- Sensors & Controls

- Automation Instrumentation Market

Automation Instrumentation Market Size, Share, and Growth Forecast, 2026 - 2033

Automation Instrumentation Market by Product Type (Field Instruments, Control Valves, Analytical Instruments), Application (Oil & Gas, Chemicals, Pharmaceuticals, Energy & Power, Food & Beverages, Metals & Mining), Component (Hardware, Software, Services), and Regional Analysis for 2026-2033

Automation Instrumentation Market Share and Trends Analysis

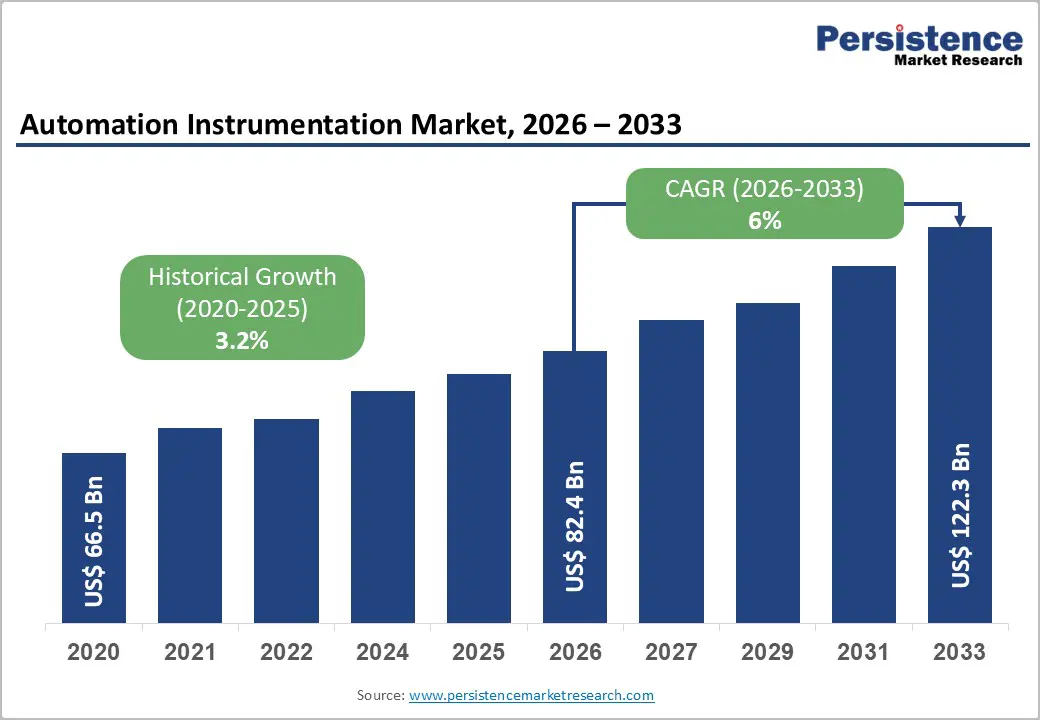

The global automation instrumentation market size is likely to be valued at US$ 82.4 billion in 2026, and is projected to reach US$ 122.3 billion by 2033, growing at a CAGR of 6% during the forecast period 2026−2033.

Market expansion is primarily driven by the rapid adoption of Industry 4.0 technologies across manufacturing sectors, increasing investments in smart factory infrastructure, and stringent regulatory requirements for process optimization and safety compliance. Digital transformation initiatives in process industries, coupled with the proliferation of Internet of Things (IoT) enabled devices, are creating unprecedented demand for advanced automation instrumentation solutions. The convergence of operational technology with information technology is fundamentally reshaping industrial control architectures, while supply chain resilience strategies adopted post-pandemic are accelerating automation investments across critical infrastructure sectors.

