- Technology

- LoRa Gateway Module Market

LoRa Gateway Module Market Size, Share, and Growth Forecast, 2025 - 2032

LoRa Gateway Module Market By Deployment Model (Private Networks, Others), Component (Software, Services, Hardware), End-user Application (Smart Cities, Industrial Automation, Smart Metering, Others), and Regional Analysis for 2025 - 2032

LoRa Gateway Module Market Share and Trends Analysis

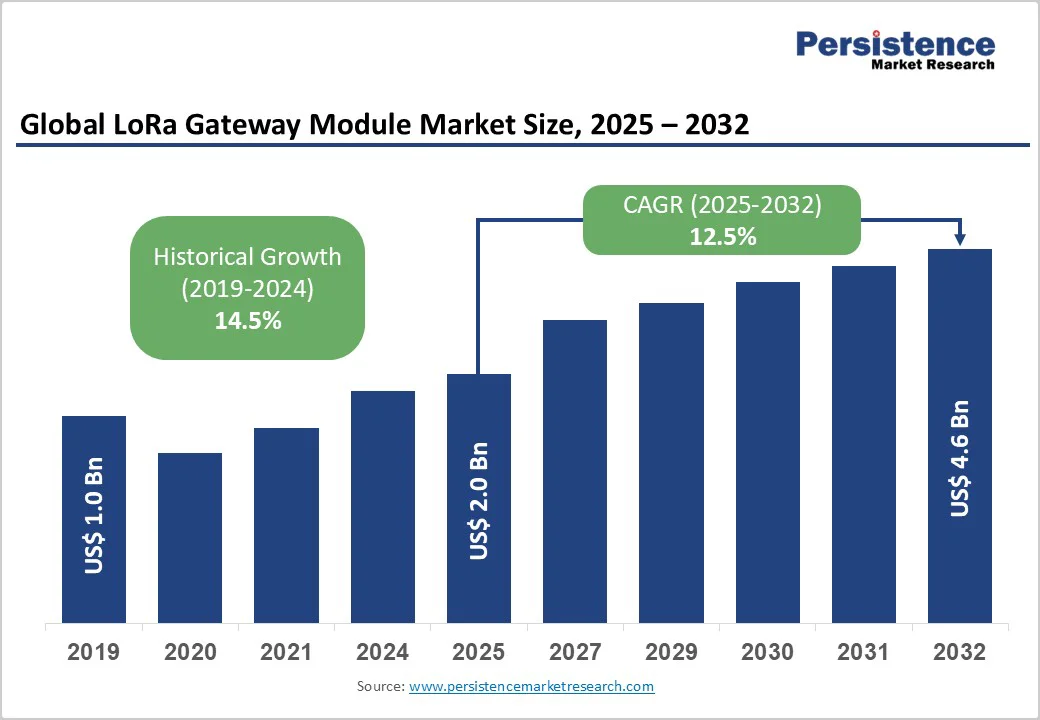

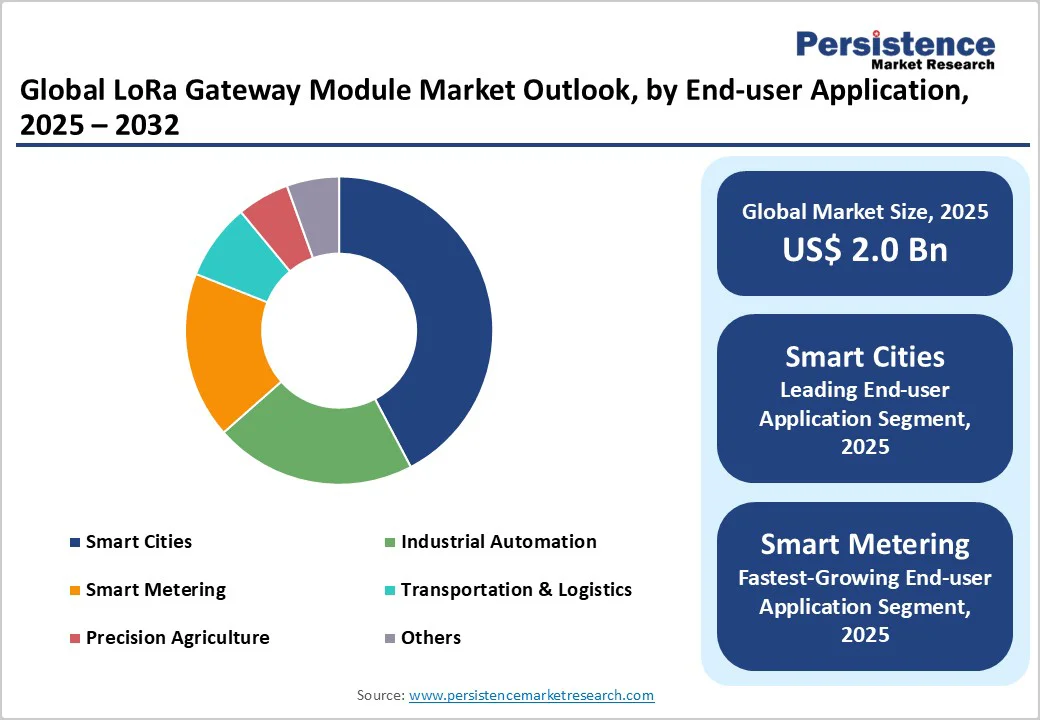

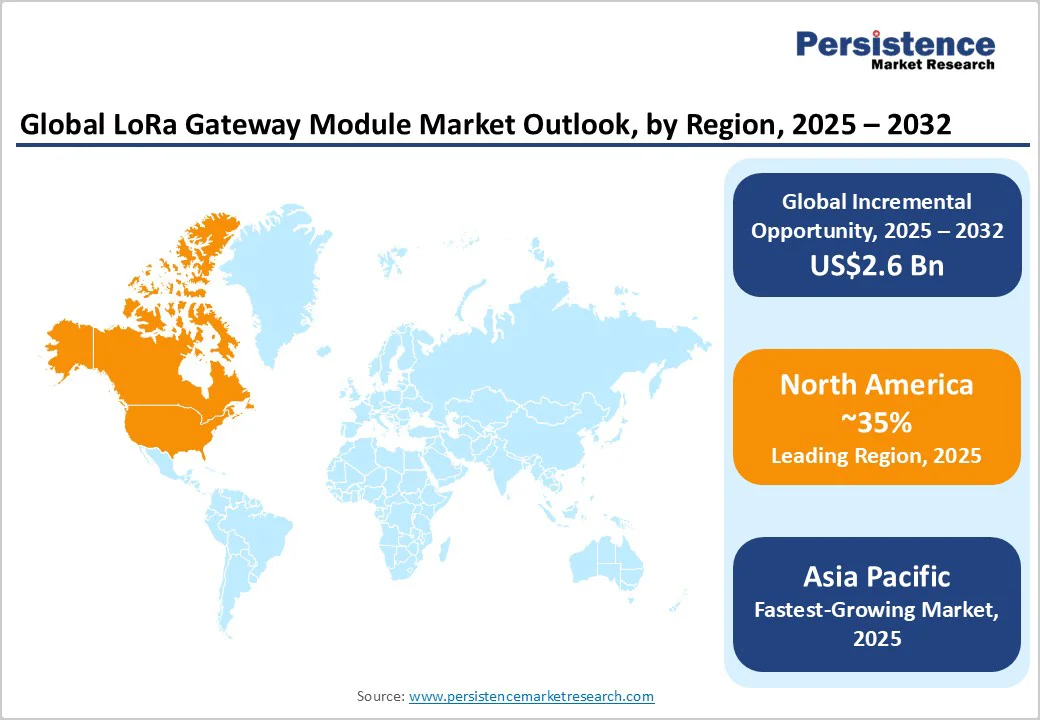

The global LoRa gateway module market size is likely to be valued at US$2.0 Billion in 2025, and is estimated to reach US$4.6 Billion by 2032, growing at a CAGR of 12.5% during the forecast period 2025−2032, driven by rapid digitization across key industries, robust IoT network rollouts, and increasing adoption of smart city infrastructure worldwide. LoRaWAN is emerging as the backbone for long-range, low-power data aggregation, driven by energy-efficient urban systems and scalable industrial connectivity. Market growth is fueled by investments in private and hybrid networks, cost-effective modules, supportive regulations, and advanced gateway innovations.

Key Industry Highlights

- Dominant & Fastest-growing Applications: Smart cities are anticipated to hold a dominant 42.3% market share in 2025, whereas smart metering is set to emerge as the fastest growing application at a 21.7% CAGR from 2025 to 2032.

- Dominant Region & Fastest-growing Regional Market: North America remains market leader with approximately 35% share in 2025, while Asia Pacific is slated to be the fastest-growing regional market at roughly 16.2% CAGR through 2032.

