- Pharmaceuticals

- Ischemic Optic Neuropathy Treatment Market

Ischemic Optic Neuropathy Treatment Market Size, Share, Growth, and Regional Forecast, 2025 to 2032

Ischemic Optic Neuropathy Treatment Market by Drug Class (Corticosteroids, Antimetabolites, Anticoagulants, Serotonin and Norepinephrine Reuptake Inhibitors (SNRIs), Nonsteroidal Anti-Inflammatory Drugs (NSAIDs), Route of Administration, Indication, Distribution Channel, and Regional Analysis from 2025 to 2032

Ischemic Optic Neuropathy Treatment Market Share and Trends Analysis

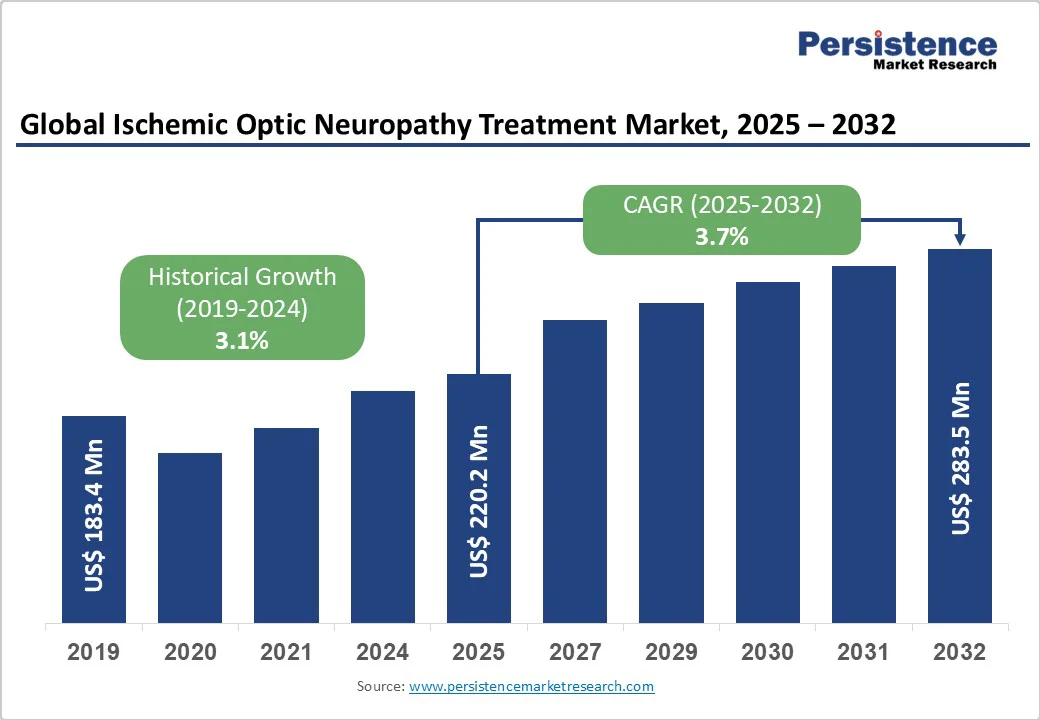

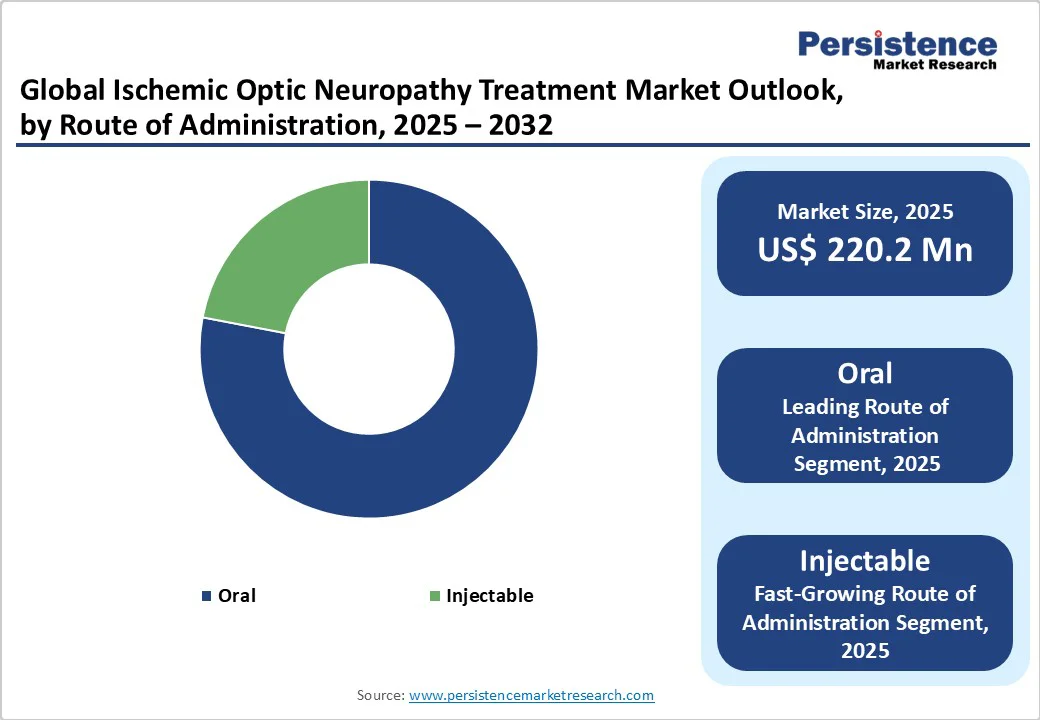

The global ischemic optic neuropathy treatment market size is estimated to reach US$ 220.2 Mn in 2025 and is projected to reach US$ 283.5 Mn by 2032, growing at a CAGR of 3.7% between 2025 and 2032.

The global ischemic optic neuropathy treatment market is witnessing significant growth due to the rising prevalence of optic nerve disorders and increasing awareness of early detection to prevent further vision deterioration.

According to the World Health Organization (WHO), over 2.2 billion people worldwide suffer from visual impairments, underscoring the urgent need for effective therapies.

Key Industry Highlights:

