- Medical Devices

- Ischemic Stroke Aspiration Systems Market

Ischemic Stroke Aspiration Systems Market Size, Share, and Growth Forecast, 2026-2033

Ischemic Stroke Aspiration Systems Market by Product Type (Catheters, Pumps, Consumables, Accessories), Application (Acute Stroke, LVO Treatment, ADAPT, Rescue Therapy, AI-Assisted Procedures), End-Use (Hospitals, Ambulatory Surgical Centers (ASCs), Specialty Clinics), and Regional Analysis for 2026-2033

Ischemic Stroke Aspiration Systems Market Share and Trends Analysis

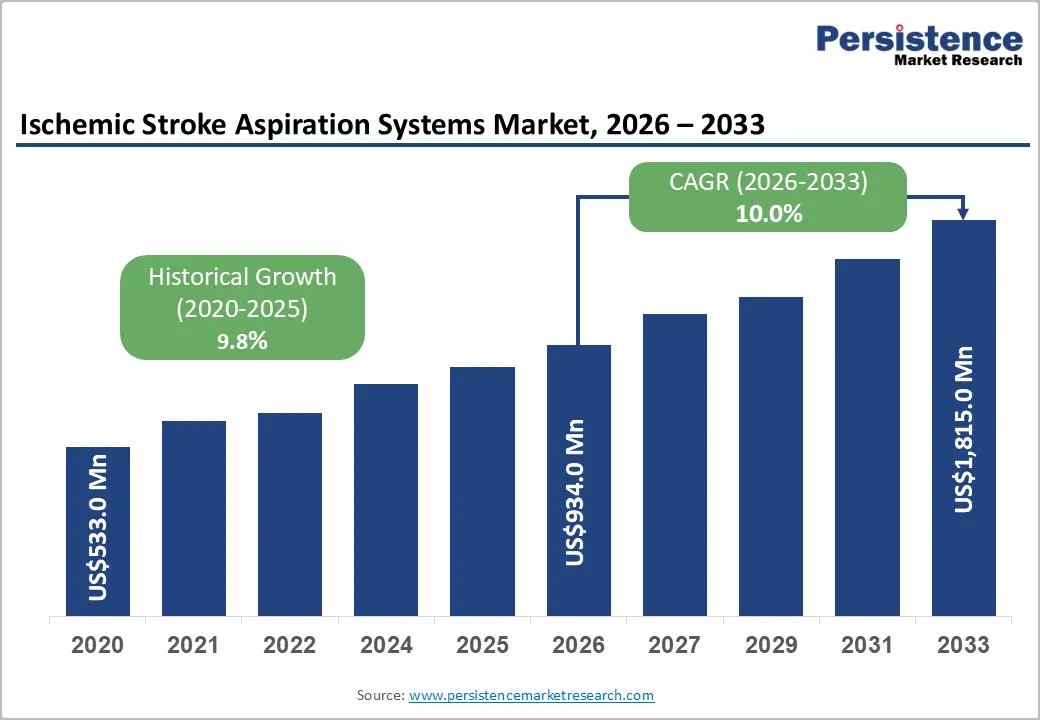

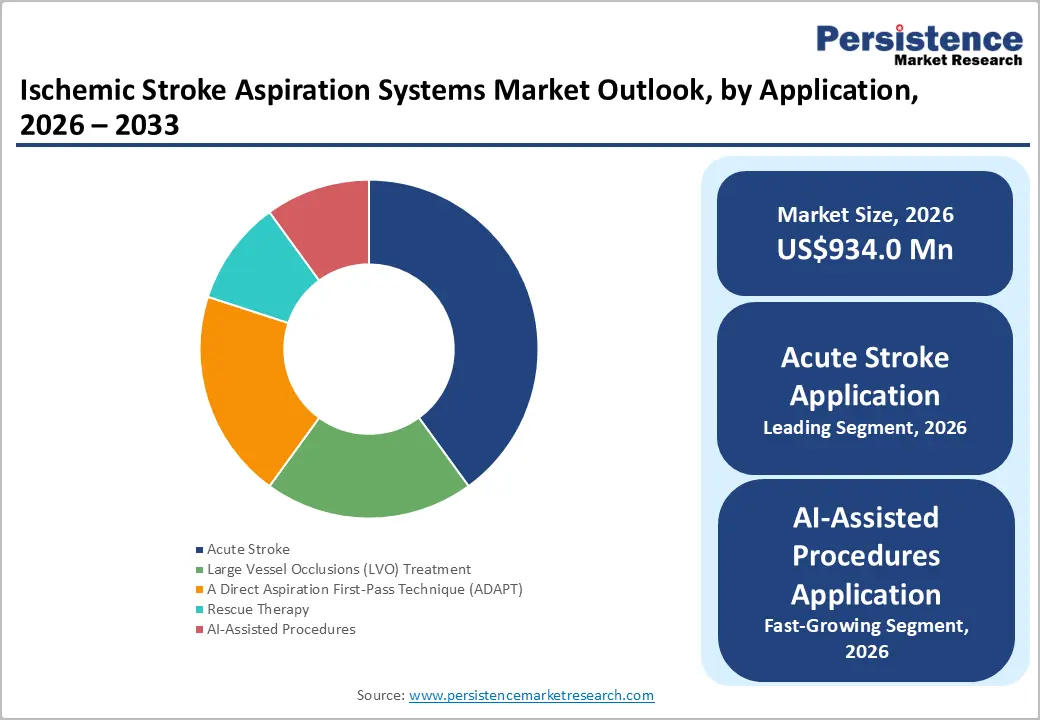

The global ischemic stroke aspiration systems market size is likely to be valued at US$ 934.0 million in 2026, and is projected to reach US$ 1,815.0 million by 2033, growing at a CAGR of 10% during the forecast period 2026–2033. These figures reflect sustained double-digit expansion driven by the rising prevalence of ischemic stroke globally, particularly among aging populations and those with lifestyle-related risk factors such as hypertension, diabetes, and obesity.

Advances in minimally invasive neurovascular procedures, including large-bore aspiration catheters, high-flow pumps, and real-time imaging integration, are improving procedural success rates and reducing intervention times. Healthcare providers are increasingly adopting aspiration-based thrombectomy modalities as standard care for acute stroke management, while public health initiatives emphasize rapid intervention to minimize long-term disability.

Key Industry Highlights

- Dominant Product Types: Catheters are set to command around 42% revenue share in 2026, while pumps are likely to grow the fastest at approximately 12% CAGR through 2033, driven by increasing adoption in advanced neurointerventional procedures.

- Leading Applications: Acute strokes are expected to lead with an estimated 40% share in 2026, while AI-assisted procedures are projected to be the fastest-growing segment at about 14% CAGR during 2026–2033, reflecting procedural efficiency and improved clinical outcomes.

- End-Use Leadership: Hospitals are anticipated to lead with around 60% revenue share in 2026, while ambulatory surgical centers are likely to be the fastest-growing at 11% CAGR from 2026 to 2033, supported by expanding stroke care infrastructure.