Key Industry Highlights

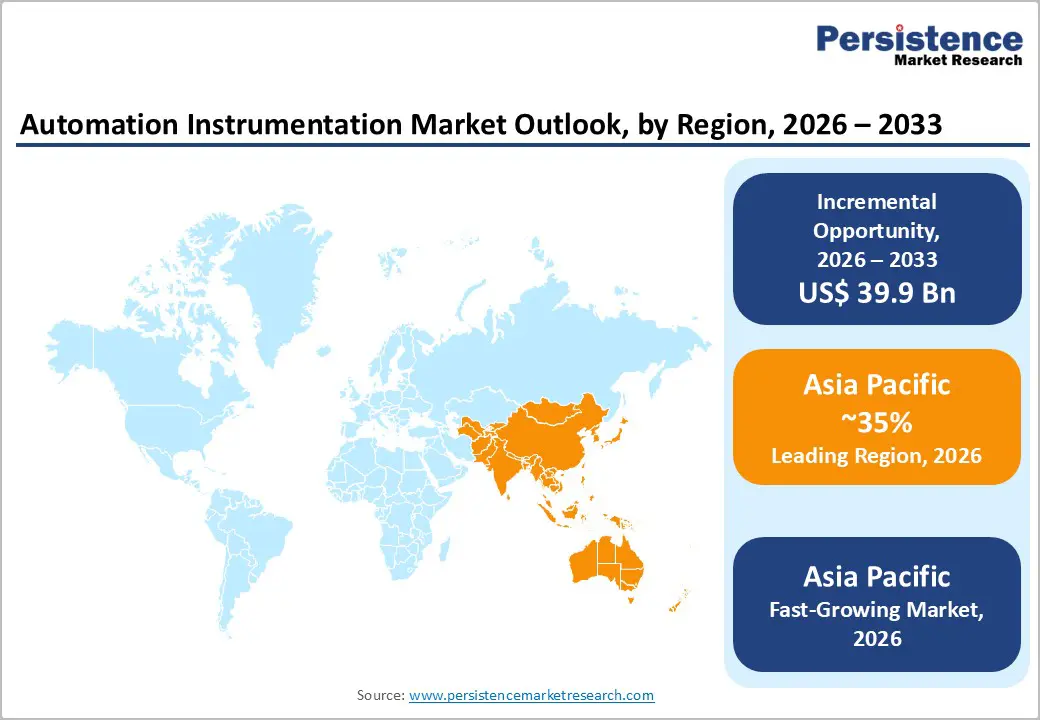

- Regional Dominance: Asia Pacific market likely to be both the leading and fastest-growing regional market through 2033, supported by the robust manufacturing ecosystems of China and India.

- Leading & Fastest-growing Product Type: Field instruments are slated to lead in 2026 with roughly 42%, whereas control valves are likely to be the fastest-growing segment during the 2026-2033 forecast period.