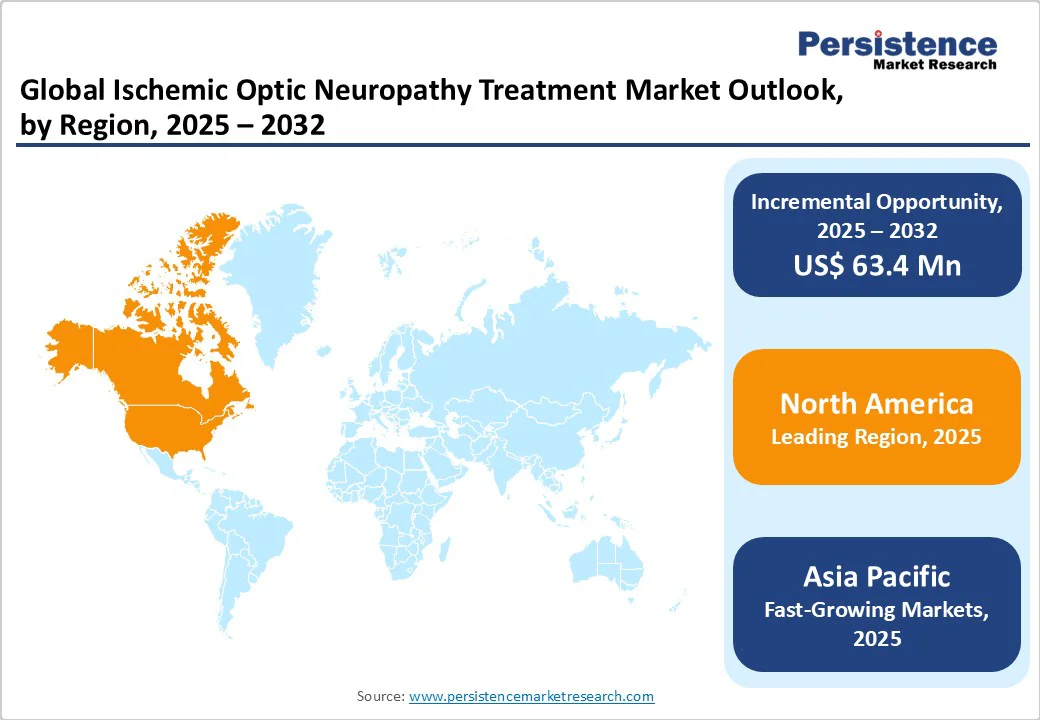

- Leading Region: North America is the top regional market due to advanced healthcare infrastructure and high adoption of innovative therapies.

- Fastest-growth: Asia Pacific shows high growth due to a large patient base, government initiatives, and a rise in treatment awareness. Anticoagulants are expected to lead the drug class segment with a 48.4% value share in 2025 due to high efficacy in preventing blood clots and improving optic nerve perfusion.

- Dominant Route of Administration: Oral administration dominates with 75.6% share in 2025, based on convenience, non-invasiveness, and patient compliance.

- Anterior ischemic optic neuropathy (AION) leads the indication category with 76.8% in 2025 owing to higher prevalence and risk of irreversible vision loss.

- NAION drives clinical demand as the most common acute optic neuropathy in adults over 50.

- Strategic R&D in optic nerve regeneration and gene therapy, shaping innovation and competitive differentiation.

| Key Insights | Details |

|---|---|

| Global Ischemic Optic Neuropathy Treatment Market Size (2025E) | US$ 220.2 Mn |

| Market Value Forecast (2032F) | US$ 283.5 Mn |

| Projected Growth (CAGR 2025 to 2032) | 3.7% |

| Historical Market Growth (CAGR 2019 to 2024) | 3.1% |

Market Dynamics

Driver - Rising Prevalence of Ischemic Optic Neuropathy and Increasing Comorbidities Drive Demand for Effective Treatment

Ischemic optic neuropathy occurs when blood flow to the optic nerve is reduced due to factors such as low blood pressure, increased intraocular pressure, constricted arteries, or impaired perfusion. Conditions like hypoperfusion, autoregulation failure, severe anemia, vasospasm, nocturnal hypotension, and sleep apnea further elevate the risk of developing this condition.

Non-arteritic anterior ischemic optic neuropathy (NAION) is the most common acute form in adults over 50, affecting 2.3-10.3 individuals per 100,000 in the U.S. annually, equating to roughly 6,000 new cases per year. Globally, NAION incidence ranges from 2.3 to 82 per 100,000 person-years, predominantly impacting older adults with systemic risk factors.

Patients often present with decreased visual acuity, visual field defects, and optic nerve swelling. The growing prevalence of NAION, driven by aging populations and increasing comorbidities, is expanding the patient pool and creating a rising demand for effective diagnostic and therapeutic solutions, positioning it as a key driver in the ischemic optic neuropathy treatment market.

Restraints - Limited Efficacy and Safety Concerns of Corticosteroids

Ischemic optic neuropathy continues to be challenging to treat effectively, with corticosteroids often recommended as first-line therapy. Although they offer temporary relief, their significant side effects—including cardiovascular complications, kidney injury, and pulmonary issues-limit widespread use.

These risks reduce patient adherence and hinder long-term treatment outcomes. The inability to provide consistently safe and effective relief underscores the pressing need for alternative therapies, making corticosteroid limitations a key restraint in the ischemic optic neuropathy treatment market.

Lack of Definitive Therapies Creates Market Challenges

Absence of effective treatments as well as emerging safety concerns significantly challenge the global ischemic optic neuropathy market. In June 2025, the World Health Organization (WHO) issued a global alert linking semaglutide medicines to cases of non-arteritic anterior ischemic optic neuropathy (NAION). NAION is a major cause of irreversible adult vision loss and the second most common optic neuropathy after glaucoma.

The European Medicines Agency’s Pharmacovigilance Risk Assessment Committee (PRAC), after reviewing clinical, post-marketing, and literature data, also recommended updating product information and advising immediate discontinuation of semaglutide upon sudden vision loss. These developments underscore the need for safer alternatives and enhanced vigilance, shaping future market dynamics.