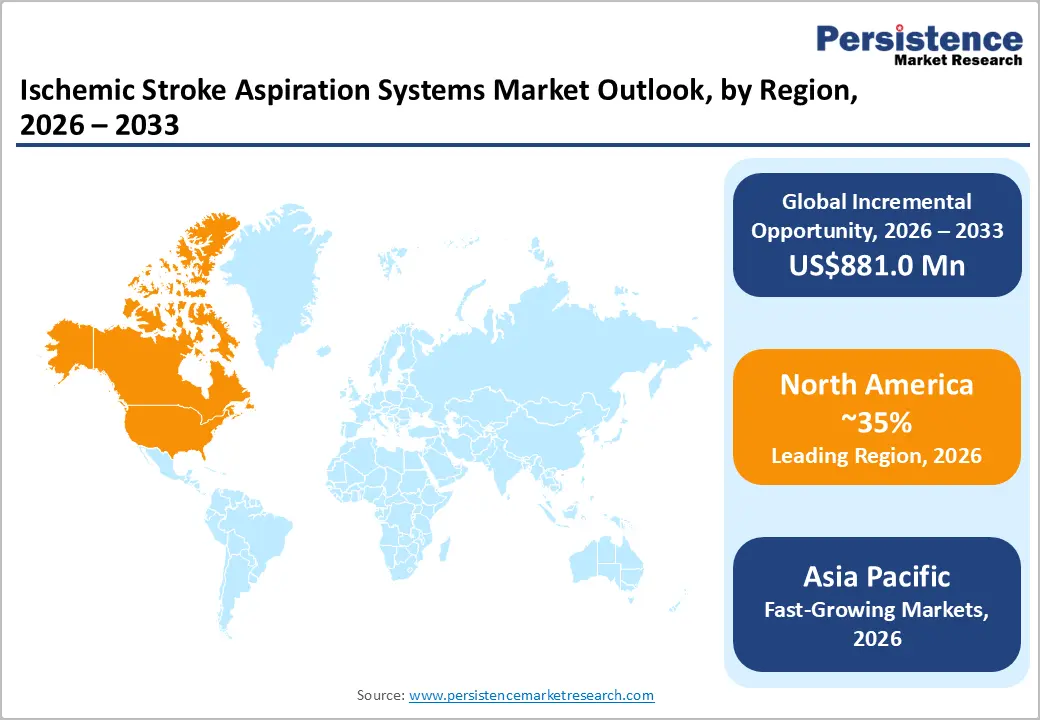

- Regional Leadership: North America is poised to dominate with an estimated 35% share in 2026, while Asia Pacific is projected to register the fastest 2026-2033 growth at approximately 11% CAGR, fueled by rising stroke prevalence.

| Key Insights | Details |

|---|---|

| Ischemic Stroke Aspiration Systems Market Size (2026E) | US$ 934.0 Mn |

| Market Value Forecast (2033F) | US$ 1,815.0 Mn |

| Projected Growth (CAGR 2026 to 2033) | 10% |

| Historical Market Growth (CAGR 2020 to 2025) | 9.8% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Global Burden of Ischemic Stroke and Aging Population

The increasing incidence of ischemic stroke continues to fuel demand for advanced treatment technologies. Stroke remains a leading cause of death and long-term disability globally, especially among aging populations and individuals with comorbid conditions such as hypertension, diabetes, and obesity. As the number of stroke cases rises, healthcare providers are prioritizing early intervention strategies to reduce morbidity and mortality. This trend is propelling demand for aspiration systems that support rapid clot removal in emergency care. Hospitals and specialty clinics are investing in equipment and training to improve procedural efficiency and patient outcomes.

Institutional recognition of improved stroke outcomes is also increasing. In January 2026, the American Heart Association (AHA) and American Stroke Association (ASA) released updated acute ischemic stroke management guidelines that emphasize rapid prehospital identification and transport to thrombectomy-capable centers, underscoring the clinical value of effective intervention technologies in standard care pathways. These guidelines reinforce structured stroke response systems, support broader adoption of aspiration-based procedures, and encourage expansion of stroke-ready infrastructure across hospitals and specialty centers.

Technological Advancements and Improved Stroke Care Infrastructure

Continuous innovation in neurointerventional technology is enhancing the precision and performance of aspiration systems. In early 2026, Johnson & Johnson launched next-generation CEREGLIDE aspiration catheters designed to reach and remove distal clots more effectively, expanding device capabilities crucial for challenging ischemic presentations. This latest device rollout demonstrates industry momentum toward more versatile and clinician-friendly systems that improve procedural success.

The catheters’ enhanced flexibility and improved distal navigation allow clinicians to treat complex vascular anatomies more efficiently, reducing procedure time and potential complications. Such advancements are reinforcing hospitals’ confidence in integrating aspiration-based thrombectomy solutions into standard acute stroke protocols.

In parallel, advancements in artificial intelligence (AI)-enabled imaging platforms are improving decision support and procedural planning. At the 2026 International Stroke Conference, a new AI imaging platform with enhanced diagnostic biomarkers debuted, offering deeper insights into brain injury assessment and informing personalized treatment decisions. Investments in stroke care infrastructure including expanded clinical programs, emergency response networks, and updated care guidelines are strengthening the ecosystem for neurointerventional adoption. These technological and infrastructural developments are collectively accelerating integration of aspiration systems into standard acute stroke workflows and improving overall clinical outcomes.

High Cost of Advanced Aspiration Systems

Despite notable clinical value, the high upfront cost of advanced aspiration systems and related supplies remains a sustained restraint, particularly in resource-constrained healthcare systems. Hospitals, especially in low and middle-income countries, face significant procurement and maintenance expenses for large-bore catheters, high-flow pumps, and AI-enabled accessories. These costs are compounded when reimbursement coverage lags behind clinical advancements, leaving providers to absorb financial strain and limiting broader accessibility in underserved regions. The high cost burden also affects capital allocation for other critical hospital services, creating competing priorities in constrained budgets.