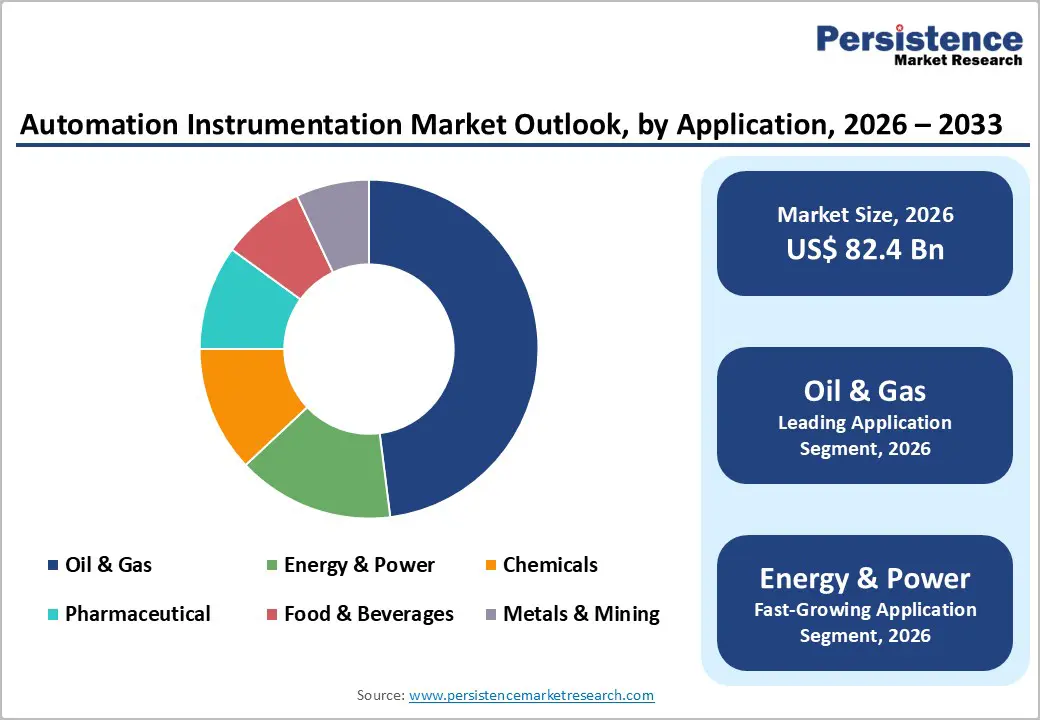

- Leading & Fastest-growing Application: Oil & gas is poised to hold an estimated 48% revenue share in 2026, while energy & power is projected to be the fastest-growing segment through 2033.

- January 2026: Pragmakon AB joined the Nordic engineering group XPartners, strengthening the latter’s capabilities in industrial IT, automation, and electrical engineering.

| Report Attribute | Details |

|---|---|

|

Automation Instrumentation Market Size (2026E) |

US$ 82.4 Bn |

|

Market Value Forecast (2033F) |

US$ 122.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6% |

|

Historical Market Growth (CAGR 2020 to 2025) |

3.2% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Industry 4.0 Adoption and Digital Manufacturing Transformation

The accelerated adoption of Industry 4.0 frameworks is continuing to act as the central force behind market expansion, as manufacturers are increasingly prioritizing digital transformation strategies. Organizations are shifting toward connected and intelligent production environments to remain competitive and resilient. Advanced automation instrumentation is functioning as the backbone of this transition by enabling smart manufacturing capabilities such as predictive maintenance, real time process visibility, and autonomous quality control. These systems are continuously collecting, interpreting, and acting on operational data, which is allowing manufacturers to improve asset utilization and reduce unplanned downtime. As factories are becoming more software driven, instrumentation is playing a critical role in ensuring seamless communication between machines, platforms, and enterprise systems.

Global policy initiatives and sustainability goals are reinforcing long term demand for advanced instrumentation solutions. Government backed programs are actively supporting industrial digitalization, energy efficiency, and intelligent infrastructure development. Smart sensors and automation platforms are helping manufacturers optimize energy usage, enhance production planning, and meet environmental compliance requirements. Investments supported by organizations such as the World Economic Forum (WEF), the International Federation of Robotics (IFR), the U.S. Department of Energy (DOE), and the European Commission (EC) are collectively shaping a future where data-driven manufacturing is becoming the standard.

Energy Efficiency Imperatives and Sustainability Commitments

Corporate sustainability commitments and long-term carbon reduction goals are increasingly shaping industrial investment priorities, and organizations are actively turning to precision instrumentation to enable effective energy optimization. Companies are integrating advanced measurement and control systems to gain deeper visibility into energy consumption across operations. These instruments are continuously supporting initiatives such as real time monitoring, load balancing, and process efficiency improvement. As sustainability strategies are becoming more data driven, precision instrumentation is allowing manufacturers to align operational performance with environmental objectives. Frameworks promoted by institutions such as the International Energy Agency (IEA) and the Science Based Targets initiative (SBTi) are reinforcing the role of accurate measurement in achieving credible and verifiable emissions reductions.

Structured energy management approaches are strengthening demand for robust instrumentation infrastructure. Organizations are increasingly adopting formal systems to standardize energy planning, implementation, and performance tracking. Energy management systems aligned with the International Organization for Standardization (ISO) 50001 standard are requiring comprehensive sensor networks, control devices, and analytics platforms. These solutions are enabling continuous improvement while ensuring regulatory compliance and operational transparency. Supportive programs from bodies such as the U.S. Department of Energy (DOE) are further accelerating adoption by demonstrating clear business value.

High Initial Capital Investment and Integration Complexity

The high upfront capital requirements for comprehensive automation instrumentation systems are continuing to limit adoption, especially among small and medium sized enterprises. Organizations are facing significant financial pressure when planning end to end automation initiatives, as costs are extending beyond equipment purchases into system design and deployment. Integration with existing production infrastructure is increasing complexity, since many facilities are operating with legacy assets that require customization. System integration activities are therefore absorbing a large share of project budgets and timelines. Manufacturers are carefully weighing long term benefits against delayed returns, which is slowing decision making and adoption. Industry bodies such as the National Association of Manufacturers (NAM) are highlighting how financial constraints are shaping automation strategies across smaller enterprises.