Opportunity - Emerging Acute Therapies Present New Opportunities to Improve Outcomes in Ischemic Optic Neuropathy

The absence of an approved acute therapy for ischemic optic neuropathy creates a significant unmet need in the global market. High disease burden of NAION, a common acute optic, often leads to irreversible monocular vision loss and secondary eye involvement in up to 15% of patients within five years creates opportunity for novel interventions.

Clinical studies such as those initiated by Fraser Health in May 2025 evaluate ophthalmic Timolol maleate 0.5% administered within 48 hours of symptom onset in NAION patients. Timolol maleate, a widely used glaucoma medication, has shown potential to enhance optic disc perfusion in preclinical studies. The development of effective acute therapies is likely to transform patient outcomes and open a new growth frontier in the global ischemic optic neuropathy treatment market

Expanding Reach Through Digital and Online Distribution Channels

Growing adoption of e-commerce platforms is improving overall convenience, ensuring timely medication delivery and enhancing treatment adherence by simplifying refills and monitoring. Patients increasingly prefer direct-to-patient access to medications in emerging regions with limited healthcare infrastructure.

Leveraging digital platforms for patient education, support services, and teleconsultation integration by pharmaceutical companies is projected to create significant opportunities in the ischemic optic neuropathy treatment market. This growing shift towards e-pharmacy and digital supply chains enables broader market penetration, particularly in underserved areas.

Category-wise Analysis

Drug Class Analysis

The anticoagulants segment is expected to hold the highest share, around 48.4% of the total drug class segment in 2025, due to their established clinical efficacy, combined with familiarity among physicians. Anticoagulants, including heparin and warfarin, prevent blood clot formation and improve blood flow, addressing a key underlying cause of ischemic optic neuropathy.

Early intervention, particularly within four weeks of symptom onset, helps minimize further optic nerve ischemia and reduce the risk of vision deterioration. High prevalence of vascular comorbidities such as hypertension, diabetes, and atherosclerosis further supports the widespread use of anticoagulants.

On the other hand, corticosteroid drugs, while widely used, face safety limitations, supporting moderate growth. Emerging segments such as SNRIs and NSAIDs benefit from clinical trials and new indications, showing a promising CAGR.

Route of Administration Analysis

Oral route of administration segment is expected to be the dominating segment by 2025 with majority share of 75.6%.

Oral delivery is cost-effective, convenient, and widely preferred due to its non-invasive nature, high patient compliance, and ease of use without requiring a sterile environment. Solid dosage forms such as tablets and capsules also offer improved drug stability and a rapid onset of action.

While oral administration leads the market, injectable formulations are witnessing a higher compound annual growth rate, driven by the development of targeted therapies, faster therapeutic effects, and use in acute or severe cases, reflecting a growing preference for specialized interventions.

Indication Analysis

The anterior ischemic optic neuropathy (AION) segment is anticipated to lead the market by 2025, accounting for approximately 76.8% of the segment share. AION is the most common cause of acute optic neuropathy, particularly in adults over 50, making it highly prevalent in the geriatric population. Its sudden onset and potential for irreversible vision loss drive significant demand for effective treatments.

The higher incidence compared to posterior ischemic optic neuropathy (PION), combined with the clinical focus on early diagnosis and management, contributes to the segment’s dominant market position. PION, although it represents a smaller segment but shows growth potential due to increasing awareness, earlier diagnosis, and emerging therapeutic approaches.

Regional Insights

North America Ischemic Optic Neuropathy Treatment Market Trends

North America ischemic optic neuropathy treatment market is expanding rapidly and is projected to account for 38.9% of the global market share by 2025. The region benefits from a well-established healthcare infrastructure, advanced ophthalmology facilities, and high accessibility to modern diagnostic and treatment options.

Market growth is further supported by favorable reimbursement policies, high per capita income, and strong government initiatives such as Medicare, Medicaid, prescription assistance programs, and glaucoma and macular degeneration support schemes.

