- Medical Devices

- Interactive Wound Dressing Market

Interactive Wound Dressing Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Interactive Wound Dressing Market by Product (Semi-Permeable Films Dressing, Semi-Permeable Foams Dressing, and Hydrogel Dressing), Application (Chronic Wounds, and Acute Wounds) End-user (Hospitals, Specialty Clinics, Ambulatory Surgery Centers, and Home Care Settings), and Regional Analysis from 2026 to 2033

Interactive Wound Dressing Market Share and Trends Analysis

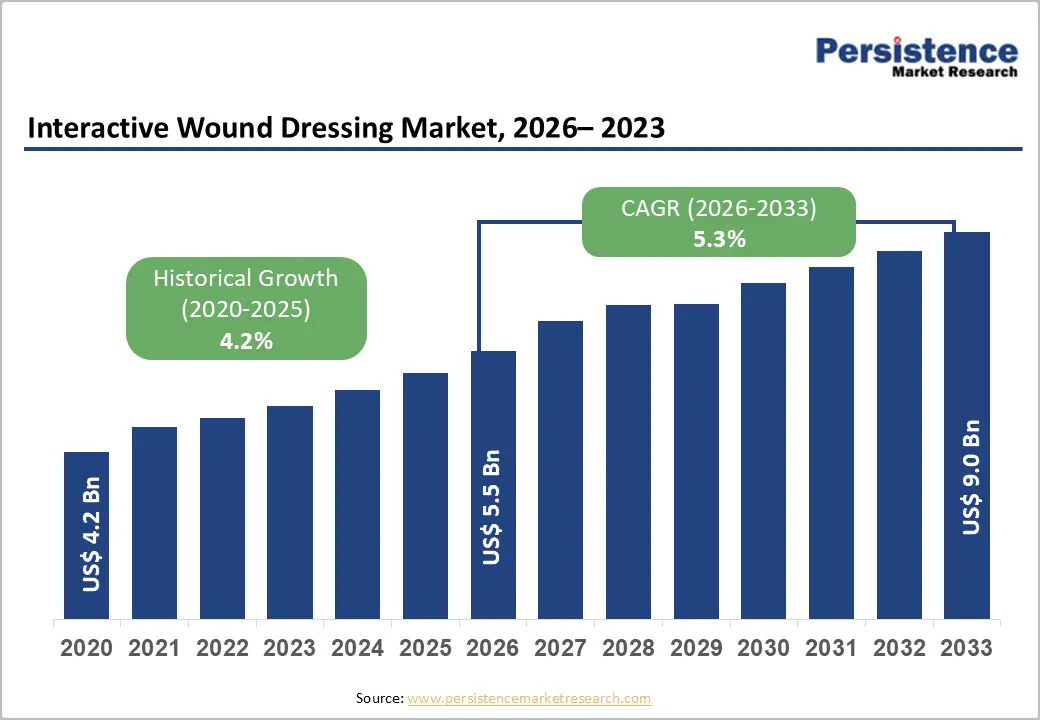

The global interactive wound dressing market size is likely to be valued at US$ 5.5 billion in 2026 to US$ 9.0 billion by 2033 growing at a CAGR of 5.3% during the forecast period from 2026 to 2033.

The global demand for interactive wound dressings is rising rapidly, driven by the increasing prevalence of chronic and acute wounds, growing awareness of advanced wound management solutions, and a strong shift toward minimally invasive and patient-centric care approaches. Rising incidence of diabetes, vascular disorders, pressure ulcers, and post-surgical wounds has significantly increased the need for moisture-balancing, infection-preventive, and healing-accelerating dressings.

Expansion of hospitals, specialty wound care clinics, ambulatory surgery centers, and home healthcare services-combined with higher healthcare spending and improved access to advanced wound therapies-is accelerating market growth. Continuous innovation in semi-permeable foams, films, and hydrogel-based dressings is enhancing exudate management, reducing infection risk, and improving healing outcomes. Additionally, growing adoption of home-based wound care, increased clinician focus on reducing hospital stays, and rising acceptance of advanced dressings in long-term care settings are further propelling market expansion.