In addition to capital investment challenges, operational and organizational requirements are adding further barriers. Advanced instrumentation systems are demanding skilled professionals to handle configuration, calibration, and ongoing maintenance. Companies are investing in workforce development to ensure teams can manage increasingly digital environments. Cybersecurity is also becoming a mandatory component, as connected instrumentation is expanding exposure to operational technology risks. This requirement is increasing project scope and complexity while raising long term support costs. Guidance from organizations such as the Manufacturing Institute is emphasizing the importance of talent readiness and risk management.

Cybersecurity Vulnerabilities and Data Privacy Concerns

The rapid expansion of connected instrumentation devices is continuously increasing exposure to industrial cyber threats and is creating complex risk management challenges. As factories are becoming more interconnected, every sensor, controller, and gateway is adding a potential entry point for malicious activity. The convergence of operational technology and information technology networks is enabling advanced analytics and visibility, yet it is also introducing vulnerabilities that can disrupt production continuity and safety. Agencies such as the Cybersecurity and Infrastructure Security Agency (CISA) are emphasizing that industrial environments now require security by design rather than reactive protection. Organizations are therefore embedding cybersecurity considerations directly into instrumentation planning and deployment processes.

Regulatory and standards compliance is further intensifying security demands. International frameworks such as the International Electrotechnical Commission (IEC) 62443 standard are requiring layered security architectures, continuous monitoring, and strict access controls. Data protection laws such as the General Data Protection Regulation (GDPR) are also imposing rigorous rules on how industrial data is collected, stored, and shared. These requirements are increasing system complexity and operational responsibility. The shortage of skilled professionals is compounding these pressures, as companies are competing for limited industrial cybersecurity expertise.

Artificial Intelligence Integration in Predictive Maintenance

The convergence of advanced instrumentation with AI is creating a transformational pathway for industrial operations and asset management. Manufacturers are increasingly embedding AI algorithms into instrumentation systems to interpret continuous streams of sensor data. These capabilities are enabling predictive maintenance, adaptive control, and early fault detection across production environments. By shifting from reactive responses to anticipatory decision making, organizations are improving equipment reliability and operational continuity. AI-driven insights are also supporting better planning and resource allocation while reducing unnecessary maintenance activity. As confidence grows, AI enabled instrumentation is becoming a core component of modern manufacturing strategies rather than an experimental add on.

Edge computing is accelerating this evolution by bringing intelligence closer to the physical process. Intelligent sensors are increasingly processing data locally, which is reducing latency and improving real time responsiveness. Machine learning (ML) models are continuously optimizing production parameters such as throughput, quality consistency, and energy efficiency. Support from initiatives led by the Department of Defense (DoD) is signaling long term institutional commitment to AI-driven manufacturing advancement. Standards and guidance promoted by the International Society of Automation (ISA) are also supporting responsible adoption. Intelligent instrumentation is rapidly redefining industrial performance by combining measurement, analytics, and autonomous action into a unified operational capability.

Growing Demand for Customized and Application-Specific Solutions

Industries are facing distinct operational, regulatory, and performance requirements, which are driving the need for tailored instrumentation approaches. Manufacturers are increasingly seeking solutions that are aligning precisely with process conditions, safety standards, and quality expectations. Sectors such as pharmaceuticals, food and beverages, and energy and power are requiring specialized instruments that support accuracy, traceability, and compliance. Companies that are actively designing flexible and configurable systems are gaining competitive advantage by solving industry specific challenges. This shift toward customization is also encouraging closer collaboration between technology providers and end users, which is strengthening long term partnerships and accelerating innovation cycles.

Industrial expansion in developing economies is creating a favorable environment for automation instrumentation adoption. Emerging markets are steadily modernizing production facilities to improve efficiency, reliability, and global competitiveness. As industrialization is progressing, organizations are prioritizing automation to address labor constraints and quality consistency. Local governments are also supporting modernization through policy frameworks and infrastructure development. These conditions are creating sustained demand for scalable and cost-effective instrumentation solutions. Automation suppliers are expanding their global footprint by adapting offerings to regional needs while maintaining performance standards. This combination of customization and geographic expansion is shaping a dynamic and resilient growth landscape for the market.