Real-world evidence underscores the financial pressures on providers for thrombectomy-based interventions. Differences in insurance coverage and reimbursement timelines can significantly affect access to advanced stroke care, as recent analyses highlight gaps between procedural costs and payer coverage for high-expense treatments, delaying procurement decisions for cutting-edge technologies. Additionally, variations in government-run healthcare reimbursement models directly shape hospital budgets and influence decisions on capital equipment investment, reinforcing cost as a barrier to widespread adoption.

Regulatory and Compliance Complexity

The stringent regulatory landscape for neurovascular and sophisticated aspiration systems poses a meaningful constraint on market momentum. Major regulatory bodies such as the U.S. Food and Drug Administration (FDA) and Europe Union (EU) Medical Device Regulation (MDR) require rigorous safety and effectiveness data before granting approvals, often extending product time-to-market and increasing development expenditures. These prolonged timelines particularly impact startups and smaller manufacturers with limited regulatory resources.

Comprehensive approval processes and extensive documentation requirements add to development costs and restrict the pace at which innovative devices reach patient care settings.

Recent developments illustrate regulatory pressures in practice. In early 2025, FDA staffing restructuring and workforce reductions were reported to slow the review of high-risk medical devices, with fewer new devices receiving approval compared to prior years, a trend attributed to operational changes within the agency that stretched reviewer capacity and elongated review cycles. These delays highlight how resource constraints within regulatory bodies can translate into slower device commercialization and higher compliance overhead for manufacturers. Bottom of Form

Expansion in Burgeoning Healthcare Markets

The developing economies of Asia Pacific, particularly China, India, and the ASEAN, are rapidly expanding stroke care capabilities due to sustained healthcare investments, improving clinical infrastructure, and broader specialty services adoption. These markets are experiencing accelerated growth in advanced diagnosis and treatment, partly driven by government-level expansion of stroke networks and capacity building in neurology departments. For example, the Indian Stroke Association launched a pilot initiative in Andhra Pradesh in 2026 to strengthen stroke care pathways and develop scalable management models, emphasizing the need for structured acute care delivery.

In addition to infrastructure, local medical innovation is gaining momentum. India’s first homegrown advanced stroke device recently completed a successful clinical trial with outcomes comparable to global standards, demonstrating the potential for domestic, cost-competitive technologies to improve access and lower treatment costs. With rising stroke prevalence, expanding middle-class healthcare demand, and scalable clinical delivery models, aspiration system providers have significant opportunity to tailor cost-effective solutions and partnerships that penetrate underserved and growing regional markets more effectively.

AI and Data-Driven Clinical Decision Support & Care Setting Expansion

Integration of AI and machine learning (ML) into stroke care continues to gain traction as a major opportunity for enhancing clinical decision support and procedural efficiency. Leading health systems are already demonstrating real-world benefits: in England, nationwide deployment of an AI-based imaging tool significantly improved thrombectomy rates and reduced treatment delays, highlighting how AI can accelerate decision pathways and broaden access to advanced care, even outside tertiary centers. These AI-driven tools also provide predictive analytics for patient recovery and risk stratification, helping clinicians make more informed treatment decisions.

As hospitals and specialty centers increasingly adopt these technologies, procedural consistency and outcomes are expected to improve across a wider patient population.

Similarly, public health programs leveraging AI for rapid CT scan analysis and stroke triage, such as those in Punjab that screened hundreds of patients and directly facilitated advanced care, illustrate how AI supports equitable access to high-impact interventions. Beyond hospital walls, this technological momentum aligns with the shift toward ambulatory surgical centers (ASCs) and specialty neurology clinics adopting aspiration systems for non-emergency and staged care, expanding utilization venues, improving cost structures, and meeting rising demand for timely interventions.

Collectively, these developments position AI-enhanced diagnostics and diverse care delivery settings as strategic catalysts for growth in the ischemic stroke aspiration systems market.

Category-wise Analysis

Product Type Insights

Catheters, likely to account for about 42% of the ischemic stroke aspiration systems market revenue share in 2026, set to dominate in 2026 due to their central role in acute ischemic stroke intervention and mechanical thrombectomy, where rapid clot engagement and removal are critical. Hospitals rely on these catheters for prompt reperfusion in large vessel occlusions. In January 2026, Imperative Care launched the Zoom 4S catheter, signaling the adoption of next-generation systems with improved navigation and performance.