- Leading & Fastest-growing Deployment Models: Private networks are likely to account for about 39.5% of the LoRa gateway module market revenue share in 2025, with hybrid networks demonstrating a robust 16.8% CAGR through 2032.

- Leading & Fastest-growing Components: Hardware modules are set to secure around 46% of the market in 2025, while software platforms are forecast to grow at 18.4% CAGR through 2032.

- Competitive Environment: Strategic partnerships, M&A transactions, and targeted R&D investments are gradually reshaping the landscape, consolidating market power in segments where technical complexity and compliance DQ drive purchasing decisions.

- Investment Trends: Burgeoning opportunities in private industrial networks, advanced utility metering infrastructure, and regionally adapted gateway manufacturing are providing actionable targets for market companies.

| Key Insights | Details |

|---|---|

|

LoRa Gateway Module Market Size (2025E) |

US$2.0 Bn |

|

Market Value Forecast (2032F) |

US$4.6 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

12.5% |

|

Historical Market Growth (CAGR 2019 to 2024) |

14.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Proliferation of Smart Utility Metering Initiatives

Global regulatory mandates for precise energy monitoring and efficiency are accelerating the deployment of smart utility meters, a niche yet defining growth catalyst for LoRa gateway modules. According to the International Energy Agency (IEA), the number of smart electric meters globally surpassed 1 billion units as of 2024. Governments across the Organisation for Economic Co-operation and Development (OECD) and emerging economies are endorsing advanced metering infrastructure to minimize grid losses, improve tariff structures, and enhance resource sustainability.

For example, the European Commission (EC)'s Energy Efficiency Directive requires all member states to replace 80% of conventional meters with smart alternatives by 2026, directly boosting the demand for LoRa-enabled gateway modules. Utility providers, confronted with legacy infrastructure, are deploying LoRaWAN networks due to their long-range capabilities and cost-effectiveness. The World Bank further estimates that deploying advanced smart metering can reduce operational costs and improve billing accuracy significantly, which in turn will encourage both public and private utilities to invest in such technologies.

Fragmented Spectrum Allocation and Regulatory Ambiguity

Despite robust market momentum, fragmented frequency spectrum allocation and ongoing regulatory ambiguity are hindering the uniform global expansion of LoRa gateway modules. Industry associations have cited inconsistent national regulations for sub-GHz bands (433 MHz, 868 MHz, 915 MHz) as a structural challenge, affecting both vendor scalability and international deployment strategies. For example, China’s CN470 band remains isolated from EU868 and US915, resulting in increased engineering costs, supply chain disruption, and delayed cross-border projects.

In Asia Pacific, industry reports suggest that a sizeable portion of LoRaWAN rollouts in India and ASEAN markets face project delays attributable to spectrum disputes or uncoordinated licensing policies, resulting in a direct risk to anticipated deployment volumes for gateway vendors between 2023 and 2025. Regulatory uncertainty also inflates compliance costs. For example, a 2025 white paper highlighted an average 8% excess spent on spectrum validation and legal fees by module manufacturers, impacting margins and slowing innovation cycles.

Private LoRaWAN Networks for Industrial Campus Automation

The emergence of private LoRaWAN networks for campus-scale industrial automation is presenting highly lucrative and actionable opportunities for gateway module vendors and solution integrators. As governments and enterprises strive to digitalize logistics hubs, refineries, and manufacturing parks, private LoRaWAN networks are enabling secure, low-latency, and granular control of production assets and environmental parameters.

These networks mitigate risks related to data sovereignty, cybersecurity, and operational resilience, which are prioritized by multinationals facing stricter global privacy regulations. For instance, Germany’s Verband Deutscher Maschinen- und Anlagenbau (VDMA) notes that nearly three-fourths of new machine installations in 2025 will be equipped with private LoRaWAN connectivity for predictive maintenance and real-time monitoring. By enabling on-premise edge computing and localized network management, gateway modules are transforming operational models, reducing downtime, and allowing customized automation.

Category-wise Analysis

Deployment Model Insights

Private LoRaWAN networks are maintaining a dominant position in the global market, holding an estimated 39.5% share in 2025. This leadership is grounded in the increasing demand for secure and customizable connectivity in sectors such as manufacturing, utilities, and smart campuses. Enterprises are prioritizing private deployments to address data privacy, regulatory compliance, and unique operational needs, particularly in regions where public network infrastructure is fragmented or insufficient. Private network deployments further benefit from reduced latency, superior reliability, and localized control, resulting in improved operational efficiencies and wider adoption in mission-critical industrial automation projects.