Category-wise Analysis

Product Type Insights

Field instruments are slated to maintain a dominant position with an estimated 42% of the automation instrumentation market revenue share in 2026. This leadership stems from the ubiquitous requirement for sensors and transmitters across all industrial automation applications. Pressure transmitters, temperature sensors, flow meters, and level measurement devices form the foundational layer of process control systems, with facilities typically deploying hundreds to thousands of field instruments depending on complexity. The segment benefits from ongoing replacement cycles, technological upgrades from analog to digital devices, and expansion of monitoring points driven by optimization initiatives.

Control valves are likely to be the fastest-growing segment during the 2026-2033 forecast period. This accelerated growth reflects the transition toward intelligent valve positioners with digital communication protocols, advanced diagnostics capabilities, and integration with asset management systems. Smart valve technologies enable predictive maintenance strategies by monitoring performance parameters including valve travel, supply pressure, and internal diagnostics. The adoption of emergency shutdown valves in safety instrumented systems, mandated by process safety regulations, further drives segment expansion.

Application Insights

Oil & gas is expected to hold the largest portion of the automation instrumentation market share, estimated to reach 48% in 2026. In the oil and gas industry, automation instrumentation plays a critical role in supporting safe, efficient, and reliable operations across extraction, processing, and transportation activities. Companies are increasingly relying on instruments such as flow meters, pressure transmitters, and control valves to monitor conditions and regulate complex processes. These systems are continuously reducing operational risks while improving resource efficiency and production stability. As oil and gas operations are becoming more complex, operators are adopting advanced instrumentation to maintain process control and ensure compliance with strict regulatory requirements. This growing focus on safety, efficiency, and compliance is steadily driving instrumentation adoption across the sector.

Energy & power is projected to be the fastest-growing segment between 2026 and 2033. The energy and power industry is increasingly relying on automation instrumentation to support efficient and reliable power generation and distribution. Operators are using instruments such as flow meters, pressure transmitters, and control valves to continuously monitor system performance and maintain process stability. The growing focus on energy efficiency and the ongoing shift toward renewable energy sources are accelerating the adoption of advanced automation solutions. The deployment of smart grid technologies and the integration of IoT platforms are improving visibility and control across networks. These developments are collectively strengthening the role of automation instrumentation in modern energy and power operations.

Regional Insights

Asia Pacific Automation Instrumentation Market Trends

The Asia Pacific market is likely to be both the leading and fastest-growing regional market for automation instrumentation in 2026, accounting for approximately 35% of the market share. China leads this dominance by holding the largest portion within the region, as its manufacturing prowess drives relentless demand for advanced systems. Japan contributes a strong share through its emphasis on precision engineering, while India gains momentum via government-backed manufacturing pushes. ASEAN countries collectively add vitality, as businesses diversify supply chains and attract foreign investments. Governments across the region actively support this growth through policies that favor industrial development, such as targeted funding and dedicated infrastructure zones.

Manufacturers in Asia Pacific leverage clear advantages, including cost-effective labor, robust supply chains, and close access to vast consumer bases, which solidify the area's role as the world's production hub. Global leaders coexist with regional giants, such as Yokogawa and Azbil, alongside rising Chinese firms that rapidly enhance their technologies. Opportunities abound in modernizing traditional factories, as Industry 4.0 adoption rates remain low, and firms that seize these prospects stand to capture major gains from ongoing digital upgrades across diverse industries.

Europe Automation Instrumentation Market Trends

Europe is set to remain a lucrative market for automation instrumentation through 2033, supported by its advanced manufacturing base and coordinated digital strategy. Countries across the region are actively strengthening industrial competitiveness through smart manufacturing adoption and process modernization. Germany is setting the regional benchmark by advancing connected production models under the Industrie 4.0 framework, which is reinforcing its leadership in high value manufacturing. Other major economies are following differentiated adoption paths that reflect sector specific strengths in areas such as automotive systems, industrial machinery, and precision engineering. This diversity is creating a balanced and resilient regional market structure that is supporting sustained demand for automation instrumentation solutions.

