoxin Binding Agents Market Trends

Europe represents the second-largest regional market, accounting for approximately 35% of global revenue. The region is defined by extremely strict regulatory standards and strong preference for premium feed additives. EU Regulation 2023/915 sets some of the world’s lowest permissible aflatoxin limits, compelling advanced mitigation strategies. Recent updates also tightened limits for DON, T-2, and HT-2 toxins, increasing compliance pressure.

Countries such as Germany, the UK, France, and Scandinavia experience a high prevalence of Fusarium toxins due to climatic conditions. Germany alone is projected to record over 12% CAGR binder adoption. European producers strongly favor natural, sustainable, and organic-certified solutions aligned with environmental regulations. This has driven innovation in enzyme-based and composite binders. Companies including Selko, Biomin, and Kemin Europe benefit from region-specific formulations tailored to local toxin profiles and regulatory frameworks.

Asia Pacific Mycotoxin Binding Agents Market Trends

Asia Pacific is the fastest-growing regional market, expanding at approximately 7.2% CAGR. China dominates the region, accounting for more than 60% of East Asian market share due to massive livestock production and recent regulatory tightening. The GB 13078-2023 standard significantly reduced allowable aflatoxin limits, accelerating binder adoption among large integrators. India represents the second-largest regional market, supported by rapid poultry expansion and strong aquaculture growth.

Indonesia also shows rising demand driven by biodiesel and aquafeed production. Market dynamics reflect strong price sensitivity, encouraging widespread use of clay-based binders alongside emerging premium adoption. Local manufacturers supply cost-effective solutions, while multinational companies expand distribution partnerships. Regulatory enforcement varies across countries, creating both entry challenges and long-term growth potential. Increasing awareness of feed quality and export standards continues to strengthen demand for binders across Asian markets.

Competitive Landscape

The global mycotoxin binding agents market displays moderate concentration, with BASF SE holding a leading position through its diversified product portfolio and strong global infrastructure. BASF’s leadership is supported by integrated manufacturing, extensive R&D investment, and strategic partnerships with major feed producers. Biomin Holding GmbH has strengthened its presence through advanced formulations focused on multi-mycotoxin control and aquaculture applications. Kemin Industries maintains strong market positioning through specialized products addressing combined toxin and pesticide risks.

Competitive differentiation increasingly centers on formulation innovation, regulatory compliance capability, and technical advisory support. Sustainability-focused and eco-compliant solutions are gaining importance due to evolving regulatory and consumer expectations. Regional players such as Olmix, Industrial Técnica Pecuaria, and Asian manufacturers serve cost-sensitive markets with localized solutions. Overall, the market reflects a dual structure where premium global suppliers coexist alongside regional manufacturers targeting distinct regulatory and performance-driven customer segments.

Key Market Developments

- In January 2023, Biomin Holding GmbH introduced an advanced mycotoxin binder featuring enhanced multi-mycotoxin binding and thermal stability designed for premium poultry and swine segments, reinforcing comprehensive contamination management in high-performance feed applications.

- In June 2023, BASF SE expanded its mycotoxin binding agent production facilities in Brazil to strengthen strategic positioning in the Latin American market and support accelerated regional and Asia Pacific demand through optimized supply chain capacity.

- In February 2024, China’s updated GB 13078-2023 feed standard reduced allowable aflatoxin limits to 10 ppb, prompting major Chinese feed manufacturers to adopt premium binder formulations to meet stricter compliance and improve animal performance outcomes.

Companies Covered in Mycotoxin Binding Agents Market

- BASF SE

- Syngenta International AG

- E.I. du Pont

- Bayer AG

- Novus International Inc.

- Cargill

- Olmix S.A.

- Nutreco N.V.

- Biomin Holding GmbH

- Kemin Industries Inc.

- Venkys Ltd.

- Anpario plc

- Impextraco N.V.

- Industrial Técnica Pecuaria, S.A.

- Alltech Inc.

- DSM-firmenich

- Adisseo

- Selko B.V.

- Trouw Nutrition

- Novozymes A/S

Frequently Asked Questions

The global mycotoxin binding agents market is projected to reach US$ 446.1 million by 2033, growing at a 4.6% CAGR driven by livestock expansion and stricter feed safety regulations.

Key demand drivers include intensifying livestock production, strict regulatory limits, climate-driven mycotoxin risks, multi-toxin contamination awareness, and expanding aquaculture feed usage.

Inorganic binders, particularly bentonite, dominate the market with about 45% share due to cost efficiency, strong aflatoxin adsorption, and widespread availability.

North America leads the market supported by large-scale livestock operations, stringent FDA regulations, high producer awareness, and strong adoption of premium binder formulations.

The strongest opportunity lies in Asia Pacific aquaculture feed safety, driven by rapid industry growth, plant-based feed adoption, and rising mycotoxin contamination risks.

Major players include BASF SE, Biomin Holding GmbH, Kemin Industries, dsm-firmenich, Cargill, Novus International, Alltech, Bayer AG, and leading regional manufacturers.