The fastest-growing deployment segment is hybrid networks, forecast to grow at a CAGR of 16.8% from 2025 to 2032. Hybrid networks blend public backbone infrastructure with dedicated private overlays, enabling organizations to merge broad coverage with granular control. This is increasingly relevant for multi-national enterprises and government agencies operating across diverse regulatory environments. Hybrid deployments maximize cost-efficiency and network redundancy, supporting flexible service delivery in smart city projects and large-scale campus configurations.

Component Insights

Hardware modules, encompassing gateway devices, concentrators, and antennas, constitute the backbone of LoRaWAN infrastructure and are anticipated to account for 46% of the market revenue share in 2025. The dominance of hardware is shaped by the upfront requirement for physical deployment in new verticals and emerging regions, particularly where mass sensor installations and legacy upgrades are underway. Investments in hardware are being accelerated by advancements that improve modularity, multi-band support, and durability, allowing for wide-ranging use in both urban and industrial settings. The commoditization of certain hardware components is driving down costs while supporting broad expansion in areas such as smart metering, environmental sensing, and logistics.

Software platforms are slated to be the fastest-growing component segment through 2032. The growing complexity of IoT deployments is heightening demand for comprehensive software solutions that enable remote device management, data visualization, predictive analytics, and automated firmware updates. Edge computing integration within gateway modules is further enhancing operational intelligence and network resiliency. Vendors are increasingly shifting toward SaaS offerings and cloud-based service models, which not only augment recurring revenues but also enhance customer loyalty through continuous feature updates and scalability.

End-user Application Insights

Smart cities are likely to represent the largest end-use segment, contributing an estimated 42.3% of the LoRa gateway module market revenue in 2025. The surge in adoption is supported by municipal initiatives targeting resource optimization, sustainability, and enhanced urban livability. Large city deployments in North America, Europe, and Asia Pacific are using LoRa gateway modules to facilitate connected lighting, intelligent parking, waste management, and integrated public safety networks. Data-driven policies and allocation of urban development budgets are ensuring steady demand for gateway modules, while public-private partnerships support the scaling of LoRaWAN networks in expansive and highly complex metropolitan environments.

Smart metering is expected to be the fastest-growing application, forecast to achieve a CAGR of 21.7% from 2025 to 2032. The momentum is spurred by global mandates for next-generation energy monitoring and water conservation. Utility providers are increasingly retrofitting legacy infrastructure and rolling out advanced metering projects across both developed and emerging economies. The capability of LoRa gateway modules to deliver reliable, long-range, low-power connectivity is propelling widespread adoption, enabling utilities to meet regulatory requirements and unlock significant operational savings. Strategic expansion opportunities exist for vendors and integrators delivering compliance-optimized solutions, scalable analytics, and robust diagnostic features to support large-scale utility networks.

Regional Insights

North America LoRa Gateway Module Market Trends

North America is set to lead by securing an estimated 35% of the LoRa gateway module market share in 2025, with the U.S. driving innovation and deployment scale. Market growth across this region is supported by accelerating smart infrastructure initiatives, federal incentives, and a proven regulatory framework for LPWAN technologies. The Federal Communications Commission (FCC) has provided stability in spectrum allocation, ensuring streamlined network deployments and compliance for utility, municipal, and industrial projects. U.S. market leadership is reinforced by world-class innovation clusters, extensive venture capital flows, and collaborative arrangements between equipment vendors and public sector agencies.

Canada and Mexico are following this trajectory with government-funded smart meter rollouts and environmental monitoring pilot programs. The competitive landscape is increasingly defined by global giants partnered with emerging edge-computing and analytics firms. Growth is additionally buoyed by ongoing expansions into critical infrastructure, particularly in metering and environmental monitoring, resulting in increased investor confidence and resilient long-term demand.

Europe LoRa Gateway Module Market Trends

Europe is slated to command approximately 25% of global market share in 2025, propelled by regulatory harmonization across Germany, the U.K., France, and Spain. The regional market is fueled by comprehensive smart city development, utility modernization, and compliance-driven metering upgrades. Targeted mandates by the European Union (EU) have eliminated major deployment barriers, fostering multi-country rollouts and accelerating market maturity. Germany and France are leading industrial IoT deployments, with substantial investment in manufacturing automation and environmental sensing. The region's open standards and synchronized regulatory environment are reducing entry barriers for mid-sized and specialized technology companies, leading to a competitive marketplace populated by both established leaders and agile new entrants.