Growth momentum is further accelerating through policy alignment, sustainability objectives, and regulatory consistency across the European Union (EU). Programs such as the Digital Europe Programme are actively supporting industrial digitalization, while climate focused initiatives are driving investments in energy efficiency and process optimization. Energy intensive sectors are increasingly deploying advanced instrumentation to improve productivity while meeting environmental targets. Highly regulated industries such as pharmaceuticals are requiring validated and traceable automation systems, which is supporting premium technology adoption. Harmonized frameworks including the Machinery Directive, ATEX explosive atmospheres regulations, and the Industrial Emissions Directive are simplifying cross border operations.

North America Automation Instrumentation Market Trends

North America is anticipated to play a leading role in brightening the automation instrumentation market outlook during the 2026-2033 forecast period. This is attributable to its strong manufacturing base and a mature innovation ecosystem. The United States is driving regional momentum through early adoption of advanced production technologies and sustained investment in research and development. Manufacturers are increasingly modernizing facilities to support reshoring strategies and improve operational resilience. Policy initiatives encouraging domestic production are accelerating automation uptake as companies are seeking to balance productivity with workforce availability. The presence of established technology providers and specialized integrators is strengthening system deployment capabilities across industries. This environment is enabling faster commercialization of advanced instrumentation while reinforcing long term industrial competitiveness.

Market expansion is also being supported by regulatory requirements and targeted incentives that are encouraging technology adoption. Standards enforced by agencies such as the Environmental Protection Agency (EPA), Occupational Safety and Health Administration (OSHA), and Food and Drug Administration (FDA) are requiring precise monitoring, safety assurance, and process validation. Industries such as chemicals, oil and gas, and pharmaceuticals are relying on automation instrumentation to meet compliance expectations while optimizing performance. Financial mechanisms including tax incentives and research credits are lowering adoption barriers. Manufacturers are prioritizing modernization of aging control systems to improve cybersecurity and data integration. The combination of regulatory alignment, innovation capacity, and infrastructure renewal will propel the North America market into a cohesive growth trajectory through 2033.

Competitive Landscape

The global automation instrumentation market structure is moderately consolidated, dominated by leading players such as Emerson Electric Co, Siemens AG, ABB Ltd., Honeywell International Inc. and Schneider Electric SE. These players collectively capture 40-42% of market share. The automation instrumentation market is highly competitive, with global and regional players actively competing to strengthen their market positions. Companies are continuously pursuing innovation, strategic partnerships, and mergers and acquisitions to broaden product offerings and expand geographic presence.

Market leaders are developing advanced instrumentation solutions that incorporate capabilities such as wireless connectivity, smart sensing, and IoT integration to meet changing industrial requirements. At the same time, sustained investment in research and development is enabling the introduction of technologies that enhance performance, reliability, and operational efficiency. These competitive strategies are collectively accelerating technological progress and shaping a dynamic market environment.

Key Industry Developments

- In January 2026, Thermo Fisher Scientific partnered with NVIDIA to integrate AI directly into scientific instruments and laboratory systems, making workflows more automated and data driven by reducing manual tasks and improving accuracy.

- In December 2025, ABB teamed up with the German Agency for International Cooperation and the Water Authority of Jordan to deploy its Genix™ Industrial IoT (IIoT) and AI Suite across the nation’s water infrastructure to improve efficiency and sustainability.

- In September 2025, Razor Labs collaborated with Process Automation (Pty) Ltd to bring its AI-based predictive maintenance platform, DataMind AI™, to mining and processing operations across South Africa and the surrounding region, combining cutting-edge analytics with local industry expertise.

Companies Covered in Automation Instrumentation Market

- Emerson Electric Co.

- Siemens AG

- ABB Ltd.

- Honeywell International Inc.

- Schneider Electric SE

- Yokogawa Electric Corporation

- Rockwell Automation Inc.

- Endress+Hauser Group

- General Electric Company

- KROHNE Group

- Azbil Corporation

- OMRON Corporation

- Mitsubishi Electric Corporation

- VEGA Grieshaber KG

- Burkert Fluid Control Systems

Frequently Asked Questions

The global automation instrumentation market is projected to reach US$ 82.4 billion in 2026.

Industry 4.0 adoption, IIoT integration, and regulatory demands for safety/efficiency are propelling the market.

The market is poised to witness a CAGR of 6% from 2026 to 2033.

AI predictive analytics, renewable energy monitoring, and emerging market digitalization offer major growth potential.

Emerson Electric Co, Siemens AG, ABB Ltd., Honeywell International Inc. and Schneider Electric SE are some of the key players in the market.