Optimized designs, including larger internal diameters and enhanced flexibility, enable more effective thrombus aspiration and shorter intervention times. As stroke centers expand capabilities, catheter use remains entrenched in standard thrombectomy protocols, securing both high revenue share and sustained market relevance.

Pumps are projected to showcase an approximate 12% CAGR during 2026–2033, represent the fastest-growing product type. High-flow electric and portable pumps provide consistent suction, procedural control, and compatibility with AI-enabled navigation systems, meeting rising demands in specialized stroke centers and ambulatory surgical settings. Increasing procedural volumes and standardization of thrombectomy protocols further drive adoption. Recent industry activity shows hospitals investing in pumps to improve efficiency, reduce procedural variability, and enhance clinical outcomes. As these devices integrate with advanced catheters, their adoption trajectory continues to accelerate, reflecting both clinical and operational benefits.

Application Insights

Acute strokes are anticipated to remain the largest application with about 40% market revenue share in 2026, due to its critical role in emergency neurointerventional care. Rapid reperfusion is essential to reduce disability and mortality, making aspiration-based thrombectomy procedures a primary therapeutic approach. In 2026, new guidelines expanded eligibility for endovascular thrombectomy up to 24 hours after symptom onset, increasing procedural volume and reinforcing clinical reliance on these systems. Hospitals integrating these protocols benefit from improved patient outcomes and workflow efficiency, maintaining the segment’s dominant market share and entrenched position in acute care networks globally.

AI-assisted procedures, expected to grow at a 14% CAGR from 2026 to 2033, are the fastest-growing application segment, driven by the integration of artificial intelligence for imaging, procedural guidance, and decision support. In October 2025, the Qure.ai qER-CTA solution received FDA clearance for automated LVO detection, improving early triage and intervention planning. Adoption of AI enhances clinician confidence, reduces procedural complications, and accelerates treatment. Hospitals and specialty centers integrating AI into thrombectomy workflows are seeing measurable efficiency gains, positioning this segment as a high-growth driver and differentiator in purchasing and procedural strategy decisions.

Regional Insights

North America Ischemic Stroke Aspiration Systems Market Trends

North America is poised to lead with an estimated 35% of the ischemic stroke aspiration systems market share in 2026, powered by its advanced healthcare ecosystem and robust clinical protocols for acute stroke care. In the United States, the 2026 update to ischemic stroke management guidelines from the American Stroke Association expanded eligibility for advanced thrombus removal and coordinated emergency services, reinforcing procedural adoption and reimbursement alignment. Comprehensive stroke networks, supported by federal and state funding, ensure rapid identification and intervention, accelerating demand for aspiration systems in major hospitals and tertiary centers.

Strategic partnerships between device makers and hospital networks further support penetration, while government initiatives aimed at reducing stroke mortality and disability expand reimbursement coverage. Investment in clinical training for neurointerventional specialists sustains procedural volumes and ensures operational efficiency. Ongoing adoption of telehealth and real-time data platforms connects paramedics directly with neurologists, improving early triage and prehospital preparedness for thrombectomy procedures. These initiatives enhance access in rural areas and reinforce hospitals’ central role in acute intervention delivery, further entrenching North America as the dominant market with sustained procedural volumes and early technology adoption.

Europe Ischemic Stroke Aspiration Systems Market Trends

Europe represents a mature and stable market for ischemic stroke aspiration systems, driven by harmonized regulations, national stroke care policies, and widespread clinical adoption in Germany, the U.K., France, and Spain. In 2025, England completed a nationwide deployment of an AI-based CT scan analysis tool across all 107 stroke centres, significantly reducing diagnostic delays and expanding the ability to triage patients rapidly for interventions such as thrombectomy. This implementation reflects how European health systems are integrating advanced diagnostics to drive procedural uptake and optimize clinical outcomes across hospitals.

National funding and innovation competitions in the U.K. have provided additional support for stroke care advancement. For instance, a £ 2.5 million U.K. funding initiative awarded to innovations in early stroke detection and rehabilitation accelerates translation of diagnostic tools and supportive technologies into clinical practice. Europe’s structured reimbursement and evidence-based outcome focus help maintain stable growth, even as budgetary constraints in some member states moderate expansion compared to North America.