Additionally, substantial investment in ophthalmology R&D and increasing awareness among healthcare providers and patients are driving the adoption of innovative therapies. These factors collectively position North America as the largest and most dynamic regional market, with continued expansion expected over the coming years.

Europe Ischemic Optic Neuropathy Treatment Market Trends

Europe is a significant player in the global market, projected to hold a 31.1% share by 2025. Germany, with its advanced healthcare infrastructure and robust research and development (R&D) initiatives, leads the region.

The country has been at the forefront of ophthalmological research, fostering collaborations between academia and industry to develop innovative treatments for eye-related disorders. This emphasis on R&D contributes to higher healthcare expenditures but also drives market growth through the introduction of novel therapies.

The aging population in Germany, as highlighted by the United Nations' World Aging Population report, underscores the increasing demand for effective treatments for age-related conditions like ION. This demographic shift is expected to further propel market expansion in the coming years.

Asia Pacific Ischemic Optic Neuropathy Treatment Market Trends

Asia Pacific region is experiencing rapid growth, driven by strategic alliances, technological advancements, and a large patient population. Countries such as China, Japan, and India are witnessing increased market penetration of key players, leading to greater availability of advanced treatment options.

The region's diverse demographic, encompassing both younger and older populations, presents a broad patient base susceptible to various eye disorders. Government initiatives aimed at improving healthcare access and affordability are further accelerating market growth. Additionally, rising awareness and early diagnosis are contributing to the increased demand for effective treatments across the region.

Competitive Landscape

The global ischemic optic neuropathy treatment landscape is a consolidated market, evolving with a mix of regenerative therapies, gene-based approaches, and pharmacovigilance-driven safety updates. Key players focus on innovation, including optic nerve regeneration and epigenetic therapies, while monitoring drug safety, creating a competitive environment centered on advanced and safer treatment options.

Key Industry Developments:

- In June 2025, the Eye & Ear Foundation highlighted advances in optic nerve regeneration, focusing on challenges in optic neuropathies like glaucoma and ADOA. Researchers discussed emerging strategies to restore optic nerve function and explore regenerative therapies.

- In June 2025, WHO issued a safety alert regarding semaglutide medicines-Ozempic®, Rybelsus®, and Wegovy®-linking their use to a very rare risk of non-arteritic anterior ischemic optic neuropathy (NAION), potentially affecting up to 1 in 10,000 users.

- On September 12, 2024, BioWorld reported on a novel gene therapy utilizing partial epigenetic reprogramming to treat ischemic optic neuropathy (ION). This approach aims to reverse age-related epigenetic changes, promoting cellular rejuvenation. Preclinical studies in glaucoma mice and nonhuman primates demonstrated improved vision and restoration of damaged optic nerve axons, offering potential for treating non-arteritic anterior ischemic optic neuropathy (NAION) and glaucoma.

Companies Covered in Ischemic Optic Neuropathy Treatment Market

- AbbVie Inc.

- Eli Lily Company

- GlaxoSmithKline

- Pfizer Inc.

- Teva Pharmaceuticals USA, Inc.

- Bausch Health Companies Inc.

- F. Hoffmann-La Roche AG

- Bayer AG

- Sanofi A.S.

- Bristol-Myers Squibb and Company

- AdvaCare Pharma

- ANI Pharmaceuticals, Inc.

- Jubilant Cadista Pharmaceuticals Inc.

- Strides Pharma Science Limited

- Boehringer Ingelheim International GmbH

- Amgen Inc.

Frequently Asked Questions

The global market is projected to be valued at US$ 220.2 Mn in 2025.

Rising prevalence of ischemic optic neuropathy, growing elderly population, and increasing adoption of advanced therapies drive the global market.

The global market is poised to witness a CAGR of 3.7% between 2025 and 2032.

Development of novel drug classes, digital/AI-enabled diagnostics, and expansion of online pharmacy channels present key growth opportunities.

Major players in the global are AbbVie Inc., Eli Lily Company, GlaxoSmithKline, Pfizer Inc., Teva Pharmaceuticals USA, Inc. and others.