Key Industry Highlights:

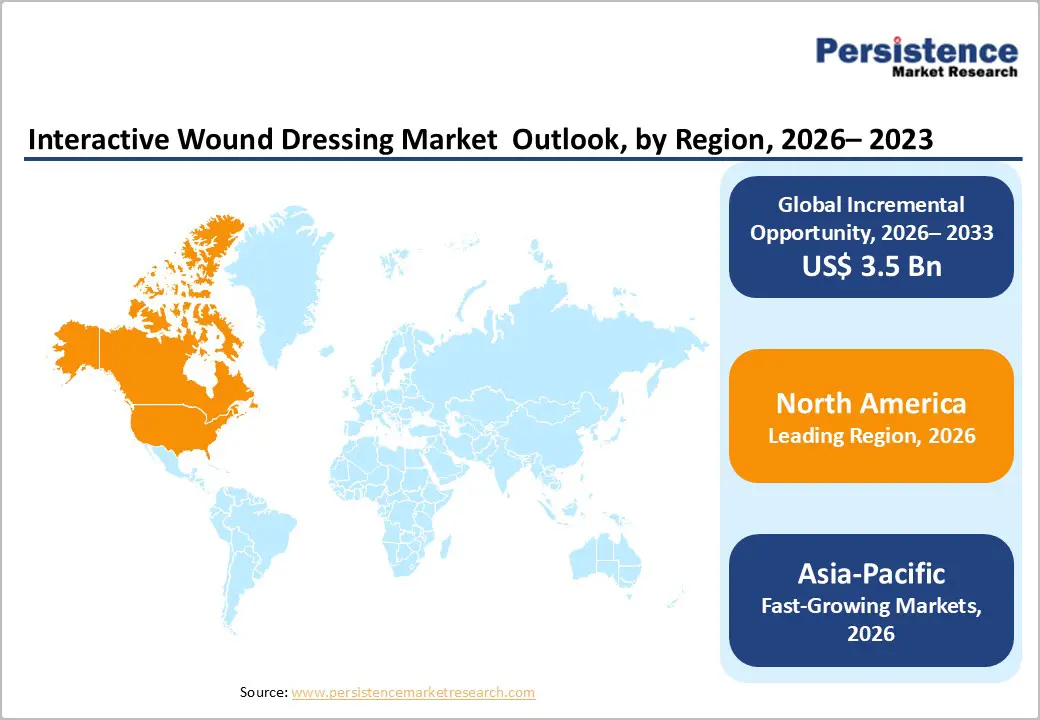

- Leading Region: North America holds the largest share at 47.8%, supported by advanced healthcare infrastructure, high adoption of advanced wound care products, strong reimbursement frameworks, and early uptake of innovative interactive dressings.

- Fastest-Growing Region: Asia Pacific is expanding fastest due to a large and aging patient population, rising prevalence of chronic diseases, rapid expansion of hospital and outpatient infrastructure, and increasing investment in advanced wound management solutions.