Asia Pacific LoRa Gateway Module Market Trends

Asia Pacific is both the fastest-growing regional market and a global capacity leader, capturing approximately 30% market share in 2025 and growing at a forecast CAGR of 16.2% through 2032. China is driving growth with extensive public sector investments, private sector innovation, and sophisticated manufacturing capabilities. Japan and South Korea are implementing advanced factory automation and large-scale utility upgrades, while India and ASEAN economies are focused on agricultural digitization and urban capacity-building. Regional governments are increasingly liberalizing spectrum policy and standardizing technology platforms, although market entry can still be complicated by fragmented band allocations.

Production and export advantages in China, Vietnam, and Malaysia are exerting downward pressure on device costs, encouraging adoption by smaller utilities and municipal agencies. Cross-border partnerships and technology transfer deals are enabling the rapid diffusion of gateway modules and LoRaWAN systems. The competitive environment is marked by the emergence of regional champions, often supported by government R&D programs, and global multinationals, both of whom are investing heavily in urban innovation, utility modernization, and supply chain connectivity.

Competitive Landscape

The global LoRa gateway module market structure is moderately fragmented but demonstrates ongoing consolidation in procurement channels and service offerings. As of 2025, the top five industry leaders – Semtech Corporation, Multi-Tech Systems, RAKwireless, TEKTELIC Communications, and Kerlink – control about two-fifths of the market, while a plethora of regional and niche vendors compete for volume contracts and vertical-specific deployments.

Market concentration is higher in North America and parts of Europe, where established brand trust and advanced product portfolios outweigh incremental cost advantages. Competitive positioning is increasingly determined by solution integration capabilities, vertical expertise, and the ability to support proprietary and open standards concurrently. Edge computing, multi-band support, and flexible orchestration platforms have emerged as differentiators for both regional expansion and tender success.

Key Industry Developments

- In June 2025, RAKwireless launched the WisDuo RAK11160, a $6.50 dual-chip IoT module combining STM32WL LoRa and ESP32-C2 for LoRaWAN, Wi-Fi, and BLE. Optimized for battery life, it supports LoRa 1.0.3 Class A/B/C, remote firmware updates, and dynamic switching between long-range and high-speed connectivity, ideal for farm sensors and vehicle-mounted LoRa gateways.

- In June 2025, Uptake Technologies introduced the first utility meter with direct satellite communication, using LoRaWAN for long-range, low-power data transmission. Designed for remote or hard-to-reach locations, it enables reliable billing and consumption monitoring without terrestrial networks. The solution targets utilities in rural areas, supporting smart water, gas, and electricity metering for compliance and operational efficiency.

- In May 2025, Semtech showcased its fourth-generation LoRa® lineup at IoT Solutions World Congress, unveiling the LoRa Plus™ LR2021 and LoRa Connect™ LR1121. These multi-band transceivers support terrestrial and satellite networks with data rates up to 2.6 Mbps, targeting AI-enabled edge devices. Demonstrations included long-range image transfer, asset tracking, smart-home dual-spreading operation, and energy-harvesting integration for sustainable IoT.

Companies Covered in LoRa Gateway Module Market

- Semtech Corporation

- Multi-Tech Systems, Inc.

- RAKwireless Technology Ltd.

- TEKTELIC Communications Inc.

- Kerlink S.A.

- Microchip Technology Inc.

- Laird Connectivity

- Gemtek Technology Co., Ltd.

- Cisco Systems, Inc.

- EUROTECH S.p.A.

- Orange S.A.

- Dapu Telecom Technology Co. Ltd.

- Link Labs, Inc.

- Advantech Co., Ltd.

- Libelium Comunicaciones Distribuidas S.L.

Frequently Asked Questions

The LoRa gateway module market is projected to reach US$2.0 Billion in 2025.

Rapid digitization across key industries, robust IoT network rollouts, and increasing adoption of smart city infrastructure worldwide are driving the market.

The LoRa gateway module market is poised to witness a CAGR of 12.5% from 2025 to 2032.

Consistently high investments in private and hybrid network deployments, particularly within smart metering and asset tracking, development of cost-effective modules, supportive regulatory frameworks, and innovations in gateway capabilities are key market opportunities.

Semtech Corporation, Multi-Tech Systems, Inc., and RAKwireless Technology Ltd. are some of the key players in the LoRa gateway module market.