Cross-border collaborations and shared best practices further strengthen clinical pathways, while ongoing integration of AI and imaging tools in major stroke centers ensures continued procedural efficiency and market stability.

Asia Pacific Ischemic Stroke Aspiration Systems Market Trends

Asia Pacific is projected to be the fastest-growing regional market for ischemic stroke aspiration systems, with an approximate 11% CAGR during the 2026-2033 forecast period, driven by widening access to stroke care, demographic trends, and increased public health focus on early intervention. Governments across the region are actively expanding stroke infrastructure; for example, in India, around 500 operational stroke care units were already established as of early 2025, with plans for further expansion to improve accessibility and outcomes for acute stroke patients. This reflects rising healthcare investment and prioritization of non-communicable disease management across urban and rural areas alike.

The momentum of the market in Asia Pacific is also bolstered by innovative public health applications of stroke technology. In Punjab, India, a government-led AI-driven stroke screening initiative rapidly identified suspected stroke cases and enabled timely referrals for advanced thrombectomy procedures at no cost to patients. Local clinical advancements, such as AI-supported screening and indigenous device trials demonstrating outcomes on par with global standards, are improving early detection, reducing access barriers, and supporting broader adoption of aspiration systems. These combined developments underscore the Asia Pacific market’s dynamic growth trajectory, reflecting unmet clinical needs and aggressive public and private healthcare investment.

Competitive Landscape

The global ischemic stroke aspiration systems market structure is moderately consolidated, with leading players such as Medtronic, Stryker, Johnson & Johnson, and Penumbra collectively accounting for a significant portion of global revenue. These established companies leverage deep relationships with hospitals and stroke centers, regulatory expertise, and integrated neurointerventional device portfolios. Heavy investments in R&D, next-generation catheters, high-flow aspiration pumps, and AI-assisted procedural platforms enable them to maintain technological leadership and meet evolving clinical demands.

Regional and niche competitors, including Imperative Care and Terumo, are focusing on specialized segments such as distal aspiration catheters, portable pumps, and emerging markets in Asia Pacific. Barriers such as regulatory approval, clinical validation requirements, and high device costs limit new entrants, though AI integration and digital imaging software open opportunities for smaller innovators to collaborate with device manufacturers. Market consolidation is expected to continue gradually, driven by strategic acquisitions, product line expansions, and partnerships between device makers and healthcare networks, while software and imaging firms increasingly integrate with hardware solutions to enhance procedural efficiency and patient outcomes.

Key Industry Developments

- In January 2026, Boston Scientific announced a definitive agreement to acquire Penumbra, Inc. for approximately US$ 14.5 billion. The acquisition provides Boston Scientific with a scaled entry into the high-growth mechanical thrombectomy and neurovascular markets, gaining access to Penumbra’s flagship technologies, including the Lightning Bolt and Lightning Flash systems for clot removal.

- In October 2025, Toro Neurovascular entered an exclusive distribution partnership with Kaneka Medical America to expand U.S. access to advanced neurovascular catheters, including the Toro 88 Catheter. The collaboration leverages Kaneka’s distribution network and integrates Toro’s specialized devices with broader neurovascular portfolios, accelerating commercial launch and market penetration.

- In October 2025, Philips and Nicolab strengthened their collaboration to enhance AI-assisted stroke diagnosis and treatment across India. The initiative enables rapid CT analysis, 3D intervention planning, and improved care delivery in both metro and Tier 2/3 cities.

Companies Covered in Ischemic Stroke Aspiration Systems Market

- Penumbra, Inc.

- Medtronic plc

- Stryker Corporation

- Boston Scientific Corporation

- MicroVention Inc.

- Terumo Corporation

- Johnson & Johnson

- Abbott Laboratories

- Imperative Care Inc.

- Acandis GmbH

Frequently Asked Questions

The global ischemic stroke aspiration systems market is projected to reach US$ 934.0 million in 2026.

Growing ischemic stroke prevalence, adoption of minimally invasive thrombectomy, and expanding stroke care infrastructure are driving the market.

The market is poised to witness a CAGR of 10% from 2026 to 2033.

Emerging healthcare markets, AI-assisted procedures, and adoption in ambulatory and specialty care settings present growth opportunities.

Some of the key players in the market include Medtronic, Stryker, Johnson & Johnson, Penumbra, Imperative Care, and Terumo.