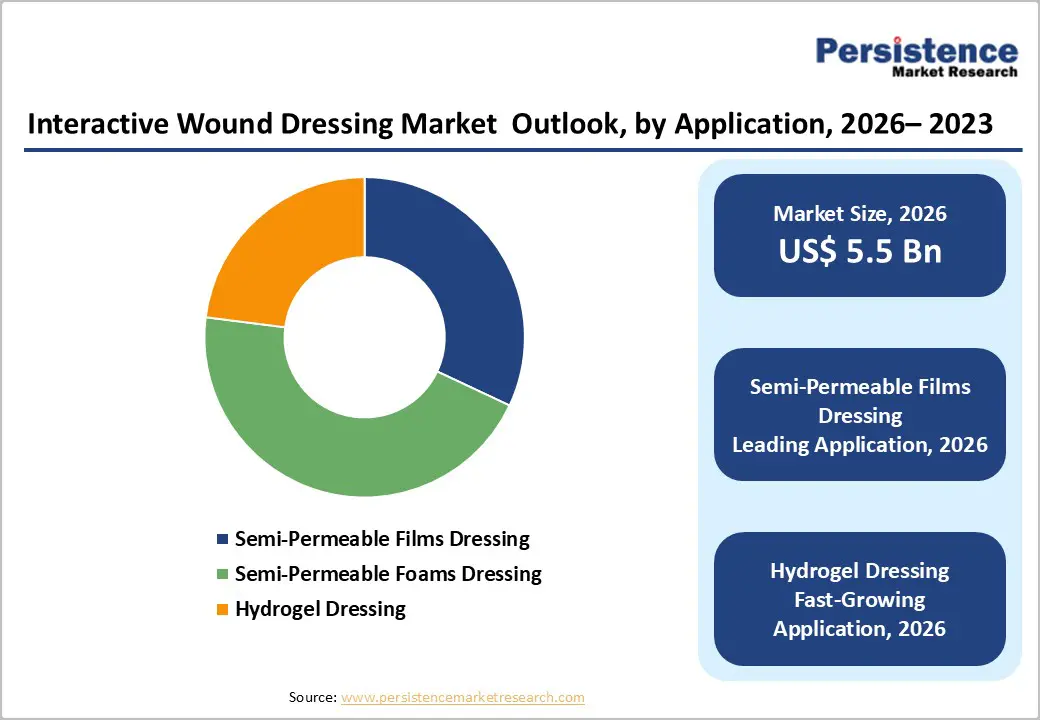

- Leading Product Segment: Semi-permeable foam dressings dominate the market due to their broad applicability across chronic and acute wounds, superior absorbency, moisture control, and suitability for both inpatient and home care settings.

- Fastest-Growing Product Segment: Hydrogel dressings are expanding rapidly as healthcare providers increasingly adopt moisture-retentive solutions for burns, surgical wounds, and chronic ulcers requiring gentle healing environments.

- Leading Application Segment: Chronic wounds remain the top application due to high treatment volumes associated with diabetic foot ulcers, pressure ulcers, and venous leg ulcers, which require prolonged and consistent use of interactive dressings.

- Fastest-Growing Application Segment: Acute wounds are scaling quickly as rising surgical procedures, trauma cases, and post-operative care needs drive demand for advanced dressings that support faster healing and infection prevention.

| Key Insights | Details |

|---|---|

| Interactive Wound Dressing Market Size (2026E) | US$ 5.5 Bn |

| Market Value Forecast (2033F) | US$ 9.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.2% |

Market Dynamics

Driver - Rising Burden of Complex Wounds and Shift toward Advanced Wound Management

The global interactive wound dressing market is being strongly driven by the rising prevalence of chronic wounds and the growing volume of surgical and trauma-related injuries. Increasing incidence of diabetes, obesity, cardiovascular disorders, and an aging population has led to a significant rise in chronic conditions such as diabetic foot ulcers, pressure ulcers, and venous leg ulcers. For instance, in 2024, according to a recently published article, it is estimated that approximately 1-2% of the population in developed countries suffers from chronic wounds at any given time, highlighting the substantial and persistent burden on healthcare systems. These wounds require long-term, consistent care and benefit from interactive dressings that maintain an optimal healing environment, manage exudate, and reduce infection risk. In parallel, the global increase in surgical procedures, road accidents, and trauma cases is expanding the demand for advanced wound care solutions in hospitals, ambulatory surgery centers, and emergency care settings. Post-operative wounds, burns, and traumatic injuries increasingly require dressings that support faster recovery and reduce complication rates.

Additionally, there is a clear shift away from conventional gauze toward advanced and moist wound healing approaches. Clinicians are increasingly adopting moisture-retentive, infection-preventive interactive dressings due to their proven ability to accelerate healing, reduce dressing change frequency, and improve patient comfort. Foam, film, and hydrogel dressings offer superior wound-bed protection, promote granulation tissue formation, and help minimize hospital stays and readmissions. Growing emphasis on evidence-based wound care protocols, improved clinical outcomes, and cost-effective long-term management is further accelerating the replacement of traditional wound care products with advanced interactive dressings across healthcare systems.

Restraints - Cost Barriers and Clinical Usage Challenges Limiting Market Adoption

The high cost of advanced interactive wound dressings remains a key restraint on broader market adoption, particularly in cost-sensitive healthcare systems and low- to middle-income regions. Compared to conventional gauze and basic wound care products, interactive dressings such as foams, films, and hydrogels involve higher manufacturing costs due to advanced materials, antimicrobial components, and extended-wear technologies. These higher prices can strain hospital budgets and limit accessibility in public healthcare systems with constrained reimbursement frameworks. In emerging markets, limited insurance coverage and out-of-pocket payment models further restrict adoption, leading many providers to continue using traditional dressings despite their lower clinical effectiveness. Cost considerations also influence procurement decisions in home care and long-term care settings, slowing penetration of premium wound care solutions.

Moreover, the risk of improper dressing selection and incorrect usage poses a significant challenge to market growth. Interactive wound dressings require careful assessment of wound type, exudate level, infection status, and healing stage to ensure optimal outcomes. Inadequate training or inconsistent clinical protocols can result in suboptimal product selection, delayed healing, or increased risk of complications. Such outcomes may reduce clinician confidence in advanced dressings and discourage widespread adoption. The lack of standardized wound care education across healthcare settings further exacerbates this issue, highlighting the need for improved clinician training and clearer usage guidelines.

Opportunity - Expansion of Home-Based Care and Technological Innovation in Wound Management

The rapid growth of home care and long-term care settings presents a significant opportunity for the interactive wound dressing market. Aging populations, rising prevalence of chronic conditions, and increasing pressure on hospital capacity are driving a shift toward at-home wound management and community-based care. Patients and healthcare providers increasingly prefer treatment approaches that reduce hospital stays, lower overall care costs, and improve quality of life. Interactive wound dressings designed for extended wear, ease of application, and reduced dressing change frequency are well suited for home care environments. These products support consistent healing outcomes while minimizing the need for frequent clinical interventions, making them attractive for elderly patients, caregivers, and home healthcare providers. Expanding reimbursement support for home-based care in developed markets further strengthens this opportunity.

Furthermore, the development of smart and sensor-enabled wound dressings is creating new avenues for product differentiation and value creation. Integration of biosensors, antimicrobial coatings, and digital wound monitoring technologies enables real-time tracking of wound conditions such as moisture levels, temperature, and infection markers. These innovations support earlier intervention, improved clinical decision-making, and reduced complication rates. Digital connectivity with mobile applications and remote monitoring platforms also aligns with the growing adoption of telehealth and remote patient management. As healthcare systems increasingly emphasize outcomes-based care, smart interactive dressings offer strong potential for premium pricing and broader adoption across both clinical and home care settings.

Category-wise Analysis

By Product, Semi-Permeable Foam Dressings Dominate Globally Due to Their Broad Use Across Chronic and Acute Wound Management

The semi-permeable foam dressing segment is projected to dominate the global interactive wound dressing market in 2026, accounting for a revenue share of 45.0%. The segment’s leadership is driven by its widespread use in managing moderate-to-high exudating wounds, including pressure ulcers, diabetic foot ulcers, venous leg ulcers, surgical wounds, and traumatic injuries. Foam dressings offer superior moisture balance, high absorbency, thermal insulation, and protection against external contaminants, making them suitable for both inpatient and outpatient care settings. Their ability to reduce dressing change frequency and minimize maceration supports faster healing and improved patient comfort. Growing adoption of advanced antimicrobial and silicone-border foam variants, along with increasing use in home care and long-term care facilities, is further strengthening segment growth. Continuous product innovation focused on conformability, extended wear time, and infection control continues to reinforce the dominance of foam dressings globally.

By Application, Chronic Wounds Lead the Market Globally Due to Rising Disease Burden and Long-Term Care Needs

The chronic wounds segment is projected to dominate the global interactive wound dressing market in 2026, accounting for a revenue share of 62.0%. This dominance is primarily driven by the rising global prevalence of diabetes, obesity, cardiovascular diseases, and an aging population, all of which contribute significantly to chronic wound incidence. Conditions such as diabetic foot ulcers, pressure ulcers, and venous leg ulcers require prolonged treatment and frequent use of interactive dressings to maintain optimal healing environments. Interactive wound dressings help regulate moisture, reduce infection risk, and promote granulation tissue formation, making them a preferred choice in chronic wound management. Increasing emphasis on early intervention, prevention of complications, and reduction of hospital readmissions is further boosting demand. Additionally, expanding home healthcare services and structured chronic wound care programs are accelerating adoption across healthcare systems.

By End-user, Hospitals Dominate Globally Due to High Patient Volume and Advanced Wound Care Capabilities

The hospitals segment is projected to dominate the global interactive wound dressing market in 2026, accounting for a revenue share of 48.0%. Hospitals manage a high volume of complex and severe wounds, including post-surgical wounds, trauma injuries, burns, and advanced chronic ulcers, which require specialized wound care products and multidisciplinary clinical oversight. Strong access to advanced wound care protocols, trained wound care specialists, and infection control infrastructure supports higher utilization of interactive dressings in hospital settings. Additionally, hospitals are early adopters of advanced antimicrobial and bioactive dressings aimed at reducing healing time and preventing complications. Rising surgical procedures, increasing trauma cases, and growing emphasis on shortening hospital stays through effective wound management further reinforce segment dominance. Integration of standardized wound care pathways and continuous clinician training also contributes to sustained market leadership.

Regional Insights

North America Interactive Wound Dressing Market Trends

The North America interactive wound dressing market is expected to dominate globally with a value share of 47.8% in 2026, led by the U.S. due to its advanced healthcare infrastructure, high wound care spending, and early adoption of technologically advanced wound management solutions. The region benefits from a strong presence of leading manufacturers, well-established distribution and reimbursement frameworks, and widespread availability of trained healthcare professionals across hospitals, outpatient centers, and home care settings. High prevalence of chronic wounds, including diabetic foot ulcers, pressure ulcers, and venous leg ulcers, continues to drive sustained demand for interactive dressings such as semi-permeable films, foams, and hydrogel-based products.

Growing focus on reducing hospital stays and preventing wound infections has accelerated adoption of moisture-balancing and antimicrobial dressings. Favorable reimbursement for advanced wound care therapies, frequent product launches, and a clear regulatory pathway through FDA approvals further support innovation and rapid clinical uptake. Additionally, increasing home healthcare adoption and integration of digital wound monitoring technologies are strengthening market penetration across the region.

Europe Interactive Wound Dressing Market Trends

Europe interactive wound dressing market is expected to grow steadily, supported by rising adoption of advanced wound care technologies, an aging population with a high burden of chronic wounds, and strong focus on evidence-based, minimally invasive treatment approaches. Countries such as Germany, the U.K., France, Italy, and the Nordic region are leading adopters due to well-developed healthcare systems, high clinical awareness, and strong hospital and outpatient care infrastructure. Increasing incidence of diabetes, vascular disorders, and post-surgical wounds is driving demand for moisture-retentive and infection-preventive dressings.

Healthcare systems across Europe emphasize cost-effective wound management, encouraging the use of interactive dressings that support faster healing and reduced complication rates. Regulatory harmonization, broader reimbursement coverage for advanced wound therapies, and integration of wound care protocols within community and home care settings are enhancing market growth. Continuous innovation by regional and global manufacturers, combined with clinician training initiatives and strong academic involvement in wound care research, is further strengthening adoption across the region.

Asia Pacific Interactive Wound Dressing Market Trends

Asia Pacific interactive wound dressing market is expected to register a relatively higher CAGR of around 7.2% between 2026 and 2033, driven by expanding healthcare access, rising prevalence of chronic diseases, and increasing awareness of advanced wound management solutions. Countries such as China, India, Japan, South Korea, and Southeast Asian nations are witnessing growing demand for interactive wound dressings due to rising diabetes incidence, increasing surgical procedures, and rapid expansion of hospital and outpatient infrastructure. Improving affordability and availability of advanced wound care products are accelerating adoption across both urban and semi-urban settings. The shift toward home-based care and community wound management is further supporting demand for easy-to-use, long-wear dressings such as foams and hydrogels.

Government initiatives to strengthen healthcare systems, rising investments in medical education, and expanding presence of global manufacturers through partnerships and local production are contributing to sustained market growth. Additionally, increasing focus on cost-efficient wound healing and infection prevention is driving broader uptake across the region.

Competitive Landscape

The global interactive wound dressing market is highly competitive, with strong participation from companies such as B. Braun SE, 3M, Cardinal Health, Smith+Nephew, Coloplast, and McKesson Medical-Surgical Inc. These players leverage extensive distributor networks, broad advanced wound care portfolios, and continuous innovation in semi-permeable films, foam dressings, hydrogel, and antimicrobial wound care technologies. Growing prevalence of chronic wounds, rising surgical volumes, and increasing demand for moisture-balancing, infection-preventive, and patient-friendly dressings are accelerating adoption across hospitals, specialty clinics, ambulatory surgery centers, and home care settings.

Manufacturers are increasingly focusing on bioactive and antimicrobial formulations, smart and sensor-enabled dressings, and ease-of-use designs that support faster healing and reduced dressing changes. Strategic priorities include expanding product portfolios, enhancing clinical efficacy and patient outcomes, strengthening clinician education programs, improving reimbursement access, and driving broader penetration in outpatient and home healthcare environments.

Key Industry Developments:

- In December 2025, MiMedx signed an exclusive U.S. distribution agreement for RegenKit-Wound Gel, expanding its advanced wound care portfolio and strengthening its presence in the interactive wound dressing market, particularly for chronic and hard-to-heal wounds.

- In July 2025, Convatec received regulatory approval to commercialize a smart wound dressing technology developed to accelerate chronic wound healing. The innovation, known as ConvaNiox, is based on a nitric oxide-releasing mechanism that was developed over seven years with scientific input from UWE Bristol. The technology is designed to enhance healing outcomes in diabetic foot ulcers and represents Convatec’s first product based on this advanced smart dressing platform.

Companies Covered in Interactive Wound Dressing Market

- B. Braun SE

- 3M

- Cardinal Health

- Smith+Nephew

- Coloplast

- McKesson Medical-Surgical Inc.

- Medline

- PAUL HARTMANN AG

- MediWound

- Mölnlycke AB

- Convatec Group PLC

- Lotus

- AVERY DENNISON CORPORATION

- Advanced Medical Solutions Limited

- Others

Frequently Asked Questions

The global interactive wound dressing market is projected to be valued at US$ 5.5 Bn in 2026.

Rising prevalence of chronic wounds and an aging population, coupled with technological advancements in interactive dressings such as moisture control, antimicrobial and smart sensor features are driving global market growth.

The global interactive wound dressing market is poised to witness a CAGR of 5.3% between 2026 and 2033.

Expansion of home healthcare and telemedicine-enabled wound care solutions represents a key growth opportunity.

B. Braun SE, 3M, Cardinal Health, Smith+Nephew, Coloplast McKesson Medical-Surgical Inc., are some of the key players in the interactive wound dressing market.